Tail Risk Dynamics under Price-Limited Constraint: A Censored Autoregressive Conditional Fréchet Model

Tao Xu, Lei Shu, Yu Chen

TL;DR

This paper introduces a new model to study extreme financial risks in markets with price limits, showing how ignoring these limits can lead to underestimating risk.

Contribution

A novel censored autoregressive conditional Fréchet model is proposed to analyze tail risk dynamics under price limits.

Findings

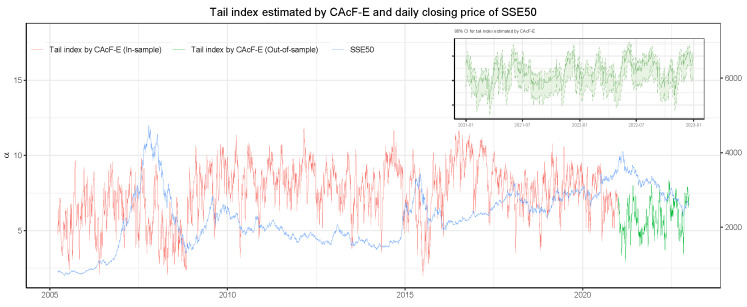

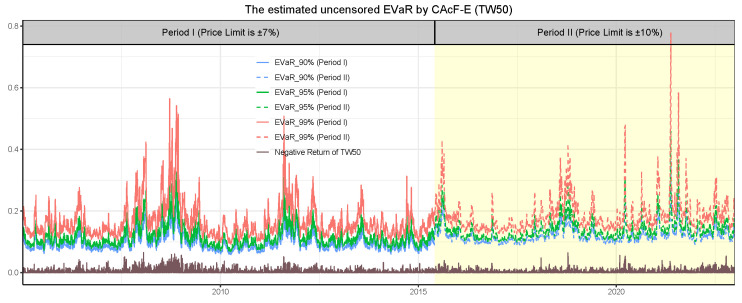

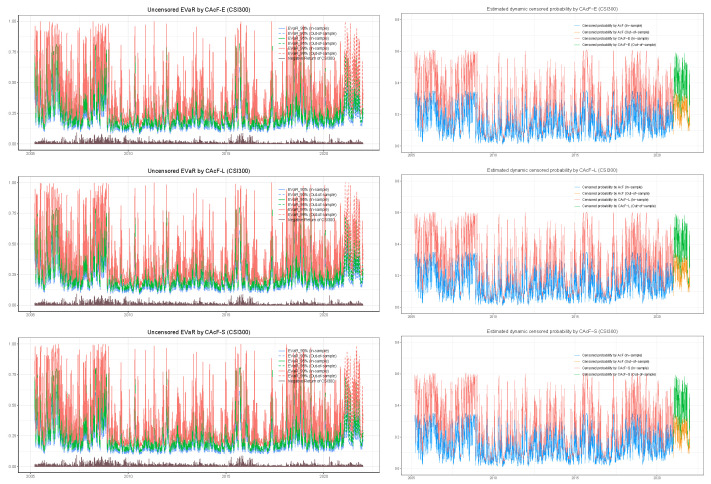

Ignoring price limits leads to serious underestimation of tail risk in constrained markets.

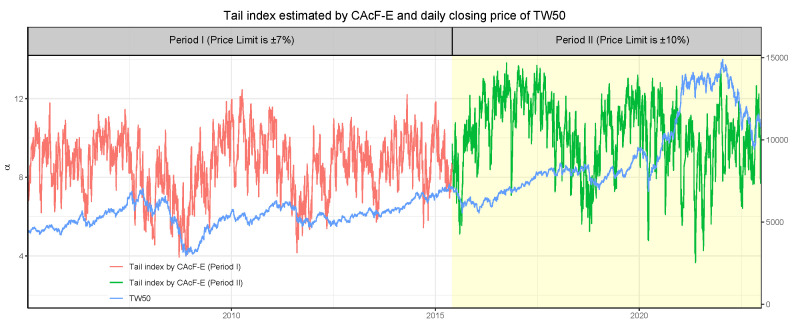

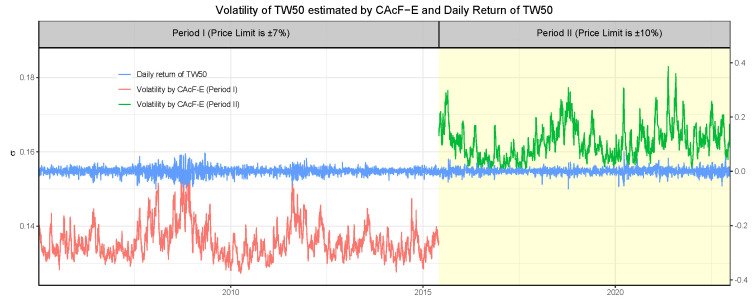

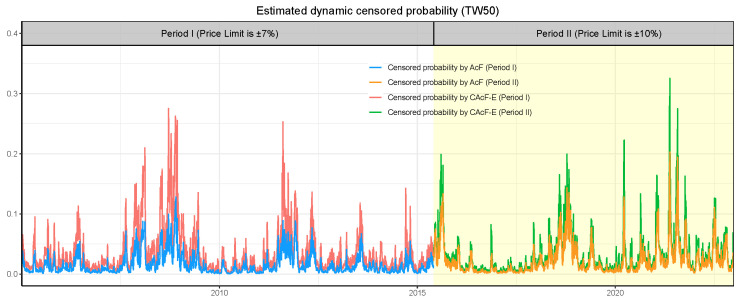

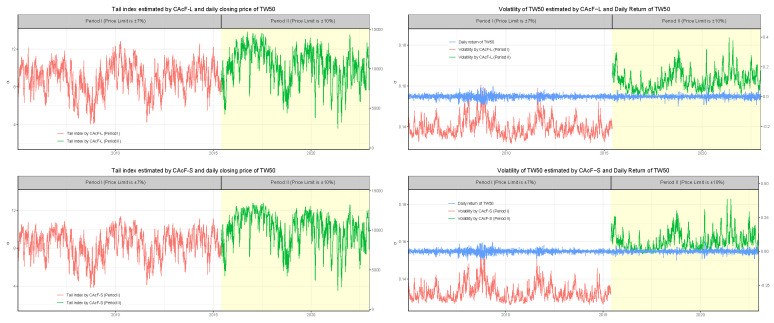

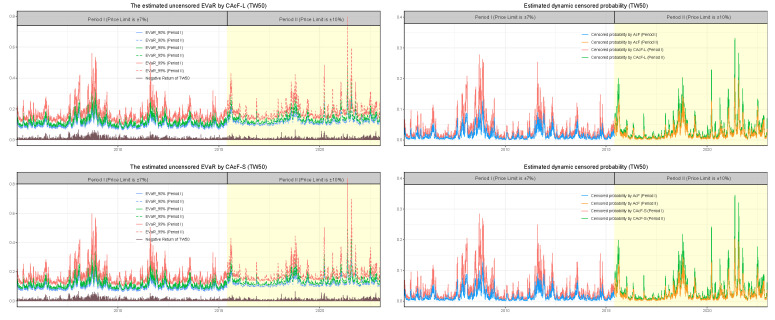

Widening price limits reduces extreme events but increases tail risk in the Chinese Taiwan stock market.

Investors with different risk preferences may make opposing decisions during extreme events.

Abstract

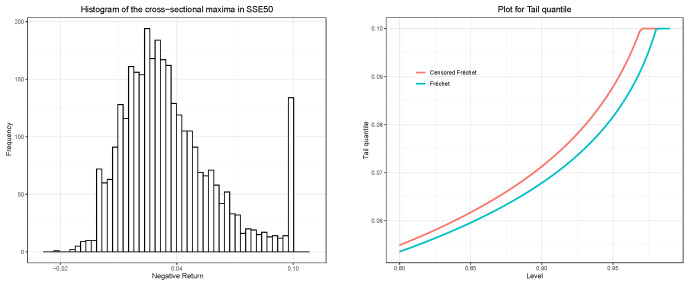

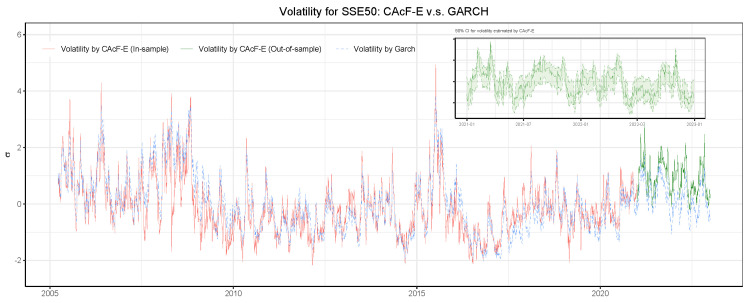

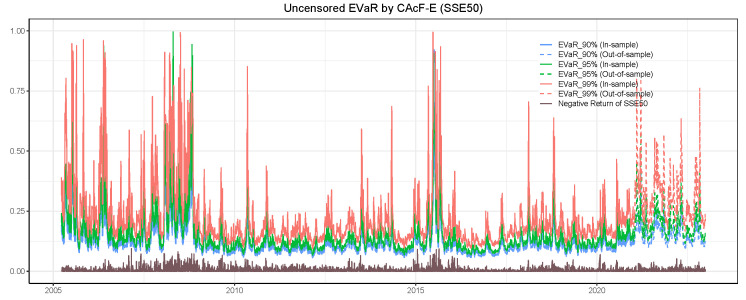

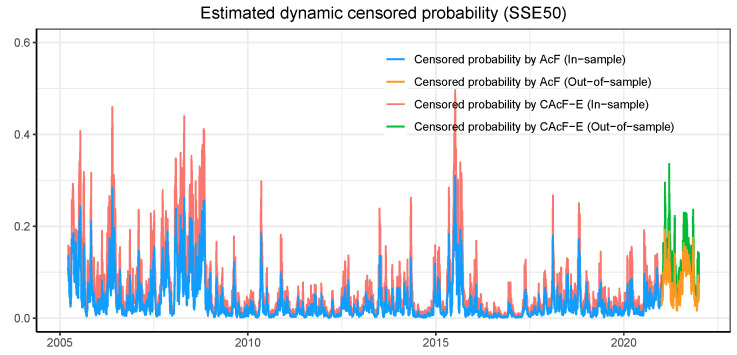

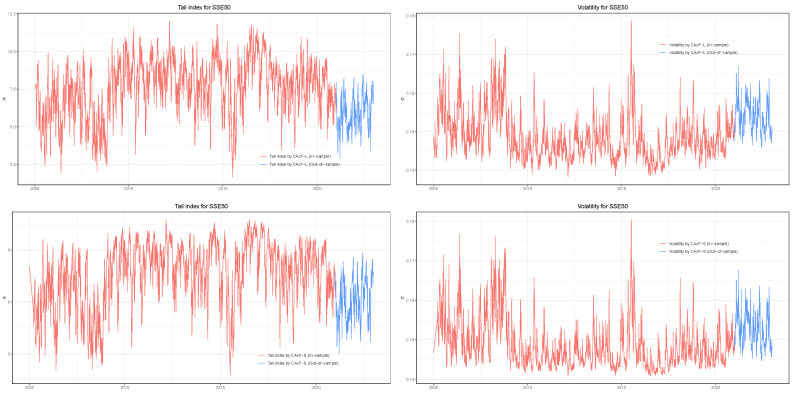

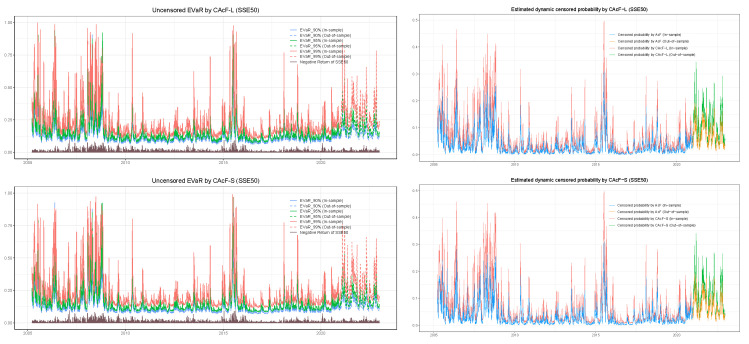

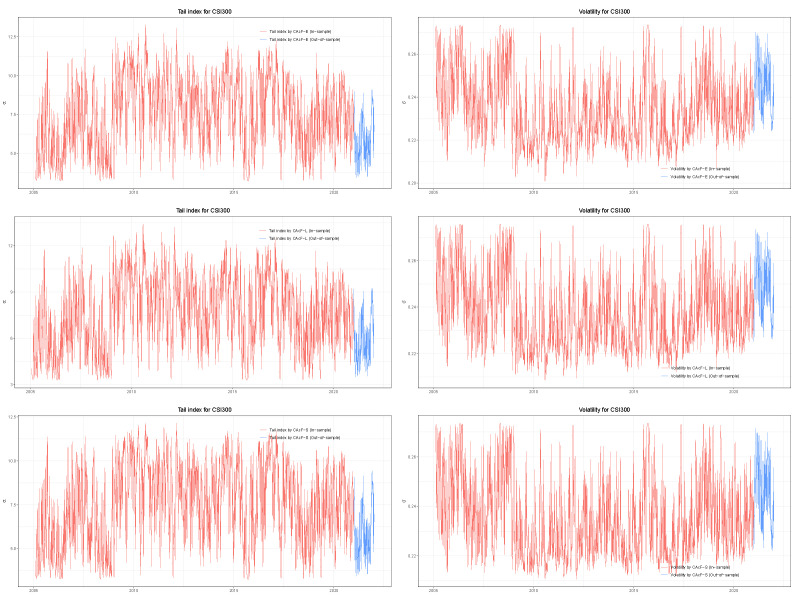

This paper proposes a novel censored autoregressive conditional Fréchet (CAcF) model with a flexible evolution scheme for the time-varying parameters, which allows deciphering tail risk dynamics constrained by price limits from the viewpoints of different risk preferences. The proposed model can well accommodate many important empirical characteristics of financial data, such as heavy-tailedness, volatility clustering, extreme event clustering, and price limits. We then investigate tail risk dynamics via the CAcF model in the price-limited stock markets, taking entropic value at risk (EVaR) as a risk measurement. Our findings suggest that tail risk will be seriously underestimated in price-limited stock markets when the censored property of limit prices is ignored. Additionally, the evidence from the Chinese Taiwan stock market shows that widening price limits would lead to a decrease…

Genes, proteins, chemicals, diseases, species, mutations and cell lines named across the full text — each resolved to its canonical identifier and authoritative record.

Click any figure to enlarge with its caption.

Figure 1

Figure 1 Figure 2

Figure 2 Figure 3

Figure 3 Figure 4

Figure 4 Figure 5

Figure 5 Figure 6

Figure 6 Figure 7

Figure 7 Figure 8

Figure 8 Figure 9

Figure 9 Figure 10

Figure 10 Figure 11

Figure 11 Figure 12

Figure 12 Figure 13

Figure 13 Figure 14

Figure 14 Figure 15

Figure 15Peer Reviews

No public reviews on file for this paper yet. If you reviewed it on a platform where reviews are public (OpenReview, ICLR, NeurIPS, ICML), you can paste yours below so the community can read it here.

Videos

No videos yet. Explain this paper in a talk, walkthrough, or lecture? Add one.

Taxonomy

TopicsFinancial Risk and Volatility Modeling · Market Dynamics and Volatility · Complex Systems and Time Series Analysis