Quasi-Maximum Exponential Likelihood Estimation of Conditional Quantiles for GARCH Models Based on High-Frequency Augmented Data

Zhenming Zhang, Shishun Zhao, Jianhua Cheng, Anze Wang

TL;DR

This paper introduces a new method for estimating risk in financial markets using high-frequency data to improve volatility predictions.

Contribution

The novelty lies in applying quasi-maximum exponential likelihood estimation to high-frequency augmented GARCH models for better conditional quantile estimation.

Findings

High-frequency data improves conditional quantile estimation in GARCH models.

Simulation studies confirm the finite-sample performance of the proposed estimators.

Empirical results show significant improvements in risk measures like Value-at-Risk.

Abstract

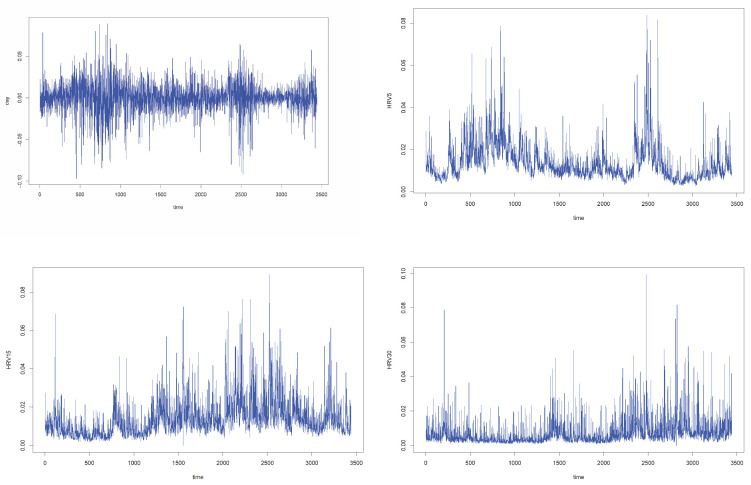

GARCH models play a fundamental role in modeling time-varying volatility in financial return series. In practice, financial returns are also well known to exhibit heavy-tailed distributions, which naturally motivates the use of quasi-maximum exponential likelihood estimation (QMELE) for accurately capturing tail behavior and risk measures such as Value-at-Risk. At the same time, the increasing availability of intraday high-frequency data has led to the development of high-frequency augmented GARCH models, which incorporate intraday information into conventional low-frequency volatility frameworks. By exploiting transaction-level data recorded at very fine time scales, these models are able to capture intraday volatility dynamics and market microstructure effects that are not reflected in standard low-frequency observations. Against this background, this paper studies conditional…

Click any figure to enlarge with its caption.

Figure 1

Figure 1Peer Reviews

No public reviews on file for this paper yet. If you reviewed it on a platform where reviews are public (OpenReview, ICLR, NeurIPS, ICML), you can paste yours below so the community can read it here.

Videos

No videos yet. Explain this paper in a talk, walkthrough, or lecture? Add one.

Taxonomy

TopicsFinancial Risk and Volatility Modeling · Stochastic processes and financial applications · Complex Systems and Time Series Analysis