Modeling and forecasting Saudi banking stability using ARIMA and exponential smoothing technique

Abdulaziz Alnajjar, Hamzeh F. Assous, Hazem Al-Najjar

TL;DR

This study uses statistical models to analyze and predict the financial stability of Saudi banks from 2014 to 2030, helping stakeholders align with Vision 2030 goals.

Contribution

The study introduces a stepwise linear regression model and applies ARIMA and exponential smoothing for forecasting Saudi banking stability.

Findings

The best model had a standard error of 7.209 and an adjusted R-squared of 71.3%.

NII1 ratio, CAR, and bank size positively affect stability, while investment and loan impairment ratios reduce it.

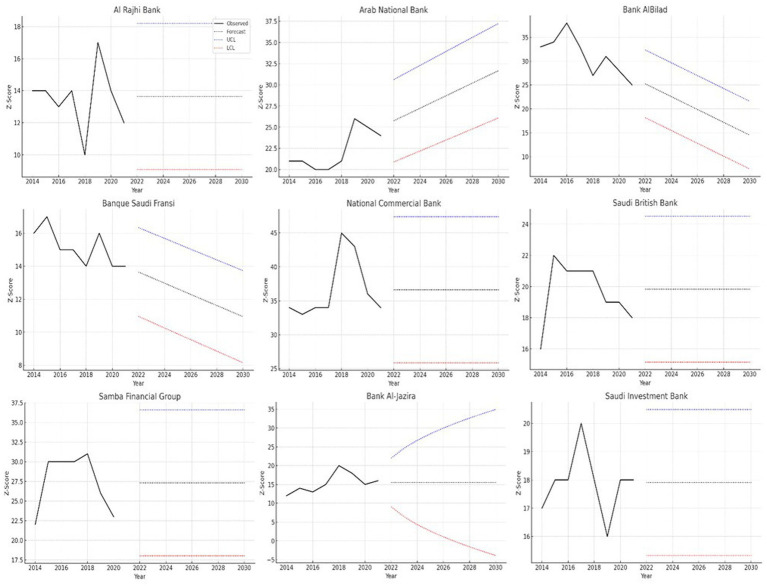

ARIMA and exponential smoothing models successfully forecast Z-scores through 2030 with metrics like RMSE and MAPE.

Abstract

This research examines the key factors influencing the financial stability of Saudi banks by developing an optimal stepwise linear regression model. The research uses financial information gathered from 11 Saudi banks over the period 2014–2021. Six categories for key performance indicators (KPIs) which consist of profitability, liquidity, asset quality, capitalization, bank size and economic growth are included in the model. The Z-score is used as its dependent variable for all stability measures. A model with the lowest standard error should be selected as the best explanatory model among all options while also maintaining the highest adjusted R-squared value. The findings showed that the chosen model has the lowest standard error around (7.209) and the highest adjusted R-squared (71.3%), The study demonstrates that NII1 ratio and CAR statistics alongside bank asset size (log of…

Click any figure to enlarge with its caption.

Figure 1

Figure 1Peer Reviews

No public reviews on file for this paper yet. If you reviewed it on a platform where reviews are public (OpenReview, ICLR, NeurIPS, ICML), you can paste yours below so the community can read it here.

Videos

No videos yet. Explain this paper in a talk, walkthrough, or lecture? Add one.

Taxonomy

TopicsFinancial Distress and Bankruptcy Prediction · Organizational and Employee Performance · Stock Market Forecasting Methods