US Food and Drug Administration Competitive Generic Therapy Approvals and Drug Competition

Kevin Kho, Rinku Patel, Harinder Singh Chahal

TL;DR

This study analyzes how pricing and sales volumes change for generic drugs after they receive approval from the FDA.

Contribution

The study provides new insights into the relationship between FDA approvals and market competition for generic drugs.

Findings

FDA approvals are associated with increased market competition for generic drugs.

Drug pricing and sales volumes show significant variation following FDA approvals.

Abstract

This cross-sectional study examines the dynamics of competitive generic therapy drug pricing and volume.

Genes, proteins, chemicals, diseases, species, mutations and cell lines named across the full text — each resolved to its canonical identifier and authoritative record.

Click any figure to enlarge with its caption.

Figure

Figure| Characteristics | No. (%) | Time to market, median (IQR) [range], d | CGTs included in competition analyses, No. | Change in price: ratio of prices after vs before CGT entry, (IQR) [range]e | Change in units: ratio of units after vs before CGT entry, (IQR) [range]f | |

|---|---|---|---|---|---|---|

| CGT products approved with exclusivity eligibility | CGTs eligible for exclusivity that marketed within 75 d | |||||

| Total products | 127 | 106 | 7 (1-40.8) [0-75] | 94 | 0.82 (0.71-0.94) [0.38-1.9] | 1.11 (0.98-1.24) [0.37-5.86] |

| Complex vs noncomplex | ||||||

| Complex | 21 (16.5) | 21 (100) | 7 (1-34) [0-69] | 20 | 0.73 (0.67-0.93) [0.38-1.15] | 1.33 (1.07-1.67) [0.74-5.84] |

| Noncomplex | 106 (83.5) | 85 (80.2) | 7 (1-50) [0-75] | 74 | 0.83 (0.73-0.94) [0.58-1.9] | 1.09 (0.96-1.18) [0.37-5.86] |

| Route of administration/dosage | ||||||

| Intravenous/injectable | 34 (26.8) | 23 (67.6) | 11 (4-55) [0-73] | 19 | 0.93 (0.85-1.03) [0.6-1.9] | 1.13 (1.09-1.44) [0.37-5.86] |

| Ophthalmic/nasal | 8 (6.3) | 8 (100) | 34 (6.8-70.5) [0-75] | 6 | 0.87 (0.72-1.11) [0.54-1.33] | 1 (0.79-1.57) [0.72-5.84] |

| Oral (liquid) | 17 (13.4) | 14 (82.4) | 3.5 (0-20.5) [0-72] | 13 | 0.82 (0.73-0.92) [0.64-0.97] | 1.16 (1.07-1.21) [1-1.41] |

| Oral (solid) | 57 (44.9) | 50 (87.7) | 7 (1-24.2) [0-72] | 46 | 0.76 (0.72-0.9) [0.58-1.12] | 1.07 (0.93-1.15) [0.6-3.9] |

| Topical/transdermal | 11 (8.7) | 11 (100) | 3 (1-38.5) [0-61] | 10 | 0.71 (0.68-0.81) [0.38-0.96] | 1.53 (1.26-1.79) [0.96-3.62] |

| Approval year | ||||||

| 2018 | 7 (5.5) | 7 (100) | 11 (3-25.5) [0-34] | 7 | 0.84 (0.68-0.86) [0.64-0.93] | 1.09 (0.99-1.1) [0.69-1.12] |

| 2019 | 22 (17.3) | 19 (86.4) | 0 (0-5.5) [0-69] | 18 | 0.9 (0.73-0.98) [0.6-1.08] | 1.01 (0.85-1.16) [0.63-2.78] |

| 2020 | 21 (16.5) | 16 (76.2) | 4.5 (0-31.8) [0-70] | 15 | 0.88 (0.72-0.91) [0.54-1.15] | 1.1 (1.04-1.16) [0.74-5.84] |

| 2021 | 41 (32.3) | 37 (90.2) | 8 (4-68) [0-75] | 29 | 0.75 (0.72-0.86) [0.61-1.15] | 1.1 (1.03-1.22) [0.61-5.86] |

| 2022 | 36 (28.3) | 27 (75.0) | 11 (6.5-52.5) [0-73] | 25 | 0.89 (0.73-1.04) [0.38-1.9] | 1.29 (1.12-1.65) [0.37-3.9] |

| Therapeutic area | ||||||

| Cardiovascular disease | 12 (9.4) | 10 (83.3) | 7 (0-8) [0-28] | 10 | 0.75 (0.73-0.85) [0.58-0.9] | 1.13 (1.08-1.17) [0.6-2.55] |

| Endocrinology, diabetes, and metabolism | 15 (11.8) | 10 (66.7) | 26.5 (5.2-53.8) [0-64] | 9 | 0.76 (0.67-0.92) [0.59-0.97] | 1.23 (1.12-1.45) [1.03-1.65] |

| Infectious disease | 16 (12.6) | 13 (81.2) | 19 (7-69) [0-71] | 13 | 0.8 (0.68-0.93) [0.38-1.1] | 1.17 (1.08-1.44) [0.89-3.62] |

| Medical countermeasure | 10 (7.9) | 9 (90.0) | 4 (2-6) [0-68] | 7 | 0.97 (0.88-1.15) [0.84-1.9] | 1.16 (1.13-1.76) [0.37-5.86] |

| Psychiatry | 15 (11.8) | 14 (93.3) | 1 (0.2-4) [0-61] | 13 | 0.87 (0.68-0.98) [0.61-1.08] | 1.05 (0.79-1.09) [0.63-1.31] |

| All others | 59 (46.5) | 50 (84.7) | 8 (2.2-55) [0-75] | 42 | 0.8 (0.71-0.95) [0.54-1.33] | 1.06 (0.93-1.22) [0.61-5.84] |

Peer Reviews

No public reviews on file for this paper yet. If you reviewed it on a platform where reviews are public (OpenReview, ICLR, NeurIPS, ICML), you can paste yours below so the community can read it here.

Videos

No videos yet. Explain this paper in a talk, walkthrough, or lecture? Add one.

Taxonomy

TopicsPharmaceutical Economics and Policy · Medication Adherence and Compliance · Health Systems, Economic Evaluations, Quality of Life

In 2017, Congress established the competitive generic therapy (CGT) pathway to incentivize generic entry when there is inadequate generic competition, ie, there is not more than 1 version (brand or generic) of that drug on the market. Certain CGT-designated products can be eligible for 180 days of marketing exclusivity postapproval, a period during which additional competitor drugs may not be approved but existing competitors are unaffected.^1,2^ Two CGT attributes incentivize quick marketing: first, exclusivity is forfeited if the drug is not marketed within 75 days postapproval (forfeiture does not transfer the exclusivity to another applicant), and second, the US Food and Drug Administration can approve competing applications that duplicate the same branded product until the exclusivity-eligible applicant markets, initiating 180-day of exclusivity.^1^ Prior work demonstrated robust company participation in the CGT pathway; this study analyzes the dynamics of CGT competition, including drug pricing and volume.^1^

Methods

We first characterized generic drug products approved with CGT exclusivity eligibility from October 1, 2017, through December 31, 2022. This study defines a drug product at the molecule-strength-dosage form level, which is consistent with the product level used for exclusivity purposes; thus, 1 molecule may be marketed in multiple products (eMethods in Supplement 1). Second, for exclusivity-eligible CGTs launching within 75 days with available competitor data pre- and post-CGT entry, we conducted a 25-month event study examining (1) mean prices and volumes of existing drugs 12 months pre-CGT entry and (2) monthly prices and volumes of CGTs, existing drugs, and competitors for 12 months post-CGT entry. As the study did not involve human participants, institutional review board approval was not required.

The price and volume outcomes are ratios of monthly values compared with their respective pre-CGT 12-month averages. A post-CGT entry price level or volume ratio less than 1 indicates a decrease in price or volume, respectively. Transactional volume and sales data were obtained from IQVIA’s National Sales Perspective and adjusted for inflation. Prices exclude manufacturer discounts and rebates.^3^ Analyses were conducted using R, version 4.3.1 (R Foundation).

Results

Among the 127 CGTs approved with exclusivity eligibility, 106 (83.5%) triggered the exclusivity by marketing within 75 days of approval within a median of 7 days (IQR, 1-41 days) (Table). CGT entry was associated with a reduced price of the median drug by 18% without significantly affecting overall market demand (Table).

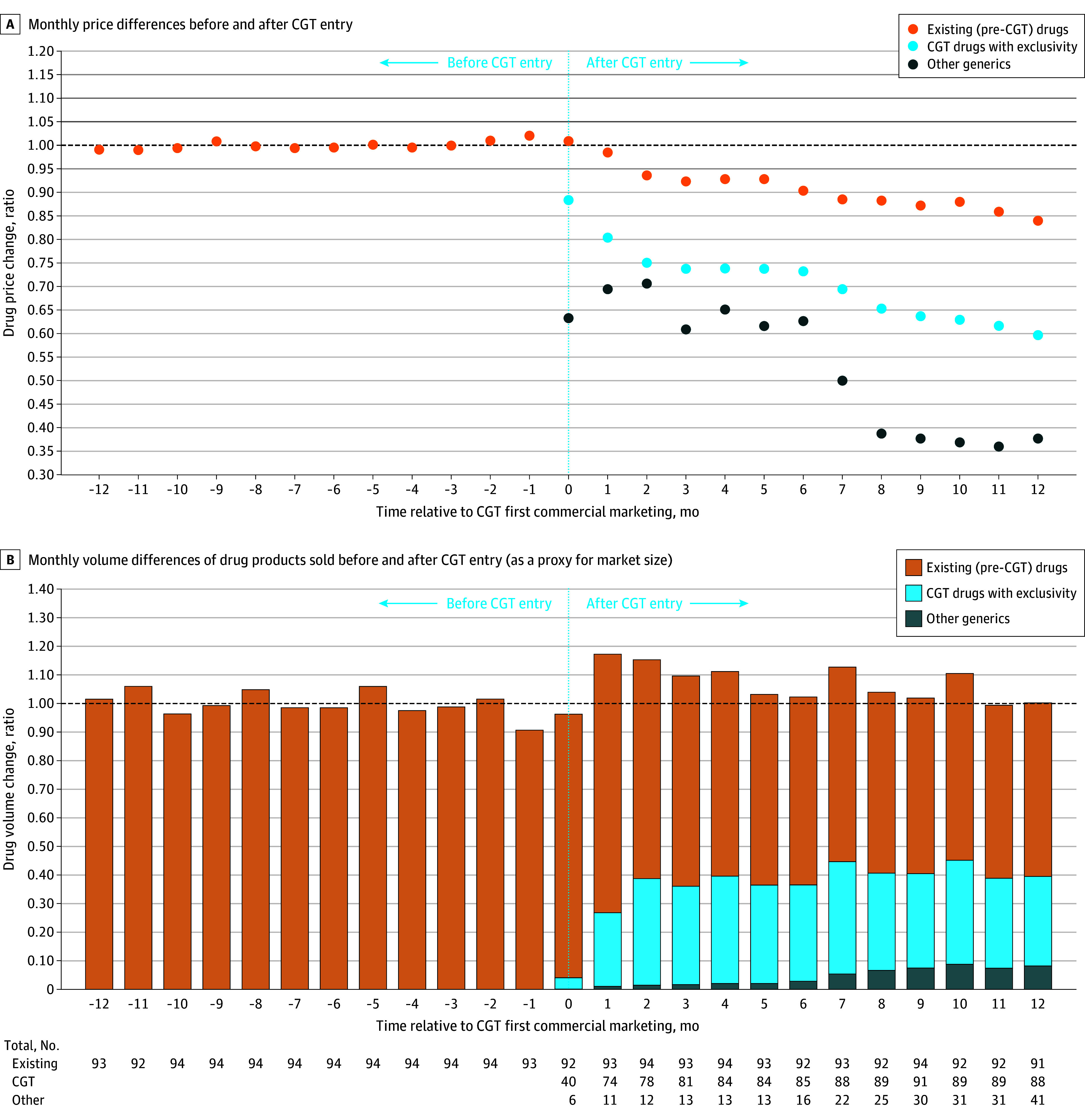

Among the 106 marketed CGTs, 94 had analyzable sales data. These drugs entered the market at lower prices than therapeutically equivalent incumbents (Figure, A). By month 12, the weighted mean prices of existing drugs and CGTs were 15.9% and 40.3% lower than average prices pre-CGT entry, respectively.

Trends in Monthly Prices and Volumes Among Drug Products 12 Months Before and After Competitive Generic Therapy (CGT) EntryData were sourced from the IQVIA National Sales Perspectives (NSP), 2017 to 2024. The NSP measures the volume of prescription drug products moving from distributors and manufacturers into various outlets within the retail and nonretail markets and captures approximately 90% of the total pharmaceutical market. Except for the mail channel, these data are estimated based on national projections. Trends in the monthly prices and volumes among drug products in the event study are pictured 12 months before and 12 months after CGT entry relative to their respective pre-CGT 12-month averages. The price level (A) is the post-CGT month’s spending on a drug over spending if bought at pre-CGT average prices. The volume ratio (B) is the post-CGT month’s volume, in units, of a drug, over the average volume pre-CGT entry. For prices and volumes, a ratio of 1 means that there was no difference in either metric before and after CGT entry; while a ratio of less than 1 indicates a decrease in drug price or volume and vice versa for a ratio of greater than 1. In some cases, another manufacturer can enter the market before the CGT product triggers exclusivity, thus the presence of other generics appearing during the CGT exclusivity period. The dip in the price ratio at months 6 and 7 was likely associated with the increased number of products entering the market after the CGT exclusivity expired, as observed in the data table. The number of other generics increased from 13 to 16 in month 6 and 22 in month 7, and this trend was observed through the end of the study period.

Total volume of products sold was relatively consistent over the 25-month period. At the end of the study, existing drugs, CGTs, and other therapeutically equivalent products comprised 61%, 31%, and 8% of market volume, respectively (Figure, B).

Discussion

A total of 106 of 127 approved CGTs (83%) launched within 75 days, quickly competing with incumbents and lowering prices while capturing market share. In contrast, among certain other non-CGT generics that are first to challenge branded drug patents and are thus eligible for 180-day exclusivity, only 50% launch within 6 months.^4^ The faster CGT entry is likely due to the use or lose nature of CGT exclusivity that only blocks other approvals once triggered by marketing. Further, typically lone generic competitors reduce prices by 31% less than the brand price. The reduction for CGTs is smaller (26.8% by month 6), likely because CGTs are lower-revenue drugs.^5^

This study was limited first by the fact that we could not determine whether the CGT pathway induces entry or is used by manufacturers who would have entered regardless. Second, because our data excluded rebates, the results may understate incumbent responses, as incumbents may have increased rebates alongside price reductions to retain market share.

During the study period, there was no lasting change in total volume of product sold despite increased numbers of manufacturers; existing and CGT products appeared to find an equilibrium to balance competition, market demand, and lower prices. However, a longer-term product-level evaluation is needed to assess whether markets for some CGTs can sustain multiple manufacturers.^6^

The reference list from the paper itself. Each links out to its DOI / PubMed record.

- 1Chahal HS, Fowler AC, Patel R, Shimer M. Characteristics and outcomes of products seeking competitive generic therapy designation and exclusivity. JAMA. 2021;326(18):1863-1865. doi:10.1001/jama.2021.1459534751720 PMC 8579229 · doi ↗ · pubmed ↗

- 2US Food and Drug Administration. Competitive generic therapies: guidance for industry. Accessed July 30, 2024. https://www.fda.gov/media/136063/download

- 3IQVIA. SMART—US Edition, national sales perspectives online tool. Accessed April 30, 2024. https://www.iqvia.com/

- 4Chahal HS, Patel R, Shimer M. Marketing of first generic drugs approved by US FDA from January 2010 to June 2017. Accessed June 13, 2022. https://www.fda.gov/about-fda/reports/reports-agency-policies-and-initiatives

- 5Conrad R, Lutter R. Generic competition and drug prices: new evidence linking greater generic competition and lower generic drug prices. Accessed September 18, 2025. https://www.fda.gov/media/133509/download

- 6Glenza J. Generic drugs in the US are too cheap to be sustainable, experts say: non–brand-name drugs are one inexpensive part of the healthcare system but they’re driving some manufacturers out of business. Accessed June 11, 2024. https://www.theguardian.com/science/2024/jan/18/us-generic-drugs-prices-causing-shortage