Analytic solutions of variance swaps for Heston models with stochastic long-run mean of variance and jumps

Jing Fu, Mazyar Ghadiri Nejad, Mazyar Ghadiri Nejad, Mazyar Ghadiri Nejad

TL;DR

This paper provides new formulas for pricing variance swaps using an advanced Heston model that includes jumps and a changing long-term variance mean.

Contribution

The paper introduces a novel pricing formula for variance swaps with a Heston model that includes stochastic long-run mean and jumps.

Findings

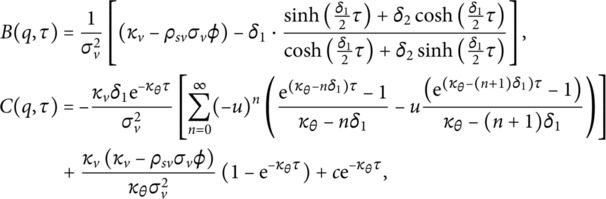

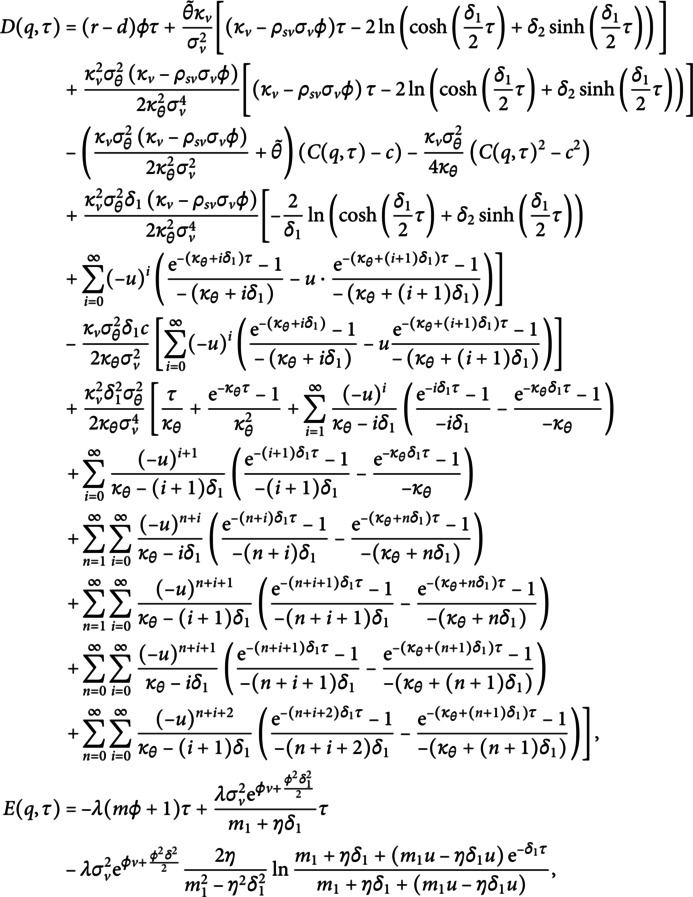

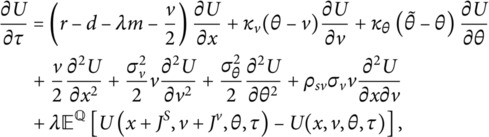

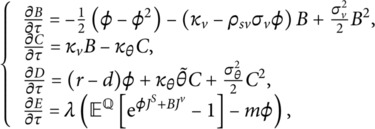

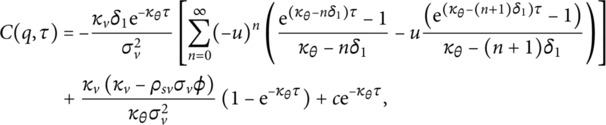

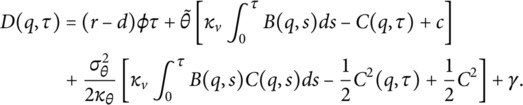

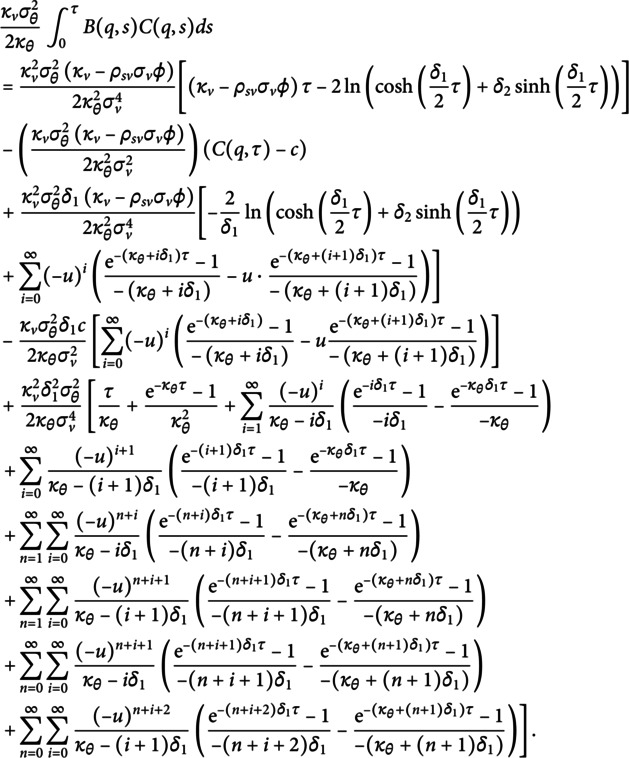

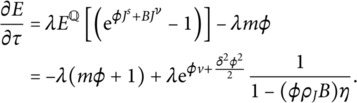

A partial integro-differential equation is derived for the joint moment-generating function.

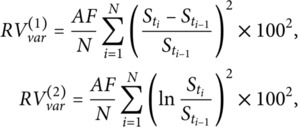

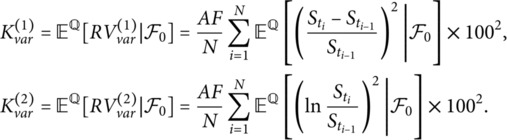

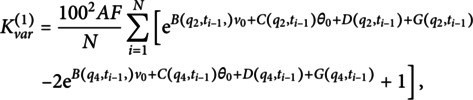

A series pricing formula is developed for discretely sampled variance swaps.

Numerical simulations confirm the formula's accuracy and analyze parameter impacts.

Abstract

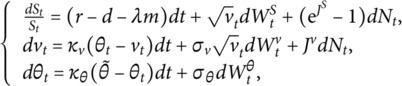

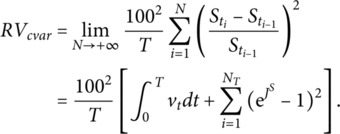

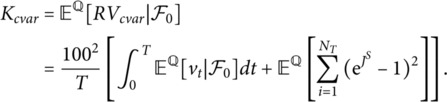

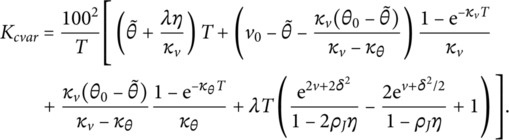

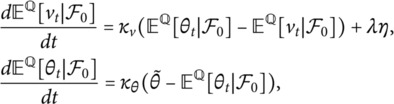

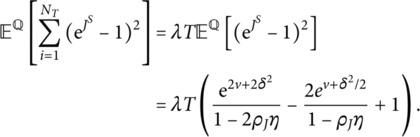

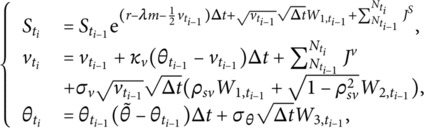

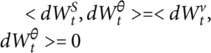

This paper presents the pricing formulas for variance swaps within the Heston model that incorporates jumps and a stochastic long-term mean for the underlying asset. By leveraging the Feynman-Kac theorem, we derive a partial integro-differential equation (PIDE) to obtain the joint moment-generating function for the aforementioned model. Furthermore, we provide a series pricing formula for discretely sampled variance swap, derived through the use of this joint moment-generating function. Additionally, we discuss the limiting properties of the pricing formula for discretely sampled variance swap, namely, the pricing formula for continuously sampled variance swap. Finally, to demonstrate the efficacy of the pricing formula, we conduct several numerical simulation experiments, including comparisons with Monte Carlo (MC) simulation results and an analysis of the impact of parameter…

Genes, proteins, chemicals, diseases, species, mutations and cell lines named across the full text — each resolved to its canonical identifier and authoritative record.

Click any figure to enlarge with its caption.

Figure 1

Figure 1 Figure 2

Figure 2 Figure 3

Figure 3 Figure 4

Figure 4 Figure 5

Figure 5 Figure 6

Figure 6 Figure 7

Figure 7 Figure 8

Figure 8 Figure 9

Figure 9 Figure 10

Figure 10 Figure 11

Figure 11 Figure 12

Figure 12 Figure 13

Figure 13 Figure 14

Figure 14 Figure 15

Figure 15 Figure 16

Figure 16 Figure 17

Figure 17 Figure 18

Figure 18 Figure 19

Figure 19 Figure 20

Figure 20 Figure 21

Figure 21 Figure 22

Figure 22 Figure 23

Figure 23 Figure 24

Figure 24 Figure 25

Figure 25 Figure 26

Figure 26 Figure 27

Figure 27 Figure 28

Figure 28 Figure 29

Figure 29 Figure 30

Figure 30 Figure 31

Figure 31 Figure 32

Figure 32 Figure 33

Figure 33 Figure 34

Figure 34 Figure 35

Figure 35 Figure 36

Figure 36 Figure 37

Figure 37 Figure 38

Figure 38 Figure 39

Figure 39 Figure 40

Figure 40 Figure 41

Figure 41 Figure 42

Figure 42 Figure 43

Figure 43 Figure 44

Figure 44 Figure 45

Figure 45 Figure 46

Figure 46 Figure 47

Figure 47 Figure 48

Figure 48 Figure 49

Figure 49 Figure 50

Figure 50Peer Reviews

No public reviews on file for this paper yet. If you reviewed it on a platform where reviews are public (OpenReview, ICLR, NeurIPS, ICML), you can paste yours below so the community can read it here.

Videos

No videos yet. Explain this paper in a talk, walkthrough, or lecture? Add one.

Taxonomy

TopicsStochastic processes and financial applications · Financial Risk and Volatility Modeling · Complex Systems and Time Series Analysis