Assessing the Early Economic Feasibility of a Curative Gene Therapy for Multiple Sclerosis Using a Risk-Adjusted Valuation Framework

Attila Imre, Balázs Nagy, Rok Hren

TL;DR

This study evaluates the economic feasibility of a potential curative gene therapy for multiple sclerosis and finds it unlikely to be commercially viable without significant cost reductions or price increases.

Contribution

The paper introduces a risk-adjusted valuation framework to assess the early economic feasibility of a curative gene therapy for MS.

Findings

Under base-case assumptions, the therapy's net present value is negative, indicating poor financial viability.

Higher treatment prices and lower manufacturing costs are required for positive financial outcomes.

Without external support or cost reductions, commercial development is economically unattractive.

Abstract

Background/Objectives: Multiple sclerosis (MS) imposes a substantial clinical, humanistic, and economic burden, and current disease-modifying therapies require lifelong administration without restoring immune tolerance. IMMUTOL, a tolerogenic gene therapy under development within an EU-funded programme, aims to induce durable remission. Methods: This study assessed the early financial feasibility of IMMUTOL using a structured risk-adjusted net present value (rNPV) model, incorporating development and operating costs, probabilities of clinical and regulatory success, manufacturing expenditure, market dynamics, and revenue projections. Uncertainty was examined through one-way, probabilistic, and scenario analyses. Results: Under base-case assumptions, IMMUTOL generated a deterministic rNPV of −$223.8 million with an internal rate of return of 3.4%. Probabilistic analysis yielded a mean…

Genes, proteins, chemicals, diseases, species, mutations and cell lines named across the full text — each resolved to its canonical identifier and authoritative record.

Click any figure to enlarge with its caption.

Figure 1

Figure 1 Figure 2

Figure 2 Figure 3

Figure 3 Figure 4

Figure 4 Figure 5

Figure 5- —European Union

- —Horizon EU IMMUTOL project

- —Ministry for Culture and Innovation

Peer Reviews

No public reviews on file for this paper yet. If you reviewed it on a platform where reviews are public (OpenReview, ICLR, NeurIPS, ICML), you can paste yours below so the community can read it here.

Videos

No videos yet. Explain this paper in a talk, walkthrough, or lecture? Add one.

Taxonomy

TopicsMultiple Sclerosis Research Studies · Health Systems, Economic Evaluations, Quality of Life · Virus-based gene therapy research

1. Introduction

Multiple sclerosis (MS) is a chronic and progressive immune-mediated neurological disorder that creates a substantial clinical [1,2,3,4,5,6,7,8,9,10,11,12], humanistic [13,14,15,16,17,18], and economic burden [19,20,21,22,23,24,25,26,27,28,29,30,31,32,33,34,35,36,37,38]. Current disease-modifying therapies reduce relapse frequency and delay progression, but they must be administered continually because they do not restore immune tolerance. Their long-term use involves adverse events, adherence challenges, and considerable cumulative cost. In response to these limitations, IMMUTOL, an EU-funded project under Horizon Europe (Grant 101080562), is developing gene therapy to re-establish immune tolerance via genetically enhanced vitamin D3–modified tolerogenic dendritic cells [39,40,41,42,43]. These emerging therapies hold the potential to induce long-lasting remission or even a functional cure in selected populations of patients with MS.

The development of such advanced medical technologies requires long timelines and major investment. Recent analyses show that a complete development cycle from concept to market introduction often requires about 10 years and about 2 billion dollars [44,45,46]. Early economic evaluation is, therefore, essential. Early-stage health technology assessment (eHTA) provides a structured method to estimate the potential price and the risk-adjusted net present value (rNPV) of an investigational therapy. Without explicit valuation models, innovators cannot form a coherent commercial plan and promising technologies may not reach patients [47,48,49,50].

Prior work by Imre et al. (2025) [50] presented an eHTA assessment of IMMUTOL, a novel gene therapy under development for MS, evaluating its potential long-term clinical and economic value using the ErasmusMC/iMTA MS microsimulation model [50,51,52,53,54,55,56]. By comparing IMMUTOL to a broad range of high-efficacy and escalation-based disease-modifying therapy sequences, the analysis shows that IMMUTOL could be cost-effective, and even dominant, at value-based price points up to €200,000, and remained within accepted Dutch willingness-to-pay thresholds at a one-time price of €500,000 under plausible clinical efficacy assumptions. Model scenarios have indicated that substantial reductions in relapse rates and disability progression (IRR ≤ 0.2, RR ≤ 0.1) are required for the therapy to maintain favourable cost-effectiveness [50].

These findings, supported by probabilistic sensitivity analyses showing a high probability of cost-effectiveness, have provided early strategic insight into the pricing, development pathway, and potential health-system impact of curative gene therapies for MS. In fact, health economists at established pharmaceutical companies routinely undertake eHTA analyses to judge the future value of internal development projects and acquisitions. However, due to the confidential nature of such analyses, these models are seldom published [47,48].

The BIO-QLS-Informa analysis of clinical development success rates (2011–2020) has provided a comprehensive evaluation of drug development outcomes, covering 12,728 phase transitions across 9704 programs and 1779 companies. The study reported an overall likelihood of approval (LOA) from Phase I of just 7.9%, confirming the persistent challenge of translating early-stage programs into approved therapies. Phase II, in which proof of efficacy and tolerability need to converge, remained the dominant bottleneck, with only 28.9% of candidates advancing, while disease area, drug modality, biomarker-guided enrolment, and prior target validation emerged as key determinants of success. Notably, for haematology, rare diseases, and advanced modalities—such as chimeric antigen receptor T-cell (CAR-T) and messenger ribonucleic acid (mRNA) therapeutics—demonstrated substantially higher LOAs, whereas solid tumour oncology and prevalent chronic diseases continued to show low success rates. Apparently, the success rate is higher in the development of gene therapies, which may benefit from accelerated regulatory pathways, improved delivery technologies, and clustered regularly interspaced short palindromic repeat (CRISPR)-based precision editing, though still facing challenges related to manufacturing complexity and long-term safety oversight [57].

Sancho-Martinez et al. (2025) [58] argued that traditional corporate finance methods fail to adequately value development-stage biotech companies because such firms lack predictable cash flows and instead derive value from uncertain, future R&D outcomes. The author proposed a layered valuation framework combining rNPV, Monte Carlo simulations, and Real Options Analysis to more accurately reflect the high attrition risk, long time horizons, and regulatory uncertainties endemic to biotech [58].

On an operational level, a structured rNPV presents a pharmaceutical industry standard, with analysis guiding several aspects of commercial planning. It informs the decision to continue or discontinue a project (go/no-go decision), supports the selection of patient groups and indications (market segmentation), and provides a basis for a pricing and payment strategy across indications and regions (payment model). It also arranges the sequence of development and commercial actions that lead to launch or exit. Throughout development, as evidence accumulates, the analysis can be updated.

Although our prior early-stage health technology assessment demonstrated that IMMUTOL could be cost-effective at plausible value-based price points [50], cost-effectiveness alone does not determine whether a development programme is financially viable. Gene therapy development is characterised by high upfront R&D expenditure, long timelines, substantial technical and regulatory risk, and complex manufacturing requirements. Even therapies that generate favourable incremental cost-effectiveness ratios may fail to attract investment if expected returns do not compensate for development risk and capital costs. This tension is particularly relevant in high-prevalence therapeutic areas, such as MS, where competitive standards of care raise the evidentiary requirements and increase development costs. Therefore, a structured financial evaluation that explicitly incorporates probabilities of success, timing of cash flows, discounting, and market dynamics is necessary to determine whether commercial development is economically feasible. The purpose of the present research is to construct such a structured rNPV model for the IMMUTOL gene therapy and to assess its early economic feasibility, assuming curative efficacy in MS.

2. Materials and Methods

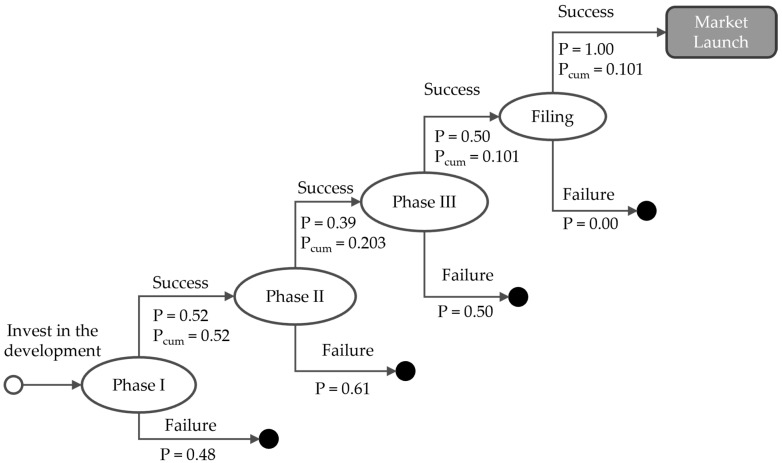

We used an rNPV framework to quantify the expected financial value of the IMMUTOL development programme [59,60,61,62,63]. The rNPV model was constructed in discrete monthly time steps and included the sequence of development costs, post-approval commercial activities, expected revenues, and expected manufacturing and operating expenditures. All financial quantities are expressed as expected values because they depend on the probability that the product progressed successfully through the clinical and regulatory pathway. Figure 1 presents a schematic diagram of the risk-adjusted model during the development phase. After the investment decision is made, there are four decision nodes where there is a probability of success or failure. Also assigned to these points are the necessary costs of development, i.e., funding the trials at different stages and funding market access activities. The cumulative probability of success from the investment decision to market entry is 10.1%.

Expected net cash flow in month was denoted by . Cash flows were discounted to present value using a constant annual discount rate with monthly compounding. The risk-adjusted net present value was defined as

This formulation extended a standard discounted cash flow approach by incorporating explicit probabilities of success for development and regulatory progression. All model parameters (including base-case values and ranges for sensitivity analysis) are detailed in Appendix A.

2.1. Modelling of Market Share

The market share model describes how the share of a new therapy changes over time in a way that reflects diffusion during early adoption and decline as competing products enter the market. The aim is to represent this trajectory with a simple and interpretable function that remains bounded and continuous. Time is measured in years after launch, and market share is written as function .

The model defines four parameters that determine the overall shape. The initial share specifies the market share at launch, denotes peak market share. The time to peak market share specifies the month in which that maximum occurs. The terminal share specifies the long run level after decline. Two rate parameters control the steepness of the curve. The growth rate governs how quickly the product approaches its peak, and the decline rate governs how quickly the product falls from its peak toward its terminal level.

The model expresses the growth phase with an exponential saturation function that rises from to and reaches exactly at . For all the function is:

The model expresses the decline phase with an exponential decay function that begins at and converges to . For all , the function is:

These two equations together produce a continuous function that increases, peaks, and then declines toward a stable level. The parameters can be estimated from empirical data or chosen to match expected adoption patterns, and the resulting function can be used directly in the economic evaluation.

2.2. Uncertainty Analysis

Uncertainty analysis used both one-way sensitivity analysis (OWSA) and probabilistic sensitivity analysis (PSA). In the OWSA, each parameter was varied independently by 10% above and below its base-case value, and the resulting changes in expected net present value were recorded. The ten parameters with the largest absolute effect were summarised in a tornado diagram.

The PSA examined the combined effect of parameter uncertainty. Each uncertain input was assigned a probability distribution, and Monte Carlo sampling drew one value from each distribution for every iteration. These sampled values were passed through the full model to generate a distribution of expected net present values. The PSA used 1000 iterations, which were sufficient to obtain stable estimates of uncertainty in the outputs.

2.3. Scenario Analysis

Scenario analysis evaluated the effect of alternative structural and economic assumptions on projected financial outcomes. Each scenario replaced one or more base-case assumptions with a predefined alternative, and the model was re-run without further changes to inputs or structure. The analysis focused on assumptions judged to be influential for long-term value, including the discount rate, manufacturing costs, market share trajectory, time to marketing authorisation, and combinations of drug price and production cost.

We also assessed a scenario in which the model was not risk-adjusted, meaning all probabilities of success for successive phases were set to 100%. In conjunction with this, because the model was no longer risk-adjusted, higher discount rates between 20% and 30% were applied. For each scenario, the model produced a net present value, an internal rate of return, a payback period when applicable, peak annual sales, and peak annual patient numbers. The decision criterion remained the same across all scenarios: a net present value above zero indicated a go decision, and a net present value at or below zero indicated a no-go decision.

3. Results

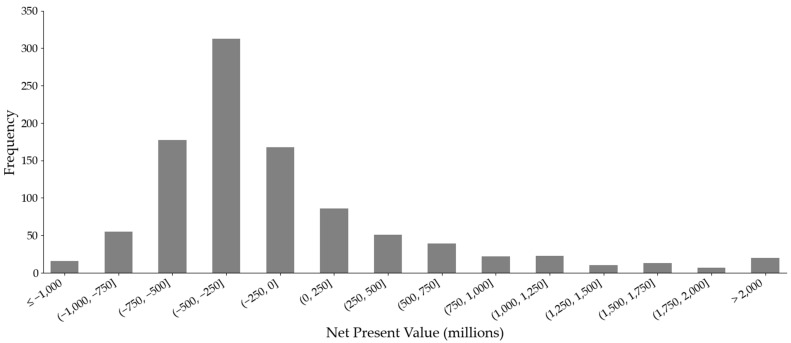

Under base-case assumptions (detailed in Appendix A), the IMMUTOL programme generated a negative financial outcome. The deterministic rNPV was −99.4 million and a 10.5% mean internal rate of return. The difference is the consequence of a positively skewed distribution of NPVs. Most iterations (72.9%) produced negative values, while a smaller set of draws combining favourable economic and technical parameters yielded high positive outliers, with some rNPV values above $2 billion.

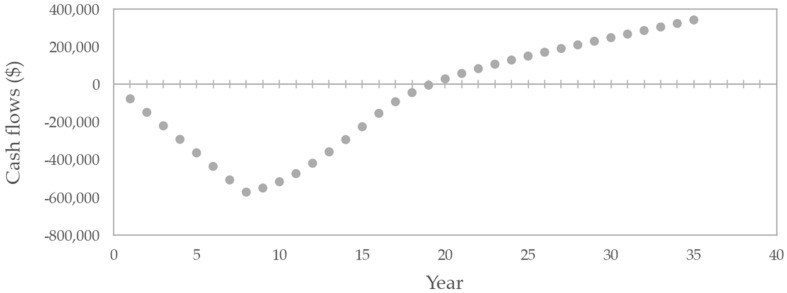

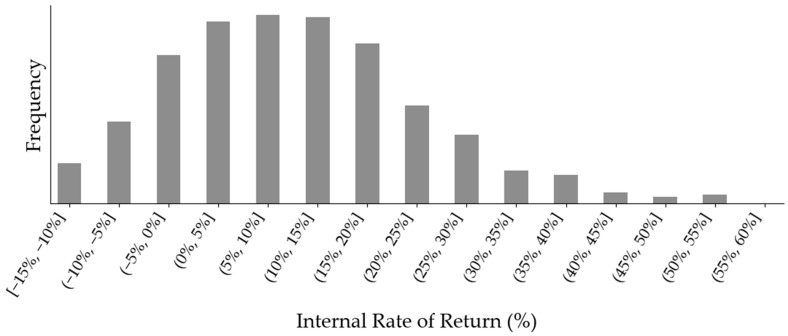

Across all Monte Carlo iterations, 729 of 1000 (72.9%) resulted in rNPV values below zero (Figure 2). The distribution concentrated in the negative region, although a long, right-hand tail was present. The project did not recover its investment within the model horizon under base-case discounting. The cumulative undiscounted cash flow curve in Figure 3 shows that total cash flows became positive only after year 19 from the model’s start. Peak annual sales reached $217.5 million, corresponding to 4730 patients in the peak year. Figure 4 presents a histogram of the probabilistic internal rate of return calculations. Overall, 43.8% of iterations produced a positive internal rate of return.

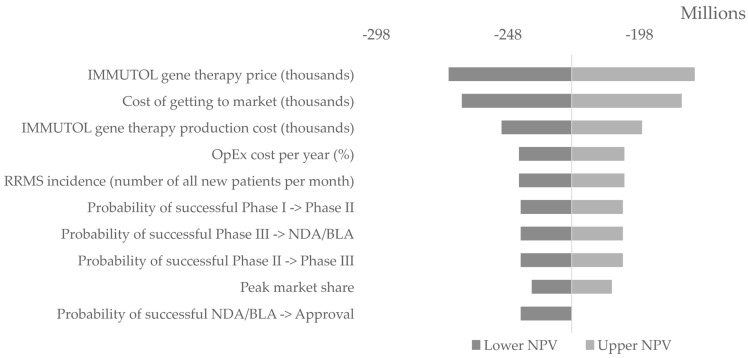

The OWSA varied each parameter by 10% around its base-case value. Treatment price was the most influential driver, with an rNPV swing of 83.6 million. Production cost per treatment produced a 40.1 million. The three probabilities of successful transition between clinical phases each generated a 30.4 million swing. Figure 5 displays the tornado plot ranking and magnitude of these effects.

Scenario analysis examined structural changes to key assumptions (Table 1). Removing discounting generated a positive NPV of 1.5 million and a production cost of 711.2 million.

The scenarios without risk adjustment evaluated cases in which all probabilities of success were set to 100% and discount rates were increased to 20–30%. At a 30% discount rate, the model produced an NPV of –55.3 million and 2.17 billion.

4. Discussion

This analysis evaluated the financial viability of developing the IMMUTOL tolerogenic gene therapy using an rNPV framework. Under base-case assumptions, the programme did not generate positive value. The deterministic rNPV was negative, and the probabilistic analysis showed that 70.2% of simulations also produced negative values. The internal rate of return remained below levels typically sought by private investors in risky biotechnology development. Taken together, the results indicate that, given current expectations about costs and risks, the programme is unlikely to be financially attractive.

A central finding is the gap between a value-based price and the price required for commercial viability. Previous work estimated a value-based price below approximately 1 million and manufacturing cost fell to, or below, $200,000. This difference cannot be closed through plausible changes in uptake, eligible population, or incremental reductions in production cost. The implication is that the price that reflects health-system value is substantially lower than the price needed to attract private investment, and this gap limits the feasibility of commercial development [64,65,66,67,68,69,70,71,72,73].

A broader policy context may help interpret these findings. Many health systems are grappling with how to reimburse one-time, high-cost curative therapies while maintaining budget sustainability [74,75,76,77,78,79,80,81,82]. Current reimbursement frameworks, largely based on upfront payment, may not align with the risk profile or societal value of tolerogenic gene therapies. Alternative payment models (e.g., outcomes-based annuities [83], risk-sharing schemes, or publicly supported development funds) could narrow the gap between value-based prices and required commercial prices; however, these mechanisms remain limited in scope, inconsistently applied across jurisdictions. While this analysis does not prescribe policy responses, it indicates that, without external intervention or changes in development costs, economic incentives may be insufficient to support continued development.

The model’s second most influential parameter was the cost of development through market approval. Although a figure of approximately $600 million aligns with published estimates, an argument could be made that tolerogenic gene therapies might achieve approval with smaller trial programmes. However, for a high-prevalence disease where multiple treatments are available, such as multiple sclerosis, regulators would likely require larger, comparative Phase III trials powered to detect clinically statistically significant differences against the current standard of care. Power calculations under these conditions yield enrolment numbers far higher than those of typical gene therapy studies. Consequently, even though gene therapies are sometimes approved on limited datasets for ultra-rare conditions, such precedents do not readily generalise to a large, competitive therapeutic area. This would limit the extent to which development costs could realistically fall, even under optimistic assumptions.

Due to these findings, several alternative development strategies merit consideration. One option is to focus on rare indications with high unmet need and limited (or no) existing treatments. These settings often permit smaller trials, shorter follow-up, and higher economically justifiable prices. The early modelling exercise for relapsing–remitting MS remains informative in this context. Without an explicit financial model for a large indication, it would not be clear that a niche indication offers a more credible financial path. The finding that the IMMUTOL gene therapy is unlikely to be viable in a mainstream indication, therefore, clarifies why a “niche-buster” approach may be appropriate [84,85,86].

A second strategy is to sequence patients by concentrating development in subgroups with limited response to current therapies. Treatment-resistant or rapidly progressing forms of MS fit this profile. A related method is staged expansion, in which development begins in a refractory subgroup or in a population identified by validated biomarkers. Broader phenotypes follow once safety and activity are established. These staged programmes could meet regulatory expectations with smaller studies for early label expansions, which reduces financial risk.

Other strategies may aim to share financial risk. Partnerships or licensing agreements during development can transfer substantial downstream costs to a partner with the capacity to complete late-stage trials and commercialisation. These arrangements are common in advanced therapy development and can temper the late-stage risks (and associated negative NPV) in the present model.

The present analysis shows the value of early health economic modelling in the development of investigational medical products, specifically gene therapy. The same approach can be applied to other pharmaceuticals, medical devices, and investigational diagnostic modalities [87,88,89,90,91,92]. Early modelling can identify development directions that are unlikely to be economically viable, and can help redirect strategies towards justifiable directions. In this role, the model functions as a decision-supporting tool that guides whether development should continue and in what form.

Several non-commercial development pathways also merit consideration. Public–private partnerships and nonprofit development structures have supported vaccine development and research in neglected diseases [85,86,93]. These arrangements can sustain programmes that have substantial clinical value but limited commercial appeal. The results of this analysis suggest that such pathways may be relevant for tolerogenic therapy in multiple sclerosis.

The study applies eHTA methods to a publicly funded research programme, uses fully disclosed parameter inputs, and reports the mathematical specification of its market-share function. It includes one-way, probabilistic, and scenario-based sensitivity analyses, allowing a systematic assessment of parameter uncertainty; these elements improve transparency and reproducibility.

However, the analysis also has limitations. Many inputs rely on the literature estimates or expert judgement, which introduces uncertainty that could only partially be quantified. Manufacturing costs, remission rates, and long-run market dynamics for tolerogenic gene therapies remain uncertain at this stage of development. The competitive landscape over a decade or longer could change substantially from current assumptions. The model, therefore, provides an early estimate that requires revision as information and empirical evidence accumulate. Future research would benefit from greater transparency in reporting NPV models for advanced therapies. These models are widely used in industry but are rarely published, which limits methodological development and comparative assessment. A more complete collection of the academic literature would support public funding decisions, improve comparability across studies, and clarify the extent to which financial feasibility aligns with clinical or societal value.

This study has identified economic constraints that limit the feasibility of commercial development. These constraints do not imply a lack of clinical promise. They indicate that current structures produce a gap between social value and financial return. As programme-specific clinical data become available, updating the model will allow a more accurate assessment of feasibility and inform decisions about whether to proceed with development. Another aspect that has, until recently, been largely overlooked is the role of patient and public involvement in health technology assessment [94,95]. Integrating patient perspectives more effectively across the development process can strengthen methodological quality, ensure alignment with patient needs, and enhance the broader societal relevance of the work.

5. Conclusions

The results indicate that profitability of investing in the development of the IMMUTOL therapy strongly depends on price and manufacturing cost, rather than on time to market or patient reach. Although a lower price of IMMUTOL could improve access, there is a high probability that it would not be economically sustainable. The combination of factors, such as high production costs inherent to gene therapy manufacturing and a crowded drug market with already effective therapies, can limit profitability even under optimistic, large-scale uptake scenarios.

The reference list from the paper itself. Each links out to its DOI / PubMed record.

- 1Claflin S.B. Tan B. Taylor B.V. The Long-Term Effects of Disease Modifying Therapies on Disability in People Living with Multiple Sclerosis: A Systematic Review and Meta-Analysis Mult. Scler. Relat. Disord.20193610137410.1016/j.msard.2019.08.01631450158 · doi ↗ · pubmed ↗

- 2Cruz Rivera S. Aiyegbusi O.L. Piani Meier D. Dunne A. Harlow D.E. Henke C. Kamudoni P. Calvert M.J. The Effect of Disease Modifying Therapies on Fatigue in Multiple Sclerosis Mult. Scler. Relat. Disord.20237910506510.1016/j.msard.2023.10506537839365 · doi ↗ · pubmed ↗

- 3Dang Y.L. Yong V.T. Sharmin S. Perucca P. Kalincik T. Seizure Risk in Multiple Sclerosis Patients Treated with Disease-Modifying Therapy: A Systematic Review and Network Meta-Analysis Mult. Scler. J.20232965766710.1177/1352458523115140036802988 · doi ↗ · pubmed ↗

- 4Elgenidy A. Abdelhalim N.N. Al-kurdi M.A. Mohamed L.A. Ghoneim M.M. Fathy A.W. Hassaan H.K. Anan A. Alomari O. Hypogammaglobulinemia and Infections in Patients with Multiple Sclerosis Treated with Anti-CD 20 Treatments: A Systematic Review and Meta-Analysis of 19,139 Multiple Sclerosis Patients Front. Neurol.202415138065410.3389/fneur.2024.138065438699050 PMC 11063306 · doi ↗ · pubmed ↗

- 5Gasim M. Bernstein C.N. Graff L.A. Patten S.B. El-Gabalawy R. Sareen J. Bolton J.M. Marriott J.J. Fisk J.D. Marrie R.A. Adverse Psychiatric Effects of Disease-Modifying Therapies in Multiple Sclerosis: A Systematic Review Mult. Scler. Relat. Disord.20182612415610.1016/j.msard.2018.09.00830248593 · doi ↗ · pubmed ↗

- 6Gonzalez-Lorenzo M. Ridley B. Minozzi S. Del Giovane C. Peryer G. Piggott T. Foschi M. Filippini G. Tramacere I. Baldin E. Immunomodulators and Immunosuppressants for Relapsing-Remitting Multiple Sclerosis: A Network Meta-Analysis Cochrane Database Syst. Rev.20241 CD 01138110.1002/14651858.CD 011381.pub 338174776 PMC 10765473 · doi ↗ · pubmed ↗

- 7Lopez-Leon S. Geissbühler Y. SabidóM. Turkson M. Wahlich C. Morris J.K. A Systematic Review and Meta-Analyses of Pregnancy and Fetal Outcomes in Women with Multiple Sclerosis: A Contribution from the IMI 2 Conce PTION Project J. Neurol.20202672721273110.1007/s 00415-020-09913-132444984 PMC 7419441 · doi ↗ · pubmed ↗

- 8Mavridis T. Papagiannakis N. Breza M. Vavougios G.D. Patas K. Daponte A. Laskaratos A. Archontakis-Barakakis P. Pantazopoulos I. Mitsikostas D.D. B-Cell Targeted Therapies in Patients with Multiple Sclerosis and Incidence of Headache: A Systematic Review and Meta-Analysis J. Pers. Med.202212147410.3390/jpm 1209147436143259 PMC 9504525 · doi ↗ · pubmed ↗