Private Equity Acquisitions of Home Health Agencies

David T. Zhu, Aakash Reddy, Geronimo Bejarano, Robert Tyler Braun

TL;DR

This study analyzes how private equity firms have acquired home health agencies in the US over time, focusing on patterns by year, firm size, and location.

Contribution

The study provides a detailed analysis of private equity acquisition trends in the home health agency sector in the US.

Findings

Private equity acquisitions of home health agencies have increased over recent years.

Larger private equity funds are more likely to acquire home health agencies.

Acquisition activity is concentrated in specific geographic regions.

Abstract

This cross-sectional study examines the pattern of home health agency acquisitions by private equity in the US by year, fund size of the acquiring firm, and location.

Genes, proteins, chemicals, diseases, species, mutations and cell lines named across the full text — each resolved to its canonical identifier and authoritative record.

Click any figure to enlarge with its caption.

Figure

Figure| Characteristic | Total No. (%) (N = 749) |

|---|---|

| Reacquisitions | |

| Total | 55 (7.3) |

| 1 | 49 (6.5) |

| 2 | 3 (0.4) |

| Target home health agency | |

| Caring Brands International/Interim HealthCare | 258 (34.4) |

| Elara Caring | 96 (12.8) |

| Aveanna Healthcare | 84 (11.2) |

| Just Home Healthcare Services | 34 (4.5) |

| BrightSpring Health Services | 33 (4.4) |

| Concierge Home Care | 25 (3.3) |

| Team Select Home Care | 22 (2.9) |

| Healthy Living at Home | 18 (2.4) |

| Choice Health at Home | 14 (1.9) |

| AccentCare Home Health | 13 (1.7) |

| Other | 152 (20.3) |

| Private equity fund size, $ | |

| Lower-middle market: 20 to 100 million | 85 (11.3) |

| Middle market: >100 to 500 million | 520 (69.4) |

| Upper-middle market: >500 million to 1 billion | 1 (0.1) |

| Megafund: >1 billion | 143 (19.1) |

| Private equity firm | |

| Wellspring Capital Management | 263 (35.1) |

| Blue Wolf Capital | 96 (12.8) |

| Bain Capital | 89 (11.9) |

| H.I.G. Capital | 34 (4.5) |

| Kohlberg Kravis Roberts & Co | 33 (4.4) |

| Waud Capital Partners | 25 (3.3) |

| Tenex Capital Management | 22 (2.9) |

| Capricorn Healthcare | 18 (2.4) |

| Trive Capital | 14 (1.9) |

| Advent International | 13 (1.7) |

| Other | 142 (19.0) |

| US Census region | |

| South | 355 (47.4) |

| Midwest | 172 (23.0) |

| West | 118 (15.8) |

| Northeast | 104 (13.9) |

| State | |

| Florida | 115 (15.4) |

| Texas | 85 (11.3) |

| California | 67 (8.9) |

| Pennsylvania | 43 (5.7) |

| New Jersey | 36 (4.8) |

| Indiana | 32 (4.3) |

| Oklahoma | 29 (3.9) |

| Kentucky | 28 (3.7) |

| Colorado | 26 (3.5) |

| Ohio | 26 (3.5) |

| Other | 262 (35.0) |

Peer Reviews

No public reviews on file for this paper yet. If you reviewed it on a platform where reviews are public (OpenReview, ICLR, NeurIPS, ICML), you can paste yours below so the community can read it here.

Videos

No videos yet. Explain this paper in a talk, walkthrough, or lecture? Add one.

Taxonomy

TopicsPrivate Equity and Venture Capital · Healthcare Policy and Management · Innovation Policy and R&D

Introduction

Postacute and long-term care delivered in US home health agencies (HHAs) has expanded over the past decade, driven by an aging population and efforts to shift care from hospitals to lower-cost settings.^1^ In parallel, HHAs have become increasingly attractive to institutional investors. Private equity (PE) investment in health care has increased across multiple health care sectors, reshaping care delivery and market structure.^2^ Rising demand and the industry’s fragmented landscape have drawn PE attention to HHAs, where roll-up strategies (acquiring and consolidating smaller agencies into larger firms) can increase valuations through multiple arbitrage.^1,3^ This study aimed to describe patterns in PE acquisitions of HHAs.

Methods

Using established methodologies,^3^ we identified PE acquisitions of HHAs from 2006 to 2024 in the Irving Levin health care market database, verified by industry reports, press releases, and HHA websites (eMethods 1 in Supplement 1). The Weill Cornell Medicine Institutional Review Board approved this cross-sectional study and waived informed consent because deidentified data were used. We followed the STROBE reporting guideline.

Provider of Services files were used to obtain each HHA’s Centers for Medicare & Medicaid Services (CMS) Certification Number, location, and other HHAs in the same transaction. We calculated the percentage of acquisitions by year, PE fund size, top-10 PE acquirers and acquired HHAs, Census region, and state. PE fund size was obtained from firms’ websites and categorized as lower-middle market (100 million), middle market (>500 million), upper-middle market (>1 billion), or megafund (>$1 billion). Prior evidence suggests fund size changes PE acquisition strategies and target selection^4^; thus, we examined whether HHA acquisitions were concentrated in certain funds or broadly distributed (eMethods 2 in Supplement 1). Data analysis was performed with R, version 4.3.3 (R Core Team).

Results

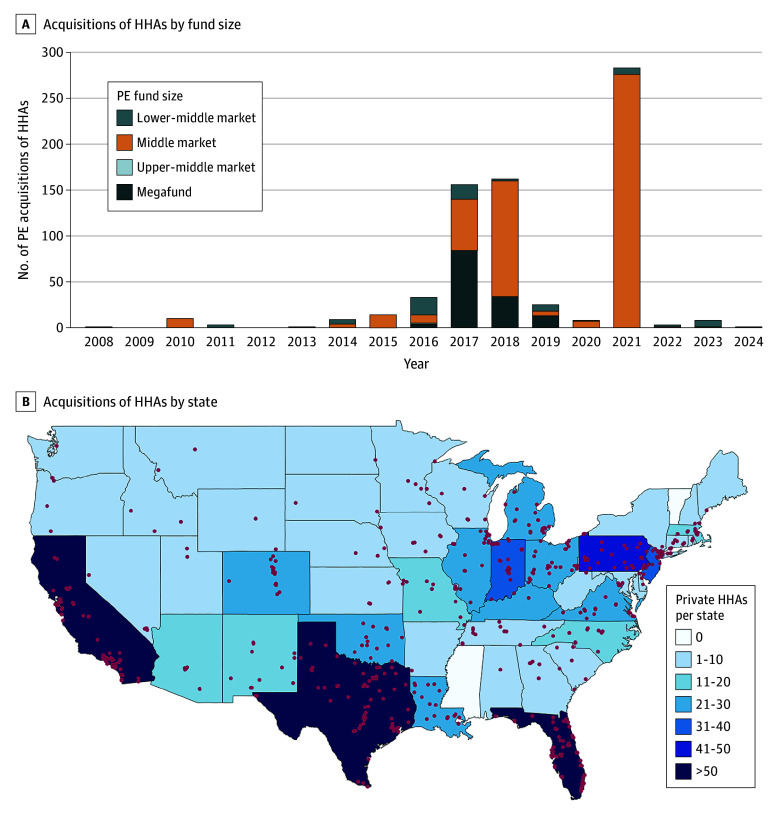

From 2006 to 2024, we identified 749 unique HHAs, of which 55 (7.3%) were involved in secondary PE buyouts (Table). Most HHAs were acquired by middle-market (520 [69.4%]) or megafund (143 [19.1%]) PE firms. Acquisitions tended to occur in batches, particularly in 2017 (156 [20.8%]), 2018 (162 [21.6%]), and 2021 (283 [37.8%]) (Figure, A). Megafunds accounted for most acquisitions in 2017, while middle-market firms led in 2018 and 2021.

Private Equity (PE) Index Acquisitions of Home Health Agencies (HHAs) by PE Fund Size and State From 2006 to 2024A, Lower-middle market fund size: 100 million, middle market fund size: more than 500 million, upper-middle market fund size: more than 1 billion, and megafund size: more than $1 billion. B, Overlying dots indicate the county where each HHA involved in a PE acquisition was located.

We identified 63 distinct HHA chains and 52 PE firms (Table). Most acquisitions involved just 3 target HHAs: Caring Brands International/Interim HealthCare (258 [34.4%]), acquired by Wellspring Capital Management in 2021; Elara Caring (96 [12.8%]), acquired by Blue Wolf Capital in 2018; and Aveanna Healthcare (84 [11.2%]), acquired by Bain Capital in 2017.

Regionally, most acquisitions occurred in the South (355 [47.4%]), followed by the Midwest (172 [23.0%]), West (118 [15.8%]), and Northeast (104 [13.9%]) (Figure, B). Florida accounted for the largest share (115 [15.4%]), followed by Texas (85 [11.3%]) and California (67 [8.9%]).

Discussion

This study extends prior research on PE acquisitions in hospitals, hospices, and nursing homes by examining the HHA sector.^1,2^ PE acquisitions of HHAs accelerated after 2017, led by middle-market and megafund firms, reflecting sustained interest across a broad range of PE investors. Regional concentration in the South, particularly Florida and Texas, parallels PE activity in other health care sectors and aligns with regions experiencing rising demand for HHAs due to aging populations.^2^

Policy changes may have contributed to these PE acquisition patterns, including the 2016 statewide extensions of CMS-imposed moratoria in Florida and Texas (which restricted new HHA market entrants) and the 2017 repeal of the proposed Home Health Groupings Model (which would have substantially reduced future Medicare payments to HHAs).^5,6^ Further research is needed to examine how PE fund size and evolving policy environments affect investment strategies in HHAs.

Study limitations include possible omission of smaller or unreported transactions and exits or divestitures, which may have shifted the composition of PE-owned HHAs over time. Future research should expand on this descriptive work to evaluate the association of PE ownership with quality of care, patient outcomes, market competition, and spending in HHAs.

The reference list from the paper itself. Each links out to its DOI / PubMed record.

- 1Zhang Z, Li K, Wang S, Fashaw-Walters S, Hou Y. Change of ownership and quality of home health agency care. JAMA Health Forum. 2024;5(11):e 243767. doi:10.1001/jamahealthforum.2024.376739485335 PMC 11530943 · doi ↗ · pubmed ↗

- 2Borsa A, Bejarano G, Ellen M, Bruch JD. Evaluating trends in private equity ownership and impacts on health outcomes, costs, and quality: systematic review. BMJ. 2023;382:e 075244. doi:10.1136/bmj-2023-07524437468157 PMC 10354830 · doi ↗ · pubmed ↗

- 3Braun RT, Stevenson DG, Unruh MA. Acquisitions of hospice agencies by private equity firms and publicly traded corporations. JAMA Intern Med. 2021;181(8):1113-1114. doi:10.1001/jamainternmed.2020.626233938919 PMC 8094028 · doi ↗ · pubmed ↗

- 4Hammer B, Knauer A, Pflücke M, Schwetzler B. Inorganic growth strategies and the evolution of the private equity business model. J Corp Finance. 2017;45:31-63. doi:10.1016/j.jcorpfin.2017.04.006 · doi ↗

- 5Extension and expansion of the provider enrollment home health agency (HHA) moratoria. Centers for Medicare & Medicaid Services. August 26, 2016. Accessed August 14, 2025. https://www.cms.gov/Medicare/Provider-Enrollment-and-Certification/Survey Certification Gen Info/Downloads/Survey-and-Cert-Letter-16-36.pdf

- 6Medicare and Medicaid programs; CY 2018 Home health prospective payment system rate update and CY 2019 Case-mix adjustment methodology refinements; home health value-based purchasing model; and home health quality reporting requirements. Federal Registrar. November 7, 2017. Accessed August 14, 2025. https://www.federalregister.gov/documents/2017/11/07/2017-23935/medicare-and-medicaid-programs-cy-2018-home-health-prospective-payment-system-rate-update-and-cy 29111624 · pubmed ↗