TL;DR

This paper introduces deep generative semi-supervised Bayesian models for reject inference in credit scoring, aiming to improve classification accuracy by inferring the creditworthiness of rejected applications using efficient stochastic gradient optimization.

Contribution

The paper develops two novel deep generative models that incorporate Gaussian mixture dependencies for reject inference, outperforming classical and alternative models.

Findings

Proposed models achieve higher accuracy in creditworthiness classification.

Models effectively handle large datasets with stochastic gradient optimization.

Experimental results show superior performance over existing methods.

Abstract

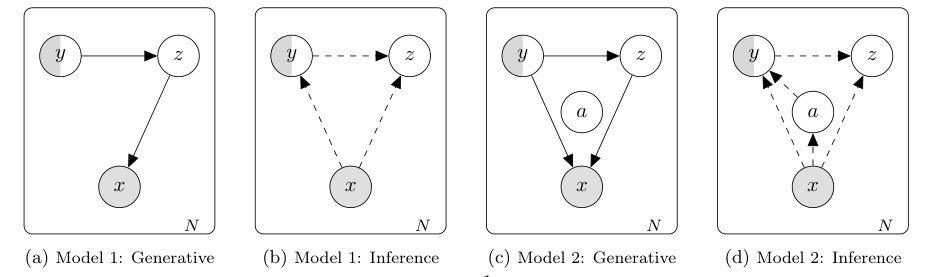

Credit scoring models based on accepted applications may be biased and their consequences can have a statistical and economic impact. Reject inference is the process of attempting to infer the creditworthiness status of the rejected applications. In this research, we use deep generative models to develop two new semi-supervised Bayesian models for reject inference in credit scoring, in which we model the data generating process to be dependent on a Gaussian mixture. The goal is to improve the classification accuracy in credit scoring models by adding reject applications. Our proposed models infer the unknown creditworthiness of the rejected applications by exact enumeration of the two possible outcomes of the loan (default or non-default). The efficient stochastic gradient optimization technique used in deep generative models makes our models suitable for large data sets. Finally, the…

Click any figure to enlarge with its caption.

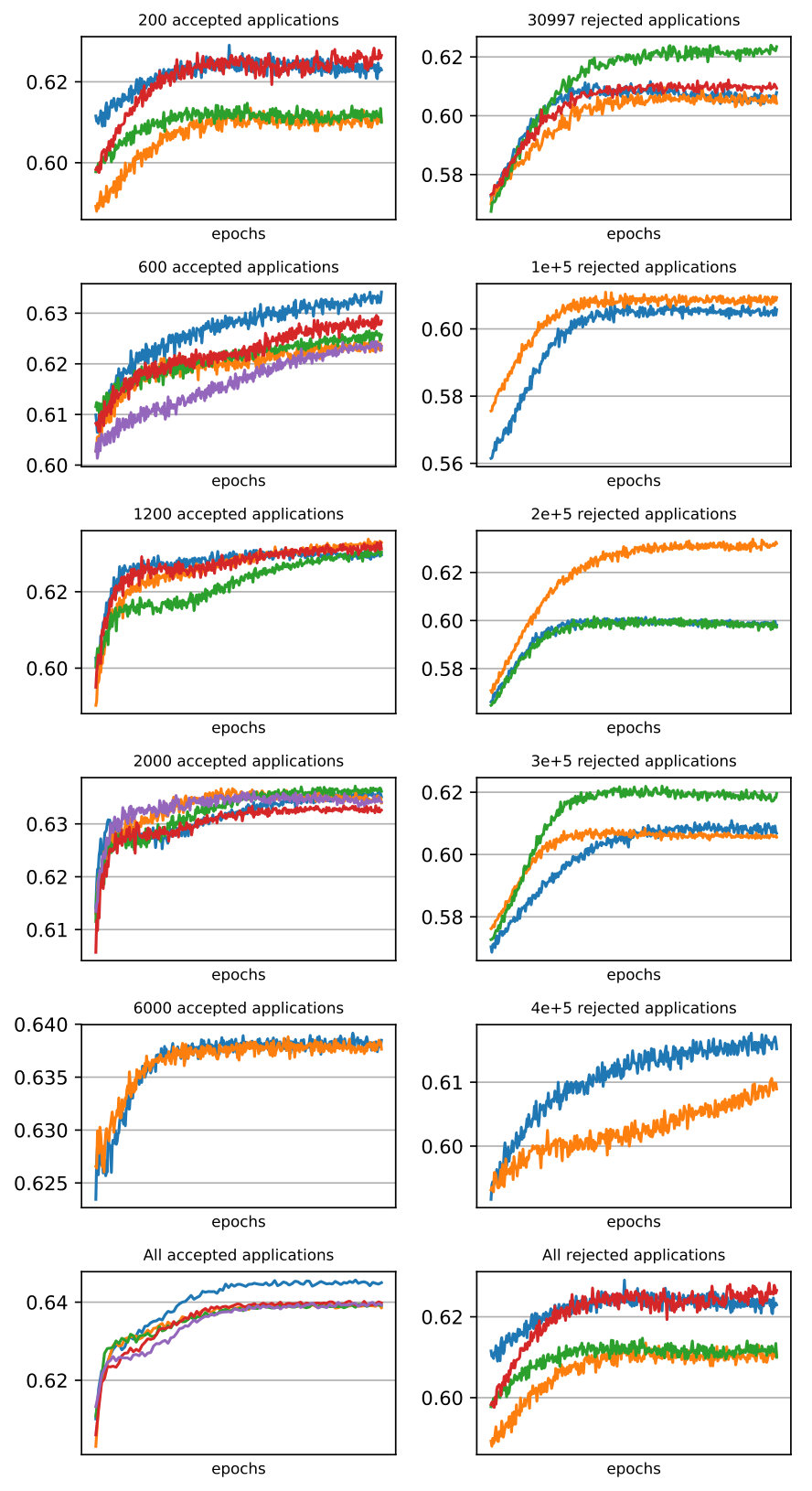

Figure 1

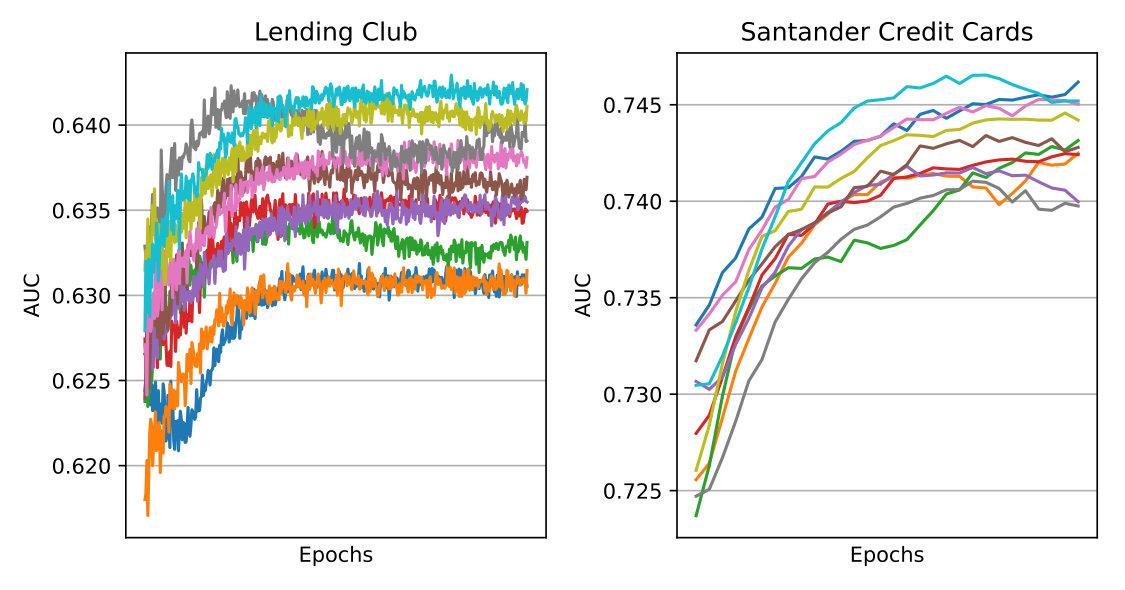

Figure 1 Figure 2

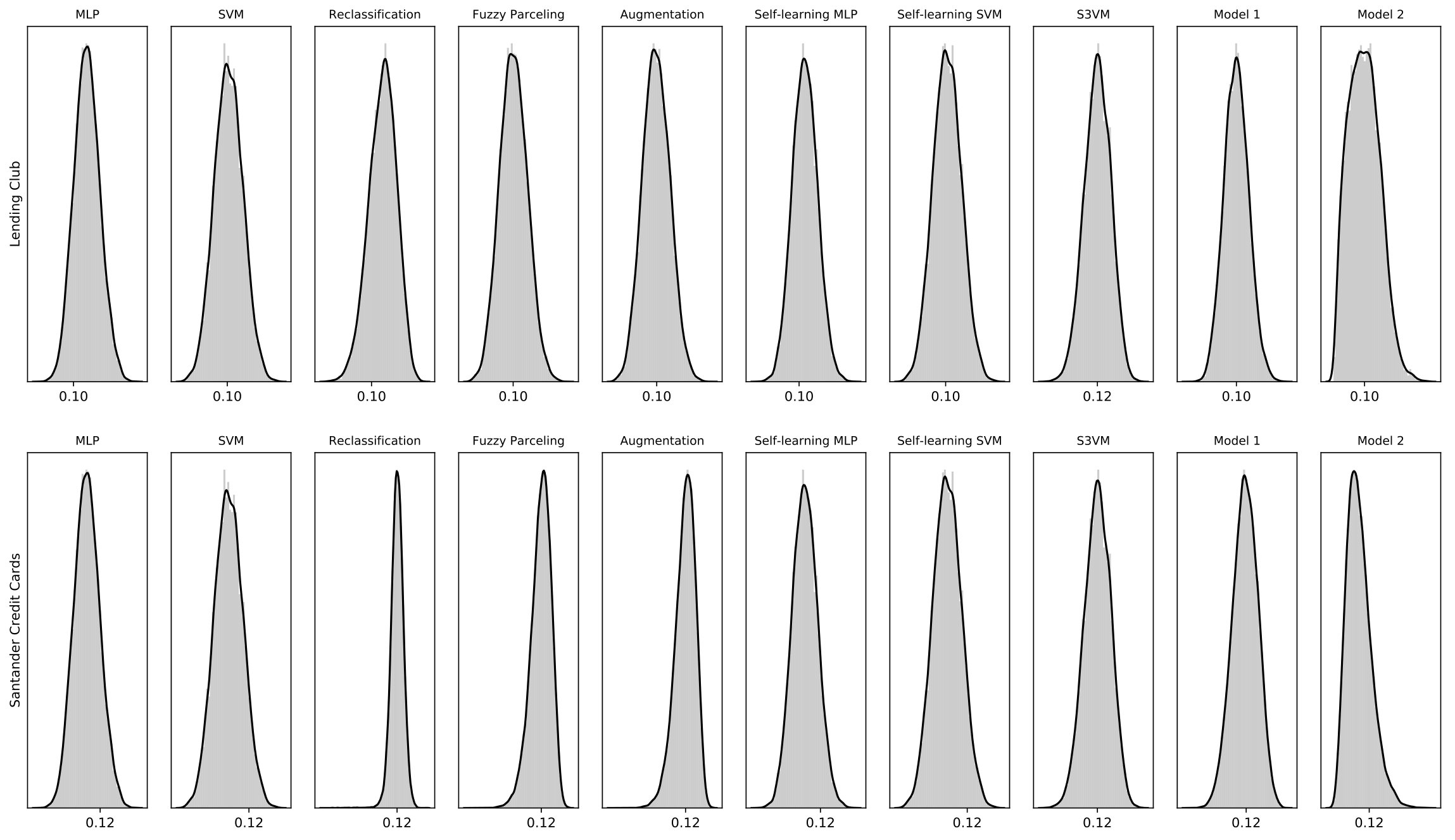

Figure 2 Figure 3

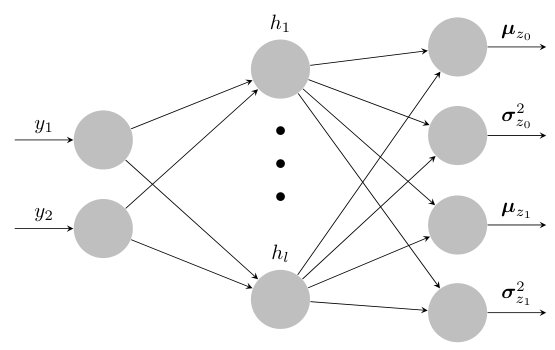

Figure 3 Figure 4

Figure 4 Figure 5

Figure 5Peer Reviews

No public reviews on file for this paper yet. If you reviewed it on a platform where reviews are public (OpenReview, ICLR, NeurIPS, ICML), you can paste yours below so the community can read it here.

Code & Models

Videos

No videos yet. Explain this paper in a talk, walkthrough, or lecture? Add one.