Employee education, labor protection intensity and auditor risk perception

Xiaotian Shen, Anni Wu, Yi Ding, Qian Sun, Mengge Liu, Rana Muhammad Ammar Zahid, Rana Muhammad Ammar Zahid, Rana Muhammad Ammar Zahid, Rana Muhammad Ammar Zahid

TL;DR

This study shows that highly educated employees can lower audit fees, but labor protection laws reduce this effect, especially in less marketized and less Confucian regions.

Contribution

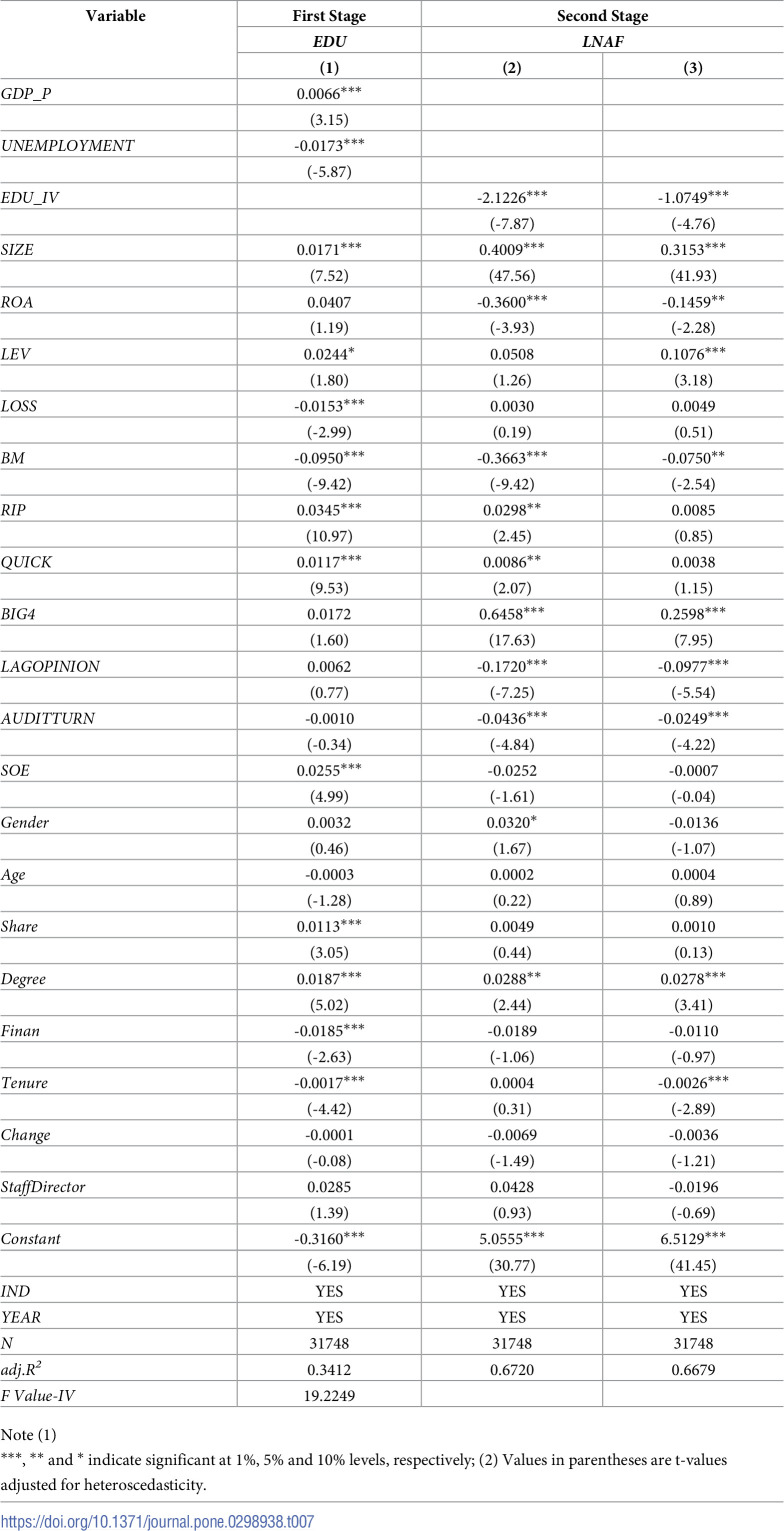

The paper introduces employee education as a new factor influencing auditor risk perception and audit fees in Chinese companies.

Findings

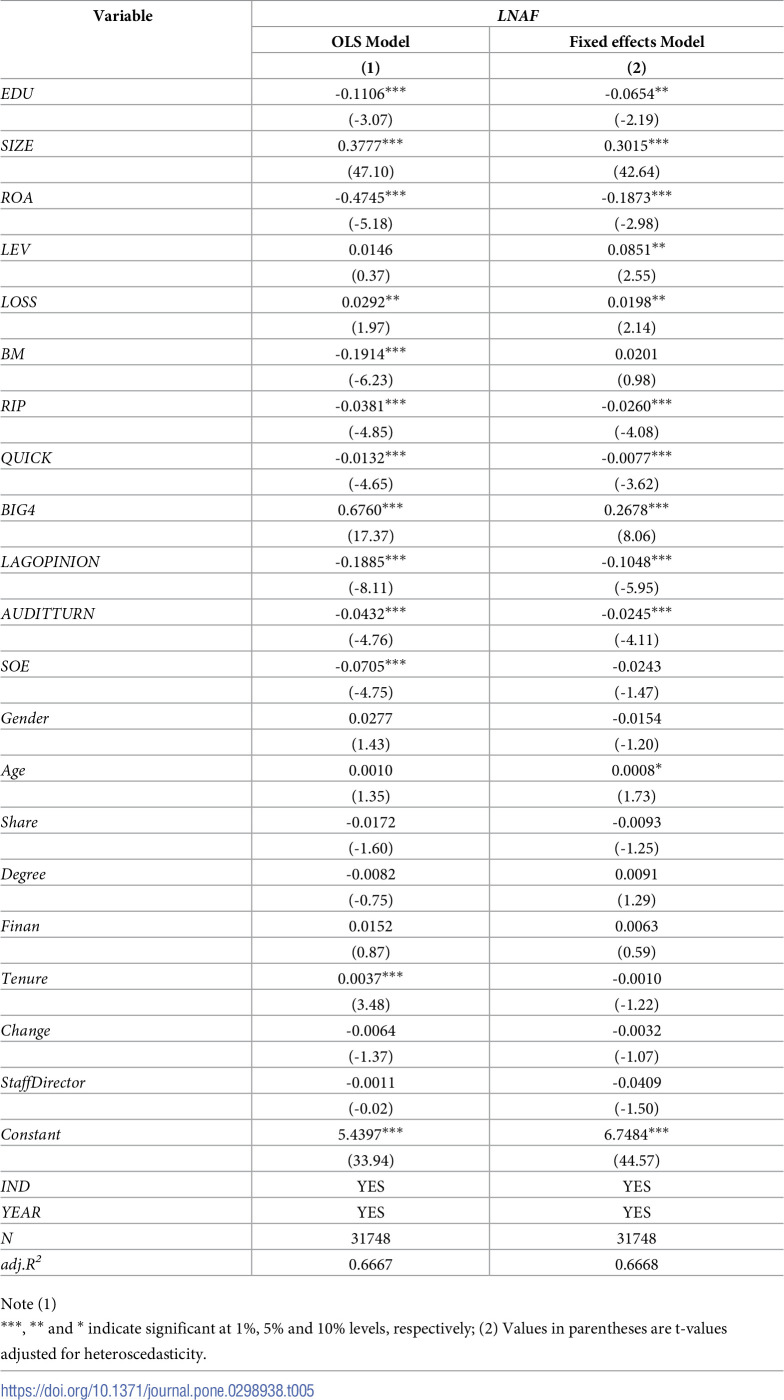

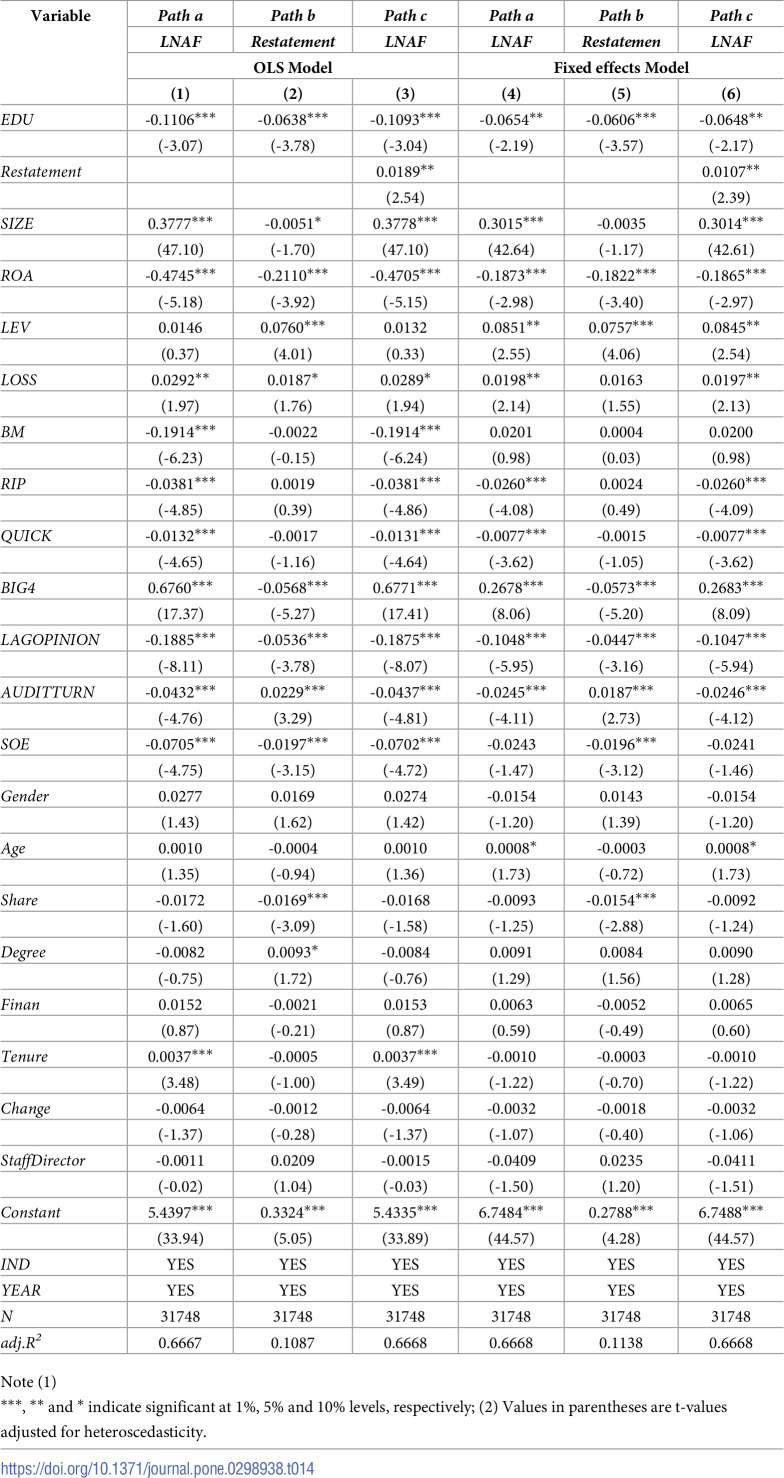

Highly educated employees are associated with lower audit fees.

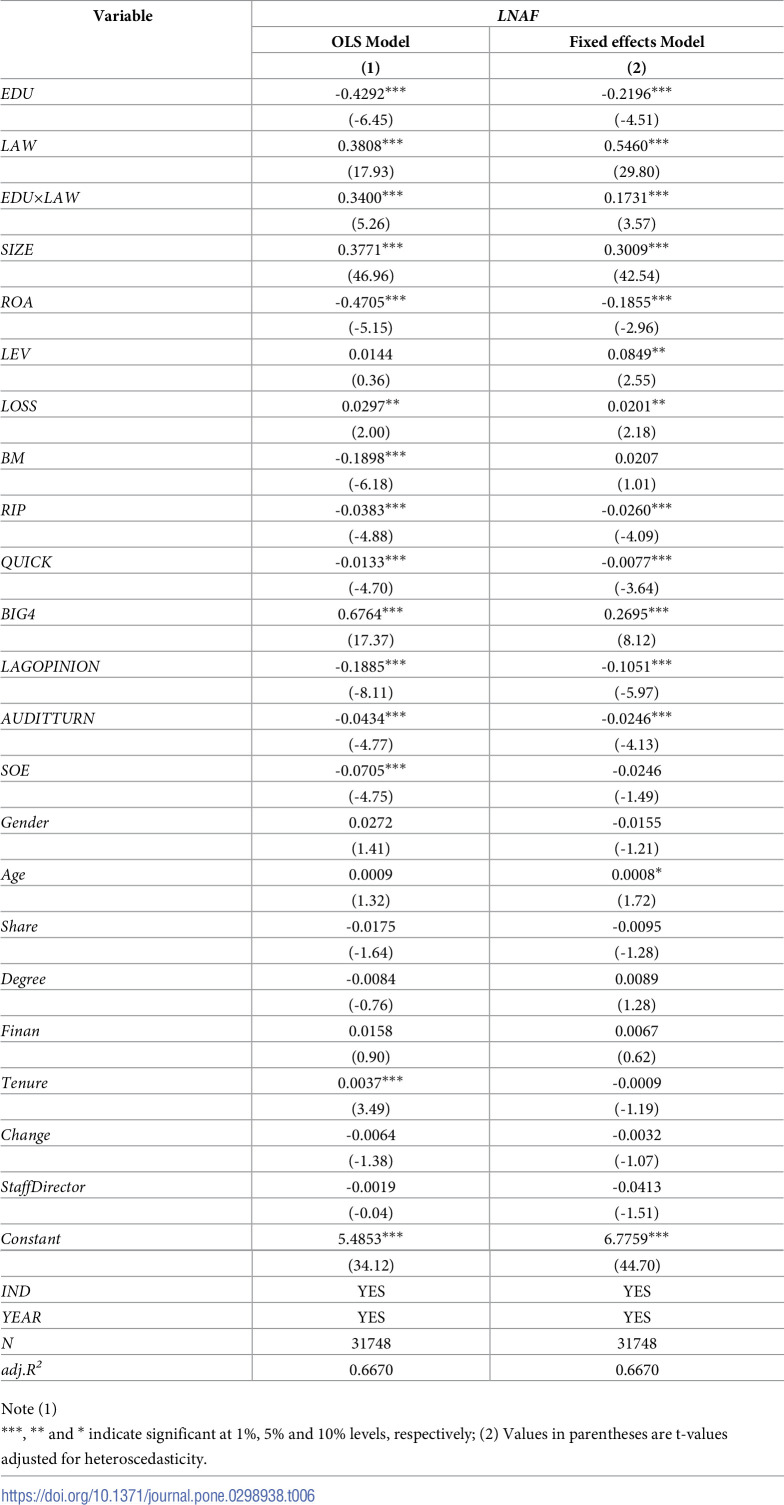

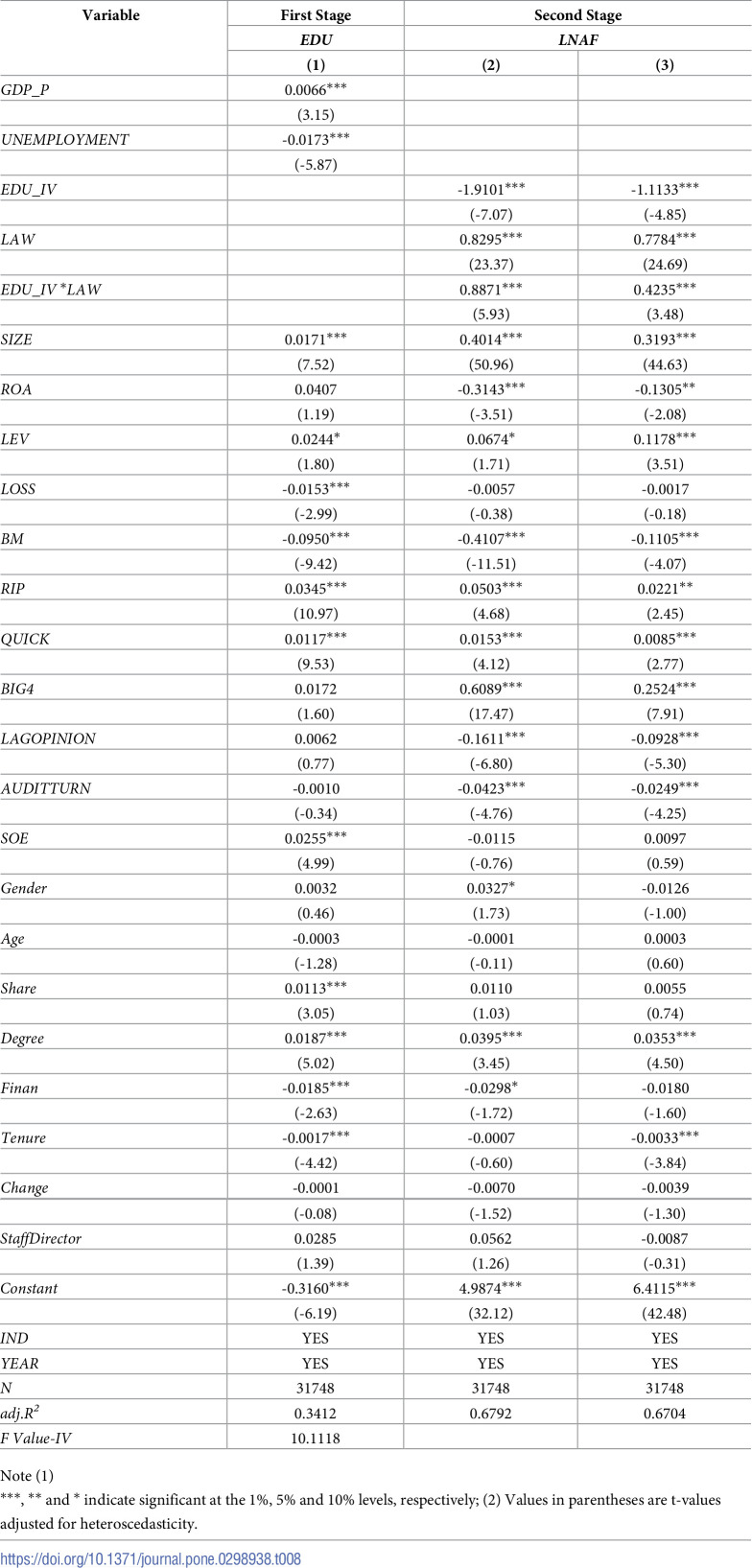

The Labor Protection Law weakens the effect of employee education on audit fees.

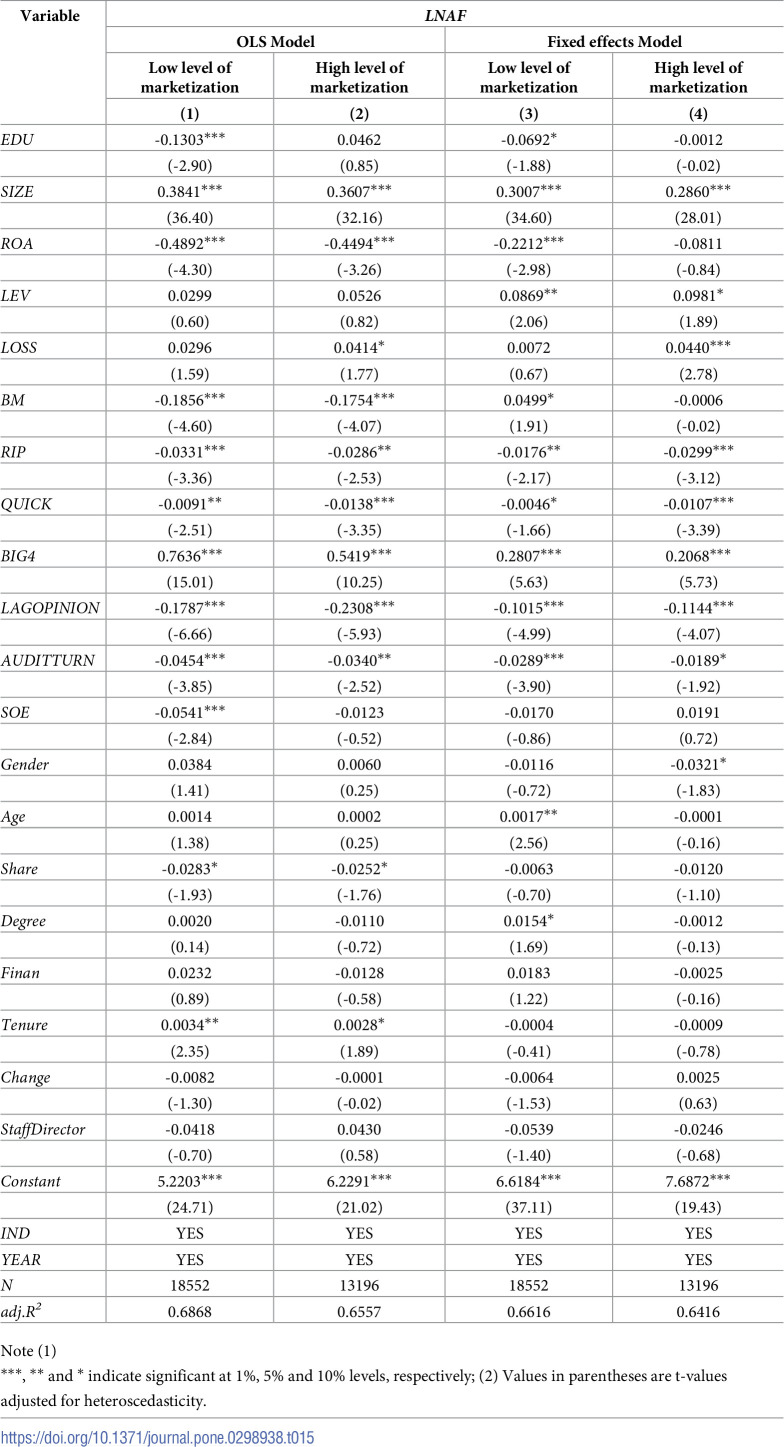

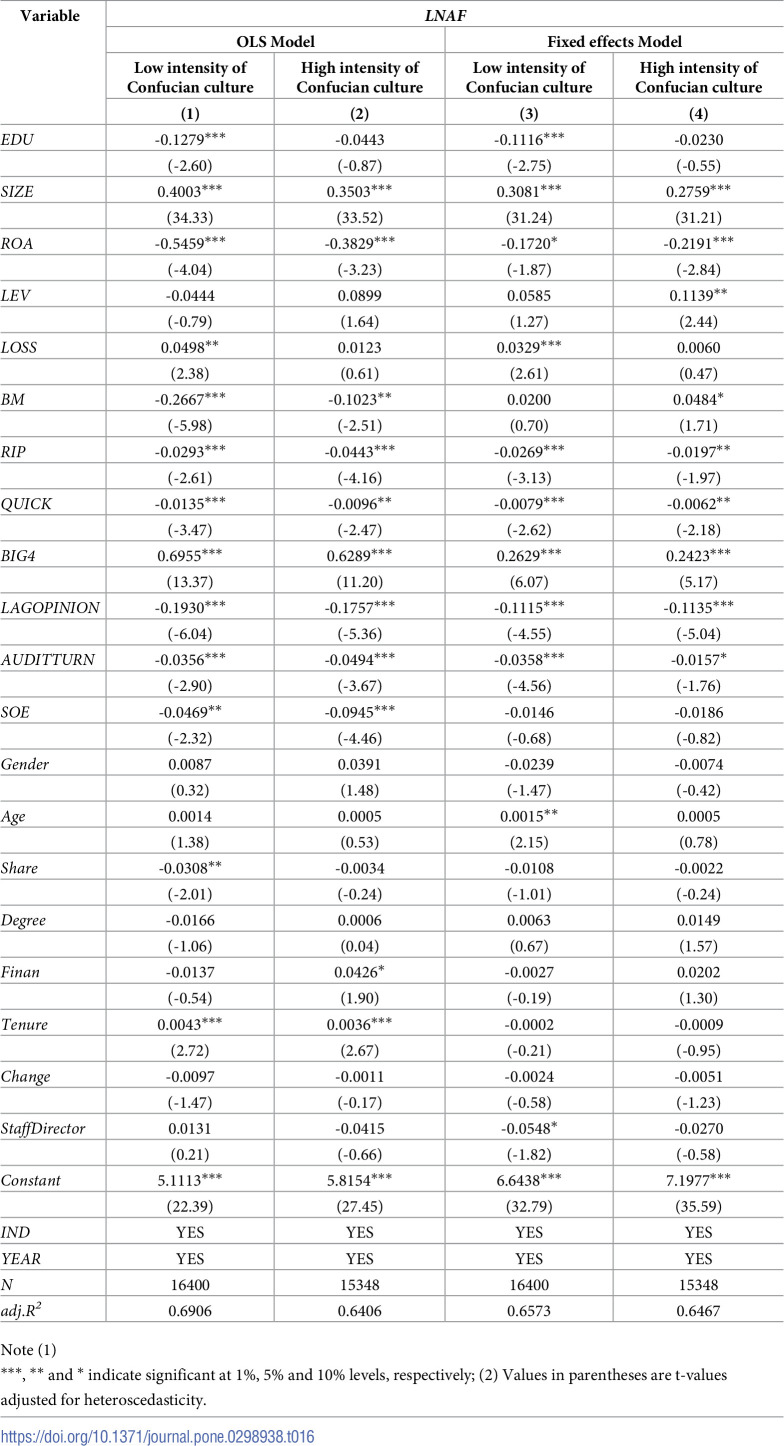

Employee education has a stronger impact in regions with low marketization and weak Confucian culture.

Abstract

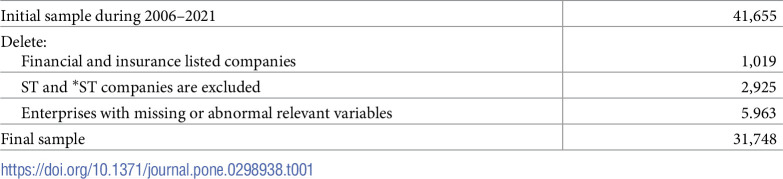

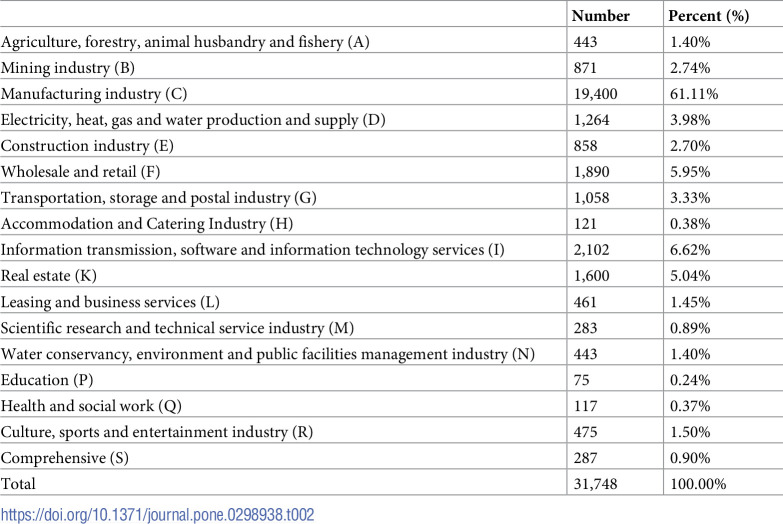

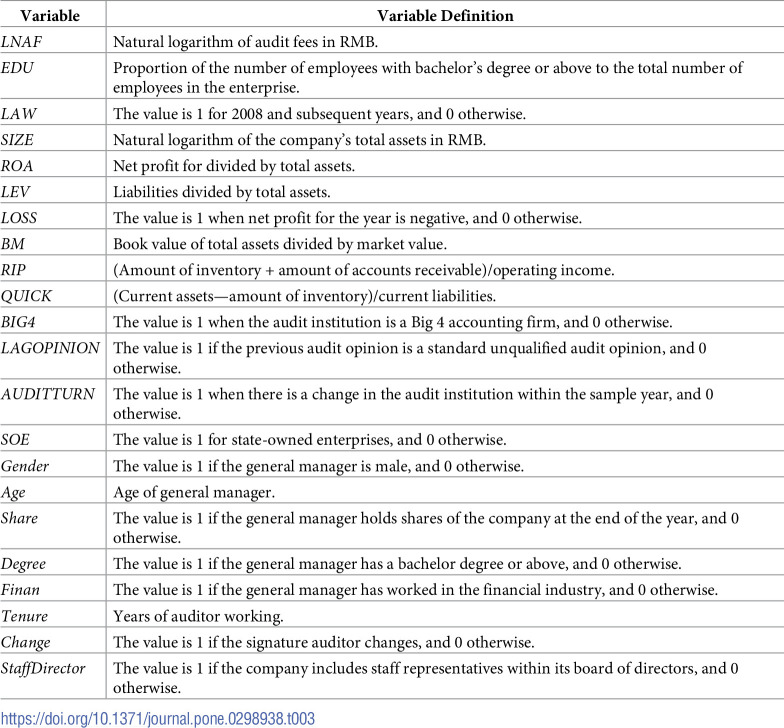

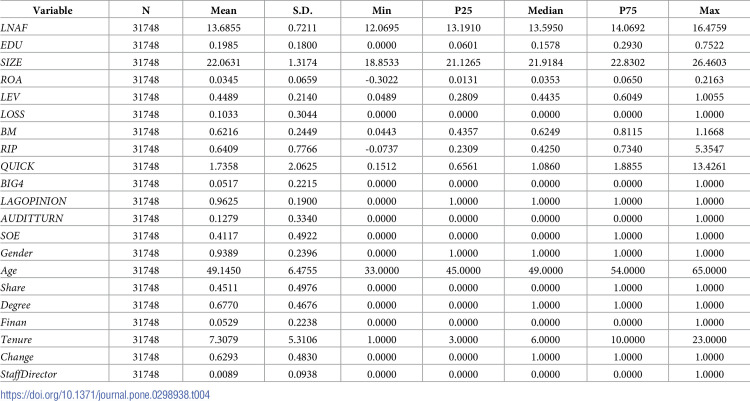

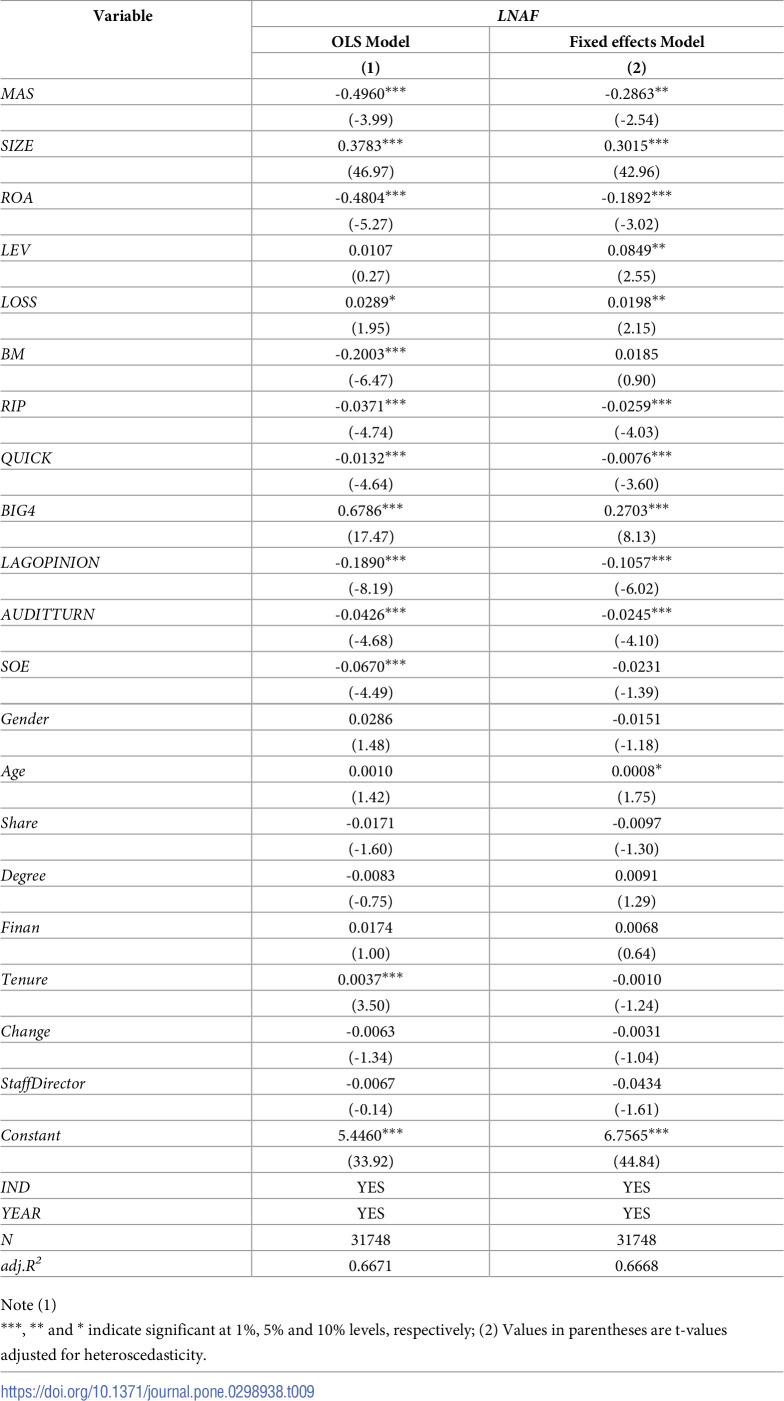

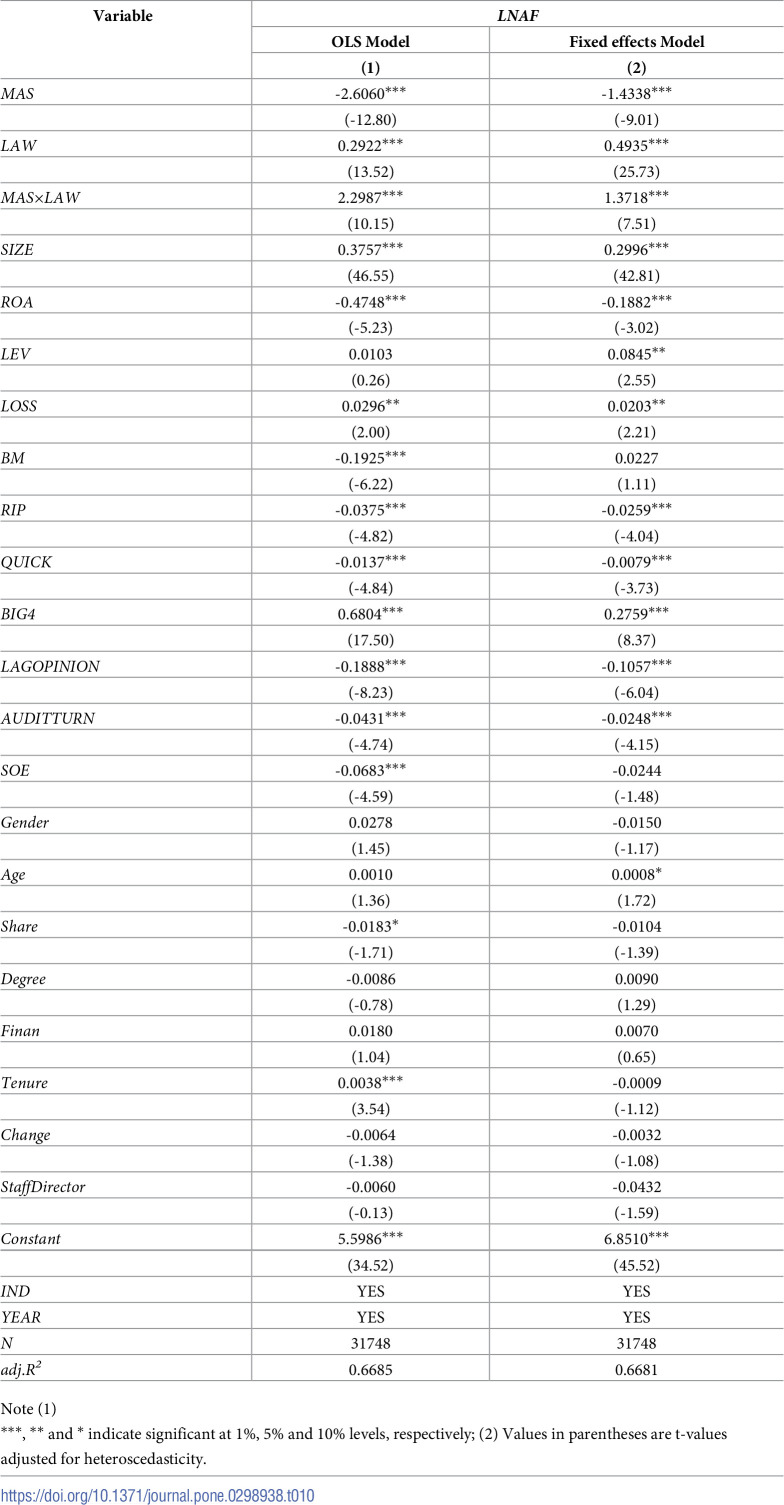

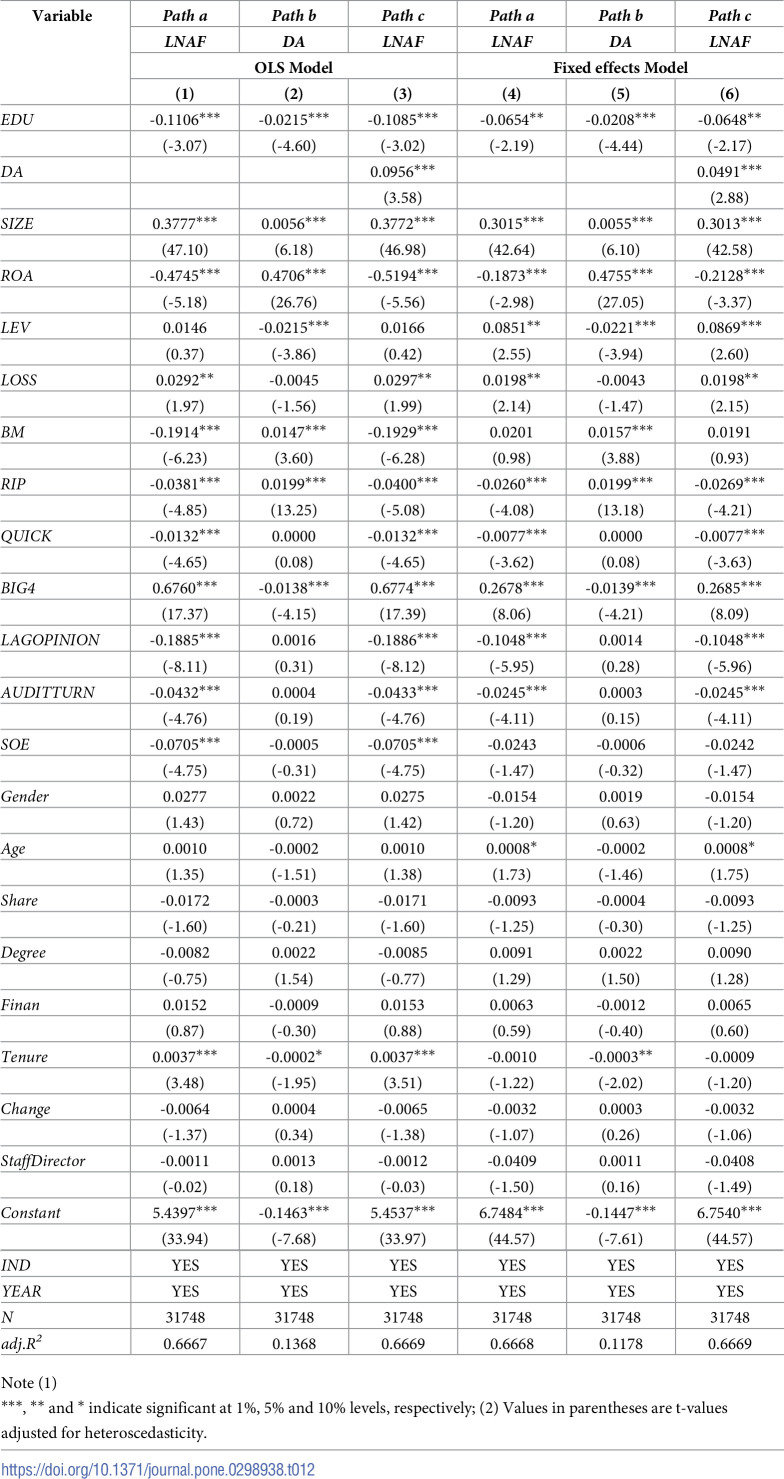

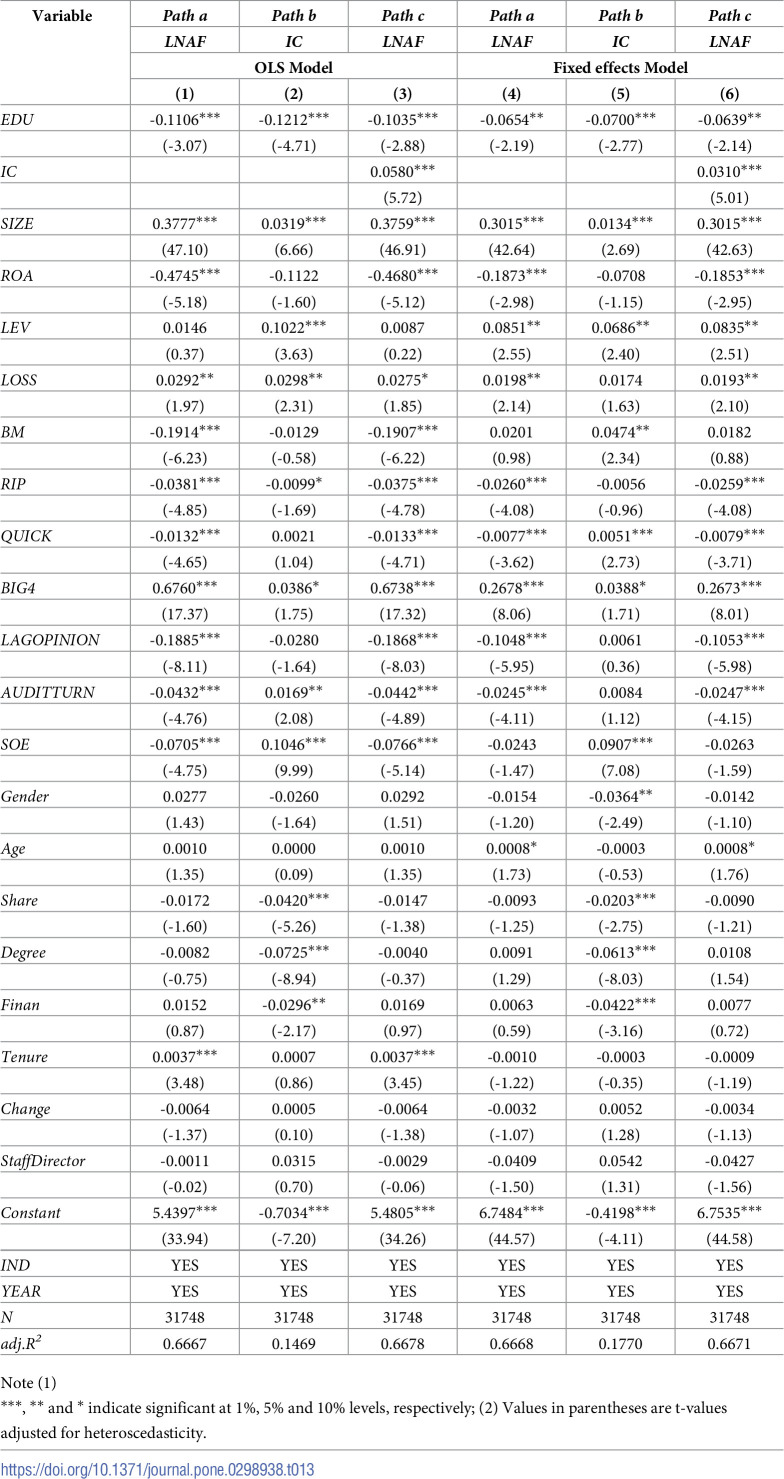

Prior literature finds senior executives can influence auditor decision making. However, few studies have discussed the impact of employee’s personal characteristics. Our research aims to fill the above research gaps by examining the impact of employee level education on audit costs. Taking A-share listed companies in Shanghai and Shenzhen from 2006 to 2021 as the research object, this paper examines the impact of employee education on audit fees. It is found that highly educated employees can effectively reduce the audit fees borne by the company, but the implementation of the Labor Protection Law weakens this inhibitory effect. In the case of low marketization level and weak Confucian culture intensity, employee education level has a more significant inhibitory effect on audit fees of listed companies. This study provides a basis for empirical research on the impact of employee…

Genes, proteins, chemicals, diseases, species, mutations and cell lines named across the full text — each resolved to its canonical identifier and authoritative record.

Click any figure to enlarge with its caption.

Figure 1

Figure 1 Figure 2

Figure 2 Figure 3

Figure 3 Figure 4

Figure 4 Figure 5

Figure 5 Figure 6

Figure 6 Figure 7

Figure 7 Figure 8

Figure 8 Figure 9

Figure 9 Figure 10

Figure 10 Figure 11

Figure 11 Figure 12

Figure 12 Figure 13

Figure 13 Figure 14

Figure 14 Figure 15

Figure 15 Figure 16

Figure 16 Figure 17

Figure 17 Figure 18

Figure 18 Figure 19

Figure 19 Figure 20

Figure 20 Figure 21

Figure 21 Figure 22

Figure 22 Figure 23

Figure 23 Figure 24

Figure 24 Figure 25

Figure 25 Figure 26

Figure 26 Figure 27

Figure 27Peer Reviews

No public reviews on file for this paper yet. If you reviewed it on a platform where reviews are public (OpenReview, ICLR, NeurIPS, ICML), you can paste yours below so the community can read it here.

Videos

No videos yet. Explain this paper in a talk, walkthrough, or lecture? Add one.

Taxonomy

TopicsAuditing, Earnings Management, Governance · Corporate Finance and Governance · Corporate Social Responsibility Reporting