Share pledge and accounting conservatism in share-pledging firms: Evidence from a natural experiment in China

Xin Wang, Yue Sun, Yanlin Li, Cuijiao Zhang

TL;DR

This study shows that when Chinese laws restricted share pledging, firms with pledged shares became more conservative in their financial reporting to avoid risks and satisfy creditors.

Contribution

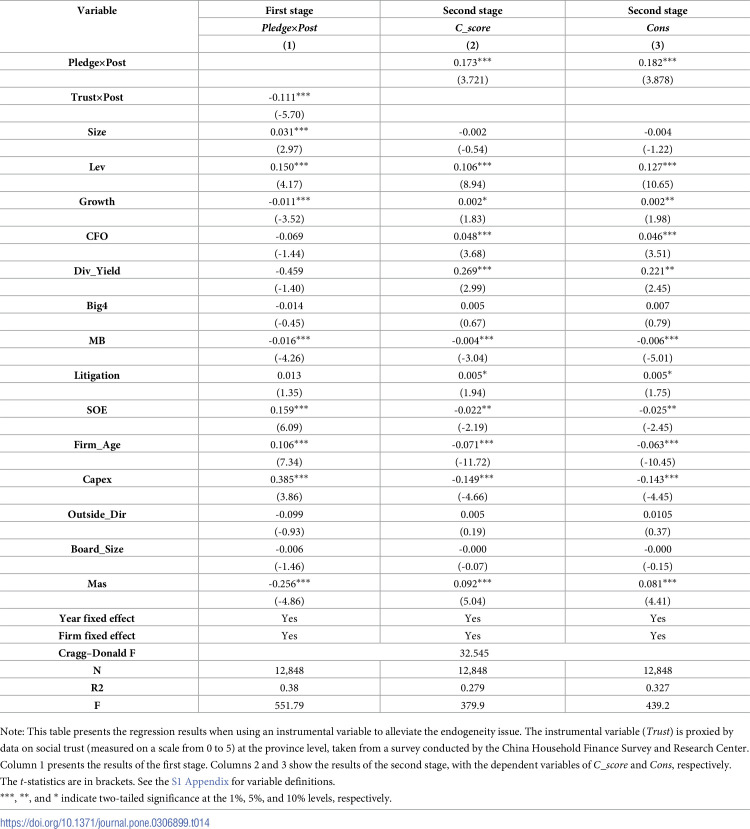

The paper provides direct evidence of creditors' demand for accounting conservatism in response to legal changes in share pledging.

Findings

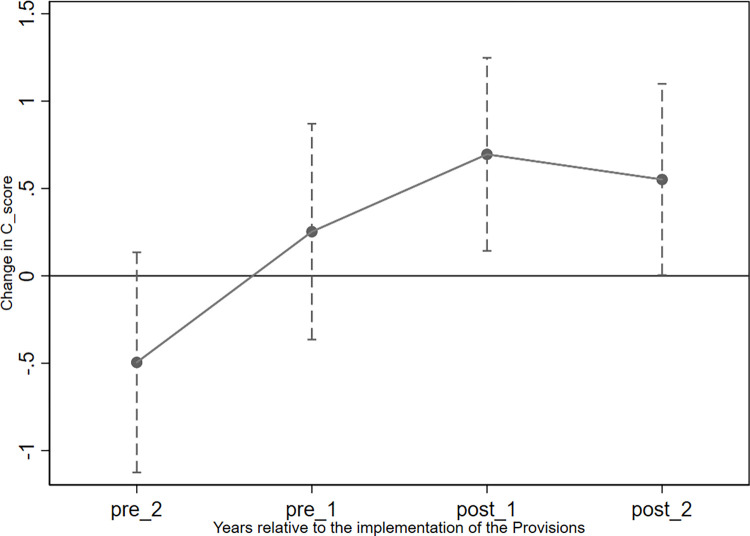

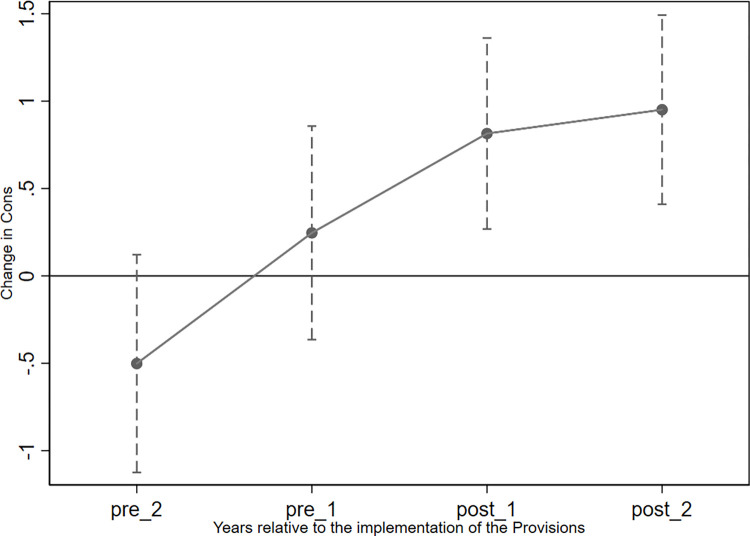

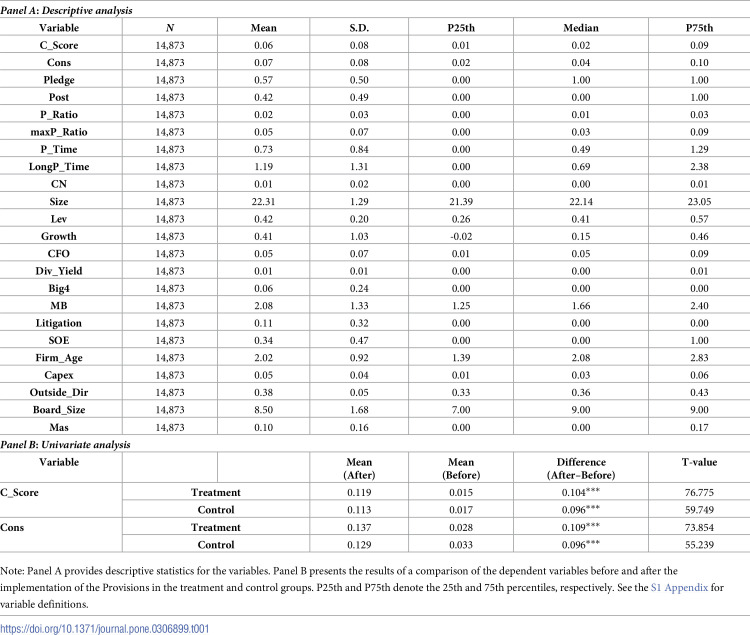

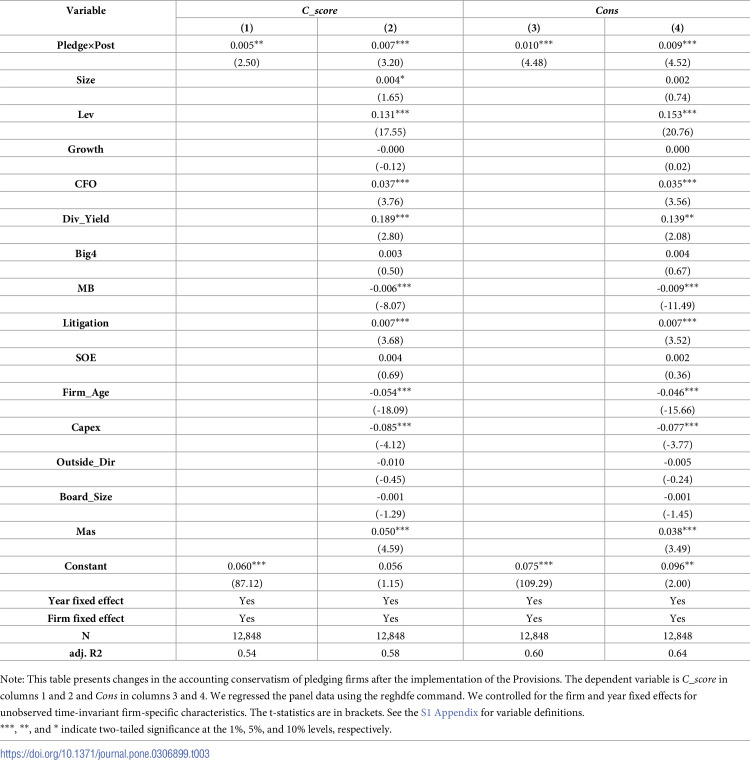

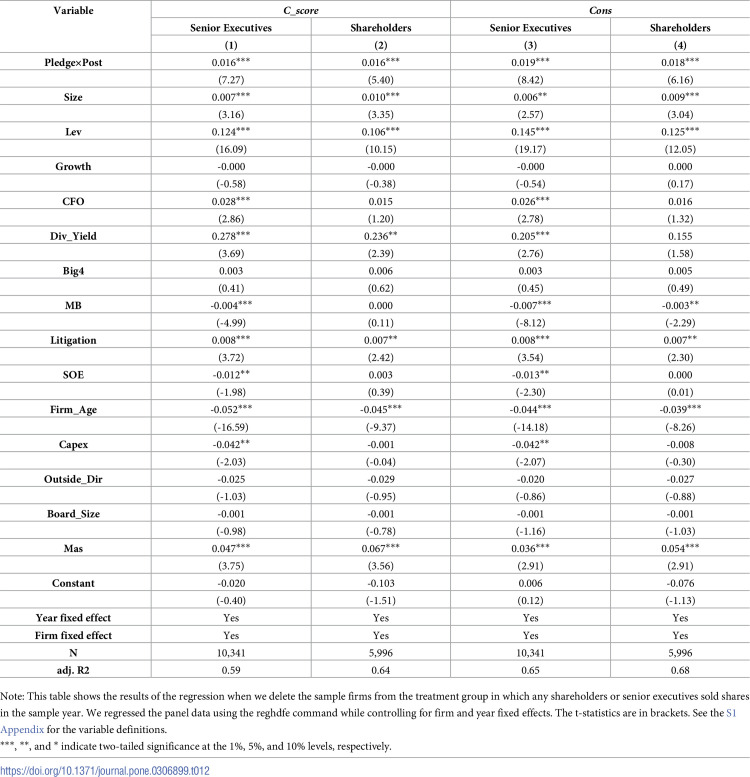

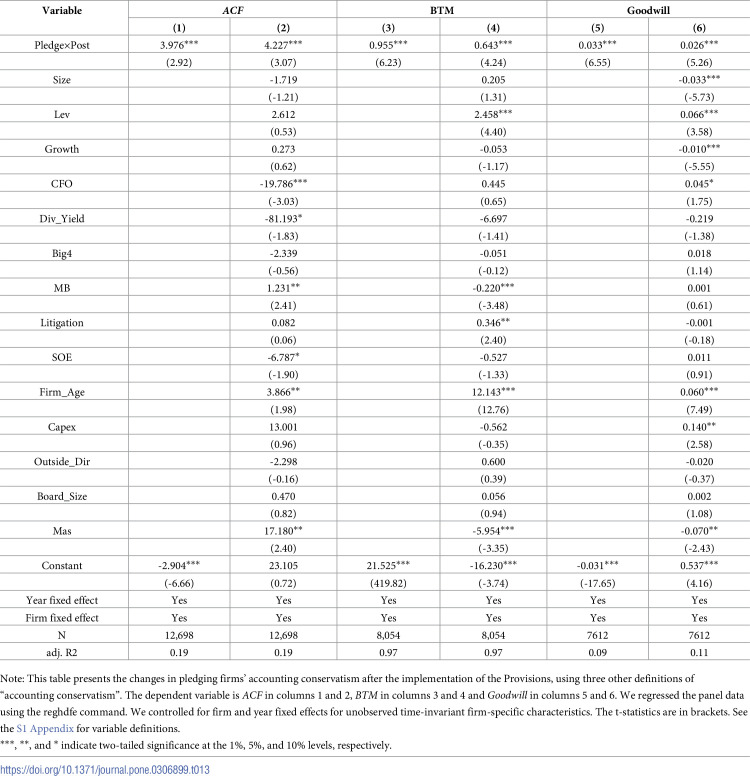

Pledging firms showed increased accounting conservatism after legal restrictions were introduced.

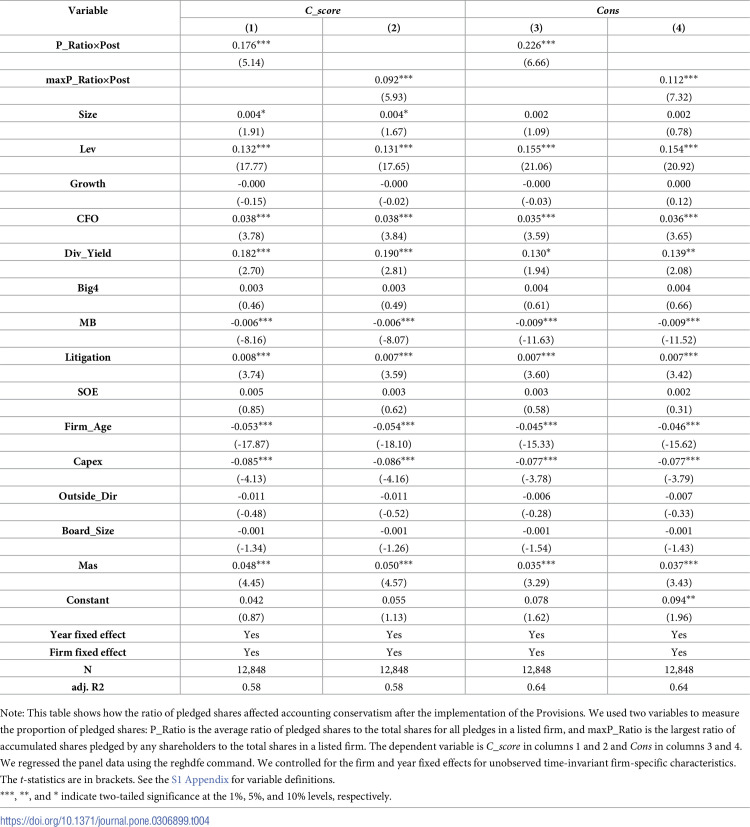

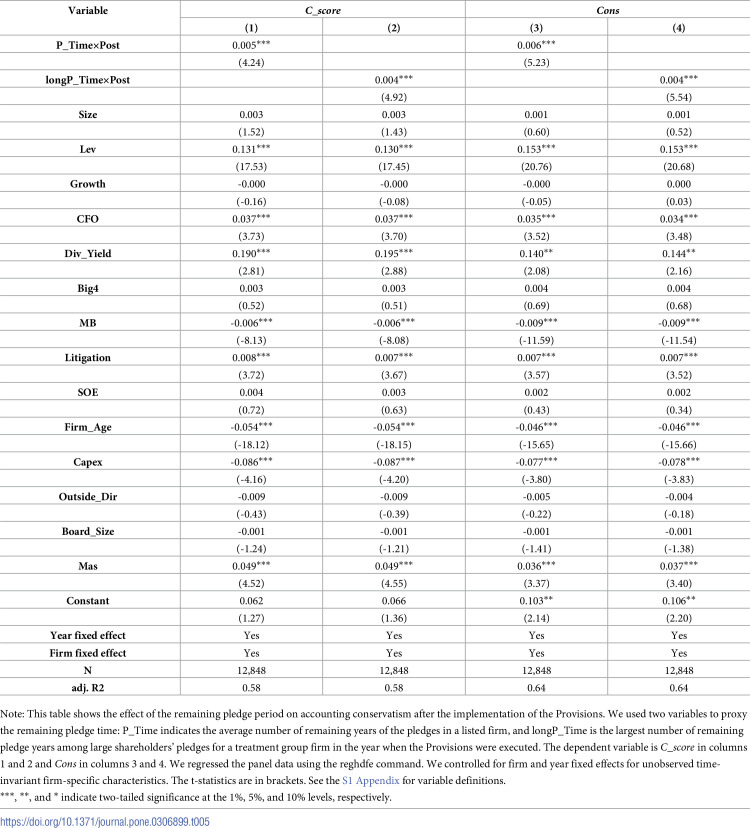

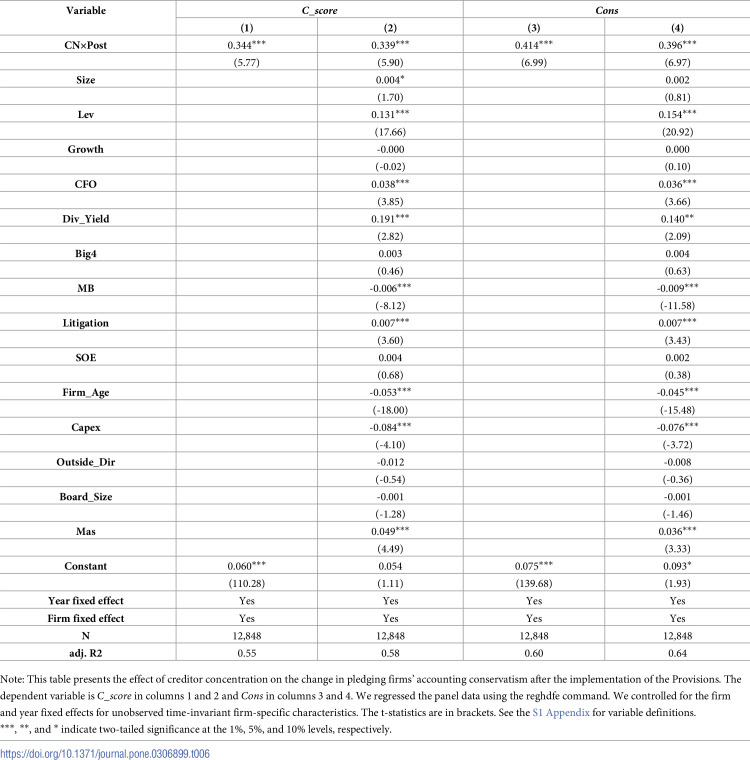

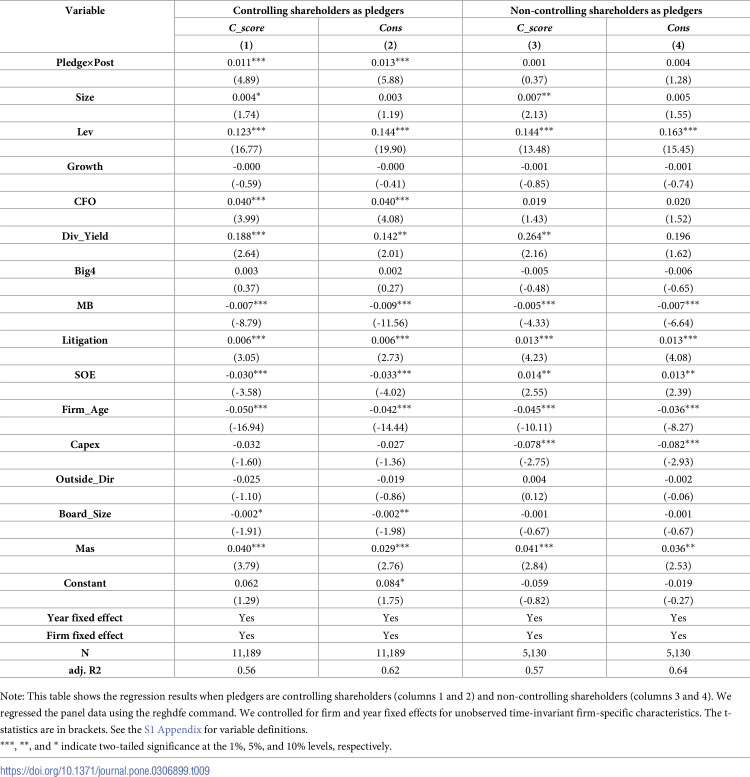

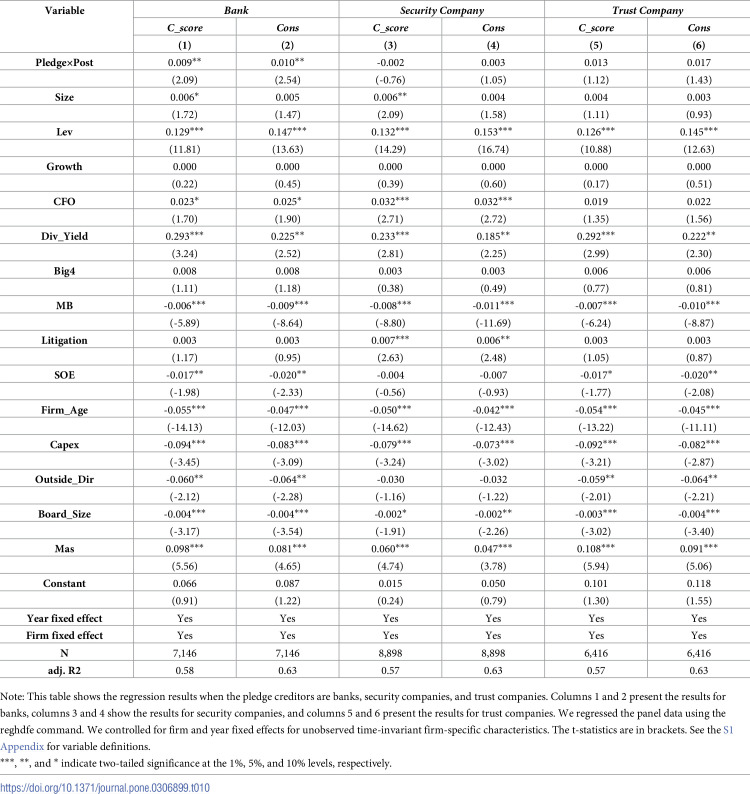

The effect was stronger in firms with higher share pledging ratios and concentrated creditors.

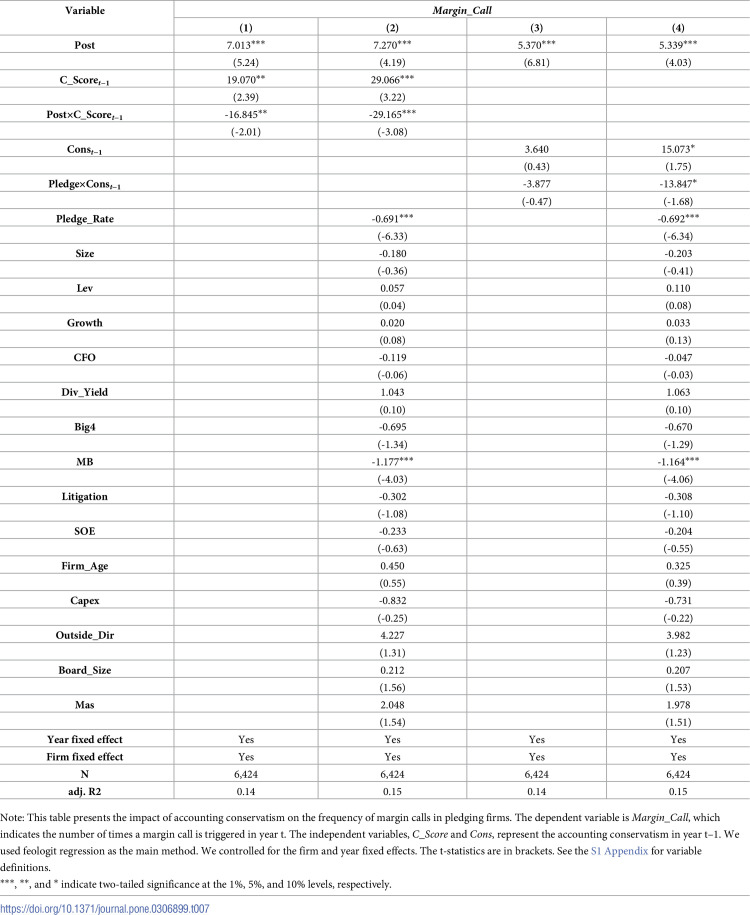

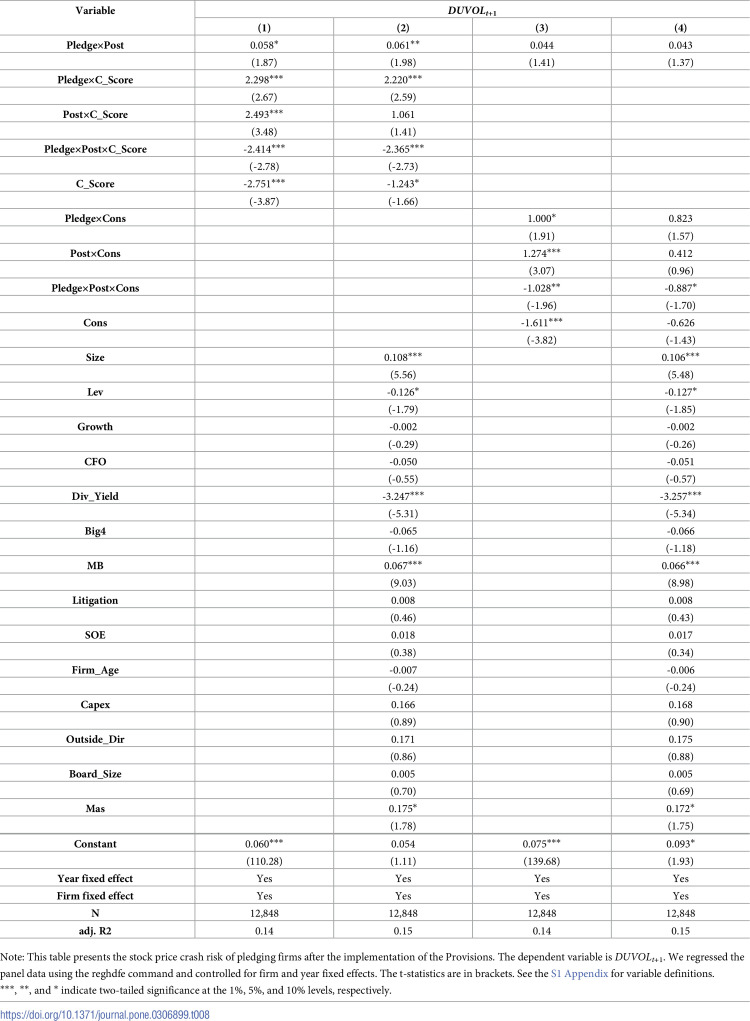

Conservatism reduced the risk of margin calls and stock price crashes.

Abstract

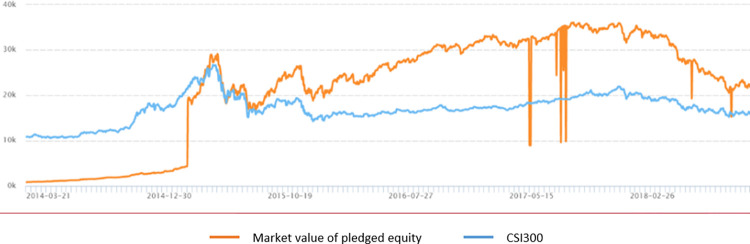

This paper focuses on firms in which insiders pledge their shares as collateral for loans. By investigating a natural experiment—China’s enactment of provisions on share reductions that restrict pledge creditors’ cashing-out behavior—we find that pledging firms exhibited more conservative financial reporting after the implementation than non-pledging firms. This effect was pronounced in firms with a higher ratio of pledged shares, a longer maturation period of the pledged shares, and more concentrated pledge creditors. Additionally, we show that pledging firms increased their accounting conservatism after the shock, leading to a lower risk of margin calls and stock price crashes. The effect on accounting conservatism was stronger in firms with controlling pledgers or when the pledge creditors were banks. Our results remained consistent after we performed several robustness tests. These…

Genes, proteins, chemicals, diseases, species, mutations and cell lines named across the full text — each resolved to its canonical identifier and authoritative record.

Click any figure to enlarge with its caption.

Figure 1

Figure 1 Figure 2

Figure 2 Figure 3

Figure 3 Figure 4

Figure 4 Figure 5

Figure 5 Figure 6

Figure 6 Figure 7

Figure 7 Figure 8

Figure 8 Figure 9

Figure 9 Figure 10

Figure 10 Figure 11

Figure 11 Figure 12

Figure 12 Figure 13

Figure 13 Figure 14

Figure 14 Figure 15

Figure 15 Figure 16

Figure 16 Figure 17

Figure 17 Figure 18

Figure 18 Figure 19

Figure 19 Figure 20

Figure 20 Figure 21

Figure 21 Figure 22

Figure 22 Figure 23

Figure 23 Figure 24

Figure 24Peer Reviews

No public reviews on file for this paper yet. If you reviewed it on a platform where reviews are public (OpenReview, ICLR, NeurIPS, ICML), you can paste yours below so the community can read it here.

Videos

No videos yet. Explain this paper in a talk, walkthrough, or lecture? Add one.

Taxonomy

TopicsAuditing, Earnings Management, Governance · Corporate Finance and Governance · Banking stability, regulation, efficiency