On the Shortfall of Tail-Based Entropy and Its Application to Capital Allocation

Pingyun Li, Chuancun Yin

TL;DR

This paper introduces a new risk measure called shortfall of tail-based entropy (STE) that captures both the magnitude and variability of extreme risks, and applies it to capital allocation in financial contexts.

Contribution

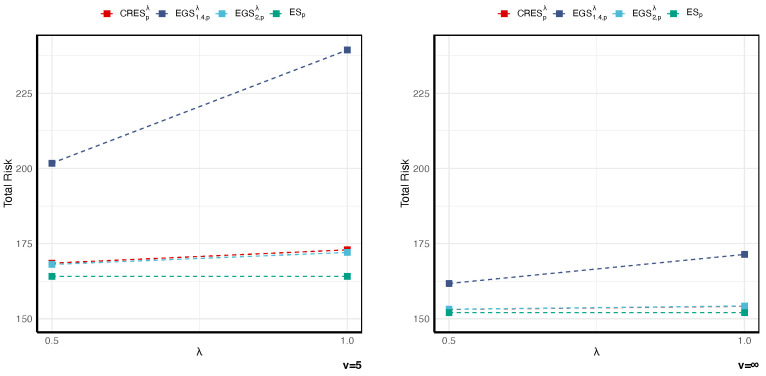

The novelty lies in combining expected shortfall with tail-based entropy to create a new coherent risk measure that penalizes tail variability.

Findings

STE generalizes several existing shortfall-type risk measures.

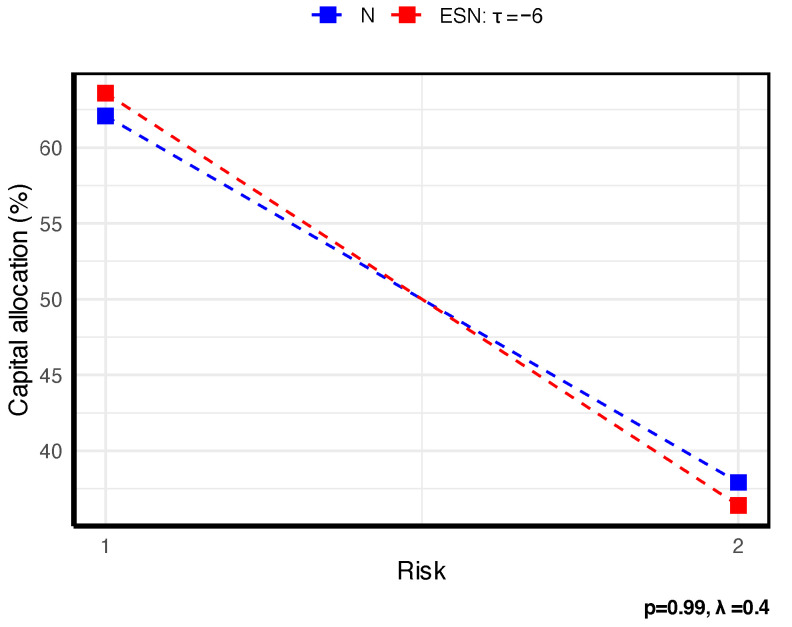

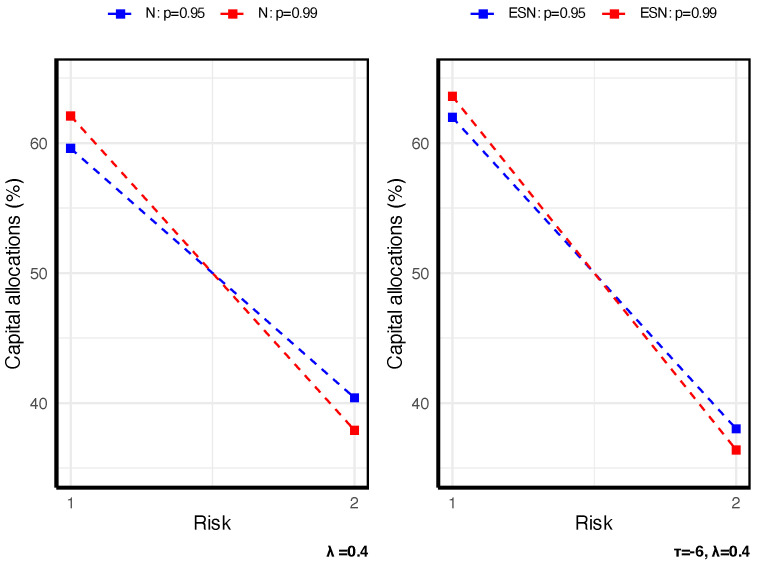

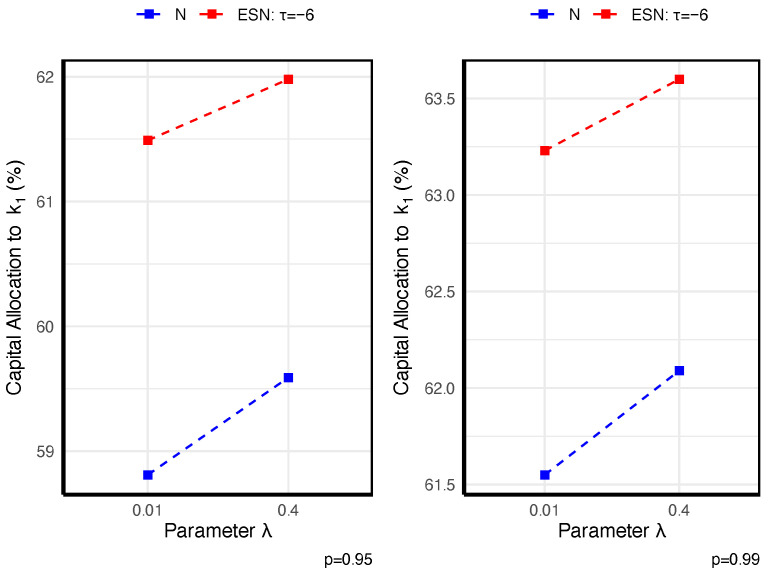

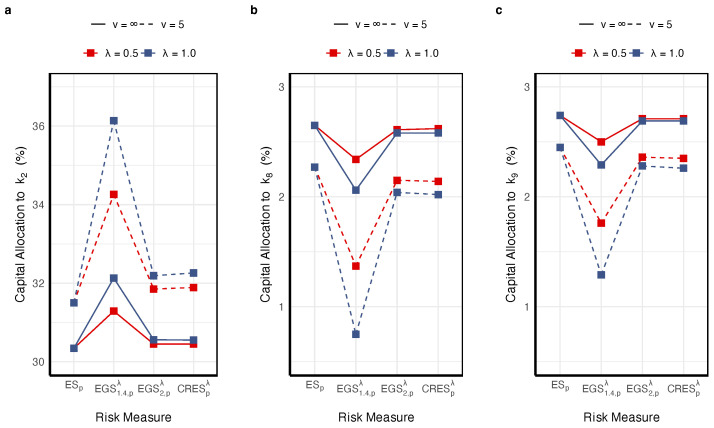

Closed-form capital allocation formulas are derived for elliptical and extended skew-normal distributions.

Empirical analysis on insurance data demonstrates the practicality of STE-based allocation.

Abstract

We introduce and study the shortfall of tail-based entropy (STE), a tail-sensitive risk functional that combines expected shortfall (ES) and tail-based entropy (TE). Beyond the tail mean, STE imposes a rank-dependent penalty on tail variability, thereby capturing both the magnitude and variability of tail risk under extremes. The framework encompasses several shortfall-type measures as special cases, such as Gini shortfall, extended Gini shortfall, shortfall of cumulative residual entropy, shortfall of right-tail deviation, and shortfall of cumulative residual Tsallis entropy. We provide equivalent characterizations of STE, derive sufficient conditions for coherence, and establish monotonicity with respect to tail-variability order. As an application, we investigate STE-based capital allocation, deriving closed-form allocation formulas under elliptical and extended skew-normal…

Genes, proteins, chemicals, diseases, species, mutations and cell lines named across the full text — each resolved to its canonical identifier and authoritative record.

Click any figure to enlarge with its caption.

Figure 1

Figure 1 Figure 2

Figure 2 Figure 3

Figure 3 Figure 4

Figure 4 Figure 5

Figure 5Peer Reviews

No public reviews on file for this paper yet. If you reviewed it on a platform where reviews are public (OpenReview, ICLR, NeurIPS, ICML), you can paste yours below so the community can read it here.

Videos

No videos yet. Explain this paper in a talk, walkthrough, or lecture? Add one.

Taxonomy

TopicsRisk and Portfolio Optimization · Financial Risk and Volatility Modeling · Probability and Risk Models