National Support for Wealth-Building for Children From Low-Income Households

Catherine K. Ettman, Andrew Anderson, Megan V. Smith, David Radcliffe, Brian C. Castrucci, Sandro Galea

TL;DR

This study explores public support for creating trust funds for children in low-income families to help build wealth.

Contribution

It introduces a novel approach to wealth-building through state-managed trust accounts for low-income children.

Findings

There is notable national support for the concept of trust funds for low-income children.

Public opinion varies by demographic factors such as income and political affiliation.

Abstract

This survey study examines national support for state-managed trust fund accounts for children from low-income households.

Genes, proteins, chemicals, diseases, species, mutations and cell lines named across the full text — each resolved to its canonical identifier and authoritative record.

Click any figure to enlarge with its caption.

Figure

Figure| Characteristics | Total respondents, No. (weighted %) | Respondents, No. (%) | ||

|---|---|---|---|---|

| Total | Oppose | Support | ||

| Total | 1870 (100.0) | 655 (32.4) | 1215 (67.6) | |

| Sex | ||||

| Male | 948 (49.3) | 332 (32.9) | 616 (67.1) | .71 |

| Female | 922 (50.7) | 323 (31.9) | 599 (68.1) | |

| Age, y | ||||

| 18-29 | 134 (20.0) | 36 (24.4) | 98 (75.6) | <.001 |

| 30-44 | 567 (25.2) | 144 (23.5) | 423 (76.5) | |

| 45-59 | 451 (24.2) | 178 (39.0) | 273 (61.0) | |

| ≥60 | 718 (30.6) | 297 (39.8) | 421 (60.2) | |

| Race and ethnicity | ||||

| Black | 183 (11.5) | 42 (22.0) | 141 (78.0) | <.001 |

| Hispanic | 286 (17.7) | 74 (23.4) | 212 (76.6) | |

| White | 1289 (61.8) | 504 (37.5) | 785 (62.5) | |

| Other | 112 (9.1) | 35 (28.9) | 77 (71.1) | |

| Household income, $ | ||||

| 0 to <45 000 | 525 (34.0) | 147 (24.9) | 378 (75.1) | .002 |

| 45 000 to <75 000 | 412 (20.6) | 158 (35.7) | 254 (64.3) | |

| 75 000 to <150 000 | 633 (29.8) | 241 (36.9) | 392 (63.1) | |

| ≥150 000 | 300 (15.6) | 109 (36.0) | 191 (64.0) | |

| Household savings, $ | ||||

| 0 | 268 (17.4) | 74 (25.3) | 194 (74.7) | <.001 |

| 1 to <20 000 | 531 (31.7) | 146 (22.3) | 385 (77.7) | |

| 20 000 to <200 000 | 548 (27.2) | 222 (41.0) | 326 (59.0) | |

| ≥200 000 | 523 (23.7) | 213 (41.4) | 310 (58.6) | |

| Household debt, $ | ||||

| 0 | 469 (26.3) | 212 (40.9) | 257 (59.1) | .01 |

| 1 to <5000 | 465 (26.0) | 158 (28.5) | 307 (71.5) | |

| 5000 to <25 000 | 485 (26.4) | 151 (30.5) | 334 (69.5) | |

| ≥25 000 | 446 (21.3) | 133 (29.2) | 313 (70.8) | |

| Self-reported overall health | ||||

| Fair or poor | 404 (21.8) | 122 (29.7) | 282 (70.3) | .35 |

| Good or above | 1466 (78.2) | 533 (33.2) | 933 (66.8) | |

| Education | ||||

| Some college or less | 1133 (63.8) | 411 (31.9) | 722 (68.1) | .58 |

| College or more | 737 (36.2) | 244 (33.4) | 493 (66.6) | |

| Marital status | ||||

| Not married | 836 (52.4) | 258 (28.0) | 578 (72.0) | <.001 |

| Married or living with partner | 1034 (47.6) | 397 (37.2) | 637 (62.8) | |

| Religious service attendance | ||||

| Never attended | 641 (33.6) | 206 (29.1) | 435 (70.9) | .08 |

| Ever attended | 1229 (66.4) | 449 (34.1) | 780 (65.9) | |

| Employment status | ||||

| Not employed | 64 (5.1) | 13 (15.6) | 51 (84.4) | .005 |

| Employed or other | 1805 (94.9) | 641 (33.3) | 1164 (66.7) | |

| Home ownership | ||||

| Does not own home | 601 (36.5) | 157 (23.7) | 444 (76.3) | <.001 |

| Owns home | 1269 (63.5) | 498 (37.4) | 771 (62.6) | |

| Political affiliation | ||||

| Democrat | 662 (34.6) | 121 (18.3) | 541 (81.7) | <.001 |

| Republican | 492 (25.8) | 274 (52.0) | 218 (48.0) | |

| Independent | 494 (26.4) | 180 (32.5) | 314 (67.5) | |

| None of the above | 222 (13.2) | 80 (31.0) | 142 (69.0) | |

| Parental status | ||||

| Minor and adult | 198 (11.2) | 65 (34.4) | 133 (65.6) | <.001 |

| Minor only | 347 (16.9) | 91 (22.8) | 256 (77.2) | |

| Adult only | 704 (32.5) | 297 (41.1) | 407 (58.9) | |

| No children | 621 (39.4) | 202 (28.9) | 419 (71.1) | |

Peer Reviews

No public reviews on file for this paper yet. If you reviewed it on a platform where reviews are public (OpenReview, ICLR, NeurIPS, ICML), you can paste yours below so the community can read it here.

Videos

No videos yet. Explain this paper in a talk, walkthrough, or lecture? Add one.

Taxonomy

TopicsSocial Issues and Policies · Gender, Labor, and Family Dynamics · Financial Literacy, Pension, Retirement Analysis

Introduction

Although less studied than income, wealth is increasingly appreciated as a foundational driver of health.^1^ Difficulty accruing assets when starting from intergenerational disadvantage has led to interest in publicly supported wealth-building policies.^2,3^ Connecticut was the first state in the country to implement a state-wide “Baby Bonds” policy, providing 3200 in a state-managed trust fund for all babies born with Medicaid coverage, as of July 1, 2023.^[4](#zld250335r4)^ Depending on market performance, funds may reach 20 000 to $30 000 by early adulthood.^4^ Several other states are considering similar policies, and understanding public support may help guide future efforts.

Methods

We estimated national support for an early wealth-building policy (ie, Baby Bonds) for low-income children using nationally representative survey data from the Cumulative Life Stressors Impact on Mental Health and Well-Being (CLIMB) Study, collected from March 27 to April 30, 2025, from the AmeriSpeak panel. Among the 2969 adults invited, 2020 completed the survey (68.0% completion rate), and 150 participants were excluded due to missing covariate data, yielding an analytic sample of 1870. Survey weights aligned the sample to the US adult population. Support for Baby Bonds was defined by a response of “strongly support” or “somewhat support” when asked, “Generally speaking, do you support or oppose creating an investment for children born into low-income households in the US”? Additional details on survey design, variable definitions, and analysis are provided in Supplement 1. This survey study followed the American Association for Public Opinion Research (AAPOR) reporting guidelines and was deemed exempt by National Opinion Research Center Institutional Review Board at the University of Chicago.

We described overall sample characteristics and assessed differences in survey-weighted prevalence of early-wealth building policy support across characteristics. We used multivariable survey-weighted logistic regression to identify factors associated with support for Baby Bonds including in the model: sex, age, race and ethnicity, household income, household savings, overall health, education, marital status, home ownership, self-reported political affiliation, and parental status. Statistical significance was set at P < .05, and all tests were 2-sided. Analyses were conducted in Stata 19.5 from May 23 to November 20, 2025.

Results

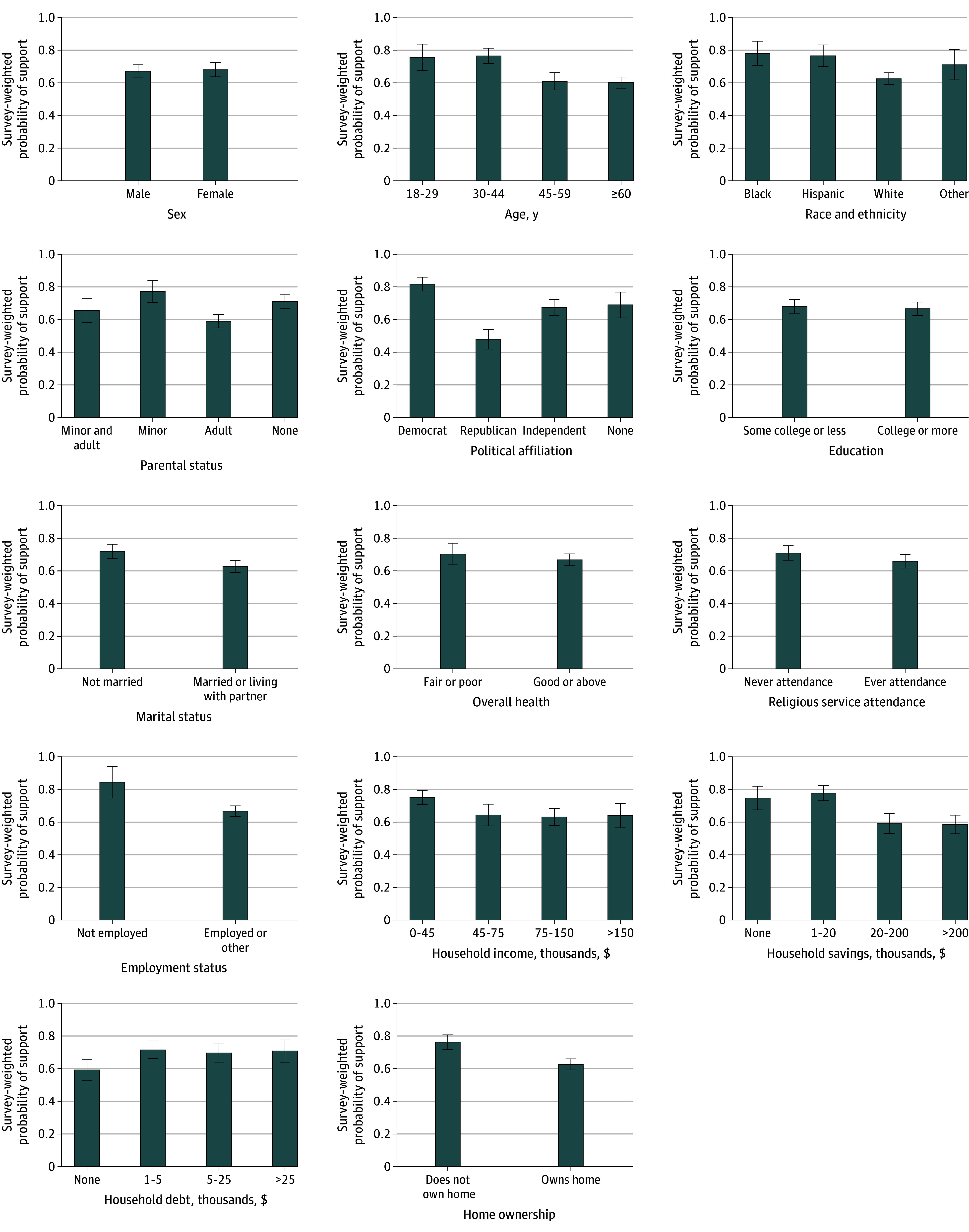

The sample consisted of 1870 respondents (922 female [50.7%, weighted], 718 age 60 years or older [30.6%, weighted], 183 Black [11.5%, weighted], 286 Hispanic [17.7%, weighted], and 1,289 White [61.8%, weighted]). We found that 67.6% of US adults reported support for creating an investment account for children born into low-income households (Table). Using survey weights, Baby Bonds were supported by 541 of 662 Democrats (81.7%), 218 of 492 Republicans (48.0%), 314 of 494 Independents (67.5%), and 142 of 222 of other adults (69.0%) (Figure). In the adjusted regression model, having no or low savings (1 to 200 000 or more) and identifying as Democrat, Independent, or none of the above (relative to Republican) were the only variables significantly associated with support for Baby Bonds.

Support for Baby Bonds by Demographic Characteristics and AssetsCumulative Life Stressors Impact on Mental Health and Well-Being (ie, CLIMB) Wave 6 data used, collected March to April 2025 (n = 1870). Survey weights applied.

Discussion

Most US adults supported wealth-building policies for children from low-income families, such as Baby Bonds. Almost half of Republicans and more than two-thirds of all other political groups (Democrat, Independent, and None) supported Baby Bonds. These findings provided an updated national perspective on support for Baby Bonds programs,^4^ building on earlier work by the American Civil Liberties Union in December 2022^2^ finding that 61% of voters supported Baby Bonds.^2^

This study has limitations. The survey did not assess preferences for different level of investments through Baby Bonds, limiting inference about other programs that provide financial support to children.

The creation of Trump Accounts through the 2025 Budget Reconciliation Act suggests a window of opportunity to advance child-oriented wealth-building programs. Trump Accounts provide $1000 for babies born between 2025 and 2028.^5^ Unlike Baby Bonds, which are automatic and income-targeted, Trump Accounts allow voluntary contributions that may be less feasible for lower-resourced families.^6^ Nonetheless, the combined momentum behind Baby Bonds and Trump Accounts may create new opportunities to advance early-life wealth building policies that promote population health.

The reference list from the paper itself. Each links out to its DOI / PubMed record.

- 1Pollack CE, Chideya S, Cubbin C, Williams B, Dekker M, Braveman P. Should health studies measure wealth? a systematic review. Am J Prev Med. 2007;33(3):250-264. doi:10.1016/j.amepre.2007.04.03317826585 · doi ↗ · pubmed ↗

- 2Johnson A. Baby Bonds: a path toward prosperity for future generations. American Civil Liberties Union. Accessed September 18, 2025. https://www.aclu.org/news/racial-justice/baby-bonds-a-path-toward-prosperity-for-future-generations

- 3Baby bonds. Institute on Race, Power and Political Economy. Accessed November 17, 2025. https://racepowerpolicy.org/baby-bonds/

- 4Baby bonds. CT.gov. Accessed September 17, 2025. https://portal.ct.gov/ott/debt-management/ct-baby-bonds

- 5Council of Economic Advisors. Trump Accounts Give the Next Generation a Jump Start on Saving. The White House; 2025.

- 6Brown M, Atherton S, Ewas J, Boshara R. How “Trump Accounts” measure up to the evidence in early wealth-building policy. Urban Institute. Accessed September 23, 2025. https://www.urban.org/urban-wire/how-trump-accounts-measure-evidence-early-wealth-building-policy