Memory-Driven Dynamics: A Fractional Fisher Information Approach to Economic Interdependencies

Larissa M. Batrancea, Ömer Akgüller, Mehmet Ali Balcı, Dilara Altan Koç, Lucian Gaban

TL;DR

This paper introduces a new method using fractional Fisher Information to study how economic indicators like interest rates and inflation interact over time.

Contribution

The novelty lies in integrating Caputo fractional derivatives with Fisher Information to capture long-range memory effects in economic data.

Findings

Fractional Fisher Information reveals stronger historical dependencies among economic indicators compared to traditional methods.

Long-memory effects amplify the information contribution of each indicator, especially in synergistic interactions.

The study shows that ignoring memory effects can lead to underestimating the true dynamics of economic interdependencies.

Abstract

This study introduces a novel approach for analyzing the dynamic interplay among key economic indicators by employing a Caputo Fractional Fisher Information framework combined with partial information decomposition. By integrating fractional derivatives into traditional Fisher Information metrics, our methodology captures long-range memory effects that govern the evolution of monetary policy, credit risk, market volatility, and inflation, represented by INTEREST, CDS, VIX, CPI, and PPI, respectively. We perform a comprehensive comparative analysis using rolling-window estimates to generate Caputo Fractional Fisher Information values at different fractional orders alongside the memoryless Ordinary Fisher Information. Subsequent correlation, cross-correlation, and transfer entropy analyses reveal how historical dependencies influence both unique and synergistic information flows between…

Genes, proteins, chemicals, diseases, species, mutations and cell lines named across the full text — each resolved to its canonical identifier and authoritative record.

Click any figure to enlarge with its caption.

Figure 1

Figure 1 Figure 2

Figure 2 Figure 3

Figure 3 Figure 4

Figure 4 Figure 5

Figure 5 Figure 6

Figure 6 Figure 7

Figure 7 Figure 8

Figure 8 Figure 9

Figure 9 Figure 10

Figure 10 Figure 11

Figure 11 Figure 12

Figure 12 Figure 13

Figure 13 Figure 14

Figure 14 Figure 15

Figure 15 Figure 16

Figure 16 Figure 17

Figure 17 Figure 18

Figure 18 Figure 19

Figure 19 Figure 20

Figure 20 Figure 21

Figure 21 Figure 22

Figure 22 Figure 23

Figure 23 Figure 24

Figure 24 Figure 25

Figure 25 Figure 26

Figure 26Peer Reviews

No public reviews on file for this paper yet. If you reviewed it on a platform where reviews are public (OpenReview, ICLR, NeurIPS, ICML), you can paste yours below so the community can read it here.

Videos

No videos yet. Explain this paper in a talk, walkthrough, or lecture? Add one.

Taxonomy

TopicsMarket Dynamics and Volatility · Complex Systems and Time Series Analysis · Stock Market Forecasting Methods

1. Introduction

Information theory provides a powerful framework for analyzing uncertainty and information flow in economic systems where agents and markets constantly process information under uncertainty. Concepts like entropy and Fisher Information quantify information content and uncertainty in economic data [1,2,3,4], enabling researchers to better understand decision-making behavior and market dynamics. Interdisciplinary fields such as econophysics and complexity economics have emerged from these approaches, challenging traditional economic theories including the Efficient Market Hypothesis and suggesting economies operate near the “edge of chaos” [5]. As Ref. [6] confirms, information-theoretic approaches now exert growing influence across economic research.

These methods have widespread applications across economic disciplines. In finance, entropy-based measures characterize risk and enhance portfolio diversification [7,8,9,10], with Ref. [11] demonstrating that mean-entropy portfolio selection rivals the Markowitz approach, leading to numerous applications in optimization, pricing, and valuation [12]. In macroeconomics, informational measures model agent signal processing and appear in inequality indices and business cycle analysis [13], while econometrics employs information-theoretic concepts in maximum likelihood estimation, the Fisher Information matrix, and model selection criteria like AIC [14,15]. Measures such as mutual information and transfer entropy help detect causality in economic time series, as demonstrated by Ref. [16] in financial markets. By framing economic problems through information flow and uncertainty, these approaches provide a unifying language for analyzing market efficiency and decision-making, making Fisher Information and entropy increasingly integral to economic analysis [17,18].

Beyond traditional information measures, partial information decomposition (PID) has emerged as a powerful framework for disentangling complex informational relationships in multivariate systems. PID allows researchers to decompose mutual information into distinct components: unique information (provided solely by individual variables), redundant information (shared across variables), and synergistic information (emerging only from their joint examination) [19,20,21,22]. This decomposition is particularly valuable in economic contexts, where multiple factors often influence a target variable through various information channels. For instance, Ref. [23] applied PID to financial time series to identify unique and shared contributions of multiple market indicators to price movements, while Ref. [24] utilized this framework to analyze the information structure of financial markets during crisis periods. PID extends beyond the capabilities of traditional bivariate measures by revealing how different economic indicators may contain complementary, overlapping, or emergent information about market conditions.

Complementing PID, transfer entropy has become a fundamental tool for quantifying directed information flow between economic time series. Unlike correlation-based measures, transfer entropy captures asymmetric and nonlinear dependencies, making it ideal for detecting Granger-causal relationships in complex economic systems [25,26]. Researchers have applied transfer entropy to study information transmission between markets [27], spillover effects across asset classes [28], and lead–lag relationships in macroeconomic indicators [29]. The measure has proven particularly valuable for identifying shifts in information flow during market transitions and economic crises [30]. By combining transfer entropy with PID and extending both through our fractional approach, we can capture not only the direction of information flow between economic variables but also how these flows are structured and influenced by long-memory effects—features that conventional approaches might overlook. This integrated methodology enables a more nuanced understanding of how memory-laden economic processes exchange information over time, revealing both immediate and persistent effects that propagate through the economic system.

Fractional calculus-based models have shown superior performance in capturing complex dynamics and improving forecasts in both finance and macroeconomics. In financial economics, a prominent example is the fractionally integrated GARCH (FIGARCH) model for asset return volatility. FIGARCH allows the volatility process to exhibit long-range dependence and has been found to better represent the persistence in volatility of stock markets, exchange rates, and even inflation rates, compared to standard GARCH models [31]. By permitting a slow hyperbolic decay of volatility shocks, fractional GARCH models can match the observed long memory in financial market volatility (often indicated by high Hurst exponents). Similarly, in macroeconomic time-series analysis, fractional differencing improves forecasting accuracy [32]. Studies on monetary aggregates and other macro indicators have shown that models with a fractional integration parameter out-perform their integer-order counterparts in out-of-sample forecasts [33,34,35]. More broadly, fractional approaches (such as ARFIMA for long-memory mean dynamics and FIGARCH for long-memory volatility) have become essential tools in econometrics when dealing with heavy-tailed distributions, persistence in economic growth rates, or persistence in volatility clustering. They capture nuanced complex dynamics—like power-law decays, self-similarity, and fractal structures—that traditional short-memory models miss. By leveraging these strengths, fractional calculus enriches economic analysis, allowing models to reflect real-world memory and complexity more faithfully than integer-order methods.

While both information-theoretic measures and fractional calculus have been applied in economics separately, fractional versions of information measures (such as Fisher Information) remain relatively underexplored in the literature. Fisher Information itself has been used in economics in various ways, for instance, as part of complexity measures combining Shannon entropy and Fisher Information to distinguish randomness from structure in financial time series [36,37,38,39,40]. These studies, however, still employ the classical Fisher Information, which assumes no long-memory in the underlying process. Fractional Fisher Information—i.e., extending Fisher’s measure to account for fractional dynamics or long-memory—has seen only limited developments, mostly in theoretical or non-economic contexts. For example, Ref. [41] introduced a definition of fractional Fisher Information in the context of stable probability distributions to prove an information-theoretic form of the Central Limit Theorem for heavy-tailed -stable laws. This work defines a fractional analogue of Fisher Information for probability densities with power-law tails, illustrating how information measures can be generalized when the underlying diffusion process is Levy-type fractional.

Similarly, in mathematical physics and biology, researchers have explored fractional Fisher Information in systems with anomalous diffusion or spatial memory—Ref. [42], for instance, studied a fractional Fisher Information in a chemotaxis organism movement model to account for memory in the diffusion term. These studies demonstrate the feasibility of defining Fisher Information in fractional-order systems, but they are largely confined to theoretical models and physical sciences. Crucially, applications in economics are virtually absent so far. Prior economic research has not combined fractional calculus and Fisher Information in a unified framework; instead, long-memory and information measures have been studied in isolation. This gap is evident: standard Fisher Information measures the “instantaneous” information content (often related to the local gradient of a likelihood), whereas economic processes with memory may carry cumulative information from the past. No comprehensive measure existed to capture that cumulative information within an economic time-series context. The lack of previous studies on fractional Fisher Information in economics represents an important knowledge gap that this study aims to address.

Given the above gap, we propose the Caputo Fractional Fisher Information (CFFI) as a new measure that incorporates long-memory effects into Fisher’s information metric. The choice of the Caputo fractional derivative is deliberate and crucial. Previous attempts to formulate fractional versions of Fisher Information (such as in the context of stable laws by Ref. [41]) did not address the practical challenges of applying fractional derivatives to real economic data. In particular, many fractional derivatives (e.g., Riemann–Liouville definitions) require non-intuitive initial conditions or produce measures that are not easily interpreted in time-evolving systems. The Caputo derivative, by contrast, is well suited for applications because it allows initial conditions to be expressed in the same form as for ordinary differential equations using standard integer-order derivatives or function values. This makes it compatible with empirical economic time series, which have known initial states or baseline conditions. Using the Caputo approach, one can start the analysis at time with usual economic initial values (say, an initial price or index level), without needing exotic fractional initializations.

Moreover, the Caputo derivative’s kernel inherently encodes a power-law memory decay [43,44,45,46]. This means CFFI naturally weights the contribution of past information in a way that matches observed long-memory behaviors: recent data points are weighted more heavily but distant past data, while down-weighted, still contribute following a power-law decay. Such a kernel is ideal for modeling economic processes where shocks or information gradually dissipates but with long-lasting effects. In essence, CFFI generalizes the classical Fisher Information to a non-local, history-aware context, while reducing to the classic measure in the limit of no memory. Notably, as the fractional order approaches 1 (meaning memory effects diminish), the CFFI converges to the ordinary Fisher Information. This consistency is important: it ensures that CFFI is an extension not a replacement of Fisher Information, retaining all the desirable properties of the standard measure when but offering additional insights when for partial memory or for higher-order memory.

Another motivation for adopting the Caputo form is the interpretability of results in an economic setting. CFFI can be understood as the “information content” of an economic variable’s trajectory, taking into account its historical path. If previous definitions of fractional Fisher Information were applied directly, they might not align with how economists interpret dynamics; for example, some definitions might be symmetric or spatial, whereas economic time series are typically one-sided in time. By using the Caputo derivative, which is a one-sided fractional operator on , we align the information measure with the time-forward evolution of economic processes. In summary, the limitations of prior fractional information measures—such as difficulty in setting initial conditions, or lack of temporal directionality—are overcome by using the Caputo derivative. CFFI fills a critical need: it provides a tool to quantify the informational implications of long-memory in economic systems, bridging the gap between information theory and fractional dynamics. It captures how much “memory-driven” structure is present in the data’s information content, which the ordinary Fisher Information would fail to detect. This makes CFFI especially suitable for financial and macroeconomic time series where persistent trends, volatility clustering, and delayed reactions are the norm.

Building on the above motivation, this study sets out to develop and apply the Caputo Fractional Fisher Information framework in economic analysis. The primary research question is as follows: How do long-memory effects influence the information structure of economic indicators, and can a fractional-order Fisher Information measure reveal interdependencies that traditional information measures miss? To answer this, we introduce CFFI and investigate its behavior in a real-world economic context. The key objectives and novel contributions of the study are summarized as follows: We formally define the CFFI metric by replacing the time derivative in the Fisher Information formulation with a Caputo fractional derivative. This yields a new information-theoretic measure that accumulates the influence of past data. We show that CFFI generalizes classical Fisher Information to systems with power-law memory, reducing to the ordinary Fisher Information in the limit of short memory. This theoretical development is a novel contribution, providing economists with a tool to measure information in non-Markovian processes. We apply the CFFI framework to an empirical analysis of five key economic indicators, spanning finance and macroeconomics: interest rates (monetary policy indicator), credit default swap spreads (credit risk), the VIX volatility index (market uncertainty), and price indices (CPI for consumer inflation and PPI for producer inflation). By computing rolling-window CFFI values for each series, we capture the time-varying information content of each indicator under different fractional orders.

This application is distinctive—to our knowledge, it is the first time fractional information measures are used to analyze real economic time series. To deepen the analysis, we combine CFFI with a partial information decomposition approach from multivariate information theory. This allows us to decompose the information shared between multiple indicators into components such as unique information, shared (redundant) information, and synergistic information. In doing so, we can address questions like the following: Does the long-memory information in, say, the PPI (producer prices) provide unique predictive power for CPI (consumer prices) beyond what is already contained in other variables? Or do certain variables together exhibit synergy—information that only emerges when considering their joint history? By using CFFI in this multivariate setting, we uncover memory-driven synergistic effects that the classical Fisher Information framework might underestimate. These findings demonstrate the added value of the fractional approach; CFFI captures the lingering impact of past events on current information flow, whereas classical Fisher Information reacts only to abrupt, recent changes.

The study is organized as follows: In Section 2, we describe the theoretical underpinnings and methodological framework, including the development of the Caputo Fractional Fisher Information (CFFI) measure and its integration with partial information decomposition (PID) techniques. This section details the rationale behind employing fractional derivatives to capture long-range memory effects in economic time series and explains the advantages of the Caputo definition over previous approaches. In Section 3, we present the empirical analysis based on data from the Turkish economy, where we compute rolling-window estimates of CFFI at various fractional orders alongside the traditional Ordinary Fisher Information (OFI) and examine their interdependencies via correlation, cross-correlation, and transfer entropy analyses. Moreover, also in Section 3 provides an in-depth discussion of the results from both an information-theoretic and economic perspective, highlighting how long-memory processes influence the unique, redundant, and synergistic informational contributions among key indicators such as INTEREST, CDS, VIX, CPI, and PPI. Finally, Section 4 concludes the paper by summarizing our main findings, discussing the implications for forecasting and policy analysis, and suggesting avenues for future research.

2. Materials and Methods

In this section, we outline a rigorous methodology for extending classical Fisher Information to systems exhibiting power-law memory effects. By incorporating Caputo fractional derivatives into the framework of information theory, we introduce a novel measure termed the Caputo Fractional Fisher Information (CFFI). This approach is particularly tailored for non-Markovian systems, where historical dependencies significantly influence the dynamics.

2.1. Theoretical Framework of CFFI

Consider a stochastic process with a time-dependent probability density function (PDF) . The left-sided Caputo fractional derivative of order for a function is defined as

where is the smallest integer greater than , is the Gamma function, and denotes the n-th ordinary derivative of . For , this expression simplifies to

where . The Caputo derivative is selected due to its suitability for physical systems as it allows initial conditions to be specified in terms of integer-order derivatives with clear interpretations [44]. The convolution kernel encodes power-law memory effects, making this operator ideal for modeling non-Markovian processes where the current state depends on the entire historical trajectory. For this methodology, we primarily consider to focus on systems with fractional dynamics involving first-order derivatives, unless otherwise specified.

In classical information theory, the score function measures the sensitivity of the log-likelihood to small changes in time [47]. To account for memory effects, we generalize this concept by replacing the ordinary derivative with the Caputo fractional derivative. Thus, the fractional score function is defined as

For , Equation (3) becomes

This formulation aggregates historical gradients with weights determined by the power-law kernel , reflecting the cumulative impact of past dynamics on the current information content. This generalization is natural for systems with long-range memory, extending the classical notion of instantaneous sensitivity to a history-dependent framework.

Building on the fractional score function, we define CFFI as the expectation of its square

The CFFI quantifies the cumulative sensitivity of the log-density to perturbations across the system’s history, weighted by the memory kernel. Analogous to the classical Fisher Information, which relates to the variance of the score function, the CFFI extends this concept to incorporate non-local temporal effects.

Substituting the Caputo derivative into the CFFI definition, we obtain its explicit integral form. For ,

For , higher-order derivatives would appear, with ; however, we focus on to align with typical fractional diffusion models. Equation (6) explicitly couples historical log-density gradients to the current PDF, highlighting the non-Markovian nature of the information measure.

For clarity regarding the fractional order parameter in our framework, we restrict to the interval based on both theoretical considerations and practical interpretations. When , the Caputo fractional derivative captures intermediate memory effects with power-law decay, while at , it reduces to the ordinary first derivative, representing memoryless dynamics. For values , the operator would correspond to higher-order fractional derivatives, incorporating derivatives of order (the ceiling of ) in its definition. While mathematically valid, these higher-order derivatives introduce oscillatory behaviors and complex initialization requirements that complicate economic interpretation.

They also tend to overemphasize rapid fluctuations rather than persistent trends, contrary to the long-memory phenomena we aim to model. Alternatively, negative values would yield fractional integrals rather than derivatives, effectively accumulating rather than differentiating information content. Such accumulation would obscure the information dynamics we seek to quantify as it would not properly characterize the sensitivity of probability distributions to parameter changes—the core concept behind Fisher Information. Therefore, restricting to provides the most appropriate balance between mathematical tractability and economic interpretability for our long-memory information analysis.

2.2. Theoretical Implications of CFFI

The CFFI offers several key insights within information theory. It captures memory-driven information flow by integrating contributions from all prior states with weights decaying according to a power-law, reflecting the system’s historical dependencies. This makes it particularly suitable for non-Markovian systems governed by fractional dynamics.

A key theoretical result establishes the connection between the CFFI and classical Fisher Information. Specifically, as the fractional order approaches to 1 below, the CFFI converges to the classical Fisher Information . This is expressed mathematically as

The proof of this convergence relies on the property that the Caputo fractional derivative approaches the ordinary time derivative as . Consequently, substituting this into the CFFI definition yields the classical Fisher Information, confirming that the CFFI generalizes the classical measure and reduces to it when memory effects vanish.

In fractional diffusion processes, the evolution of the probability density is governed by a fractional diffusion equation, often expressed via the fractional Fokker-Planck equation

where D is the diffusion coefficient, is the Laplacian operator, representing spatial dispersion.

Equation (8) describes subdiffusive behavior, where the spread of particles is slower than in classical diffusion due to memory effects encoded by the fractional derivative. When , it reduces to the standard diffusion equation.

2.3. Entropy Production of CFFI

The CFFI connects to the fractional entropy production rate, generalizing classical information-theoretic relationships. Let us define the entropy of the system as

The fractional entropy production rate is the fractional derivative of the entropy

Substituting the fractional diffusion equation into Equation (10) yields

In order to simplify Equation (11), we use integration by parts. Assume the boundary terms (e.g., ) vanish at

Thus,

This expression resembles the classical entropy production rate but is now in the fractional context. In classical diffusion ( ), the entropy production rate relates to the Fisher Information via the de Bruijn identity

where is the classical Fisher Information. For fractional diffusion, a similar relationship holds

where is a fractional analogue of the Fisher Information. While the exact form of may differ from , the CFFI captures the memory effects in the information dynamics, linking fractional entropy production to information measures in non-Markovian systems.

2.4. Cramér–Rao Bound of CFFI

In classical statistics, the Cramér–Rao bound provides a lower bound on the variance of an unbiased estimator, inversely proportional to the Fisher Information

where is the classical Fisher Information for a parameter . For systems with memory, the CFFI extends this concept to fractional contexts.

Assume is an unbiased estimator of , i.e., . Applying the Caputo fractional derivative to both sides of the unbiasedness condition yields

Since is a constant, its Caputo derivative is zero

Thus,

Define the fractional score function as the Caputo fractional derivative of the log-likelihood:

Using the linearity of the expectation operator and the fact that , we have

Consider the covariance between and the fractional score function . By the Cauchy–Schwarz inequality,

The right-hand side is the product of the variance of and the CFFI

From the unbiasedness condition and the fractional Leibniz rule, we derive the following identity

This follows because the Caputo derivative of with respect to is 1.

Substituting Equation (26) into the covariance inequality,

Rearranging, we obtain the fractional Cramér–Rao bound

The fractional Cramér–Rao bound provides a memory-dependent measure of estimation precision. When the CFFI is large, the bound tightens, leading to lower variance in the estimator. This occurs because historical gradients are strongly informative about the parameter , enhancing the estimator’s accuracy. The fractional order plays a critical role in controlling the strength of memory effects. Smaller values of correspond to stronger memory decay, which reduces and loosens the bound. This reflects increased uncertainty due to the fading influence of historical data. Importantly, the bound explicitly accounts for power-law memory, making it particularly suitable for non-Markovian systems characterized by long-range temporal dependencies.

2.5. CFFI Integration with PID

To broaden the scope of CFFI, we explore its integration with Partial Information Decomposition (PID), a framework that decomposes mutual information among variables into unique, redundant, and synergistic components. This synthesis aims to elucidate how memory effects, inherent in fractional dynamics, shape information sharing in systems with long-range dependencies. While classical PID assumes memoryless interactions, our approach explicitly models historical dependencies through fractional calculus.

Consider time-dependent stochastic processes with a joint PDF and marginals . Classical PID decomposes the mutual information as

where , R, and S represent unique, redundant, and synergistic information, respectively [48]. To generalize this for memory-dependent systems, we replace ordinary derivatives with Caputo fractional derivatives in the Fisher Information framework.

Define Caputo Fractional Conditional Fisher Information (CFCFI) for conditioned on

where is the Caputo derivative of order . This quantifies the sensitivity of the conditional log-density to historical variations in for . Analogously, define

The fractional unique information that provides about is defined as

representing the reduction in uncertainty about when conditioning on , excluding contributions from . Similarly, is defined for , capturing the unique information provides about .

A preliminary heuristic for redundant information is given by

However, this approach requires refinement to avoid overcounting overlapping memory effects. The minimum operator, while intuitive, does not account for the temporal interdependencies between and that arise from shared historical influences on . For instance, if both and for exhibit correlated memory-driven dynamics (e.g., joint responses to past external shocks), their redundant contributions to may not align with the pairwise minimum of their individual conditional Fisher informations. To address this, a more rigorous definition of redundancy should incorporate the joint memory kernel of and . One refinement could involve integrating their cross-history dependencies through a convolution of their fractional score functions

where modulates the decay of cross-temporal interactions. This formulation explicitly penalizes redundant information that arises from overlapping historical trajectories, ensuring that shared memory effects are counted only once.

A critical consideration in our formulation of redundant information (Equation (35)) is the selection of the decay factor , which modulates how cross-temporal interactions between variables are weighted. This parameter governs how rapidly the influence of historical overlaps in information content diminishes over time. The theoretical basis for stems from the memory characteristics of the underlying economic processes. While in the Caputo fractional derivative determines the memory decay within individual variables, specifically controls the decay of cross-variable memory effects. The relationship between these parameters can be understood as follows: When , the cross-temporal interactions decay at the same rate as the memory within individual variables, suggesting symmetric memory effects across variables. When , cross-temporal interactions persist longer than individual memory effects, which may be appropriate for systems where joint historical influences (such as major economic shocks) leave a more enduring impact on multiple variables than on any single variable. Finally, when cross-temporal interactions decay more rapidly than individual memory, suitable for systems where correlations between variables are primarily short-term while individual variables exhibit longer memory.

In our empirical implementation, we determine through a calibration procedure that minimizes the residuals between observed joint information and the sum of estimated information components. Specifically, we select , which satisfies

where all components are computed using candidate values of within the range .

Synergistic information is then defined as the residual

where represents a fractional mutual information derived from the divergence between the joint and product distributions. A candidate definition leverages the Caputo derivative of the log-density ratio

This measure quantifies the divergence of the joint distribution from the product of marginals, weighted by the system’s historical dependencies. By grounding redundancy and synergy in the non-local dynamics of fractional calculus, this refined framework ensures consistency with the memory-aware structure of CFFI, avoiding overcounting while preserving interpretability.

The definition of fractional mutual information in Equation (38) naturally raises questions about whether this measure satisfies the fundamental information-theoretic properties of classical mutual information. We now examine two critical properties—non-negativity and monotonicity—and establish the conditions under which they hold in our fractional framework.

For classical mutual information, non-negativity ( ) follows directly from the Kullback–Leibler divergence properties. For the fractional mutual information , non-negativity requires additional consideration due to the presence of the Caputo fractional derivative. The fractional mutual information is non-negative for if the joint and marginal probability densities are -differentiable with respect to time and the processes exhibit memory decay consistent with the Caputo kernel. We can demonstrate this by rewriting Equation (33) in terms of a fractional Kullback–Leibler divergence

where the fractional KL divergence is defined as

Unlike the classical case, the non-negativity is not immediately evident. However, by applying the convexity of the logarithm function and the linearity of the Caputo derivative, we can establish that

Since the classical KL divergence is non-negative at each historical time point , and the Caputo kernel is positive for all , the fractional KL divergence inherits this non-negativity, provided that the memory decay is monotonic as governed by the Caputo kernel.

The monotonicity property in classical information theory states that conditioning on additional variables cannot increase mutual information. For fractional mutual information, we examine whether . The fractional mutual information satisfies the monotonicity property for under the same conditions required for non-negativity, plus the additional requirement that the memory effects are consistent across all variables. The key insight is that the Caputo derivative preserves the data processing inequality due to its linear, convolutional structure. At each historical time point , the classical monotonicity property holds for the instantaneous mutual information. The fractional derivative aggregates these historical values with a power-law weighting, preserving the direction of the inequality.

However, it is important to note that monotonicity may not hold under certain circumstances: when , introducing oscillatory effects in the memory kernel; when different variables exhibit inconsistent memory characteristics; or in the presence of strong non-stationarity that disrupts the temporal structure of information flow.

An important consideration in the CFFI-based PID framework is whether the Caputo Fractional Conditional Fisher Information (CFCFI) preserves the fundamental information-theoretic property that conditioning reduces uncertainty. Specifically, we need to establish whether the following inequality holds

This inequality is a cornerstone of classical information theory and is essential for a coherent partial information decomposition. We can demonstrate that this inequality holds for CFFI under appropriate conditions for stochastic processes , , and with joint probability density function that is -differentiable. Specifically, the inequality is valid for when the conditional probability densities and have continuous partial derivatives with respect to t, the fractional derivatives and are well defined, and the processes satisfy the Markov property with respect to their historical trajectories.

To establish this property, we recall our definitions of CFCFI

Using the law of conditional expectation and applying Jensen’s inequality to the convex function , we have

The Caputo derivative preserves the data processing inequality because it is a linear operator that applies a convolution with a positive kernel to the ordinary derivative

Since conditioning on additional variables cannot increase the variance of the score function at each historical time point , and the Caputo derivative applies a monotonic weighting to these historical scores, the inequality holds.

It is worth noting that this inequality may not hold in several scenarios. First, if , higher-order derivatives introduce oscillatory effects that could potentially violate the monotonicity property. Second, in strongly non-stationary processes where the impact of additional conditioning variables varies significantly across different historical periods, the inequality might be compromised. Third, when there are discontinuities in the probability densities, making the Caputo derivatives ill-defined at certain points, the relationship becomes uncertain.

The preservation of this inequality is crucial for our CFFI-based PID framework as it ensures that the unique, redundant, and synergistic information components maintain their information-theoretic interpretations when memory effects are included. By establishing this property, we confirm that the CFFI extension of PID provides a consistent framework for analyzing memory-driven information dynamics in economic systems.

3. Results and Discussions

3.1. Dataset

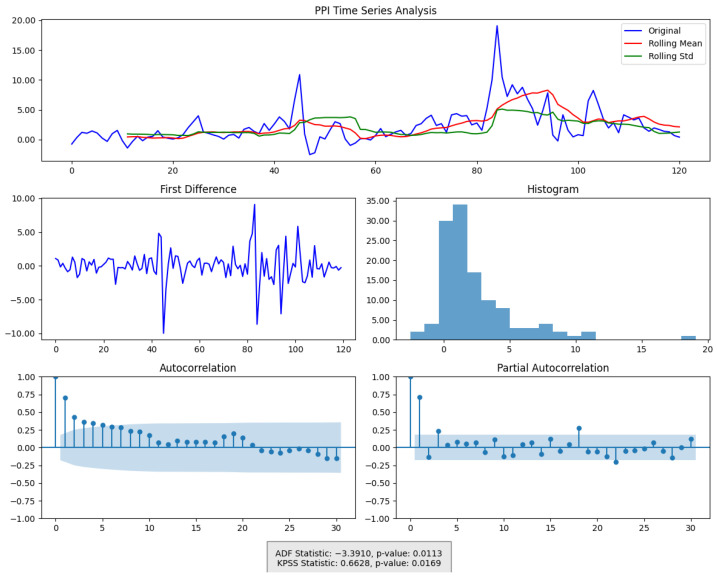

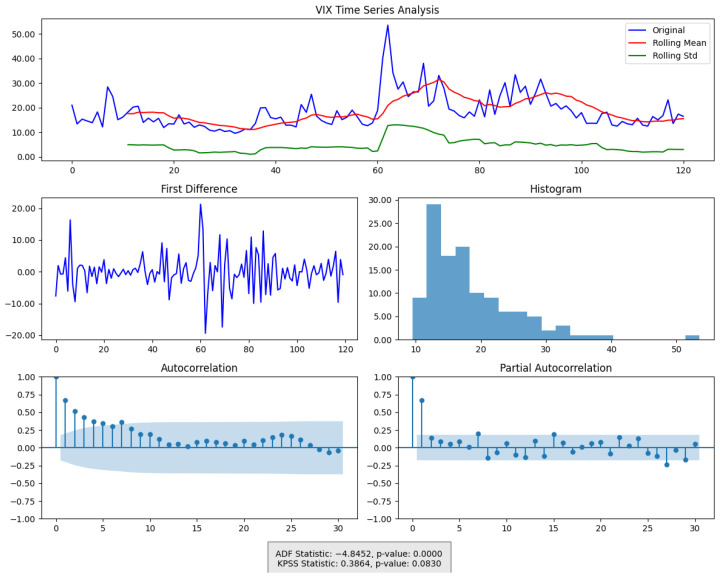

The dataset employed in this study spans a decade—from January 2015 to January 2025—and comprises monthly observations of five pivotal economic indicators for the Turkish economy: the Short-Term Policy Interest Rate (INTEREST), Credit Default Swap Spreads (CDS), the Consumer Price Index (CPI), the Producer Price Index (PPI), and the Volatility Index (VIX). These variables have been meticulously selected to capture the multifaceted dynamics underlying Turkey’s economic performance. Specifically, INTEREST, sourced from the Turkish Central Bank and cross-verified with data from the International Monetary Fund, reflects the nation’s monetary policy stance and its influence on borrowing costs and investment activities. CDS, obtained from Bloomberg and corroborated with data from Moody’s Analytics, provides a measure of credit risk and market sentiment regarding Turkish sovereign and corporate bonds. CPI and PPI, which are primary indicators of consumer and producer inflation, respectively, have been retrieved from the Turkish Statistical Institute and supplemented with regional data from the World Bank to ensure reliability. Lastly, VIX, acquired from the Chicago Board Options Exchange and adjusted for local market conditions, serves as an indicator of expected market volatility and investor uncertainty.

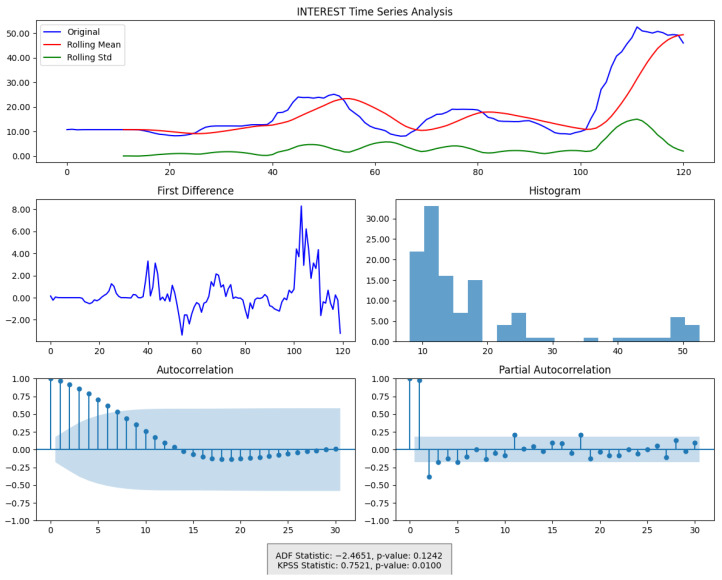

To ensure the robustness and scientific validity of our analysis, extensive data quality control measures are implemented. Each dataset has undergone rigorous crosschecking to guarantee the absence of missing values, and any identified gaps were systematically addressed using forward and backward imputation techniques. Additionally, to mitigate potential issues related to non-stationarity, moving averages are computed across the series, thereby smoothing short-term fluctuations and accentuating the underlying trends. The stationarity properties of the five economic indicators utilized in this study—INTEREST, CDS, CPI, PPI, and VIX—are also assessed through a combination of formal statistical tests and graphical analysis. Table A1 in Appendix A presents the results of the Augmented Dickey–Fuller (ADF) and Kwiatkowski–Phillips–Schmidt–Shin (KPSS) tests applied to both the original series and their first differences.

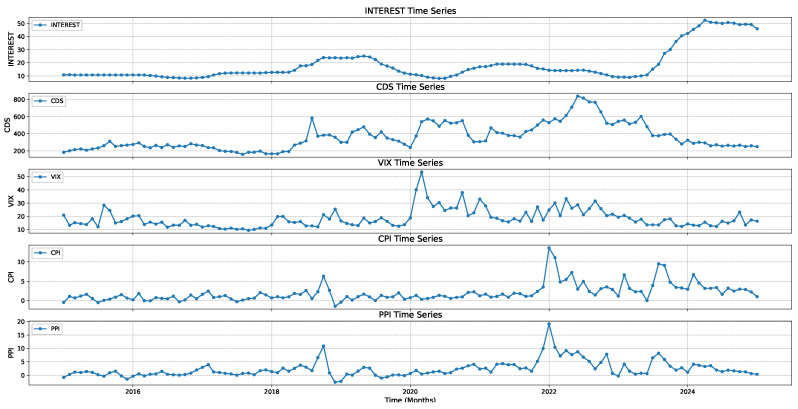

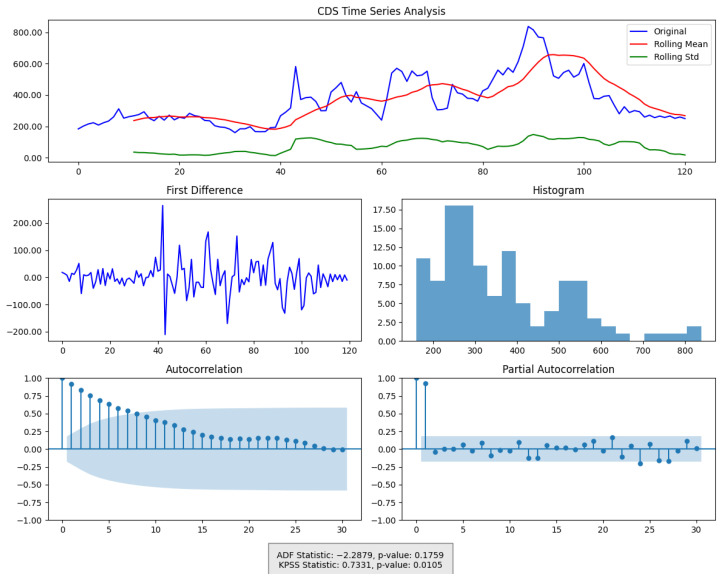

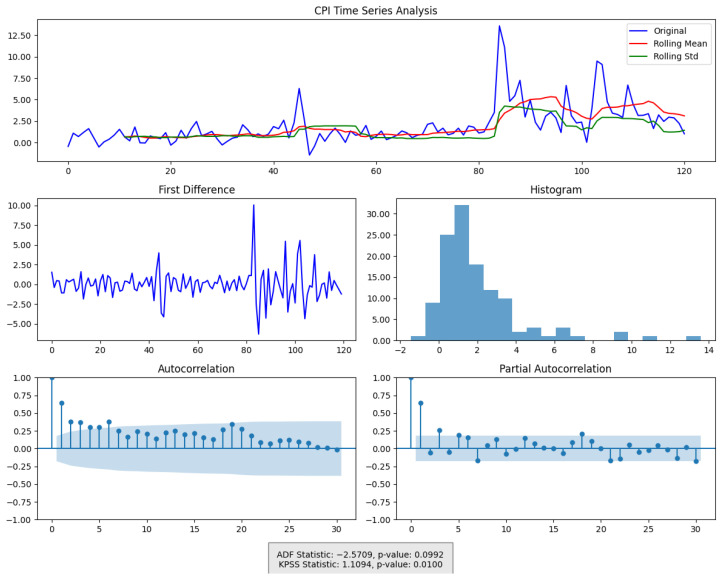

The time series of economic indicators are presented in Figure 1.

The distinct yet interrelated temporal patterns observed in Figure 1 underscore the potential for complex information flows among these economic indicators. For instance, sharp spikes in the INTEREST or VIX may contribute significantly to synergistic information when considered alongside other variables, while prolonged gradual trends—such as those in CPI or PPI—can exhibit memory effects that are well captured by fractional derivatives. CDS, showing intermittent jumps, may offer both unique and redundant information relative to the other series, depending on how strongly those jumps coincide with shifts in the remaining indicators. These observations motivate the use of measures like CFFI and PID, which can help disentangle how much of the variability in one series is uniquely explained by a particular indicator, how much is shared among multiple indicators, and how much arises from synergistic interactions across the entire system.

3.2. Results on CFFI

Our analysis begins with a robust discretization of the Caputo fractional derivative applied to our time series. For a series sampled at uniform time steps , the derivative of a function at time is approximated using a Riemann sum. In particular, the derivative is computed as

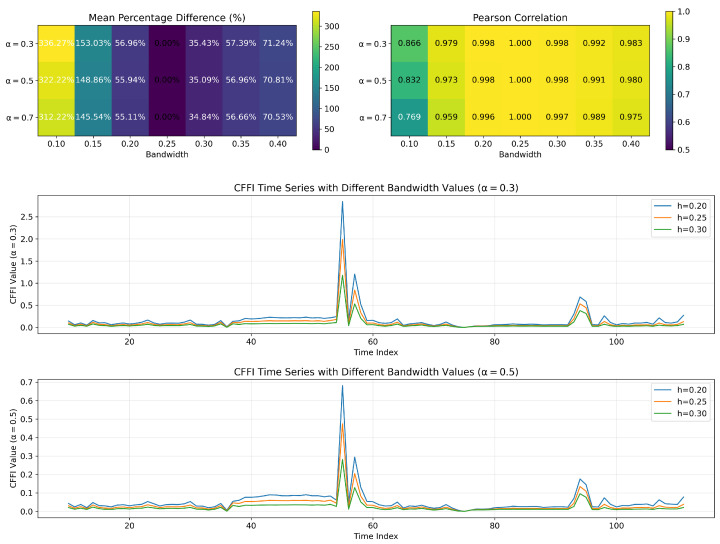

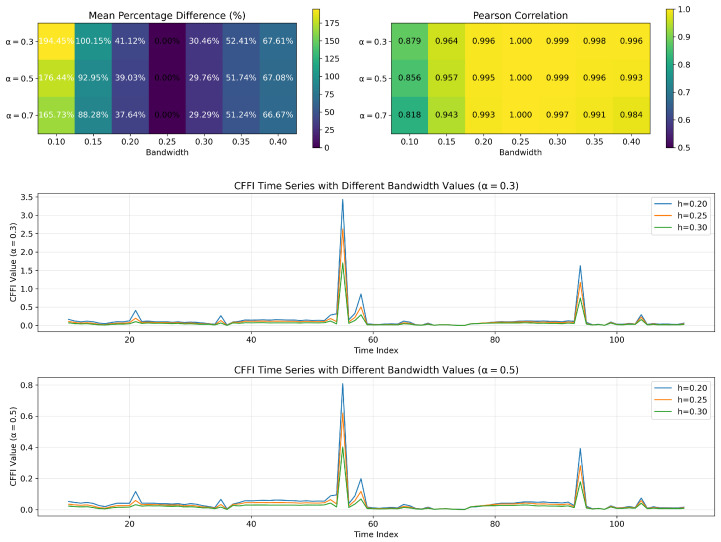

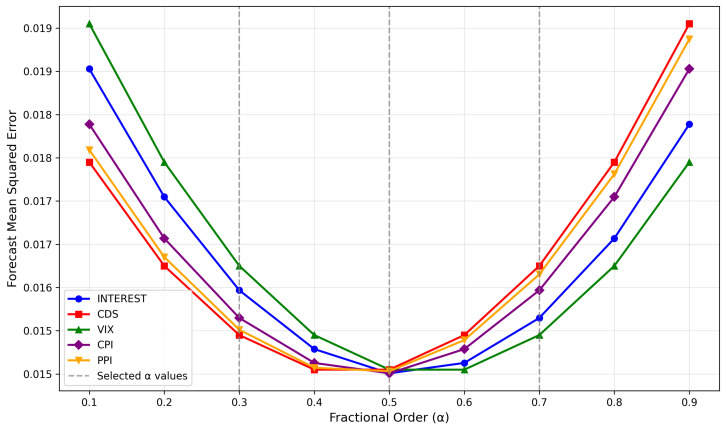

where is determined via finite differences (typically using a centered difference method), and is the Gamma function. A small constant (e.g., ) is introduced in the denominators to avoid numerical instabilities, and the fractional order is selected from values such as , , or to capture different strengths of memory effects. More details on the choice of values are presented in Appendix B, and sensitivity analysis for parameter is presented in Appendix C.

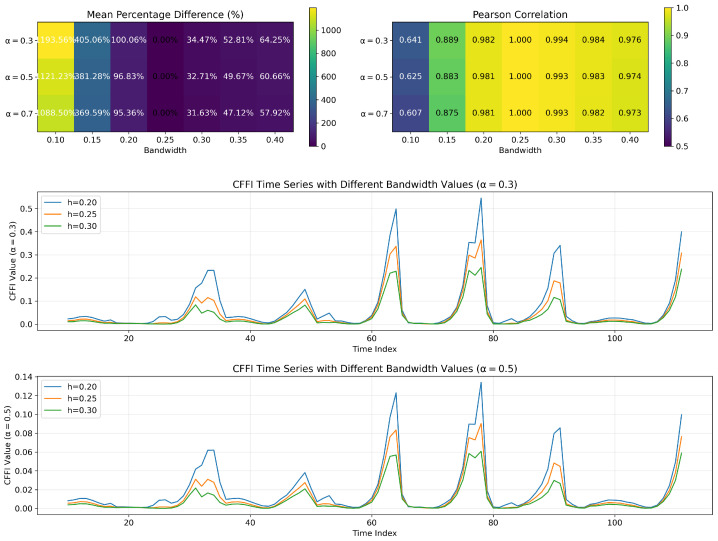

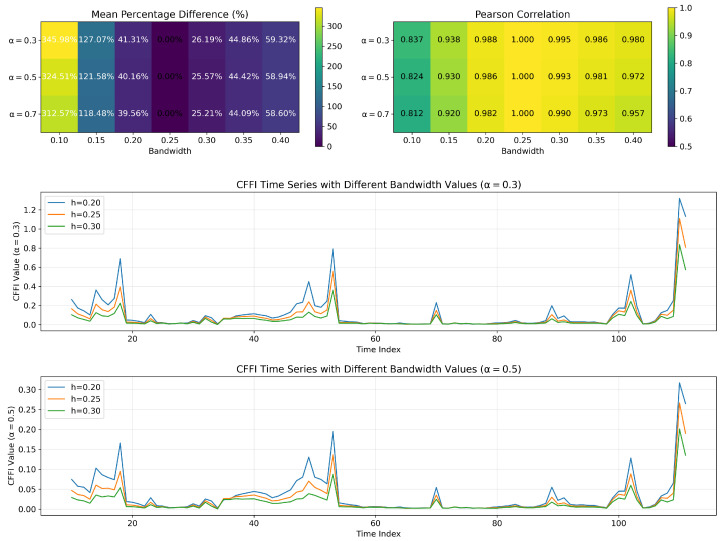

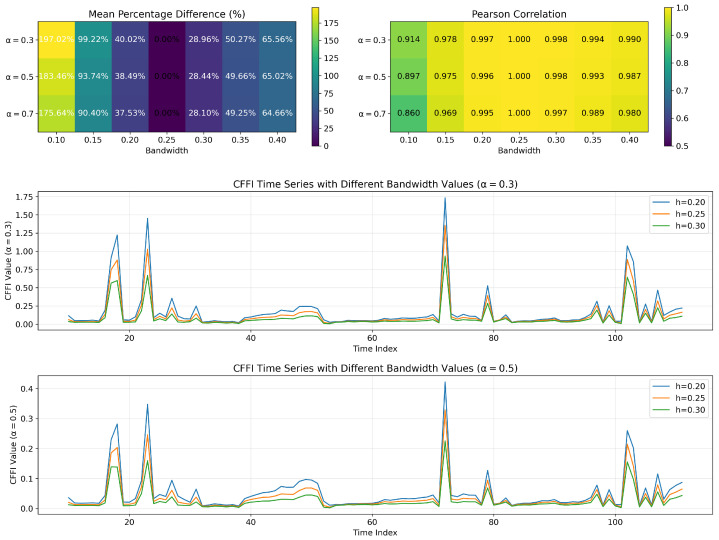

Subsequently, we estimate the log-density of the observed data using a non-parametric density estimation method. In this framework, the observed time series is smoothed using a kernel-based approach with a bandwidth parameter set to approximately – . This smoothing process yields an estimate of , which serves as the input for the fractional derivative calculation. The choice of bandwidth is critical as it balances the trade-off between resolution and smoothness, ensuring that the density is neither over-smoothed nor too noisy. Details on the bandwidth choice is presented in Appendix D.

While our theoretical framework is formulated in continuous time, practical implementation necessitates discrete-time approximation methods for analyzing sampled economic data observed at regular monthly intervals. For a discretely sampled time series with uniform time steps , we approximate the Caputo fractional derivative using the L1 scheme (first-order approximation)

where the weights are defined as for . This approximation carries a global truncation error of , which is sufficient for our monthly economic data, though higher-order schemes could be employed for higher frequency data if necessary.

The continuous CFFI definition in Equation (5) involves an expectation over the squared fractional score function, which we implement in discrete time as

where represents a grid of points spanning the support of the distribution, are quadrature weights proportional to , and is the kernel density estimate at time and value . We employ an adaptive grid refinement strategy that places more points in regions where the density or its derivative changes rapidly, thereby ensuring accurate numerical integration.

For density estimation, we utilize a Gaussian kernel with bandwidth h as previously discussed

where w defines the rolling window size (20 observations in our case), and is the standard Gaussian kernel. The log-density is then approximated as , with a small added to avoid numerical issues with near-zero density values.

Building on the estimated log-density and its fractional derivative, we define CFFI. This measure is computed as the expectation of the squared fractional derivative of the log-density, formally expressed as

In practical terms, for each time point, the squared value of the discretized fractional derivative is multiplied by to obtain an information measure analogous to the classical Fisher Information, yet modified to incorporate the non-local memory effects present in the system.

To capture the temporal evolution of these information measures, we implement a rolling-window analysis. The data are divided into overlapping segments of fixed size—typically 20 observations per window—and within each segment, the entire procedure (density estimation, fractional derivative computation, and CFFI calculation) is performed. The window is then incrementally advanced (with a step size of one observation), yielding a time series of CFFI estimates. This rolling-window approach provides a dynamic view of the information flow, enabling us to detect and analyze changes in the system’s informational characteristics over time.

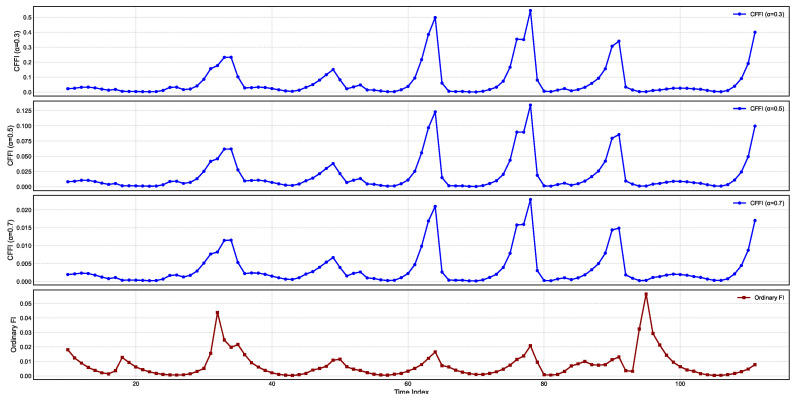

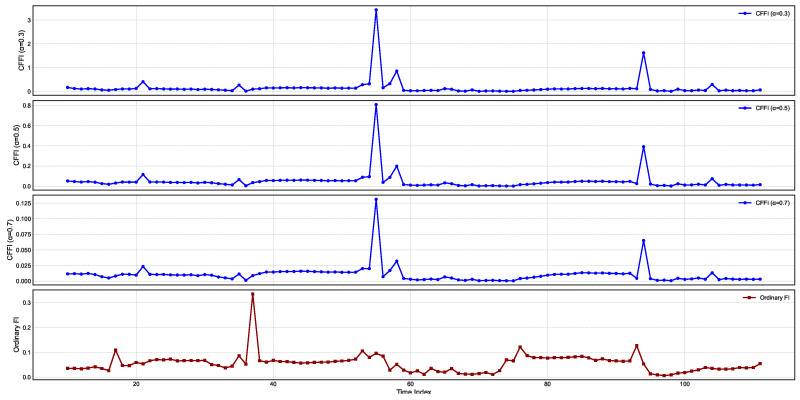

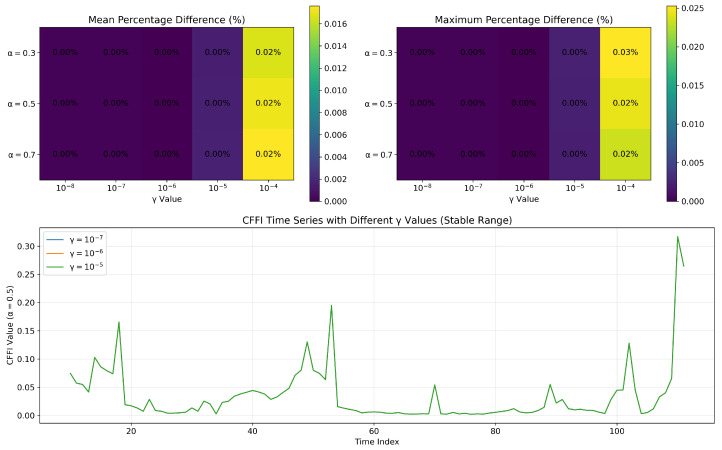

Figure 2 presents temporal changes on CFFI for INTEREST.

In all three fractional plots, the spikes in CFFI appear at consistent time indices, suggesting that the system undergoes pronounced changes in its probability distribution at these intervals. However, the amplitude of the peaks varies markedly with . For , the peaks are higher, indicating that the measure is more sensitive to past data when the system undergoes transitions. As increases to and , the peaks become smaller, reflecting a more moderate weighting of historical states in the fractional derivative. This outcome aligns with the notion that smaller values emphasize long-range memory effects, causing the measure to accumulate higher values during episodes of pronounced distributional shifts.

Comparing these fractional measures with the ordinary Fisher Information (OFI) in the bottom panel reveals both similarities and distinctions. All four plots show the same general pattern of repeated spikes, indicating that the timing of significant shifts in the underlying interest rate distribution is consistent regardless of whether memory is taken into account. Yet the scale of the OFI curve differs substantially, most notably when is small. In the fractional framework, historical influences accumulate over time, amplifying the response whenever the log-density undergoes changes. By contrast, OFI captures primarily local (i.e., instantaneous) sensitivity of the log-density to small perturbations, leading to lower overall peak magnitudes and a narrower perspective on how the system evolves.

From a dynamical standpoint, these results underscore the impact of long-range dependencies in modeling the sensitivity of the interest rate distribution to perturbations. The high-amplitude spikes for reflect a strong memory effect, where past fluctuations remain influential for a longer duration and thus elevate the CFFI values. As grows closer to 1, the measure converges toward OFI, resulting in more moderate peak values and reduced sensitivity to historical states.

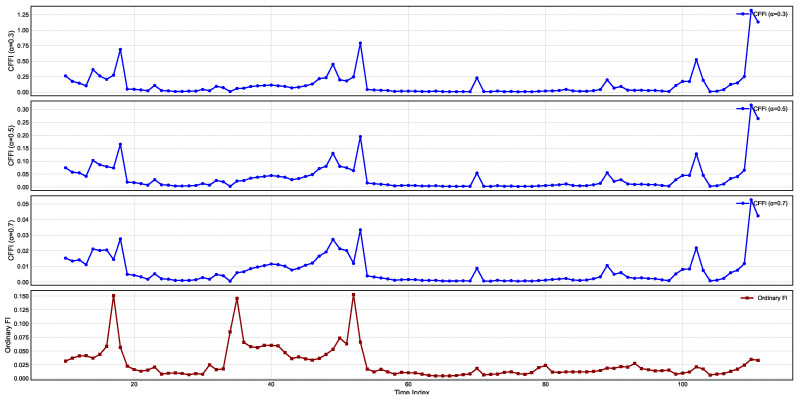

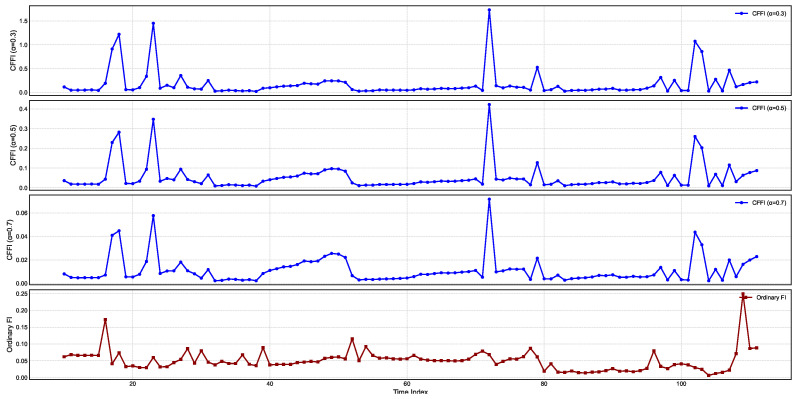

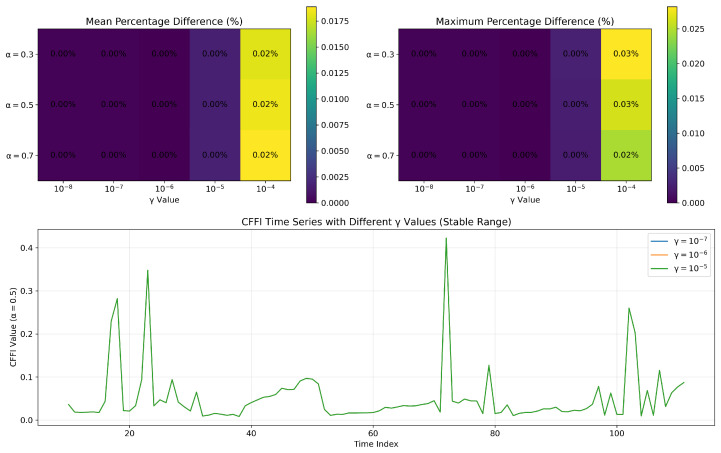

Figure 3 presents temporal changes on CFFI for CDS.

CFFI curves for CDS series exhibit pronounced peaks at specific time indices, suggesting intervals during which the probability distribution of CDS experiences heightened sensitivity to perturbations. For each fractional order , the spikes occur broadly in the same locations, indicating that the primary shifts in the underlying CDS distribution are robust to changes in the fractional order. However, the magnitude of these peaks diminishes as increases, reflecting a progressive reduction in how strongly historical states influence the present. Smaller values (e.g., ) emphasize longer-range memory effects, thereby producing higher peaks when significant distributional changes occur, whereas larger values place more emphasis on more recent data, leading to relatively lower peak heights.

While both the CFFI and OFI exhibit their most notable rises around similar time points, the fractional measures typically reach higher or more sustained values, especially for smaller . This discrepancy stems from the fact that the CFFI integrates historical gradients of the log-density via a power-law kernel, thereby aggregating the influence of prior states into the current measure. By contrast, the OFI captures only the instantaneous sensitivity of the log-density, effectively treating the CDS series as Markovian and memoryless. Consequently, the OFI curve often displays narrower spikes, reflecting the immediate response to distributional changes without the extended contribution of past data. These results emphasize the importance of fractional approaches for capturing the long-term dependencies that can characterize CDS behavior, particularly in contexts where market sentiment and risk assessments accumulate over time.

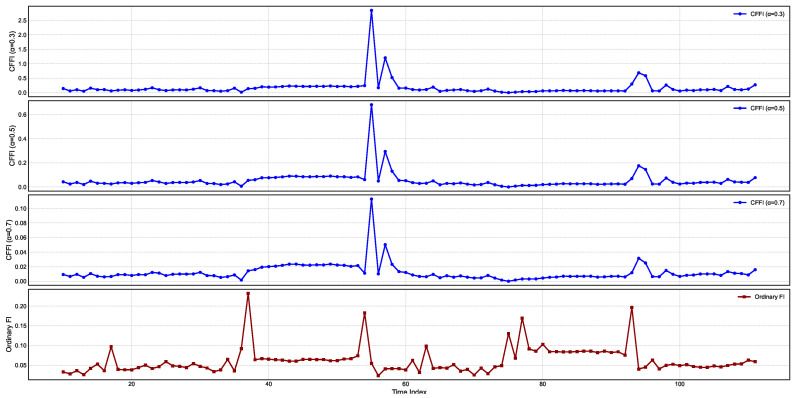

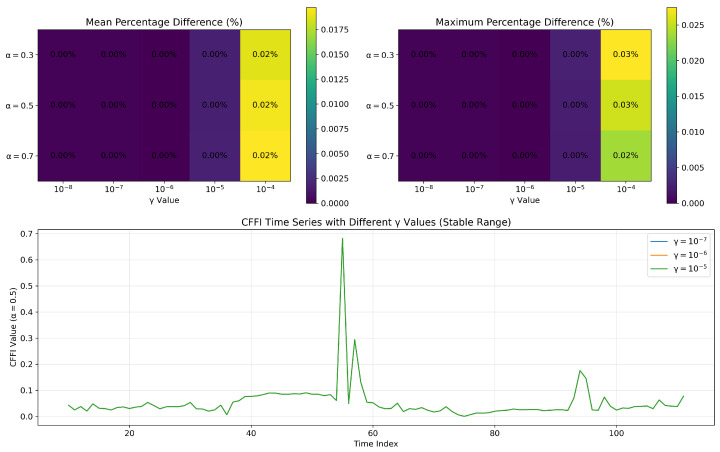

Figure 4 presents temporal changes on CFFI for CPI.

CFFI curves for CPI, a particularly large spike emerges around the same time index for all fractional orders. This sudden jump indicates a moment of heightened sensitivity in the CPI distribution, suggesting that the underlying statistical properties of CPI underwent a marked shift. Although the exact timing of this spike remains consistent across different values, the amplitude varies, with the lower fractional order ( ) showing a more pronounced peak. Such behavior reflects the stronger memory effect introduced by smaller , whereby more distant historical states exert a cumulative influence on the current dynamics, thus amplifying the response whenever there is a significant change in the probability distribution.

A closer look at the CFFI plots for higher fractional orders, such as , reveals that while the major transition is still captured, its magnitude is less extreme. This reduction in peak height illustrates how larger places greater emphasis on more recent states, effectively tempering the contributions of longer historical windows. Consequently, the measure remains sensitive to major distributional shifts but does so with a shorter memory horizon. A smaller second spike in the and curves further highlights how a longer memory can detect subtle variations in the distribution that might be overlooked or appear muted when memory is shortened.

The OFI exhibits multiple peaks of moderate amplitude, capturing the localized changes in CPI distribution. However, it does not reflect the same degree of cumulative effect seen in the smaller curves, which more aggressively aggregate historical gradients of the log-density. As a result, the OFI and higher curves converge toward similar profiles, whereas the lower measures stand out with their sharper, more pronounced transitions.

Figure 5 presents temporal changes on CFFI for PPI.

For smaller fractional orders, such as , the amplitude of these spikes is especially large, underscoring the stronger memory effect that emerges when historical data are given substantial weight. In contrast, higher fractional orders ( and ) continue to capture the same core transitions but with lower peak magnitudes, illustrating that shorter memory horizons dampen the impact of older states on the present information measure. OFI in the bottom panel captures some of the same transitions but lacks the pronounced accumulation of effects characteristic of lower fractional orders, thus producing lower or narrower peaks overall.

When compared to CPI, which also exhibited prominent spikes in its fractional information measures, the PPI displays timing and amplitude patterns that can be slightly offset. Such differences highlight how producer-level price changes may lead or lag shifts at the consumer level. From a memory perspective, the PPI’s smaller- curves more vigorously integrate historical fluctuations in producer costs, amplifying the response to any abrupt distributional change. Meanwhile, CPI may reflect downstream effects of these shifts but with its own timing and magnitude. Observing both PPI and CPI through the lens of fractional derivatives thus provides a complementary view of inflationary pressures, capturing how price changes at the producer stage can propagate to consumer prices with distinct delays and intensities.

Figure 6 presents temporal changes on CFFI for VIX.

Across all fractional orders, these peaks generally occur at similar time indices, but the amplitudes vary considerably, reflecting the different strengths of memory effects encoded in each . When is small, the measure integrates historical data more extensively, which can amplify responses to a single abrupt change and produce higher peak values. In contrast, larger places more weight on recent data, leading to comparatively tempered spikes that still capture the timing of significant transitions but with a reduced magnitude.

By comparing these curves with OFI at the bottom, one observes that the memoryless framework also registers a series of peaks aligned with the most prominent shifts in the PPI distribution. However, OFI tends to exhibit either narrower or lower spikes than those seen for smaller fractional orders, underscoring the role of historical influences in magnifying the fractional measures. This dynamic is particularly important for producer-level inflation, where past fluctuations in costs or supply conditions can reverberate through time. In periods of rapid change—whether triggered by commodity price shocks or policy shifts—the fractional derivatives accumulate the effects of earlier volatility, often producing sharp surges in the CFFI. The ordinary measure, by contrast, responds primarily to the immediate local gradient in the log-density, missing some of the accumulated impact of past states. These results highlight the potential value of a fractional calculus perspective for studying inflationary processes as it can reveal how lingering producer-side shocks shape the distribution over longer horizons.

3.3. Correlation Analysis

To investigate cross-indicial dependencies, we conduct correlation and transfer entropy analyses on rolling estimates of CFFI and OFI for each index. The correlation analysis evaluates linear pairwise relationships between indices, facilitating the identification of synchronous patterns and shared trends in informational dynamics across diverse markets. Complementarily, transfer entropy is employed to quantify directional information flow between indices, thereby capturing non-linear and asymmetrical dependencies that may signify lead–lag relationships.

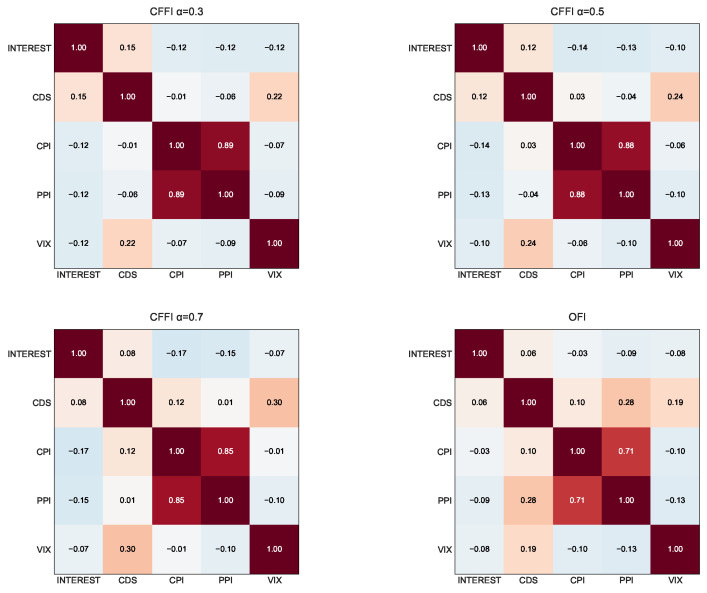

Figure 7 depicts correlation matrices.

From an information-theoretic perspective, the correlation matrices based on CFFI in Figure 7 reveal how the informational dynamics of key economic indicators co-evolve under different memory assumptions. The CFFI quantifies how sensitive an index’s probability distribution is to its past behavior, and by comparing these measures across indices, we gain insight into the shared historical influences among them. When is small, such as , the CFFI places considerable weight on long-range memory; this means that the accumulated historical shifts in an index’s distribution significantly drive its information measure. In practical terms, a strong correlation at between INTEREST and CDS suggests that the deep-rooted, historical sensitivities of monetary policy signals and perceived default risk are tightly linked, possibly reflecting persistent economic regimes or long-term policy influences. As increases to 0.7, the CFFI becomes more responsive to recent fluctuations rather than extended historical trends. This transition can lead to altered correlations, for instance, between CPI and PPI, if their short-term inflationary dynamics diverge from their long-term patterns.

In contrast, the memoryless OFI captures only the local, instantaneous sensitivity of the distribution, often yielding moderate correlations that overlook the layered, historical dependencies detected by fractional models. For example, while the correlation between INTEREST and VIX may appear moderate under OFI, the stronger association observed under CFFI at indicates that long-term market volatility is more closely linked to the enduring effects of monetary policy signals. Overall, these comparative analyses underscore the value of incorporating memory effects into information measures as doing so unveils deeper, more nuanced interdependencies among critical economic indicators such as interest rates, credit risk, inflation measures, and market volatility.

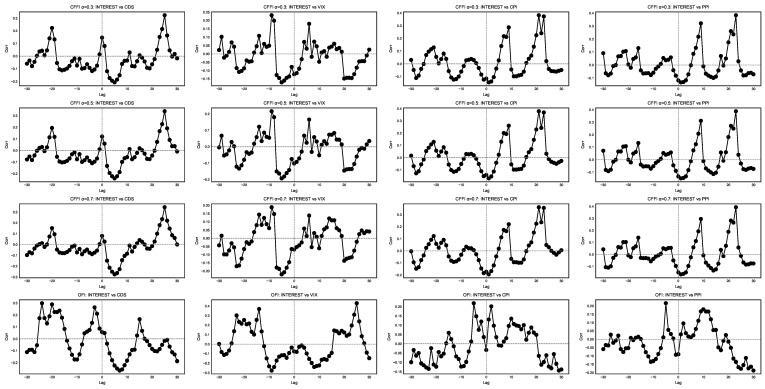

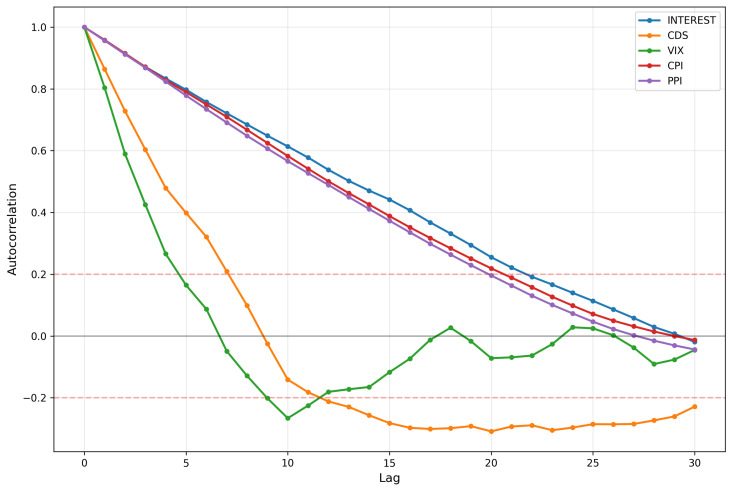

Figure 8 displays cross-correlation analyses with lags between selected indices.

In Figure 8, each row corresponds to a particular way of modeling the memory embedded in the informational dynamics of short-term policy interest rates (INTEREST) and various economic indicators (CDS, VIX, CPI, and PPI). Each column compares INTEREST with a different indicator—credit default swaps (CDSs), implied market volatility (VIX), consumer inflation (CPI), or producer inflation (PPI)—across time lags. The horizontal axis denotes the lag, where positive lags suggest that changes in the first series precede changes in the second, and negative lags indicate the opposite ordering. Peaks in these curves reveal potential lead–lag relationships, while their width and height reflect the persistence and magnitude of the co-movement.

From an information-theoretic viewpoint, smaller values of assign substantial weight to deep historical states when computing the CFFI. In the top row, this often manifests as broader or more pronounced cross-correlation peaks, implying that extended past conditions in one index’s distributional shifts—such as a persistently low interest rate regime—can foreshadow future movements in another indicator’s information measure. For instance, if CFFI : INTEREST vs. CDS exhibits a strong positive-lag peak, it suggests that historically rooted shifts in monetary policy signals have long-lasting effects on perceived credit risk, driving CDS dynamics with a delay. Conversely, as grows to 0.5 or 0.7, the CFFI becomes more sensitive to recent changes, causing narrower peaks closer to zero lag. Under these more moderate memory horizons, immediate feedback loops—such as short-term market reactions to interest rate announcements—can dominate the correlation structure, reducing the influence of older policy regimes on current credit risk or volatility expectations.

Comparing these fractional rows to the OFI row in the bottom panels highlights the differences between memory-sensitive and memoryless frameworks. OFI emphasizes local, instantaneous changes in the distribution of each index, so the cross-correlations frequently peak near zero lag and show fewer secondary peaks at large positive or negative lags. This can obscure certain lead–lag patterns that fractional measures detect. For instance, OFI: INTEREST vs. VIX may show a moderate peak around lag zero, suggesting an immediate reaction of implied market volatility to interest rate signals, yet it may lack the long-tail behavior visible in CFFI : INTEREST vs. VIX. Such a discrepancy implies that short-run volatility responses can be captured by OFI, whereas extended historical influences—such as entrenched monetary regimes that shape long-term risk appetites—are only discernible through fractional measures with smaller .

From an economic perspective, these differences matter because interest rates, credit risk, volatility, and inflation indicators can each embody a distinct combination of short-term shocks and long-term structural factors. If, for example, INTEREST and PPI exhibit sustained correlations at a positive lag under , it may indicate that entrenched monetary policy paths eventually feed into producer-level price pressures over extended horizons. On the other hand, smaller-lag peaks under or OFI might reflect quicker pass-through effects, such as immediate cost changes that producers face after a policy announcement.

3.4. Transfer Entropy

Table 1 displays transfer entropy results for the configuration .

A small fractional order accentuates long-range memory, so each index’s deep historical states strongly shape its present-day distributional changes. Notably, the largest transfer entropy arises from INTEREST to VIX, implying that the historical accumulation of short-term policy signals carries significant predictive power over implied market volatility’s informational dynamics. In other words, when the central bank’s policy stance—embedded in INTEREST’s distribution—shifts after a protracted historical buildup, it can substantially alter how the VIX distribution evolves, reflecting heightened sensitivity in markets prone to long-lasting monetary conditions. A similarly robust effect appears from CDS to VIX, suggesting that perceived default risk exerts a directional influence on volatility measures, further underscoring how risk premiums can ripple through markets over extended horizons.

On the inflationary front, the asymmetry between CPI → PPI and PPI → CPI is striking. The larger transfer entropy from CPI to PPI suggests that consumer-level inflation signals, when viewed through a long-memory lens, convey more informational impact on producer-level price shifts than vice versa. This may indicate that protracted changes in consumer inflation—possibly linked to entrenched expectations or wage-price spirals—eventually filter back into producers’ pricing decisions, influencing their cost structures and profit margins. By contrast, the lower value from PPI to CPI implies that while producer prices still offer some informational cues for consumer inflation, the effect is relatively weaker under strong memory conditions, highlighting the role of sustained demand-side pressures.

Comparisons to correlation or cross-correlation findings reinforce these interpretations. A strong correlation may reveal synchronous or lagged co-movements, but the directionality gleaned from transfer entropy is key for understanding which index actively drives shifts in another’s informational content. For instance, a moderate correlation between INTEREST and VIX might mask the fact that, under , policy signals truly lead volatility rather than simply co-moving.

Table 2 displays transfer entropy results for the configuration .

At , CFFI balances long-range memory with a more immediate focus on recent distributional shifts, creating an intermediate memory horizon. As shown in Table 2, many of the transfer entropy (TE) values exceed those at , indicating that while historical influences remain important, mid-range changes in an index’s distributional behavior now hold greater sway. For instance, the largest directional influence appears from INTEREST to VIX (0.226628), which is even more pronounced than at . This heightened flow of information suggests that intermediate-horizon monetary policy signals may drive market volatility more forcefully as traders and investors respond to evolving policy expectations without fully relying on deep historical anchors. By the same token, VIX itself exerts a stronger influence on INTEREST and CDS compared to smaller , implying that intermediate-memory processes can also capture feedback loops in which volatility shifts feed back into credit risk perceptions and policy considerations.

From an economic perspective, these results highlight how the mid-range memory captured at can amplify or reconfigure certain lead–lag relationships that were less prominent at . INTEREST and CDS exhibit reciprocal influences (0.179559 vs. 0.184342), suggesting that moderately persistent signals in monetary policy and credit markets inform each other’s informational changes. Meanwhile, CPI’s stronger bidirectional TE with both INTEREST and CDS—compared to smaller —hints that consumer-level inflation data, when viewed over a moderate historical window, becomes more influential in shaping interest rate expectations and risk premiums. PPI still registers notable information flows to and from CPI, consistent with the notion that producer-level and consumer-level inflation remain interlinked, but the intermediate memory horizon may emphasize shorter supply-chain effects rather than deeply entrenched pricing regimes.

Comparing these findings to those at suggests that certain relationships intensify as the model shifts away from deep historical accumulation toward more recent signals. The fact that INTEREST, CDS, and VIX exhibit consistently high transfer entropy values underscores their collective role in shaping market sentiment and risk, but the specific magnitudes at reveal how mid-range memory can reinforce feedback loops that are less visible under a predominantly long-memory ( ) framework. Consequently, while smaller can uncover enduring monetary or risk-based regimes, highlights how moderately persistent signals also carry significant informational weight, potentially aligning more closely with the fluid market adjustments and evolving economic narratives typical of a mid-term horizon.

Table 3 displays transfer entropy results for the configuration .

At , TE values indicate that a shorter memory horizon captures more immediate, recent dynamics in the informational interplay among economic indicators. For example, the directional flow from INTEREST to CDS increases significantly—from roughly 0.099 at to 0.256 at —implying that recent shifts in monetary policy have a pronounced impact on credit risk as perceived through CDS spreads. Similarly, the transfer entropy from CDS to INTEREST rises steadily across the spectrum, reaching approximately 0.275 at , which suggests a strong feedback mechanism where contemporary changes in credit risk also influence policy signals. In contrast, the relationship between INTEREST and VIX appears to be more nuanced; while the TE from CDS to VIX increases with higher , the value from INTEREST to VIX peaks at an intermediate memory length ( ) and then slightly declines at . This pattern may indicate that the impact of monetary policy on market volatility is maximized when recent dynamics dominate but does not necessarily continue to intensify with an even shorter memory window.

Additionally, the TE values involving inflation measures (CPI and PPI) generally increase as rises, suggesting that, over a shorter memory horizon, consumer and producer price changes are more strongly interrelated with shifts in monetary policy. Overall, these findings from Table 3—when compared with the lower values—demonstrate that a mid-range memory horizon enhances the detectability of directional information flows, highlighting the immediate responsiveness of economic agents to recent events, while also underlining that certain relationships, such as those involving market volatility, may be optimized at intermediate memory levels rather than at the shortest horizons.

Table 4 displays transfer entropy results for OFI.

Under the memoryless framework provided by OFI, the transfer entropy values indicate a moderate yet consistent flow of information among key economic indicators. For instance, the directional transfer entropy from INTEREST to CDS is approximately 0.296 and nearly 0.290 in the reverse direction, suggesting a robust mutual linkage between monetary policy signals and credit risk. Similar values observed for the interactions between INTEREST and VIX (around 0.311 and 0.285, respectively) point to an immediate and symmetric influence between policy measures and market volatility. Furthermore, the relatively similar transfer entropy values between inflation measures—such as CPI and PPI—reinforce the notion that, in the absence of long-memory effects, the instantaneous sensitivities across these indices are stable and homogeneous.

Comparing these OFI-based results to the fractional CFFI outcomes reveals key differences in the informational dynamics. Fractional models, particularly at lower values like 0.3 and moderate values like 0.5, tend to amplify or differentiate directional dependencies by incorporating extended historical information. For example, while the OFI approach shows a moderate and nearly symmetric exchange between INTEREST and CDS, the fractional measures might reveal a stronger or more asymmetric influence when long-range memory effects are considered. This suggests that while OFI captures the immediate response of economic agents to market shocks, the fractional framework can uncover deeper, lagged interactions that emerge over longer horizons. Economically, these findings imply that short-term market adjustments—such as rapid policy responses or sudden shifts in credit conditions—are well represented by OFI, whereas the incorporation of memory through fractional measures may highlight delayed, yet significant, influences that affect market volatility, inflation, and overall risk perceptions in a more nuanced manner.

3.5. Partial Information Decomposition

Now, we present PID analysis results with selecting INTEREST as the dependent variable. INTEREST plays a pivotal role in monetary policy transmission, and our correlation analyses reveal that its informational dynamics are closely interwoven with those of CDS, VIX, CPI, and PPI under various memory assumptions. The consistently robust correlations indicate that fluctuations in interest rates are intimately linked with shifts in credit risk, market volatility, and inflationary trends. Moreover, our transfer entropy analyses underscore a significant directional flow of information between INTEREST and the other indices, with notable evidence that historical variations in interest rates can predict subsequent changes in these economic variables.

PID results are presented in Table 5 for different configurations. For the analysis presented in this paper, we employ values that are approximately times the corresponding value for each fractional order, reflecting the empirical observation that cross-variable memory effects in economic systems typically decay somewhat faster than within-variable memory.

In these PID results, the unique information components reveal the extent to which each source index provides distinct, non-overlapping insights into the evolution of INTEREST. For instance, under the fractional framework with , the unique contributions from CDS, CPI, PPI, and VIX are relatively high, indicating that deep historical memory allows each of these economic variables to impart considerable individual influence on interest rate dynamics. From an information-theoretic perspective, this means that the probability distribution shifts of each index carry substantial autonomous signals that can affect monetary policy outcomes. Economically, such pronounced unique information is consistent with scenarios where prolonged monetary accommodation or sustained risk perceptions distinctly shape different facets of the financial environment, such as credit conditions or inflation expectations.

As the fractional order increases to and further to , the unique information values decline markedly. This reduction suggests that when the analysis gives more weight to recent data, the distinct long-term contributions of each source become less pronounced, thereby diminishing the individual signals that were evident under a long-memory regime. Concurrently, the redundant information—which represents the overlap in the informational content among the indices—also decreases as increases, reflecting a shift from enduring, shared historical influences to more immediate and idiosyncratic responses. However, the most striking change is observed in the synergistic information component. At , the synergistic value is exceptionally high, implying that the combined effect of these indices produces emergent dynamics that far exceed the sum of their individual contributions. This synergistic interplay is indicative of a complex, interdependent system where long-term interactions and historical contingencies drive interest rates in a way that is only revealed when deep memory is accounted for.

In contrast, under the memoryless OFI framework, all three PID components—unique, redundant, and especially synergistic—are uniformly lower. The OFI results suggest that when only the immediate, local changes in the information measures are considered, the cumulative and cooperative effects of the sources are largely missed. The relatively muted unique values in OFI imply that instantaneous responses of each economic variable do not capture the rich, individually distinct influences that arise when historical dependencies are incorporated. Similarly, the lower redundant and synergistic values under OFI indicate that the emergent, joint informational effects among CDS, CPI, PPI, and VIX are significantly underrepresented in a memoryless context. Consequently, while OFI may offer a snapshot of immediate interactions, the fractional PID approach provides a more comprehensive understanding of how both historical and short-term dynamics intertwine to shape monetary policy, as reflected in the evolution of interest rates. Ultimately, these findings underscore the critical importance of accounting for long-range memory when modeling the complex interplay of economic indicators as doing so unveils deeper interdependencies that are essential for robust economic forecasting and policy analysis.

4. Conclusions

In this study, we explored the dynamic interplay among key economic indicators by applying CFFI framework alongside the traditional Ordinary Fisher Information. Our analysis spanned multiple fractional orders, which allowed us to uncover how long-term memory and short-term dynamics differently shape the informational structure underlying monetary policy, credit risk, market volatility, and inflation measures. By incorporating advanced techniques such as correlation analysis, cross-correlation functions, transfer entropy, and PID, we quantified not only the intensity of pairwise relationships but also the directional and synergistic contributions among these variables.

The findings reveal that when long-range memory is emphasized—reflected in lower fractional orders such as —each index conveys substantial unique and synergistic information. For instance, during prolonged periods of monetary accommodation as seen in the aftermath of the global financial crisis, the historical accumulation of low interest rates left a deep imprint on credit risk measures like CDS spreads. Such persistent dynamics result in high transfer entropy values and strong correlations between INTEREST and CDS, highlighting how past monetary policy significantly influences market perceptions of default risk. As the fractional order increases to and further to , the model shifts focus toward more immediate, short-term changes, resulting in a noticeable reduction in the unique and redundant components and a marked decline in the synergistic information. This suggests that while immediate market reactions—such as the rapid adjustment in market volatility following a policy announcement—are captured by higher values, the profound, intertwined effects that emerge over extended periods are attenuated.

In contrast, the memoryless OFI framework consistently underestimates these deeper, synergistic interactions. OFI tends to capture only the instantaneous, localized responses among the variables, such as the immediate volatility spikes following a rate change, but fails to reveal the enduring, historically embedded relationships that the fractional models uncover. Economically, these findings underscore the importance of considering long-term memory effects: during episodes like the European debt crisis, for example, sustained uncertainty and prolonged low interest rates influenced market volatility and risk perceptions in ways that a short-term, memoryless analysis could not fully capture.

Ultimately, by embracing the complexity of long-range dependencies through fractional analysis, our results offer a compelling call for integrating memory-sensitive approaches into economic modeling—an essential step toward more resilient and adaptive policy-making in an increasingly complex financial landscape. For monetary authorities, our findings suggest that policy decisions should incorporate fractional information measures to better account for the lingering effects of past interventions, particularly given the strong memory-driven synergies observed between interest rates and market volatility indicators. Central banks could improve policy effectiveness by calibrating intervention timing and magnitude based on CFFI-derived insights about how historical information propagates through the system with power-law decay rather than exponential dissipation. Similarly, financial regulators would benefit from adopting fractional information decomposition techniques to identify early-warning signals of systemic risk that emerge from the interplay between long-memory processes in credit markets and inflation indicators. Such an approach would enable more proactive macroprudential policies by distinguishing between short-term noise and genuine information shifts in market dynamics. More broadly, economic forecasting frameworks could enhance their predictive accuracy by replacing conventional information measures with fractional alternatives that capture how historical market conditions continue to influence present dynamics even after considerable time has elapsed.

By quantifying these memory effects through CFFI analysis, policymakers can develop more nuanced intervention strategies that acknowledge the persistent informational impact of past economic shocks, ultimately leading to more stable financial markets and improved economic outcomes in environments characterized by complex interdependencies and long-range memory effects.

The reference list from the paper itself. Each links out to its DOI / PubMed record.

- 1Makowski M. Piotrowski E.W. Frąckiewicz P. Szopa M. Transactional interpretation for the principle of minimum Fisher information Entropy 202123146410.3390/e 2311146434828162 PMC 8622043 · doi ↗ · pubmed ↗

- 2Kyrtsou C. Mikropoulou C. Papana A. Exploitation of Information as a Trading Characteristic: A Causality-Based Analysis of Simulated and Financial Data Entropy 202022113910.3390/e 2210113933286908 PMC 7597289 · doi ↗ · pubmed ↗

- 3Ruiz Reina M.Á. Entropy method for decision-making: Uncertainty cycles in tourism demand Entropy 202123137010.3390/e 2311137034828069 PMC 8623377 · doi ↗ · pubmed ↗

- 4Saldanha D. Mallikarjunappa T. Oware K.M. Determinants of adaptive behaviour in stock market: A review Vision 20252911212410.1177/09722629221148809 · doi ↗

- 5Jakimowicz A. The role of entropy in the development of economics Entropy 20202245210.3390/e 2204045233286226 PMC 7516932 · doi ↗ · pubmed ↗

- 6Gutiérrez O. Salas-Fumás V. Agency Contracts under Maximum-Entropy Entropy 20212395710.3390/e 2308095734441097 PMC 8393672 · doi ↗ · pubmed ↗

- 7Novais R.G. Wanke P. Antunes J. Tan Y. Portfolio optimization with a mean-entropy-mutual information model Entropy 20222436910.3390/e 2403036935327880 PMC 8947404 · doi ↗ · pubmed ↗