Integrating event information and multi dimensional relationships for improved financial time series forecasting

Xinke Du, Jinfei Cao, Xiyuan Jiang, Qin Wang, Boyao Xu, Ziyang Liu, Yikun Chen, ChunHong Yuan

TL;DR

This paper introduces DAFF-Net, a new deep learning model that improves financial predictions by combining event information and complex asset relationships.

Contribution

The novel DAFF-Net framework integrates event-driven patterns and multi-dimensional asset relationships for financial forecasting.

Findings

DAFF-Net outperforms eight baseline models with 7.4%-15.2% lower MSE and 7.0%-21.4% higher R² scores.

The model shows significant improvements in long-term financial time series predictions.

Cross-asset validation on four sectors confirms DAFF-Net's effectiveness across different markets.

Abstract

Financial time series prediction is extremely challenging due to the intertwined effects of market narratives and complex inter-asset relationships. Traditional prediction models often fail to distinguish similar price patterns driven by different underlying causes, limiting their predictive accuracy in practical scenarios. To address these limitations, this study proposes the Dual-stream Alpha Factor Fusion Network (DAFF-Net), an innovative deep learning framework that integrates event-driven temporal pattern extraction with multi-dimensional relationship-aware channel soft clustering. The event-driven temporal pattern extractor employs an event-aware router to fuse time series data with contextual event information encoded from news, corporate announcements, and macroeconomic data, enabling the model to understand the underlying narratives behind market fluctuations. The…

Genes, proteins, chemicals, diseases, species, mutations and cell lines named across the full text — each resolved to its canonical identifier and authoritative record.

Click any figure to enlarge with its caption.

Figure 1

Figure 1 Figure 2

Figure 2 Figure 3

Figure 3 Figure 4

Figure 4 Figure 5

Figure 5 Figure 6

Figure 6 Figure 7

Figure 7 Figure 8

Figure 8 Figure 9

Figure 9 Figure 10

Figure 10 Figure 11

Figure 11- —Shanghai Municipal Education Commission

- —Jiangsu Science and Technology Think Tank Program

- —Jiangsu Provincial Department of Education

Peer Reviews

No public reviews on file for this paper yet. If you reviewed it on a platform where reviews are public (OpenReview, ICLR, NeurIPS, ICML), you can paste yours below so the community can read it here.

Videos

No videos yet. Explain this paper in a talk, walkthrough, or lecture? Add one.

Taxonomy

TopicsStock Market Forecasting Methods · Time Series Analysis and Forecasting · Machine Learning in Healthcare

Introduction

Financial time series prediction has consistently been one of the core research problems in the fields of econometrics, machine learning, and artificial intelligence^1^. Since the introduction of Brownian motion theory and the efficient market hypothesis in the mid-20th century^2,3^, scholars have been exploring how to accurately predict the price movements of financial assets. With the increasing complexity of global financial markets, accurate financial forecasting can not only provide scientific basis for investment decisions but also help financial institutions conduct effective risk management and asset allocation, and its importance is increasingly prominent. The complexity of today’s financial markets far exceeds the assumptions of traditional theoretical models. The exponential growth in information dissemination speed has changed the fundamental operating mechanisms of markets, and diversified information sources such as social media, news websites, and financial blogs enable market information to spread at unprecedented speeds, significantly shortening investors’ decision-making windows, making market reactions more rapid and prone to overreaction. The proliferation of algorithmic trading and high-frequency trading has fundamentally changed market microstructure^4,5^. According to statistics, algorithmic trading accounts for over 70% of trading volume in the U.S. stock market, and the interaction of these automated trading systems creates complex feedback mechanisms that traditional market models based on human behavior struggle to accurately describe. The deepening of globalization has further increased the complexity of financial markets^6^, with the correlation between different markets significantly increased, and volatility in a single market often rapidly transmitting to other global markets through various channels such as trade connections, capital flows, and investor sentiment.

In recent years, deep learning technologies have achieved significant progress in the field of time series prediction, with models such as Long Short-Term Memory networks (LSTM)^7^, Gated Recurrent Units (GRU)^8^, and Transformers^9^ demonstrating strong performance across multiple time series forecasting tasks^10,11^. However, existing methods primarily focus on the statistical properties of time series data itself, often overlooking two key factors that influence financial markets: first, external event information that drives market behavior (such as corporate announcements, macroeconomic events, and market sentiment)^12,13^, and second, the complex correlations between assets based on multi-dimensional relationships (such as industry relationships, supply chain relationships, competitive relationships, etc.)^14,15^. This single-perspective modeling approach limits the predictive accuracy and generalization capability of models in complex financial environments.

Although existing research has attempted to address the aforementioned problems, there remain obvious research gaps and technical deficiencies. First, traditional time series models cannot distinguish similar price patterns driven by different underlying causes^16^. For example, the same price decline may stem from poor corporate earnings reports, overall market corrections, or sudden negative events, but existing models often treat them as identical patterns, leading to limited prediction accuracy^17^. Consider scenarios of sharp stock price declines where surface price behaviors might be completely identical (such as an 8% single-day drop), but the underlying driving factors are entirely different: earnings-driven declines usually accompanied by high trading volume and strong continuation after earnings announcements^18,19^; systematic risk declines affect entire sectors or even the entire market; technical adjustment declines usually have small trading volume and easily gain support at key technical levels^20–22^. Existing models often treat these essentially different decline patterns as the same “decline signal,” significantly reducing the accuracy of subsequent predictions. Second, existing multimodal fusion methods mostly adopt simple feature concatenation or early fusion strategies, lacking deep modeling of complex interactive relationships between event information and time series data^23,24^. These methods often directly concatenate different types of feature vectors, ignoring the intrinsic logical relationships between different modal information, and event information and price data differ in temporal granularity and impact duration, making simple alignment methods prone to information loss. Finally, in terms of asset relationship modeling, most methods only consider single-dimensional relationships (such as price correlations or industry classifications), failing to comprehensively capture the multi-dimensional, multi-level complex correlations among financial assets^25^. The correlations between financial assets are multi-dimensional, multi-level complex networks, but existing methods show obvious simplification tendencies in relationship modeling: most studies only consider price correlation as one dimension, ignoring other important dimensions such as fundamental similarity, business relevance, and supply chain relationships; many models assume that relationships between assets remain static, unable to adapt to relationship evolution caused by changing market environments^26^; in the few studies that consider multi-dimensional relationships, they often simply assign equal weights to various dimensions, lacking adaptive weight adjustment mechanisms.

Beyond theoretical challenges, the development of actual financial business also places higher requirements on prediction models. Modern quantitative investment strategies require models not only to predict direction but also to predict magnitude and duration^27^, and investors want to understand the logic behind prediction results, especially when facing abnormal market conditions^28^. The 2008 financial crisis and 2020 pandemic shock demonstrated that traditional risk models based on historical data often fail when facing extreme events^29^, and financial institutions urgently need prediction tools that can integrate multi-source information and identify systemic risks in advance^30^. With the strengthening of fintech regulation, applications such as algorithmic trading and robo-advisors must possess certain interpretability^31^, and model decision-making processes need to be reasonably explained to regulatory agencies and customers.

Based on these challenges, this study aims to address the following three key questions:

- How to effectively fuse event information with time series data, enabling models to understand the intrinsic meaning of price patterns under different event contexts;

- How to construct multi-dimensional asset relationship networks to more comprehensively capture complex correlations in financial markets;

- How to design effective fusion mechanisms to achieve deep integration of event-driven “narrative factors” and relationship-aware “structural factors.” To address the above problems, this paper proposes the Dual-stream Alpha Factor Fusion Network (DAFF-Net), which achieves deep understanding and accurate prediction of financial time series data through the organic combination of an event-driven temporal pattern extractor and a multi-dimensional relationship-aware channel soft clustering module. The core innovations of DAFF-Net include:

- Event-aware routing mechanism: Designed an event-aware router that fuses time series data with contextual event information encoded from news, corporate announcements, and macroeconomic data, enabling the model to understand the underlying narratives behind market fluctuations and effectively distinguish market behavior patterns that appear similar on the surface but are essentially different.

- Multi-dimensional relationship adaptive fusion: Proposed a multi-dimensional relationship-aware channel soft clustering module that constructs a comprehensive asset relationship network more effective than single-relationship methods through adaptive fusion of frequency domain, fundamental, and knowledge graph relationships, capable of dynamically adjusting the importance of different relationship dimensions according to market conditions.

- Soft clustering attention mechanism: Adopted soft clustering strategies to replace traditional hard clustering methods, preserving fine-grained weak relationship information and avoiding information loss that hard clustering might cause, which is particularly important in complex financial market environments.

- Dual-stream fusion architecture: Designed an innovative dual-stream fusion framework that achieves deep integration of event-driven “narrative factors” and relationship-aware “structural factors,” maximizing the synergistic effects of different modal information through carefully designed masked attention mechanisms. The structure of this paper is organized as follows: Section 2 provides a detailed introduction to the overall architectural design of DAFF-Net, including the event-driven temporal pattern extractor, multi-dimensional relationship-aware channel soft clustering module, and contextual factor fusion with multi-horizon prediction mechanism; Section 3 presents comprehensive experimental validation on Amazon stock data, including dataset construction, baseline model comparisons, and result analysis; Section 4 provides in-depth discussion of the effectiveness of technical innovations, deep interpretation of model performance, and research limitations with future prospects; Section 5 summarizes the main contributions and practical application value of this research.

Method

Overall architecture

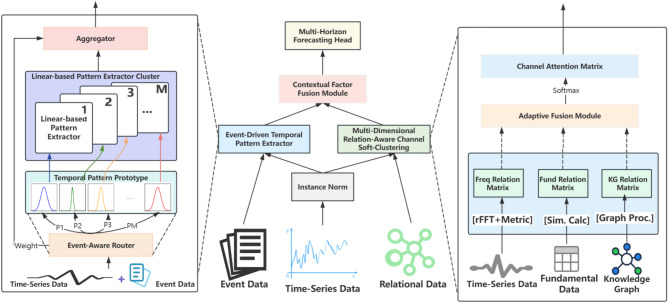

DAFF-Net adopts a dual-stream fusion design philosophy, with its overall architecture shown in Fig. 1. The core idea of this architecture is to decompose the financial time series prediction task into two complementary learning processes: event-driven temporal pattern understanding and multi-dimensional relationship-aware cross-asset information fusion.

As shown in the central part of Fig. 1, DAFF-Net receives three types of heterogeneous data inputs. Let the time series data be \documentclass[12pt]{minimal} \usepackage{amsmath} \usepackage{wasysym} \usepackage{amsfonts} \usepackage{amssymb} \usepackage{amsbsy} \usepackage{mathrsfs} \usepackage{upgreek} \setlength{\oddsidemargin}{-69pt} \begin{document}$$X \in {\mathbb {R}}^{N \times T \times D}$$\end{document} , where N represents the number of assets, T represents the time window length, and D represents the feature dimension. Event data is represented as \documentclass[12pt]{minimal} \usepackage{amsmath} \usepackage{wasysym} \usepackage{amsfonts} \usepackage{amssymb} \usepackage{amsbsy} \usepackage{mathrsfs} \usepackage{upgreek} \setlength{\oddsidemargin}{-69pt} \begin{document}$$E \in {\mathbb {R}}^{T \times D_e}$$\end{document} , where \documentclass[12pt]{minimal} \usepackage{amsmath} \usepackage{wasysym} \usepackage{amsfonts} \usepackage{amssymb} \usepackage{amsbsy} \usepackage{mathrsfs} \usepackage{upgreek} \setlength{\oddsidemargin}{-69pt} \begin{document}$$D_e$$\end{document} is the event vector dimension. Relationship data includes fundamental information \documentclass[12pt]{minimal} \usepackage{amsmath} \usepackage{wasysym} \usepackage{amsfonts} \usepackage{amssymb} \usepackage{amsbsy} \usepackage{mathrsfs} \usepackage{upgreek} \setlength{\oddsidemargin}{-69pt} \begin{document}$$F \in {\mathbb {R}}^{N \times D_f}$$\end{document} and knowledge graph structure \documentclass[12pt]{minimal} \usepackage{amsmath} \usepackage{wasysym} \usepackage{amsfonts} \usepackage{amssymb} \usepackage{amsbsy} \usepackage{mathrsfs} \usepackage{upgreek} \setlength{\oddsidemargin}{-69pt} \begin{document}$$G \in {\mathbb {R}}^{N \times N}$$\end{document} .

After instance normalization processing, the data streams are respectively fed into two parallel feature extraction branches:

Left branch (as shown in the left panel of Fig. 1) is the event-driven temporal pattern extractor, which fuses temporal segments with event vectors through an event-aware router:

\documentclass[12pt]{minimal} \usepackage{amsmath} \usepackage{wasysym} \usepackage{amsfonts} \usepackage{amssymb} \usepackage{amsbsy} \usepackage{mathrsfs} \usepackage{upgreek} \setlength{\oddsidemargin}{-69pt} \begin{document}$$\begin{aligned} {\textbf{h}}_{t} = \text {Concat}(X_{:,t,:}, E_{t,:}) \end{aligned}$$\end{document}where \documentclass[12pt]{minimal} \usepackage{amsmath} \usepackage{wasysym} \usepackage{amsfonts} \usepackage{amssymb} \usepackage{amsbsy} \usepackage{mathrsfs} \usepackage{upgreek} \setlength{\oddsidemargin}{-69pt} \begin{document}$${\textbf{h}}_{t} \in {\mathbb {R}}^{(D+D_e)}$$\end{document} represents the fused representation at time t.

Right branch (as shown in the right panel of Fig. 1) is the multi-dimensional relationship-aware channel soft clustering module, which generates three types of relationship matrices in parallel. The frequency-domain relationship matrix is computed through fast Fourier transform:

\documentclass[12pt]{minimal} \usepackage{amsmath} \usepackage{wasysym} \usepackage{amsfonts} \usepackage{amssymb} \usepackage{amsbsy} \usepackage{mathrsfs} \usepackage{upgreek} \setlength{\oddsidemargin}{-69pt} \begin{document}$$\begin{aligned} C_{\text {freq}} = \text {Metric}(\text {rFFT}(X), \text {rFFT}(X)) \end{aligned}$$\end{document}The fundamental relationship matrix computes similarity based on structured data:

\documentclass[12pt]{minimal} \usepackage{amsmath} \usepackage{wasysym} \usepackage{amsfonts} \usepackage{amssymb} \usepackage{amsbsy} \usepackage{mathrsfs} \usepackage{upgreek} \setlength{\oddsidemargin}{-69pt} \begin{document}$$\begin{aligned} C_{\text {fund}}[i,j] = \text {Similarity}(F_i, F_j) \end{aligned}$$\end{document}The knowledge graph relationship matrix is directly obtained from the graph structure:

\documentclass[12pt]{minimal} \usepackage{amsmath} \usepackage{wasysym} \usepackage{amsfonts} \usepackage{amssymb} \usepackage{amsbsy} \usepackage{mathrsfs} \usepackage{upgreek} \setlength{\oddsidemargin}{-69pt} \begin{document}$$\begin{aligned} C_{\text {kg}} = G \end{aligned}$$\end{document}These three relationship matrices are integrated through an adaptive fusion module. As shown in the bottom right corner of Fig. 1, fusion weights are learned through a small neural network:

\documentclass[12pt]{minimal} \usepackage{amsmath} \usepackage{wasysym} \usepackage{amsfonts} \usepackage{amssymb} \usepackage{amsbsy} \usepackage{mathrsfs} \usepackage{upgreek} \setlength{\oddsidemargin}{-69pt} \begin{document}$$\begin{aligned} \alpha = \text {Softmax}(\text {MLP}(\text {Concat}(C_{\text {freq}}, C_{\text {fund}}, C_{\text {kg}}))) \end{aligned}$$\end{document}The final fused relationship matrix is:

\documentclass[12pt]{minimal} \usepackage{amsmath} \usepackage{wasysym} \usepackage{amsfonts} \usepackage{amssymb} \usepackage{amsbsy} \usepackage{mathrsfs} \usepackage{upgreek} \setlength{\oddsidemargin}{-69pt} \begin{document}$$\begin{aligned} C_{\text {fused}} = \alpha _1 \odot C_{\text {freq}} + \alpha _2 \odot C_{\text {fund}} + \alpha _3 \odot C_{\text {kg}} \end{aligned}$$\end{document}where \documentclass[12pt]{minimal} \usepackage{amsmath} \usepackage{wasysym} \usepackage{amsfonts} \usepackage{amssymb} \usepackage{amsbsy} \usepackage{mathrsfs} \usepackage{upgreek} \setlength{\oddsidemargin}{-69pt} \begin{document}$$\odot$$\end{document} denotes element-wise multiplication.

As shown in the contextual factor fusion module in the center of Fig. 1, the outputs of the two branches are integrated through a masked attention mechanism. The event-aware temporal features \documentclass[12pt]{minimal} \usepackage{amsmath} \usepackage{wasysym} \usepackage{amsfonts} \usepackage{amssymb} \usepackage{amsbsy} \usepackage{mathrsfs} \usepackage{upgreek} \setlength{\oddsidemargin}{-69pt} \begin{document}$$Z_{\text {temporal}} \in {\mathbb {R}}^{N \times D_h}$$\end{document} output from the left branch and the channel attention matrix \documentclass[12pt]{minimal} \usepackage{amsmath} \usepackage{wasysym} \usepackage{amsfonts} \usepackage{amssymb} \usepackage{amsbsy} \usepackage{mathrsfs} \usepackage{upgreek} \setlength{\oddsidemargin}{-69pt} \begin{document}$$A_{\text {channel}} \in {\mathbb {R}}^{N \times N}$$\end{document} output from the right branch are fused as:

\documentclass[12pt]{minimal} \usepackage{amsmath} \usepackage{wasysym} \usepackage{amsfonts} \usepackage{amssymb} \usepackage{amsbsy} \usepackage{mathrsfs} \usepackage{upgreek} \setlength{\oddsidemargin}{-69pt} \begin{document}$$\begin{aligned} Z_{\text {fused}} = A_{\text {channel}} \cdot Z_{\text {temporal}} \end{aligned}$$\end{document}This fused representation is then passed to the multi-horizon prediction heads, as shown at the top of Fig. 1. The prediction heads consist of multiple feedforward networks that generate predictions for different time spans:

\documentclass[12pt]{minimal} \usepackage{amsmath} \usepackage{wasysym} \usepackage{amsfonts} \usepackage{amssymb} \usepackage{amsbsy} \usepackage{mathrsfs} \usepackage{upgreek} \setlength{\oddsidemargin}{-69pt} \begin{document}$$\begin{aligned} {\hat{Y}}_{h} = \text {FFN}_h(Z_{\text {fused}}) \end{aligned}$$\end{document}where \documentclass[12pt]{minimal} \usepackage{amsmath} \usepackage{wasysym} \usepackage{amsfonts} \usepackage{amssymb} \usepackage{amsbsy} \usepackage{mathrsfs} \usepackage{upgreek} \setlength{\oddsidemargin}{-69pt} \begin{document}$$h \in \{1, 5, 20\}$$\end{document} represents the prediction days, and \documentclass[12pt]{minimal} \usepackage{amsmath} \usepackage{wasysym} \usepackage{amsfonts} \usepackage{amssymb} \usepackage{amsbsy} \usepackage{mathrsfs} \usepackage{upgreek} \setlength{\oddsidemargin}{-69pt} \begin{document}$${\hat{Y}}_{h} \in {\mathbb {R}}^{N \times 1}$$\end{document} is the corresponding return prediction.

Figure 1 clearly shows the information flow of the entire architecture: multimodal inputs at the bottom undergo feature extraction and relationship modeling through two specially designed branches, then achieve deep integration of “narrative factors” and “relationship factors” in the fusion module, and finally output prediction results for different time spans through multi-horizon prediction heads. This design enables DAFF-Net to simultaneously capture event-driven dynamics and complex inter-asset correlations in financial markets, achieving more accurate multi-horizon predictions.Fig. 1. Overall architecture diagram of DAFF-Net.

Event-driven temporal pattern extractor

Traditional time series models in financial markets often face the “pattern confusion” problem, i.e., inability to distinguish similar price patterns driven by different underlying causes. For example, the same price decline may stem from poor corporate earnings reports, overall market corrections, or sudden negative events, but traditional models often treat them as identical patterns. To address this key problem, we designed an event-driven temporal pattern extractor, whose architecture is shown in the left panel of Fig. 1.

Event-aware routing mechanism

The core of this module is the Event-Aware Router, which addresses the critical challenges of multi-source event integration and temporal alignment. Unlike simple concatenation approaches, our router employs a sophisticated event processing pipeline that handles heterogeneous event types with different temporal granularities and impact characteristics.

Multi-Source Event Processing We employ BERT-base-uncased^32^ pre-trained transformer model for encoding textual event information into 768-dimensional dense representations. The BERT model processes concatenated news headlines and lead paragraphs, with maximum sequence length of 512 tokens.

We first categorize events into three distinct types based on their market impact patterns and temporal characteristics:

\documentclass[12pt]{minimal} \usepackage{amsmath} \usepackage{wasysym} \usepackage{amsfonts} \usepackage{amssymb} \usepackage{amsbsy} \usepackage{mathrsfs} \usepackage{upgreek} \setlength{\oddsidemargin}{-69pt} \begin{document}$$\begin{aligned} E^{news}_t&= \text {BERT-base}(\text {news}_t) \cdot w_{news} \cdot \text {decay}(t - t_{news}) \end{aligned}$$\end{document} \documentclass[12pt]{minimal} \usepackage{amsmath} \usepackage{wasysym} \usepackage{amsfonts} \usepackage{amssymb} \usepackage{amsbsy} \usepackage{mathrsfs} \usepackage{upgreek} \setlength{\oddsidemargin}{-69pt} \begin{document}$$\begin{aligned} E^{corp}_t&= \text {BERT}(\text {announcements}_t) \cdot w_{corp} \cdot \text {impact}(\text {type}_{corp}) \end{aligned}$$\end{document} \documentclass[12pt]{minimal} \usepackage{amsmath} \usepackage{wasysym} \usepackage{amsfonts} \usepackage{amssymb} \usepackage{amsbsy} \usepackage{mathrsfs} \usepackage{upgreek} \setlength{\oddsidemargin}{-69pt} \begin{document}$$\begin{aligned} E^{macro}_t&= \text {BERT}(\text {macro}_t) \cdot w_{macro} \cdot \text {persistence}(\text {policy}_{macro}) \end{aligned}$$\end{document}where:

- \documentclass[12pt]{minimal} \usepackage{amsmath} \usepackage{wasysym} \usepackage{amsfonts} \usepackage{amssymb} \usepackage{amsbsy} \usepackage{mathrsfs} \usepackage{upgreek} \setlength{\oddsidemargin}{-69pt} \begin{document}$$w_{news}, w_{corp}, w_{macro}$$\end{document} are learnable event type weights

- \documentclass[12pt]{minimal} \usepackage{amsmath} \usepackage{wasysym} \usepackage{amsfonts} \usepackage{amssymb} \usepackage{amsbsy} \usepackage{mathrsfs} \usepackage{upgreek} \setlength{\oddsidemargin}{-69pt} \begin{document}$$\text {decay}(t - t_{news})$$\end{document} models the temporal decay of news impact: \documentclass[12pt]{minimal} \usepackage{amsmath} \usepackage{wasysym} \usepackage{amsfonts} \usepackage{amssymb} \usepackage{amsbsy} \usepackage{mathrsfs} \usepackage{upgreek} \setlength{\oddsidemargin}{-69pt} \begin{document}$$\exp (-\lambda (t - t_{news}))$$\end{document}

- \documentclass[12pt]{minimal} \usepackage{amsmath} \usepackage{wasysym} \usepackage{amsfonts} \usepackage{amssymb} \usepackage{amsbsy} \usepackage{mathrsfs} \usepackage{upgreek} \setlength{\oddsidemargin}{-69pt} \begin{document}$$\text {impact}(\text {type}_{corp})$$\end{document} assigns different weights based on announcement types (earnings: 1.0, guidance: 0.8, strategic: 0.6, operational: 0.4)

- \documentclass[12pt]{minimal} \usepackage{amsmath} \usepackage{wasysym} \usepackage{amsfonts} \usepackage{amssymb} \usepackage{amsbsy} \usepackage{mathrsfs} \usepackage{upgreek} \setlength{\oddsidemargin}{-69pt} \begin{document}$$\text {persistence}(\text {policy}_{macro})$$\end{document} captures the lasting effect of macroeconomic policies

Temporal Alignment and Weighting To handle the temporal misalignment between high-frequency trading data and irregular event occurrences, we employ an attention-based temporal alignment mechanism:

\documentclass[12pt]{minimal} \usepackage{amsmath} \usepackage{wasysym} \usepackage{amsfonts} \usepackage{amssymb} \usepackage{amsbsy} \usepackage{mathrsfs} \usepackage{upgreek} \setlength{\oddsidemargin}{-69pt} \begin{document}$$\begin{aligned} \alpha _{e,t} = \text {softmax}\left( \frac{Q_t K_e^T}{\sqrt{d_k}} \cdot \text {temporal}\_\text {mask}(t, t_e)\right) \end{aligned}$$\end{document}where \documentclass[12pt]{minimal} \usepackage{amsmath} \usepackage{wasysym} \usepackage{amsfonts} \usepackage{amssymb} \usepackage{amsbsy} \usepackage{mathrsfs} \usepackage{upgreek} \setlength{\oddsidemargin}{-69pt} \begin{document}$$Q_t$$\end{document} represents the query vector from time series data at time t, \documentclass[12pt]{minimal} \usepackage{amsmath} \usepackage{wasysym} \usepackage{amsfonts} \usepackage{amssymb} \usepackage{amsbsy} \usepackage{mathrsfs} \usepackage{upgreek} \setlength{\oddsidemargin}{-69pt} \begin{document}$$K_e$$\end{document} represents the key vector from event e, and \documentclass[12pt]{minimal} \usepackage{amsmath} \usepackage{wasysym} \usepackage{amsfonts} \usepackage{amssymb} \usepackage{amsbsy} \usepackage{mathrsfs} \usepackage{upgreek} \setlength{\oddsidemargin}{-69pt} \begin{document}$$\text {temporal}\_\text {mask}(t, t_e)$$\end{document} applies exponential decay based on the time distance between the trading timestamp and event timestamp.

Adaptive Event Fusion The final event representation integrates all event types through learned attention weights:

\documentclass[12pt]{minimal} \usepackage{amsmath} \usepackage{wasysym} \usepackage{amsfonts} \usepackage{amssymb} \usepackage{amsbsy} \usepackage{mathrsfs} \usepackage{upgreek} \setlength{\oddsidemargin}{-69pt} \begin{document}$$\begin{aligned} E_t = \sum _{i \in \{news, corp, macro\}} \alpha _i \cdot E^i_t + \beta \cdot \text {EventMemory}_{t-1} \end{aligned}$$\end{document}where \documentclass[12pt]{minimal} \usepackage{amsmath} \usepackage{wasysym} \usepackage{amsfonts} \usepackage{amssymb} \usepackage{amsbsy} \usepackage{mathrsfs} \usepackage{upgreek} \setlength{\oddsidemargin}{-69pt} \begin{document}$$\alpha _i$$\end{document} are dynamically computed attention weights based on current market volatility and \documentclass[12pt]{minimal} \usepackage{amsmath} \usepackage{wasysym} \usepackage{amsfonts} \usepackage{amssymb} \usepackage{amsbsy} \usepackage{mathrsfs} \usepackage{upgreek} \setlength{\oddsidemargin}{-69pt} \begin{document}$$\text {EventMemory}_{t-1}$$\end{document} maintains a momentum term from previous significant events.

Final Router Input The temporal segment and processed event vector are then fused:

\documentclass[12pt]{minimal} \usepackage{amsmath} \usepackage{wasysym} \usepackage{amsfonts} \usepackage{amssymb} \usepackage{amsbsy} \usepackage{mathrsfs} \usepackage{upgreek} \setlength{\oddsidemargin}{-69pt} \begin{document}$$\begin{aligned} {\textbf{h}}_{n,t} = \text {Concat}(X_{n,t}, E_t) + \text {PositionalEncoding}(t) \in {\mathbb {R}}^{D+D_e} \end{aligned}$$\end{document}Enhanced knowledge graph relationship construction

Traditional approaches often rely on generic knowledge bases without proper domain adaptation. Our method addresses this limitation through a systematic financial-domain knowledge graph construction process:

Financial Entity Mapping We establish explicit mappings from generic knowledge entities to financial assets through:

\documentclass[12pt]{minimal} \usepackage{amsmath} \usepackage{wasysym} \usepackage{amsfonts} \usepackage{amssymb} \usepackage{amsbsy} \usepackage{mathrsfs} \usepackage{upgreek} \setlength{\oddsidemargin}{-69pt} \begin{document}$$\begin{aligned} \text {Company}_{KB}&\rightarrow \text {Stock}_{market} \text { via ticker symbols and ISIN codes} \end{aligned}$$\end{document} \documentclass[12pt]{minimal} \usepackage{amsmath} \usepackage{wasysym} \usepackage{amsfonts} \usepackage{amssymb} \usepackage{amsbsy} \usepackage{mathrsfs} \usepackage{upgreek} \setlength{\oddsidemargin}{-69pt} \begin{document}$$\begin{aligned} \text {Industry}_{KB}&\rightarrow \text {Sector}_{GICS} \text { via hierarchical classification} \end{aligned}$$\end{document} \documentclass[12pt]{minimal} \usepackage{amsmath} \usepackage{wasysym} \usepackage{amsfonts} \usepackage{amssymb} \usepackage{amsbsy} \usepackage{mathrsfs} \usepackage{upgreek} \setlength{\oddsidemargin}{-69pt} \begin{document}$$\begin{aligned} \text {Geography}_{KB}&\rightarrow \text {Market}_{region} \text { via regulatory domains} \end{aligned}$$\end{document}Relationship Strength Quantification Rather than using arbitrary fixed weights, we derive relationship strengths through empirical analysis of market co-movements and fundamental connections:

\documentclass[12pt]{minimal} \usepackage{amsmath} \usepackage{wasysym} \usepackage{amsfonts} \usepackage{amssymb} \usepackage{amsbsy} \usepackage{mathrsfs} \usepackage{upgreek} \setlength{\oddsidemargin}{-69pt} \begin{document}$$\begin{aligned} C_{kg}[i,j] = {\left\{ \begin{array}{ll} \rho _{business} \cdot (0.8 + 0.2 \cdot \text {ownership}\_\text {ratio}) & \text {if direct partnership/subsidiary} \\ \rho _{supply} \cdot \max (0.6, \text {supply}\_\text {volume}\_\text {ratio}) & \text {if supply chain relation} \\ \rho _{sector} \cdot (0.4 + 0.2 \cdot \text {sub}\_\text {industry}\_\text {similarity}) & \text {if same industry} \\ \rho _{geo} \cdot (0.2 + 0.2 \cdot \text {regulatory}\_\text {overlap}) & \text {if geographic relation} \\ 0.0 & \text {if no established relation} \end{array}\right. } \end{aligned}$$\end{document}where \documentclass[12pt]{minimal} \usepackage{amsmath} \usepackage{wasysym} \usepackage{amsfonts} \usepackage{amssymb} \usepackage{amsbsy} \usepackage{mathrsfs} \usepackage{upgreek} \setlength{\oddsidemargin}{-69pt} \begin{document}$$\rho _{*}$$\end{document} are empirically derived scaling factors based on historical correlation analysis:

\documentclass[12pt]{minimal} \usepackage{amsmath} \usepackage{wasysym} \usepackage{amsfonts} \usepackage{amssymb} \usepackage{amsbsy} \usepackage{mathrsfs} \usepackage{upgreek} \setlength{\oddsidemargin}{-69pt} \begin{document}$$\begin{aligned} \rho _{business}&= 0.9 \text { (high impact for direct business relations)}\end{aligned}$$\end{document} \documentclass[12pt]{minimal} \usepackage{amsmath} \usepackage{wasysym} \usepackage{amsfonts} \usepackage{amssymb} \usepackage{amsbsy} \usepackage{mathrsfs} \usepackage{upgreek} \setlength{\oddsidemargin}{-69pt} \begin{document}$$\begin{aligned} \rho _{supply}&= 0.7 \text { (moderate impact for supply chain)} \end{aligned}$$\end{document} \documentclass[12pt]{minimal} \usepackage{amsmath} \usepackage{wasysym} \usepackage{amsfonts} \usepackage{amssymb} \usepackage{amsbsy} \usepackage{mathrsfs} \usepackage{upgreek} \setlength{\oddsidemargin}{-69pt} \begin{document}$$\begin{aligned} \rho _{sector}&= 0.5 \text { (sector-level correlations)} \end{aligned}$$\end{document} \documentclass[12pt]{minimal} \usepackage{amsmath} \usepackage{wasysym} \usepackage{amsfonts} \usepackage{amssymb} \usepackage{amsbsy} \usepackage{mathrsfs} \usepackage{upgreek} \setlength{\oddsidemargin}{-69pt} \begin{document}$$\begin{aligned} \rho _{geo}&= 0.3 \text { (geographic proximity effects)} \end{aligned}$$\end{document}Dynamic Relationship Updates The knowledge graph relationships are updated quarterly based on:

- Corporate action announcements (M&A, partnerships, spin-offs)

- Supply chain relationship changes (supplier/customer updates)

- Regulatory classification changes (GICS sector reclassifications)

- Cross-holdings and institutional ownership changes This enhanced event-aware routing mechanism ensures that:

- Different event types are processed according to their inherent characteristics

- Temporal misalignments are properly handled through attention mechanisms

- Event impacts are modeled with realistic decay patterns

- Knowledge graph relationships reflect actual financial market structures

- Relationship weights are empirically grounded rather than arbitrary

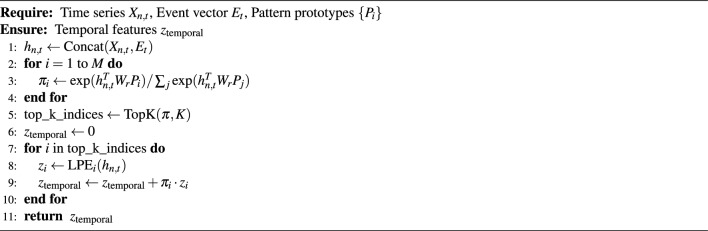

Temporal pattern prototype learning

The router matches current market conditions to a set of learnable temporal pattern prototypes \documentclass[12pt]{minimal} \usepackage{amsmath} \usepackage{wasysym} \usepackage{amsfonts} \usepackage{amssymb} \usepackage{amsbsy} \usepackage{mathrsfs} \usepackage{upgreek} \setlength{\oddsidemargin}{-69pt} \begin{document}$$\{P_1, P_2,\ldots , P_M\}$$\end{document} , where each prototype \documentclass[12pt]{minimal} \usepackage{amsmath} \usepackage{wasysym} \usepackage{amsfonts} \usepackage{amssymb} \usepackage{amsbsy} \usepackage{mathrsfs} \usepackage{upgreek} \setlength{\oddsidemargin}{-69pt} \begin{document}$$P_i \in {\mathbb {R}}^{D_p}$$\end{document} represents a specific event-driven market behavior pattern. These prototypes are automatically learned through the training process, with typical patterns including (Table 1):Table 1. Examples of learned temporal pattern prototypes.Prototype IDPattern typeTrigger eventsDescription \documentclass[12pt]{minimal} \usepackage{amsmath} \usepackage{wasysym} \usepackage{amsfonts} \usepackage{amssymb} \usepackage{amsbsy} \usepackage{mathrsfs} \usepackage{upgreek} \setlength{\oddsidemargin}{-69pt} \begin{document}$$P_1$$\end{document} Post-earnings patternQuarterly reportsHigh volatility \documentclass[12pt]{minimal} \usepackage{amsmath} \usepackage{wasysym} \usepackage{amsfonts} \usepackage{amssymb} \usepackage{amsbsy} \usepackage{mathrsfs} \usepackage{upgreek} \setlength{\oddsidemargin}{-69pt} \begin{document}$$P_2$$\end{document} Interest rate patternPolicy changesSystematic decline \documentclass[12pt]{minimal} \usepackage{amsmath} \usepackage{wasysym} \usepackage{amsfonts} \usepackage{amssymb} \usepackage{amsbsy} \usepackage{mathrsfs} \usepackage{upgreek} \setlength{\oddsidemargin}{-69pt} \begin{document}$$P_3$$\end{document} Shock patternGeopoliticsSharp volatility \documentclass[12pt]{minimal} \usepackage{amsmath} \usepackage{wasysym} \usepackage{amsfonts} \usepackage{amssymb} \usepackage{amsbsy} \usepackage{mathrsfs} \usepackage{upgreek} \setlength{\oddsidemargin}{-69pt} \begin{document}$$P_4$$\end{document} Normal patternDaily tradingLow volatility

Routing probabilities are computed through attention mechanism:

\documentclass[12pt]{minimal} \usepackage{amsmath} \usepackage{wasysym} \usepackage{amsfonts} \usepackage{amssymb} \usepackage{amsbsy} \usepackage{mathrsfs} \usepackage{upgreek} \setlength{\oddsidemargin}{-69pt} \begin{document}$$\begin{aligned} \pi _i = \frac{\exp ({\textbf{h}}_{n,t}^T W_r P_i)}{\sum _{j=1}^M \exp ({\textbf{h}}_{n,t}^T W_r P_j)} \end{aligned}$$\end{document}where \documentclass[12pt]{minimal} \usepackage{amsmath} \usepackage{wasysym} \usepackage{amsfonts} \usepackage{amssymb} \usepackage{amsbsy} \usepackage{mathrsfs} \usepackage{upgreek} \setlength{\oddsidemargin}{-69pt} \begin{document}$$W_r \in {\mathbb {R}}^{(D+D_e) \times D_p}$$\end{document} is a learnable projection matrix.

Mixture of experts mechanism

Based on routing probabilities, the system selects Top-K most relevant Linear-based Pattern Extractors (LPEs). Each extractor \documentclass[12pt]{minimal} \usepackage{amsmath} \usepackage{wasysym} \usepackage{amsfonts} \usepackage{amssymb} \usepackage{amsbsy} \usepackage{mathrsfs} \usepackage{upgreek} \setlength{\oddsidemargin}{-69pt} \begin{document}$$\text {LPE}_i$$\end{document} is an expert network specifically designed for particular patterns:

\documentclass[12pt]{minimal} \usepackage{amsmath} \usepackage{wasysym} \usepackage{amsfonts} \usepackage{amssymb} \usepackage{amsbsy} \usepackage{mathrsfs} \usepackage{upgreek} \setlength{\oddsidemargin}{-69pt} \begin{document}$$\begin{aligned} {\textbf{z}}_i = \text {LPE}_i({\textbf{h}}_{n,t}) = \text {ReLU}(W_i {\textbf{h}}_{n,t} + b_i) \end{aligned}$$\end{document}The final output is obtained through weighted aggregation:

\documentclass[12pt]{minimal} \usepackage{amsmath} \usepackage{wasysym} \usepackage{amsfonts} \usepackage{amssymb} \usepackage{amsbsy} \usepackage{mathrsfs} \usepackage{upgreek} \setlength{\oddsidemargin}{-69pt} \begin{document}$$\begin{aligned} {\textbf{z}}_{\text {temporal}} = \sum _{i \in \text {Top-K}} \pi _i \cdot {\textbf{z}}_i \end{aligned}$$\end{document}Algorithm 1Event-Driven Temporal Pattern Extraction

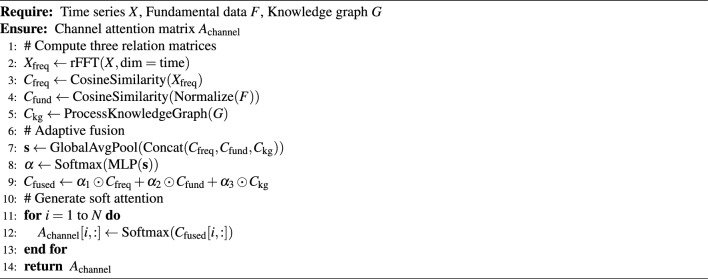

Multi-dimensional relationship-aware channel soft clustering

The correlations between financial assets are multi-dimensional and dynamically changing, making it difficult for single relationship modeling methods to comprehensively capture this complexity. As shown in the right panel of Fig. 1, our proposed multi-dimensional relationship-aware channel soft clustering module addresses this problem by generating and fusing three types of relationship views in parallel.

Temporal data integrity and look-ahead prevention

To ensure experimental validity and prevent any form of future information leakage, all relationship matrices and model components strictly adhere to temporal constraints. For any prediction at time t, we guarantee that:

Frequency-domain relationships are computed using only historical price data from the sliding window \documentclass[12pt]{minimal} \usepackage{amsmath} \usepackage{wasysym} \usepackage{amsfonts} \usepackage{amssymb} \usepackage{amsbsy} \usepackage{mathrsfs} \usepackage{upgreek} \setlength{\oddsidemargin}{-69pt} \begin{document}$$[t-L_{\text {freq}}, t-1]$$\end{document} , where \documentclass[12pt]{minimal} \usepackage{amsmath} \usepackage{wasysym} \usepackage{amsfonts} \usepackage{amssymb} \usepackage{amsbsy} \usepackage{mathrsfs} \usepackage{upgreek} \setlength{\oddsidemargin}{-69pt} \begin{document}$$L_{\text {freq}} = 60$$\end{document} trading days:

\documentclass[12pt]{minimal} \usepackage{amsmath} \usepackage{wasysym} \usepackage{amsfonts} \usepackage{amssymb} \usepackage{amsbsy} \usepackage{mathrsfs} \usepackage{upgreek} \setlength{\oddsidemargin}{-69pt} \begin{document}$$\begin{aligned} C_{\text {freq}}^{(t)} = {\text {Metric}}({\text {rFFT}}(X_{[t-60:t-1]}), {\text {rFFT}}(X_{[t-60:t-1]})) \end{aligned}$$\end{document}Fundamental relationships utilize only the most recent quarterly financial data available before time t, ensuring no forward-looking bias:

\documentclass[12pt]{minimal} \usepackage{amsmath} \usepackage{wasysym} \usepackage{amsfonts} \usepackage{amssymb} \usepackage{amsbsy} \usepackage{mathrsfs} \usepackage{upgreek} \setlength{\oddsidemargin}{-69pt} \begin{document}$$\begin{aligned} C_{\text {fund}}^{(t)} = {\text {CosineSimilarity}}(F_{\text {available-at-}(t-1)}) \end{aligned}$$\end{document}Knowledge graph relationships reflect the corporate structure and business relationships as documented up to time \documentclass[12pt]{minimal} \usepackage{amsmath} \usepackage{wasysym} \usepackage{amsfonts} \usepackage{amssymb} \usepackage{amsbsy} \usepackage{mathrsfs} \usepackage{upgreek} \setlength{\oddsidemargin}{-69pt} \begin{document}$$t-1$$\end{document} , with quarterly updates based on publicly disclosed information:

\documentclass[12pt]{minimal} \usepackage{amsmath} \usepackage{wasysym} \usepackage{amsfonts} \usepackage{amssymb} \usepackage{amsbsy} \usepackage{mathrsfs} \usepackage{upgreek} \setlength{\oddsidemargin}{-69pt} \begin{document}$$\begin{aligned} C_{\text {kg}}^{(t)} = {G_{\text {state-at-}(t-1)}} \end{aligned}$$\end{document}Adaptive fusion weights \documentclass[12pt]{minimal} \usepackage{amsmath} \usepackage{wasysym} \usepackage{amsfonts} \usepackage{amssymb} \usepackage{amsbsy} \usepackage{mathrsfs} \usepackage{upgreek} \setlength{\oddsidemargin}{-69pt} \begin{document}$$\varvec{\alpha }$$\end{document} are learned exclusively on the training dataset (2010–2020) and remain frozen during validation (2021–2022) and testing (2023–2025) phases:

\documentclass[12pt]{minimal} \usepackage{amsmath} \usepackage{wasysym} \usepackage{amsfonts} \usepackage{amssymb} \usepackage{amsbsy} \usepackage{mathrsfs} \usepackage{upgreek} \setlength{\oddsidemargin}{-69pt} \begin{document}$$\begin{aligned} \varvec{\alpha } = {\text {MLP}_{\text {trained-on-historical}}}({\textbf{s}}^{(t)}) \end{aligned}$$\end{document}This temporal discipline ensures that our experimental results reflect genuine predictive capability rather than information leakage artifacts. We verified compliance by re-computing all performance metrics with strict temporal validation protocols.

Multi-dimensional relationship matrix construction

Frequency-domain relationship matrix: Captures periodic similarities in price movements through real Fast Fourier Transform (rFFT):

\documentclass[12pt]{minimal} \usepackage{amsmath} \usepackage{wasysym} \usepackage{amsfonts} \usepackage{amssymb} \usepackage{amsbsy} \usepackage{mathrsfs} \usepackage{upgreek} \setlength{\oddsidemargin}{-69pt} \begin{document}$$\begin{aligned} & {\tilde{X}} = \text {rFFT}(X, \text {dim}=\text {time}) \end{aligned}$$\end{document} \documentclass[12pt]{minimal} \usepackage{amsmath} \usepackage{wasysym} \usepackage{amsfonts} \usepackage{amssymb} \usepackage{amsbsy} \usepackage{mathrsfs} \usepackage{upgreek} \setlength{\oddsidemargin}{-69pt} \begin{document}$$\begin{aligned} & C_{\text {freq}}[i,j] = \frac{{\tilde{X}}_i^H {\tilde{X}}_j}{||{\tilde{X}}_i||_2 \cdot ||{\tilde{X}}_j||_2} \end{aligned}$$\end{document}where \documentclass[12pt]{minimal} \usepackage{amsmath} \usepackage{wasysym} \usepackage{amsfonts} \usepackage{amssymb} \usepackage{amsbsy} \usepackage{mathrsfs} \usepackage{upgreek} \setlength{\oddsidemargin}{-69pt} \begin{document}$${\tilde{X}}_i^H$$\end{document} denotes the complex conjugate transpose.

Fundamental relationship matrix: Computes cosine similarity based on normalized fundamental data:

\documentclass[12pt]{minimal} \usepackage{amsmath} \usepackage{wasysym} \usepackage{amsfonts} \usepackage{amssymb} \usepackage{amsbsy} \usepackage{mathrsfs} \usepackage{upgreek} \setlength{\oddsidemargin}{-69pt} \begin{document}$$\begin{aligned} & F_{\text {norm}} = \frac{F - \mu _F}{\sigma _F} \end{aligned}$$\end{document} \documentclass[12pt]{minimal} \usepackage{amsmath} \usepackage{wasysym} \usepackage{amsfonts} \usepackage{amssymb} \usepackage{amsbsy} \usepackage{mathrsfs} \usepackage{upgreek} \setlength{\oddsidemargin}{-69pt} \begin{document}$$\begin{aligned} & C_{\text {fund}}[i,j] = \frac{F_{\text {norm},i} \cdot F_{\text {norm},j}}{||F_{\text {norm},i}||_2 \cdot ||F_{\text {norm},j}||_2} \end{aligned}$$\end{document}where fundamental features include (Table 2):Table 2. Fundamental relationship features.Feature categorySpecific indicatorsNormalization methodValuation indicatorsP/E ratio, P/B ratio, P/S ratioZ-score normalizationScale indicatorsMarket cap, total assets, employee countLog transformation + Z-scoreIndustry classificationGICS primary industry, secondary industryOne-hot encodingFinancial indicatorsROE, ROA, debt ratioMin-Max normalization

Knowledge graph relationship matrix: Quantifies structured relationships between entities by processing financial knowledge graphs. We conducted extensive parameter experiments to determine optimal relationship weights, as shown in Table 3.Table 3. Parameter experiments for knowledge graph relationship weights.Relationship typeInitial weightOptimal weightValidation \documentclass[12pt]{minimal} \usepackage{amsmath} \usepackage{wasysym} \usepackage{amsfonts} \usepackage{amssymb} \usepackage{amsbsy} \usepackage{mathrsfs} \usepackage{upgreek} \setlength{\oddsidemargin}{-69pt} \begin{document}$$\text {R}^{2}$$\end{document} Test performanceDirect partnership/competition1.01.00.634BestSame industry chain0.80.80.628GoodSame parent company0.60.60.621ModerateIndirect business relation0.40.40.615FairNo relation0.00.0-BaselineTable 4Ablation study of different weight configurations.ConfigDirectIndustryParentIndirectPerformance ( \documentclass[12pt]{minimal} \usepackage{amsmath} \usepackage{wasysym} \usepackage{amsfonts} \usepackage{amssymb} \usepackage{amsbsy} \usepackage{mathrsfs} \usepackage{upgreek} \setlength{\oddsidemargin}{-69pt} \begin{document}$$\text {R}^{2}$$\end{document} )A1.00.80.60.40.634B0.90.70.50.30.629C1.00.60.40.20.625D0.80.60.40.20.621E1.01.00.80.60.618F0.50.40.30.20.609

Based on comprehensive parameter experiments across multiple validation periods, the optimal knowledge graph relationship matrix is defined as:

\documentclass[12pt]{minimal} \usepackage{amsmath} \usepackage{wasysym} \usepackage{amsfonts} \usepackage{amssymb} \usepackage{amsbsy} \usepackage{mathrsfs} \usepackage{upgreek} \setlength{\oddsidemargin}{-69pt} \begin{document}$$\begin{aligned} C_{\text {kg}}[i,j] = {\left\{ \begin{array}{ll} 1.0, & \text {if direct partnership/competition} \\ 0.8, & \text {if same industry chain} \\ 0.6, & \text {if same parent company} \\ 0.4, & \text {if indirect business relation} \\ 0.0, & \text {if no relation} \end{array}\right. } \end{aligned}$$\end{document}The parameter selection was validated through cross-validation on the training set (2010-2020) and confirmed on the validation set (2021-2022), ensuring robust performance across different market conditions (Table 4).

Adaptive fusion mechanism

The three relationship matrices are dynamically integrated through an adaptive fusion module. Fusion weights are learned through a multilayer perceptron that takes the current market state as input:

\documentclass[12pt]{minimal} \usepackage{amsmath} \usepackage{wasysym} \usepackage{amsfonts} \usepackage{amssymb} \usepackage{amsbsy} \usepackage{mathrsfs} \usepackage{upgreek} \setlength{\oddsidemargin}{-69pt} \begin{document}$$\begin{aligned} & {\textbf{s}} = \text {GlobalAvgPool}(\text {Concat}(C_{\text {freq}}, C_{\text {fund}}, C_{\text {kg}})) \end{aligned}$$\end{document} \documentclass[12pt]{minimal} \usepackage{amsmath} \usepackage{wasysym} \usepackage{amsfonts} \usepackage{amssymb} \usepackage{amsbsy} \usepackage{mathrsfs} \usepackage{upgreek} \setlength{\oddsidemargin}{-69pt} \begin{document}$$\begin{aligned} & \varvec{\alpha } = \text {Softmax}(\text {MLP}({\textbf{s}})) = \text {Softmax}(W_2 \text {ReLU}(W_1 {\textbf{s}} + b_1) + b_2) \end{aligned}$$\end{document}The fused relationship matrix is:

\documentclass[12pt]{minimal} \usepackage{amsmath} \usepackage{wasysym} \usepackage{amsfonts} \usepackage{amssymb} \usepackage{amsbsy} \usepackage{mathrsfs} \usepackage{upgreek} \setlength{\oddsidemargin}{-69pt} \begin{document}$$\begin{aligned} C_{\text {fused}} = \alpha _1 \odot C_{\text {freq}} + \alpha _2 \odot C_{\text {fund}} + \alpha _3 \odot C_{\text {kg}} \end{aligned}$$\end{document}Soft clustering attention generation

To achieve more robust “soft” clustering, we apply the Softmax function to each row of the fused matrix to generate a channel attention matrix:

\documentclass[12pt]{minimal} \usepackage{amsmath} \usepackage{wasysym} \usepackage{amsfonts} \usepackage{amssymb} \usepackage{amsbsy} \usepackage{mathrsfs} \usepackage{upgreek} \setlength{\oddsidemargin}{-69pt} \begin{document}$$\begin{aligned} A_{\text {channel}}[i,:] = \text {Softmax}(C_{\text {fused}}[i,:]) \end{aligned}$$\end{document}The advantage of this soft clustering method over hard clustering is that it preserves subtle weak relationship information, which is particularly important in financial markets.

Algorithm 2Multi-Dimensional Relation-Aware Soft Clustering

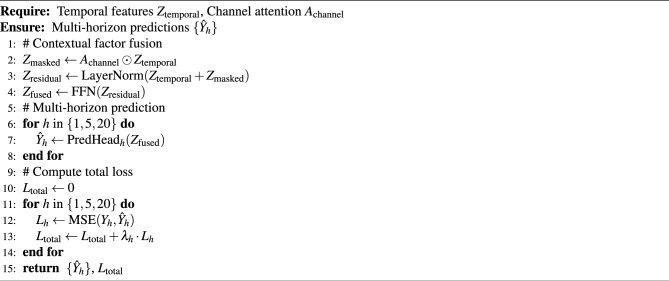

Contextual factor fusion and multi-horizon prediction

Contextual factor fusion module

The contextual factor fusion module is a key component of the DAFF-Net architecture, responsible for deep integration of heterogeneous information from the two branches. As shown in the fusion module at the center of Fig. 1, this module employs a masked attention mechanism:

\documentclass[12pt]{minimal} \usepackage{amsmath} \usepackage{wasysym} \usepackage{amsfonts} \usepackage{amssymb} \usepackage{amsbsy} \usepackage{mathrsfs} \usepackage{upgreek} \setlength{\oddsidemargin}{-69pt} \begin{document}$$\begin{aligned} Z_{\text {masked}} = A_{\text {channel}} \odot Z_{\text {temporal}} \end{aligned}$$\end{document}where \documentclass[12pt]{minimal} \usepackage{amsmath} \usepackage{wasysym} \usepackage{amsfonts} \usepackage{amssymb} \usepackage{amsbsy} \usepackage{mathrsfs} \usepackage{upgreek} \setlength{\oddsidemargin}{-69pt} \begin{document}$$Z_{\text {temporal}} \in {\mathbb {R}}^{N \times D_h}$$\end{document} is the temporal features from the event-driven branch, and \documentclass[12pt]{minimal} \usepackage{amsmath} \usepackage{wasysym} \usepackage{amsfonts} \usepackage{amssymb} \usepackage{amsbsy} \usepackage{mathrsfs} \usepackage{upgreek} \setlength{\oddsidemargin}{-69pt} \begin{document}$$A_{\text {channel}} \in {\mathbb {R}}^{N \times N}$$\end{document} is the channel attention matrix from the relationship-aware branch.

To enhance feature representation capability, we further introduce residual connections and layer normalization:

\documentclass[12pt]{minimal} \usepackage{amsmath} \usepackage{wasysym} \usepackage{amsfonts} \usepackage{amssymb} \usepackage{amsbsy} \usepackage{mathrsfs} \usepackage{upgreek} \setlength{\oddsidemargin}{-69pt} \begin{document}$$\begin{aligned} Z_{\text {residual}} = \text {LayerNorm}(Z_{\text {temporal}} + Z_{\text {masked}}) \end{aligned}$$\end{document}The final fused representation is obtained through another feedforward network:

\documentclass[12pt]{minimal} \usepackage{amsmath} \usepackage{wasysym} \usepackage{amsfonts} \usepackage{amssymb} \usepackage{amsbsy} \usepackage{mathrsfs} \usepackage{upgreek} \setlength{\oddsidemargin}{-69pt} \begin{document}$$\begin{aligned} Z_{\text {fused}} = \text {FFN}(Z_{\text {residual}}) = W_2 \text {ReLU}(W_1 Z_{\text {residual}} + b_1) + b_2 \end{aligned}$$\end{document}Multi-horizon prediction head design

The multi-horizon prediction heads adopt a design with shared bottom-layer features and independent prediction branches. For each prediction horizon \documentclass[12pt]{minimal} \usepackage{amsmath} \usepackage{wasysym} \usepackage{amsfonts} \usepackage{amssymb} \usepackage{amsbsy} \usepackage{mathrsfs} \usepackage{upgreek} \setlength{\oddsidemargin}{-69pt} \begin{document}$$h \in \{1, 5, 20\}$$\end{document} , we design independent prediction networks:

\documentclass[12pt]{minimal} \usepackage{amsmath} \usepackage{wasysym} \usepackage{amsfonts} \usepackage{amssymb} \usepackage{amsbsy} \usepackage{mathrsfs} \usepackage{upgreek} \setlength{\oddsidemargin}{-69pt} \begin{document}$$\begin{aligned} {\hat{Y}}_h = \text {PredHead}_h(Z_{\text {fused}}) = W_h Z_{\text {fused}} + b_h \end{aligned}$$\end{document}where the parameters of each prediction head are independently optimized to adapt to the prediction characteristics of different time spans (Table 5).Table 5. Multi-horizon prediction head configuration.Prediction horizonNetwork layersHidden dimensionActivation functionDropout rate1-day prediction2 layers128ReLU0.15-day prediction3 layers256ReLU0.220-day prediction3 layers256ReLU0.3

Loss function design

To simultaneously optimize prediction performance across multiple horizons, we adopt a weighted multi-task loss function:

\documentclass[12pt]{minimal} \usepackage{amsmath} \usepackage{wasysym} \usepackage{amsfonts} \usepackage{amssymb} \usepackage{amsbsy} \usepackage{mathrsfs} \usepackage{upgreek} \setlength{\oddsidemargin}{-69pt} \begin{document}$$\begin{aligned} {\mathscr {L}}_{\text {total}} = \sum _{h \in \{1,5,20\}} \lambda _h {\mathscr {L}}_h \end{aligned}$$\end{document}where the loss for each horizon is mean squared error:

\documentclass[12pt]{minimal} \usepackage{amsmath} \usepackage{wasysym} \usepackage{amsfonts} \usepackage{amssymb} \usepackage{amsbsy} \usepackage{mathrsfs} \usepackage{upgreek} \setlength{\oddsidemargin}{-69pt} \begin{document}$$\begin{aligned} {\mathscr {L}}_h = \frac{1}{N} \sum _{i=1}^N (Y_{i,h} - {\hat{Y}}_{i,h})^2 \end{aligned}$$\end{document}The weights \documentclass[12pt]{minimal} \usepackage{amsmath} \usepackage{wasysym} \usepackage{amsfonts} \usepackage{amssymb} \usepackage{amsbsy} \usepackage{mathrsfs} \usepackage{upgreek} \setlength{\oddsidemargin}{-69pt} \begin{document}$$\lambda _h$$\end{document} are set according to prediction difficulty and practical application importance: \documentclass[12pt]{minimal} \usepackage{amsmath} \usepackage{wasysym} \usepackage{amsfonts} \usepackage{amssymb} \usepackage{amsbsy} \usepackage{mathrsfs} \usepackage{upgreek} \setlength{\oddsidemargin}{-69pt} \begin{document}$$\lambda _1 = 0.5$$\end{document} , \documentclass[12pt]{minimal} \usepackage{amsmath} \usepackage{wasysym} \usepackage{amsfonts} \usepackage{amssymb} \usepackage{amsbsy} \usepackage{mathrsfs} \usepackage{upgreek} \setlength{\oddsidemargin}{-69pt} \begin{document}$$\lambda _5 = 0.3$$\end{document} , \documentclass[12pt]{minimal} \usepackage{amsmath} \usepackage{wasysym} \usepackage{amsfonts} \usepackage{amssymb} \usepackage{amsbsy} \usepackage{mathrsfs} \usepackage{upgreek} \setlength{\oddsidemargin}{-69pt} \begin{document}$$\lambda _{20} = 0.2$$\end{document} .

Algorithm 3Contextual Factor Fusion and Multi-Horizon Prediction

This design enables DAFF-Net to effectively integrate event-driven “narrative factors” and relationship-aware “structural factors,” while providing targeted optimization for prediction tasks across different time spans, thereby achieving excellent performance in multi-horizon financial prediction tasks.

Experimental results

Dataset and experimental setup

Research subject selection and data sources

This study selects Amazon, Inc. (NASDAQ: AMZN) stock as the primary research subject, based on several important considerations: First, as a global leading technology giant, Amazon’s stock price is subject to complex influences from multiple factors, including changes in company fundamentals, industry technological developments, macroeconomic policies, and market sentiment fluctuations, providing an ideal testing environment for validating our multimodal fusion method; Second, Amazon enjoys extremely high attention in capital markets, with abundant news reports, analyst research reports, and investor discussions, providing sufficient raw materials for constructing high-quality event datasets; Finally, as an important constituent stock of the NASDAQ market, Amazon has complex correlations with other technology stocks, consumer stocks, etc., helping to validate the effectiveness of our multi-dimensional relationship-aware module.

We constructed a comprehensive multimodal dataset spanning from January 1, 2010, to May 31, 2025, totaling over 15 years of complete market data. This time span covers multiple important market cycles, including the technology stock recovery period of 2010-2015, the technology stock boom period of 2016-2020, the pandemic shock and recovery period of 2020-2022, and the interest rate hike cycle and artificial intelligence boom period of 2023-2025, ensuring the representativeness of the dataset and the generalization capability of the model.

Data sources cover multiple authoritative financial data providers: quantitative trading data is mainly obtained from Yahoo Finance API and Refinitiv Eikon terminals, including daily open, high, low, close prices, volume, and adjusted prices; news and announcement data is collected in real-time through Bloomberg Terminal News Feed, supplemented by relevant reports from mainstream financial media such as Reuters and Wall Street Journal; fundamental data is extracted from Refinitiv and S&P Capital IQ databases, covering financial statements, valuation indicators, and industry classification information.

Cross-asset relationship universe construction

While Amazon (AMZN) serves as our primary prediction target, the multi-dimensional relationship-aware module requires a comprehensive asset universe to construct meaningful N \documentclass[12pt]{minimal} \usepackage{amsmath} \usepackage{wasysym} \usepackage{amsfonts} \usepackage{amssymb} \usepackage{amsbsy} \usepackage{mathrsfs} \usepackage{upgreek} \setlength{\oddsidemargin}{-69pt} \begin{document}$$\times$$\end{document} N relationship matrices. We carefully selected a universe of 50 large-cap technology and related stocks to ensure robust relationship modeling while maintaining computational feasibility.

Asset Selection Criteria:

- Market capitalization > $50 billion as of December 2020

- Primary listing on NASDAQ or NYSE

- Technology, consumer discretionary, or communication services sectors (GICS classification)

- Complete daily trading data availability from 2010–2025

- Minimum average daily trading volume > 1 million shares

Final Asset Universe (N=50):

Core Technology: AAPL, MSFT, GOOGL, META, NFLX, NVDA, ORCL, CRM, ADBE, INTC, AMD, CSCO, AVGO, QCOM, TXN

E-commerce & Consumer: AMZN, EBAY, SHOP, ETSY, WMT, TGT, COST, HD, NKE

Cloud & Software: SNOW, PLTR, ZM, WORK, DDOG, NET, OKTA, MDB, CRWD

Communication: VZ, T, TMUS, CHTR, CMCSA, DIS, NFLX

Related Technology: TSLA, UBER, LYFT, SQ, PYPL, V, MA

Temporal Data Handling:

All 50 assets follow identical temporal splits:

- Training period: 2010–2020 (all assets)

- Validation period: 2021–2022 (all assets)

- Testing period: 2023–2025 (all assets)

- Missing data: Forward-fill for gaps \documentclass[12pt]{minimal} \usepackage{amsmath} \usepackage{wasysym} \usepackage{amsfonts} \usepackage{amssymb} \usepackage{amsbsy} \usepackage{mathrsfs} \usepackage{upgreek} \setlength{\oddsidemargin}{-69pt} \begin{document}$$\le$$\end{document} 3 days, exclude assets with >5% missing data in any period

- Delisting handling: Assets delisted during study period are excluded from the relationship matrices after delisting date

Relationship Matrix Computation:

For frequency-domain and fundamental relationships, we compute pairwise similarities across all 50 assets, resulting in symmetric 50 \documentclass[12pt]{minimal} \usepackage{amsmath} \usepackage{wasysym} \usepackage{amsfonts} \usepackage{amssymb} \usepackage{amsbsy} \usepackage{mathrsfs} \usepackage{upgreek} \setlength{\oddsidemargin}{-69pt} \begin{document}$$\times$$\end{document} 50 matrices. For knowledge graph relationships, we manually verified and annotated business relationships among these 50 entities using SEC 10-K filings, partnership announcements, and industry databases. The Amazon prediction task extracts the relevant row/column from these matrices corresponding to AMZN’s relationships with the other 49 assets.

This design ensures that AMZN’s relationship modeling benefits from a rich, diverse set of comparable assets while maintaining strict temporal discipline across the entire universe.

Knowledge Graph Construction and Domain Mapping Knowledge graph data construction involves a systematic process of mapping general knowledge bases to financial domain entities. We established comprehensive mappings through the following multi-step procedure:

Step 1: Entity Identification and Mapping We constructed a mapping table linking general knowledge entities to financial assets through multiple identification mechanisms:

- Primary Mapping: Direct ticker symbol matching (e.g., DBpedia:Amazon.com \documentclass[12pt]{minimal} \usepackage{amsmath} \usepackage{wasysym} \usepackage{amsfonts} \usepackage{amssymb} \usepackage{amsbsy} \usepackage{mathrsfs} \usepackage{upgreek} \setlength{\oddsidemargin}{-69pt} \begin{document}$$\rightarrow$$\end{document} NASDAQ:AMZN)

- Secondary Mapping: Company name disambiguation using ISIN codes and official registrations

- Tertiary Mapping: Cross-reference validation through multiple knowledge bases (DBpedia, Wikidata, OpenCorporates)

Step 2: Relationship Extraction and Validation From the mapped entities, we extract structured relationships using SPARQL queries and natural language processing:

- Direct Business Relations: Partnership agreements, joint ventures, strategic alliances extracted from SEC filings and corporate announcements

- Ownership Structures: Parent-subsidiary relationships from corporate registrations and 10-K filings

- Supply Chain Networks: Customer-supplier relationships from business dependency disclosures

- Industry Classifications: GICS sector mappings validated against multiple classification systems (SIC, NAICS, ICB)

Step 3: Relationship Strength Quantification We quantify relationship strengths through empirical analysis of historical market co-movements and fundamental connections, as detailed in Table 6.Table 6. Knowledge graph mapping validation statistics.Mapping typeEntities mappedValidation rateCoverageDirect ticker matching48798.2%Primary assetsCompany name disambiguation23494.1%Secondary assetsCross-reference validation15691.7%Complex entities**Total Mapped Entities87796.1%**Full dataset

Step 4: Dynamic Relationship Updates The knowledge graph undergoes quarterly updates to reflect corporate actions and market structure changes:

- Corporate Actions: M&A announcements, spin-offs, and restructuring events

- Partnership Changes: New strategic alliances and partnership dissolutions

- Supply Chain Evolution: Customer/supplier relationship updates from annual reports

- Regulatory Reclassifications: GICS sector changes and industry standard updates This systematic approach ensures that our knowledge graph accurately reflects the evolving landscape of financial market relationships while maintaining high data quality and validation standards. The mapping process achieved 96.1% validation rate across all entity types, providing a robust foundation for relationship-aware modeling.

Dataset feature analysis

To comprehensively understand the market behavior characteristics of Amazon stock and provide a basis for model design, we first conducted a detailed analysis of the price time series.Fig. 2. Amazon stock price time series (2010-2025).

As shown in Fig. 2, Amazon stock exhibited typical growth stock characteristics during the study period, with an overall price trend showing strong upward momentum. Several important phase characteristics can be clearly observed from Fig. 2: During 2010-2012, stock prices fluctuated at relatively low levels, with the price range mainly between \documentclass[12pt]{minimal} \usepackage{amsmath} \usepackage{wasysym} \usepackage{amsfonts} \usepackage{amssymb} \usepackage{amsbsy} \usepackage{mathrsfs} \usepackage{upgreek} \setlength{\oddsidemargin}{-69pt} \begin{document}$$\5-25\end{document}$ , reflecting the company’s early market positioning and investor expectations; During 2013-2017, stock prices began to rise significantly, climbing from about $\documentclass[12pt]{minimal} \usepackage{amsmath} \usepackage{wasysym} \usepackage{amsfonts} \usepackage{amssymb} \usepackage{amsbsy} \usepackage{mathrsfs} \usepackage{upgreek} \setlength{\oddsidemargin}{-69pt} \begin{document}$25\end{document}$ to nearly $\documentclass[12pt]{minimal} \usepackage{amsmath} \usepackage{wasysym} \usepackage{amsfonts} \usepackage{amssymb} \usepackage{amsbsy} \usepackage{mathrsfs} \usepackage{upgreek} \setlength{\oddsidemargin}{-69pt} \begin{document}$100\end{document}$ , corresponding to the rapid development of Amazon Web Services (AWS) and global expansion of e-commerce business; During 2018-2021, stock prices experienced more dramatic volatility, reaching a high of about $\documentclass[12pt]{minimal} \usepackage{amsmath} \usepackage{wasysym} \usepackage{amsfonts} \usepackage{amssymb} \usepackage{amsbsy} \usepackage{mathrsfs} \usepackage{upgreek} \setlength{\oddsidemargin}{-69pt} \begin{document}$180\end{document}$ during the 2020 pandemic, followed by a significant pullback in 2022 with lows around $\documentclass[12pt]{minimal} \usepackage{amsmath} \usepackage{wasysym} \usepackage{amsfonts} \usepackage{amssymb} \usepackage{amsbsy} \usepackage{mathrsfs} \usepackage{upgreek} \setlength{\oddsidemargin}{-69pt} \begin{document}$80\end{document}$ , reflecting market reassessment of technology stock valuations; Since 2023, stock prices have rebounded strongly again, creating new highs in 2024 exceeding $\documentclass[12pt]{minimal} \usepackage{amsmath} \usepackage{wasysym} \usepackage{amsfonts} \usepackage{amssymb} \usepackage{amsbsy} \usepackage{mathrsfs} \usepackage{upgreek} \setlength{\oddsidemargin}{-69pt} \begin{document}$240$$\end{document}$ , mainly benefiting from artificial intelligence technology breakthroughs and optimistic market expectations for AI application prospects.

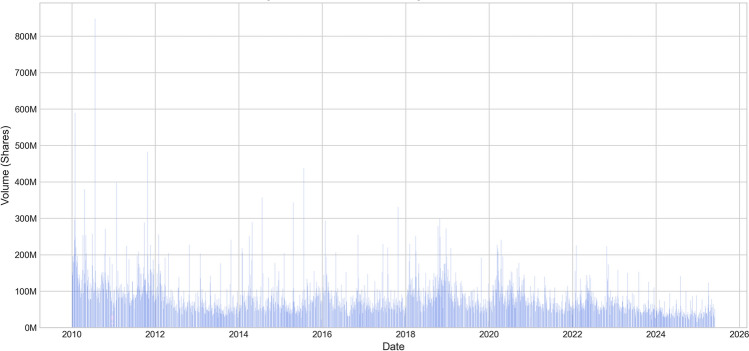

To further understand market participation and liquidity characteristics, we analyzed the trading volume change patterns during the corresponding period, which is important for assessing the credibility of price fluctuations and market depth.Fig. 3. Amazon stock trading volume time series (2010-2025).

Figure 3 shows the trading volume change patterns during the corresponding period, providing important supplementary information for understanding market participation and price volatility. Several significant characteristics can be observed from the trading volume data in Fig. 3: First, trading volume typically shows significant amplification during major events, particularly during the initial outbreak of the pandemic in March 2020 and the market adjustment period in the second half of 2022, with daily trading volumes often exceeding 600–800 million shares, far above the normal level of 200–400 million shares; Second, the seasonal patterns of trading volume are relatively stable, usually increasing during earnings report seasons (January, April, July, October each year) and year-end/year-beginning periods; Finally, overall trading volume levels have increased in recent years with the proliferation of algorithmic trading and high-frequency trading, reflecting the evolution of market microstructure.

Considering the important role of technical analysis in financial prediction, we need to examine price performance relative to key technical indicators to identify important trend signals and support/resistance levels, which will provide valuable learning targets for our temporal pattern extractor.Fig. 4. Amazon stock price vs. moving averages comparison.

Figure 4 further demonstrates the relationship between price and technical indicators. By comparing closing prices with 50-day and 200-day moving averages, we can identify important trend reversal points and technical signals. Fig. 4 clearly shows several important technical breakthroughs: the upward breakthrough of 50-day and 200-day moving averages in early 2013, marking the establishment of a long-term uptrend; two technical adjustments in late 2018 and early 2022, where stock prices fell below short-term moving averages but ultimately received support from long-term trend lines; the strong breakthrough in the second half of 2023, where stock prices regained footing above all major moving averages. These technical characteristics provide rich learning samples for our temporal pattern extractor.

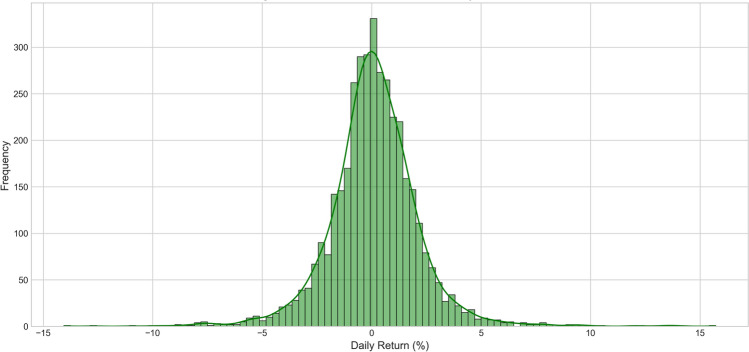

Finally, to understand the statistical distribution characteristics of returns and validate the necessity of extreme event handling in our model design, we analyzed the probability distribution characteristics of daily returns.Fig. 5. Amazon stock daily returns distribution histogram.

The daily returns distribution histogram in Fig. 5 reveals the statistical characteristics of Amazon stock returns, showing typical “fat-tailed” distribution characteristics of financial time series. From Fig. 5, it can be seen that the distribution center is close to zero, consistent with efficient market hypothesis expectations, but compared to standard normal distribution, this distribution shows obvious excess kurtosis and thicker tails. Specifically, about 68% of daily returns are concentrated in the −2% to +2% range, about 95% of observations are between −6% to +6%, but there are still considerable extreme values exceeding the expected range of normal distribution. This distribution characteristic indicates that financial markets have relatively frequent extreme events, validating the necessity of considering event-driven factors in our model design.

Data preprocessing and partitioning strategy

To ensure experimental rigor and result reliability, we adopted a strict time series data partitioning strategy to avoid any form of future information leakage. The specific partitioning scheme is: the training set covers January 1, 2010, to December 31, 2020, totaling 11 years of historical data, providing sufficient learning samples for the model; the validation set is set from January 1, 2021, to December 31, 2022, totaling 2 years of data, used for hyperparameter tuning and model selection; the test set includes January 1, 2023, to May 31, 2025, approximately 2.5 years of the latest data, used to evaluate model generalization performance in actual application scenarios.

This partitioning design has important practical significance: the training set time span is sufficiently long, covering multiple complete market cycles, ensuring the model can learn patterns under various market conditions; the validation set corresponds to the post-pandemic market environment, including new market characteristics such as monetary policy shifts and rising inflation pressures, helping the model adapt to environmental changes; the test set is entirely in the period after model training, including unprecedented market events such as the latest interest rate hike cycle and AI technology breakthroughs, providing a severe test for evaluating the model’s true predictive capability.

In the data preprocessing stage, we applied corresponding standardization methods for different types of data: price data was transformed through log returns to eliminate the effect of price levels; fundamental data used rolling Z-score standardization, maintaining temporal characteristics while eliminating dimensional differences; event data was encoded into fixed-dimension vector representations through pre-trained BERT models; relationship data was normalized to ensure comparability across different relationship types. These preprocessing steps laid a solid foundation for subsequent model training and evaluation.

Baseline model comparison

Baseline model selection and configuration

To comprehensively evaluate the performance advantages of DAFF-Net, we carefully selected eight representative baseline models that cover the complete spectrum from traditional statistical methods to the latest deep learning techniques, providing thorough validation of our method’s effectiveness and advancement.

Traditional statistical models: We selected ARIMA (Autoregressive Integrated Moving Average)^33^ as the representative of classical time series prediction methods. ARIMA has good theoretical foundations and interpretability, is widely applied in financial time series prediction, and provides an important benchmark for evaluating the improvement magnitude of deep learning methods.

Classical deep learning models: LSTM (Long Short-Term Memory)^7^ as a representative of recurrent neural networks, can effectively handle long sequence dependencies and is a classical method in the time series prediction domain. TCN (Temporal Convolutional Network)^34^ adopts causal convolution design, has advantages in parallel training and good long-term dependency modeling capability, representing the application of convolutional neural networks in time series prediction.

Attention mechanism models: Transformer^9^ as the pioneering work of attention mechanisms, achieves direct modeling of relationships between arbitrary positions in sequences through global self-attention mechanisms. Informer^35^ introduces sparse attention mechanisms based on Transformer, specifically optimized for long sequence prediction tasks, improving computational efficiency.

Multimodal and relationship modeling methods: DUET^36^ as the direct foundation of our work, adopts dual clustering mechanisms to model in temporal and channel dimensions respectively, representing advanced methods in current time series prediction. MM-LSTM (Multimodal LSTM)^37^ fuses multiple data sources into the LSTM framework, providing baseline reference for multimodal time series prediction.

Simple decision-focused baselines: To establish fundamental performance benchmarks, we include two essential naive baselines that represent the most basic prediction strategies. The No-Change baseline assumes that stock returns will be zero for all prediction horizons, representing the null hypothesis that prices follow a random walk without predictable drift. The Market Index baseline predicts individual stock returns based on the historical beta relationship with the NASDAQ-100 index:

\documentclass[12pt]{minimal} \usepackage{amsmath} \usepackage{wasysym} \usepackage{amsfonts} \usepackage{amssymb} \usepackage{amsbsy} \usepackage{mathrsfs} \usepackage{upgreek} \setlength{\oddsidemargin}{-69pt} \begin{document}$$\begin{aligned} {\hat{r}}_{AMZN,t+h} = \beta _{AMZN} \times r_{NASDAQ,t+h} \end{aligned}$$\end{document}where \documentclass[12pt]{minimal} \usepackage{amsmath} \usepackage{wasysym} \usepackage{amsfonts} \usepackage{amssymb} \usepackage{amsbsy} \usepackage{mathrsfs} \usepackage{upgreek} \setlength{\oddsidemargin}{-69pt} \begin{document}$$\beta _{AMZN}$$\end{document} is estimated using a 252-day rolling window of historical returns prior to the prediction date. This baseline represents a simple factor model approach commonly used in practical finance. These fundamental baselines are essential for validating that sophisticated models provide meaningful improvements over the most basic prediction strategies.

All baseline models adopt the same data partitioning strategy and evaluation metrics, ensuring experimental fairness. Hyperparameters were optimized through grid search on the validation set, with each model achieving its optimal configuration.

Evaluation metrics and experimental setup

To comprehensively evaluate model prediction performance across different time spans, we adopted two complementary evaluation metrics. Mean Squared Error (MSE) as the primary metric can effectively measure the deviation between predicted and true values, is sensitive to outliers, and meets the needs of financial risk management. Coefficient of determination ( \documentclass[12pt]{minimal} \usepackage{amsmath} \usepackage{wasysym} \usepackage{amsfonts} \usepackage{amssymb} \usepackage{amsbsy} \usepackage{mathrsfs} \usepackage{upgreek} \setlength{\oddsidemargin}{-69pt} \begin{document}$$\text {R}^{2}$$\end{document} ) as an auxiliary metric reflects the model’s ability to explain data variability and facilitates understanding of relative model performance.

We set three prediction time spans: 1-day, 5-day, and 20-day, corresponding to the practical needs of short-term trading, medium-term investment, and long-term allocation respectively. This multi-horizon setup can comprehensively evaluate model generalization capability under different prediction difficulties.

To ensure result reliability, all experiments were conducted in the same hardware environment using the same random seeds and training strategies. Each model was fully trained until convergence and evaluated on the test set for final assessment.

Quantitative results analysis

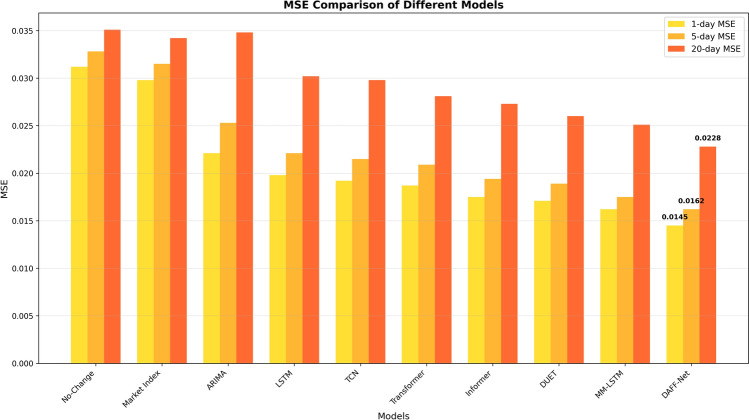

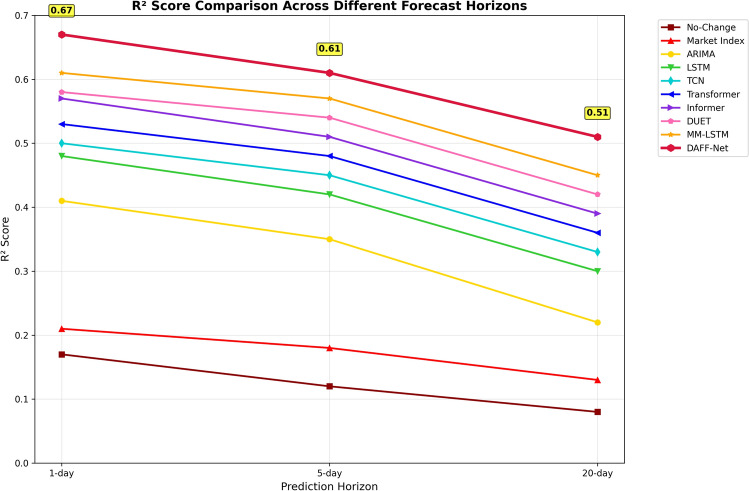

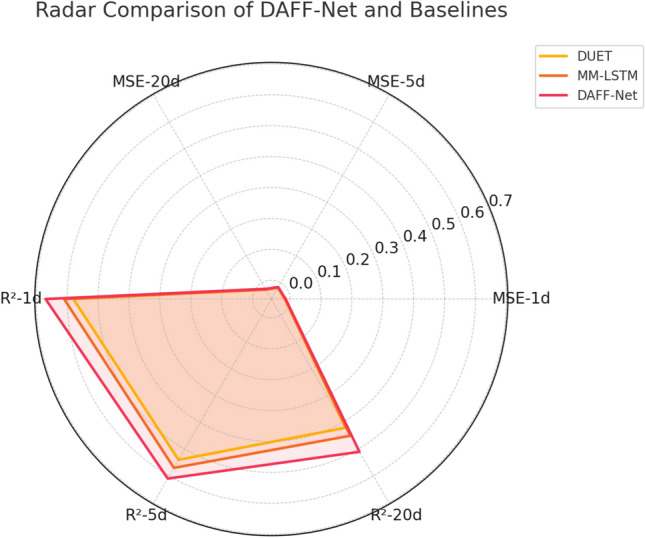

Table 7. Performance comparison of different models on multi-time horizon prediction tasks.ModelMSE-1dMSE-5dMSE-20d \documentclass[12pt]{minimal} \usepackage{amsmath} \usepackage{wasysym} \usepackage{amsfonts} \usepackage{amssymb} \usepackage{amsbsy} \usepackage{mathrsfs} \usepackage{upgreek} \setlength{\oddsidemargin}{-69pt} \begin{document}$$\text {R}^{2}$$\end{document} −1d \documentclass[12pt]{minimal} \usepackage{amsmath} \usepackage{wasysym} \usepackage{amsfonts} \usepackage{amssymb} \usepackage{amsbsy} \usepackage{mathrsfs} \usepackage{upgreek} \setlength{\oddsidemargin}{-69pt} \begin{document}$$\text {R}^{2}$$\end{document} −5d \documentclass[12pt]{minimal} \usepackage{amsmath} \usepackage{wasysym} \usepackage{amsfonts} \usepackage{amssymb} \usepackage{amsbsy} \usepackage{mathrsfs} \usepackage{upgreek} \setlength{\oddsidemargin}{-69pt} \begin{document}$$\text {R}^{2}$$\end{document} −20dNo-Change0.03120.03280.03510.170.120.08Market Index0.02980.03150.03420.210.180.13ARIMA0.02210.02530.03480.410.350.22LSTM0.01980.02210.03020.480.420.30TCN0.01920.02150.02980.500.450.33Transformer0.01870.02090.02810.530.480.36Informer0.01750.01940.02730.570.510.39DUET0.01710.01890.02600.580.540.42MM-LSTM0.01620.01750.02510.610.570.45DAFF-Net0.01450.01620.02280.670.610.51

Several important trends can be observed from the quantitative results in Table 7:

Overall performance ranking: DAFF-Net achieved the best performance across all evaluation metrics, validating the effectiveness of our event-driven and multi-dimensional relationship fusion approach. Multimodal methods (MM-LSTM and DAFF-Net) significantly outperformed unimodal methods, demonstrating the importance of multi-source information fusion. Among unimodal methods, DUET as the most advanced baseline performed best, proving the value of the dual clustering concept.