Multivariate Modeling of Natural Gas Spot Trading Hubs Incorporating Futures Market Realized Volatility

Michael Weylandt, Yu Han, Katherine B. Ensor

TL;DR

This paper introduces a joint modeling approach using high-frequency data and Bayesian estimation to improve volatility prediction and risk management in LNG spot markets, especially for less liquid hubs.

Contribution

It develops a novel multivariate model that leverages liquid hub data to enhance volatility estimates for illiquid hubs, with robust Bayesian estimation techniques.

Findings

Model outperforms traditional methods in predictive accuracy.

Effective in markets with sparse and irregular data.

Applicable to other commodities with similar data patterns.

Abstract

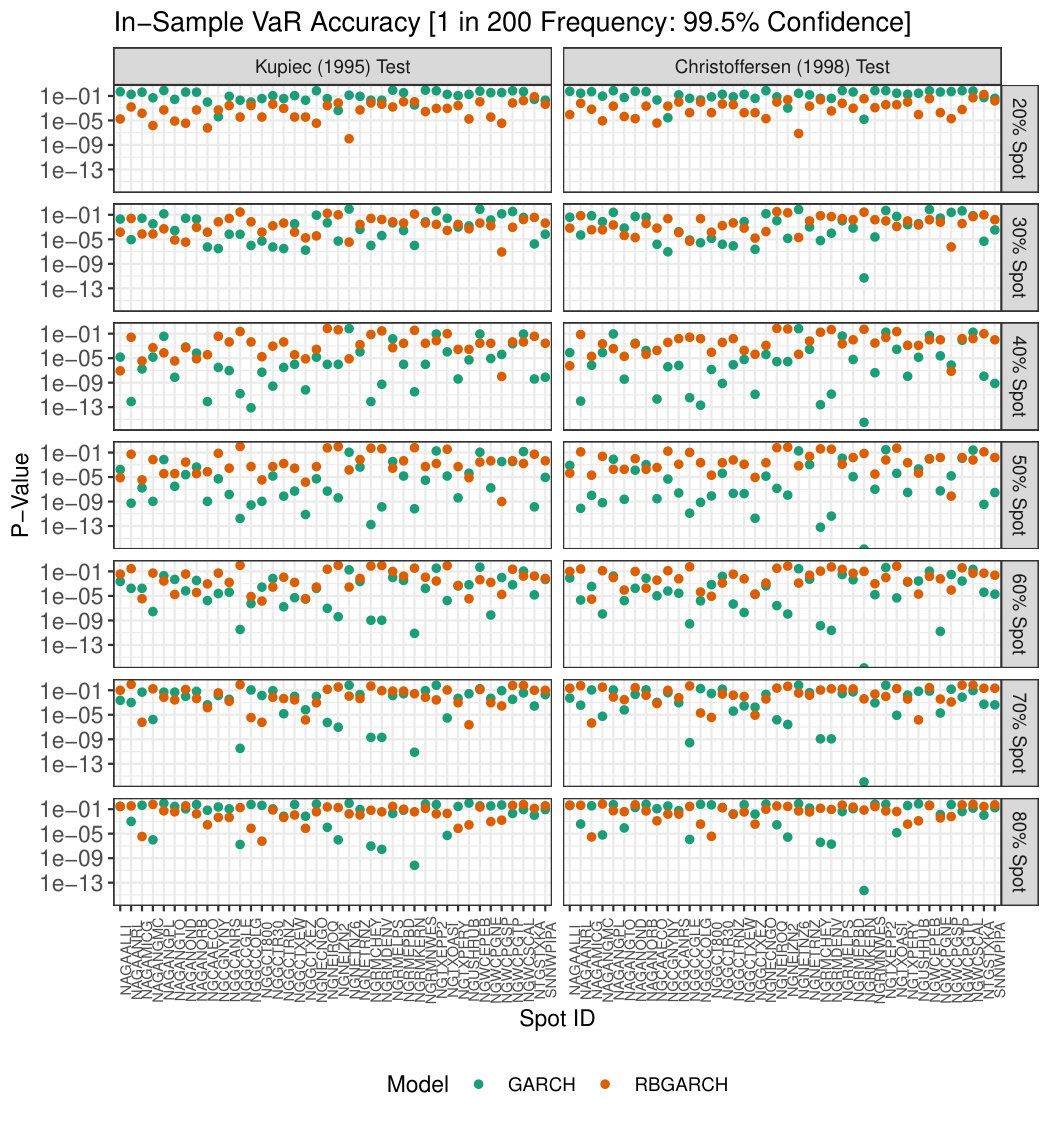

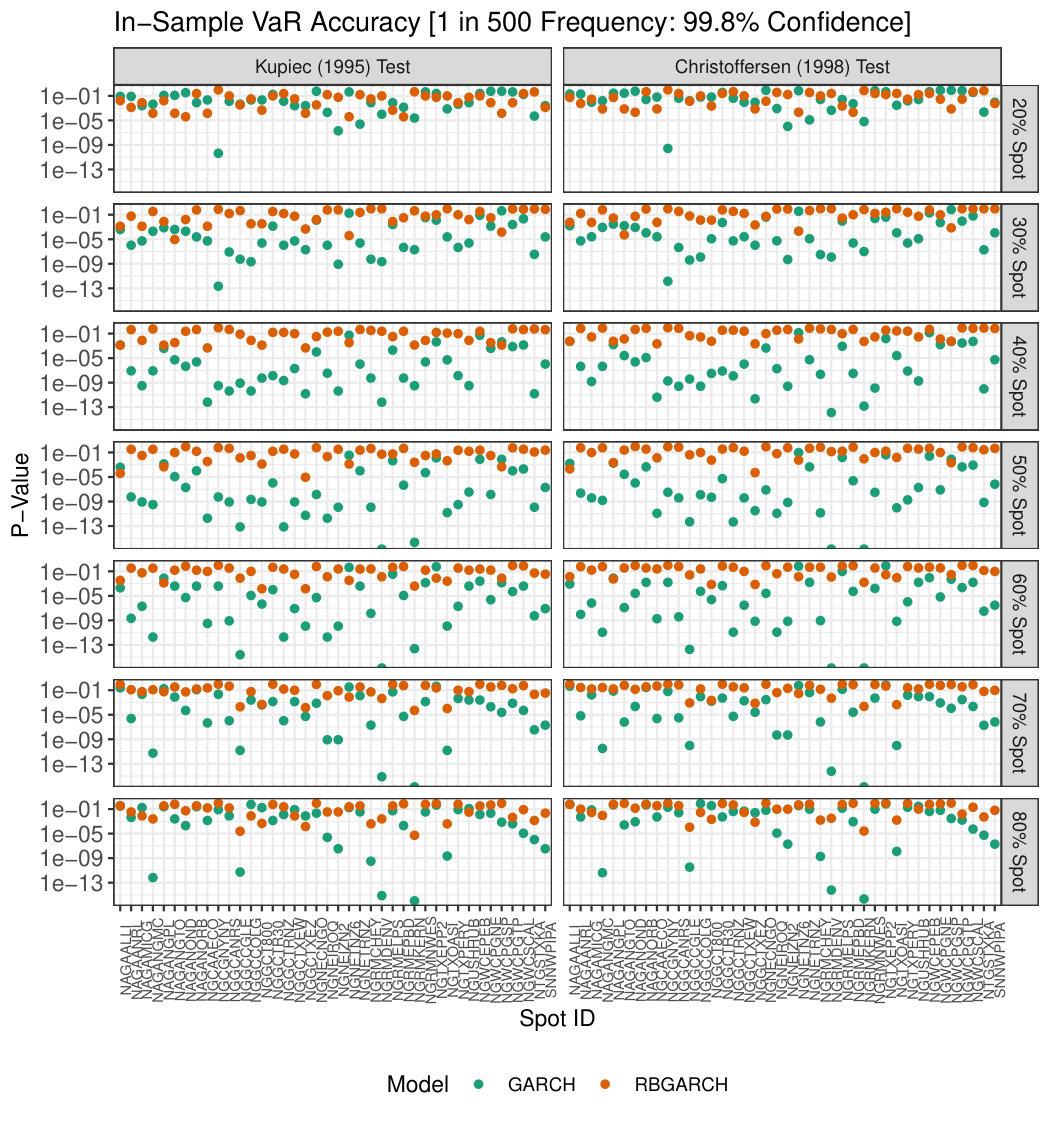

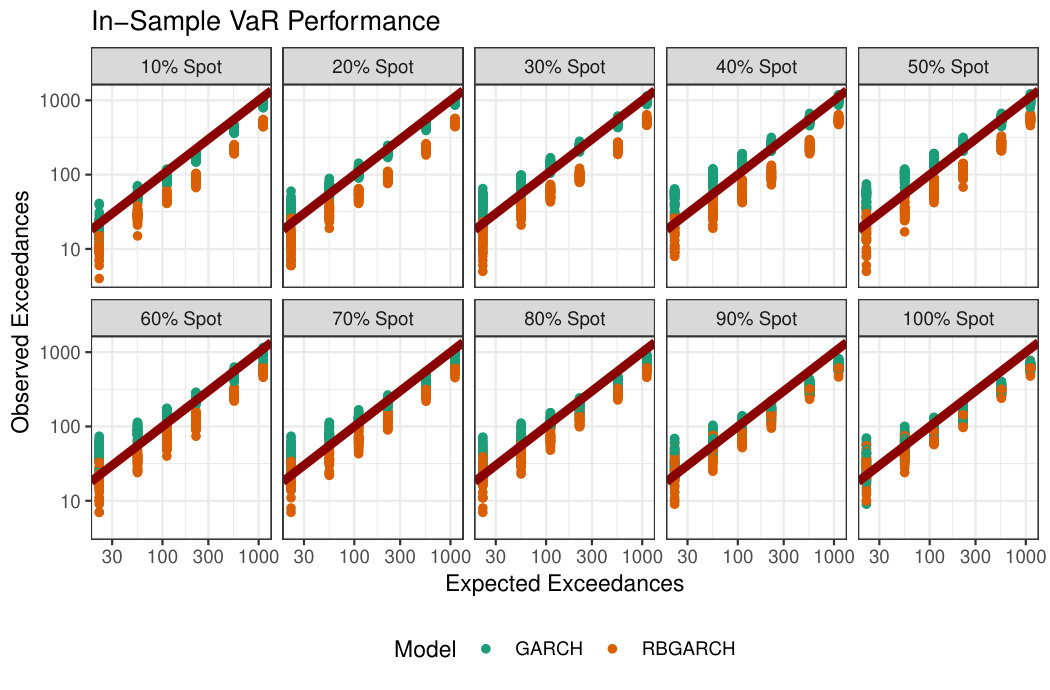

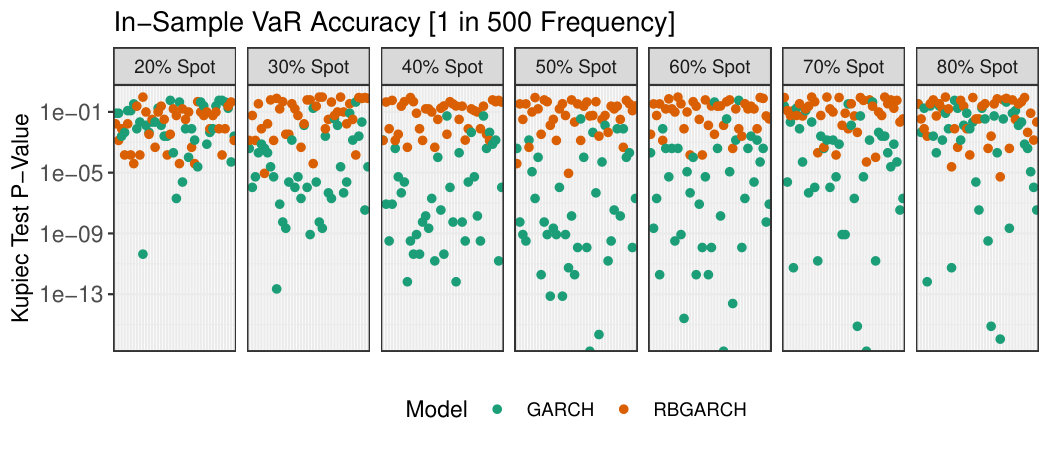

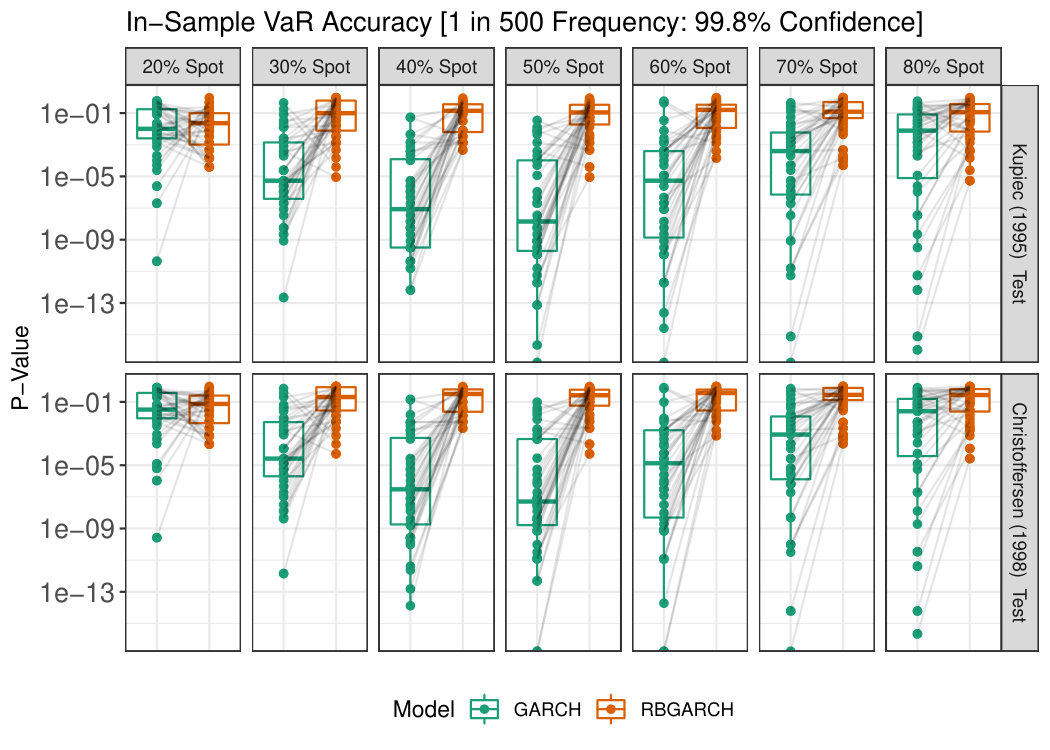

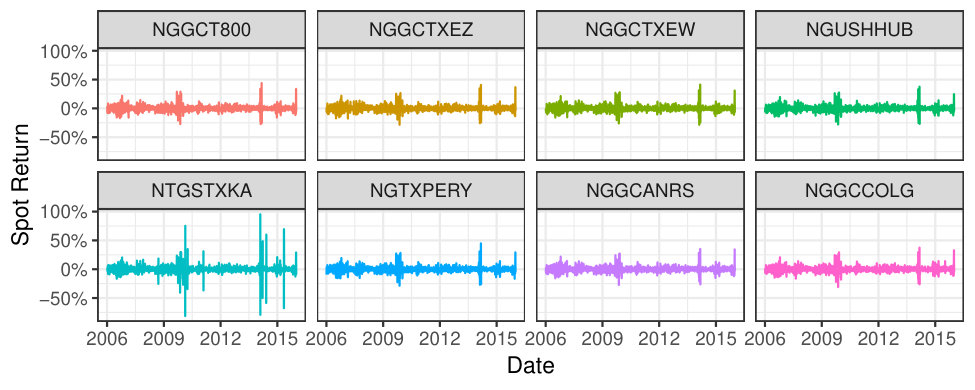

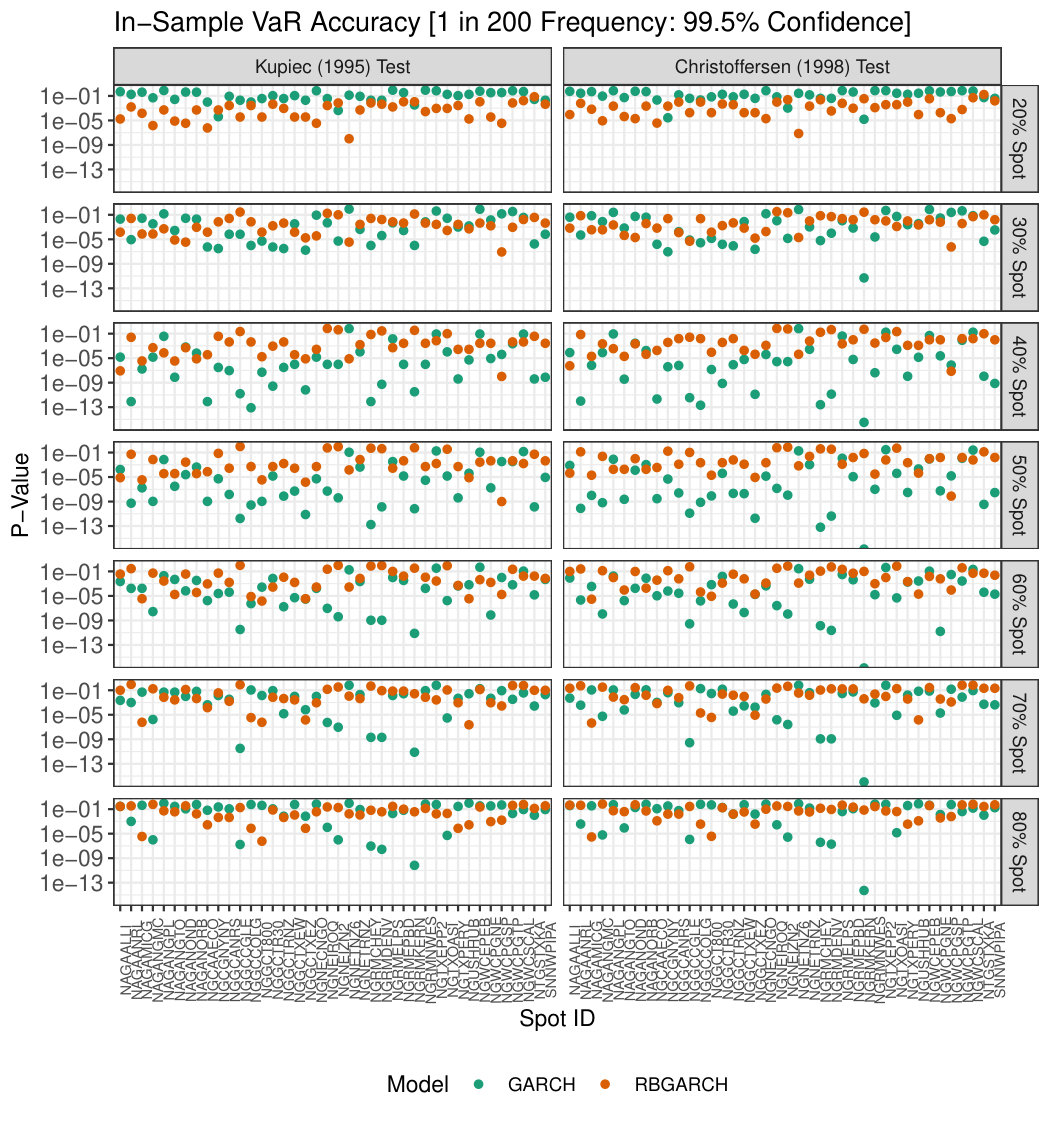

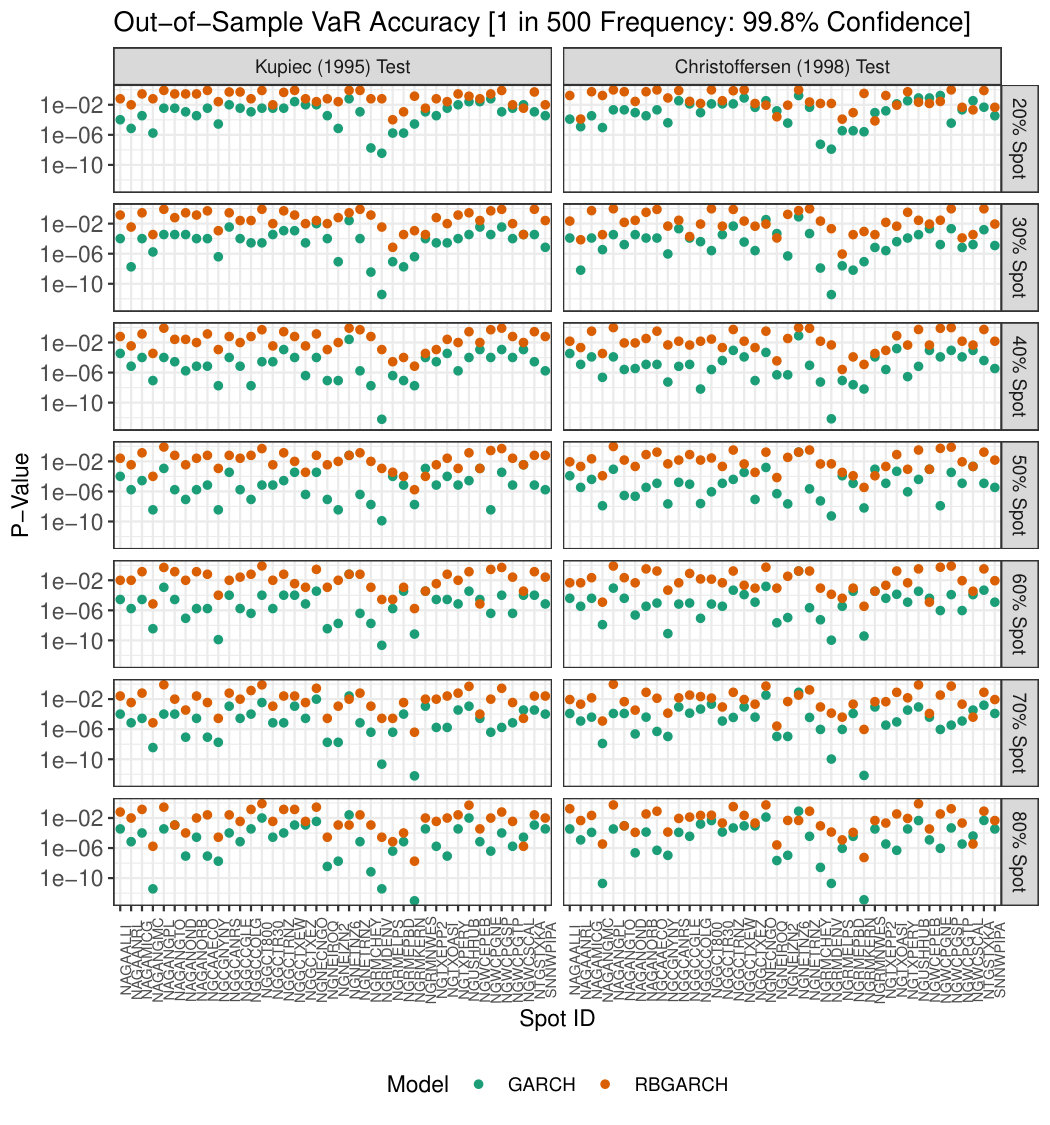

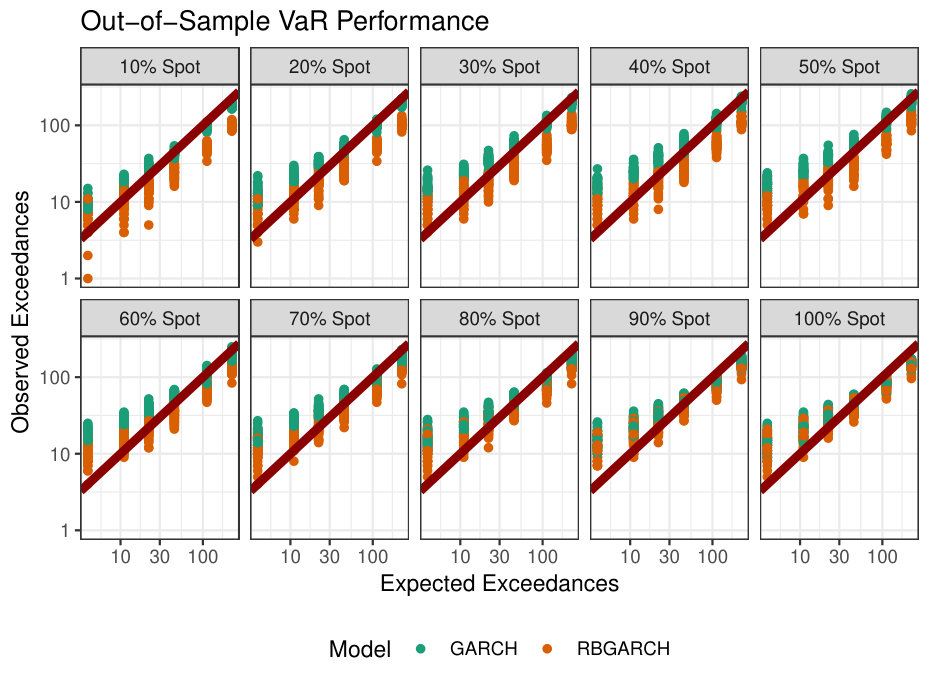

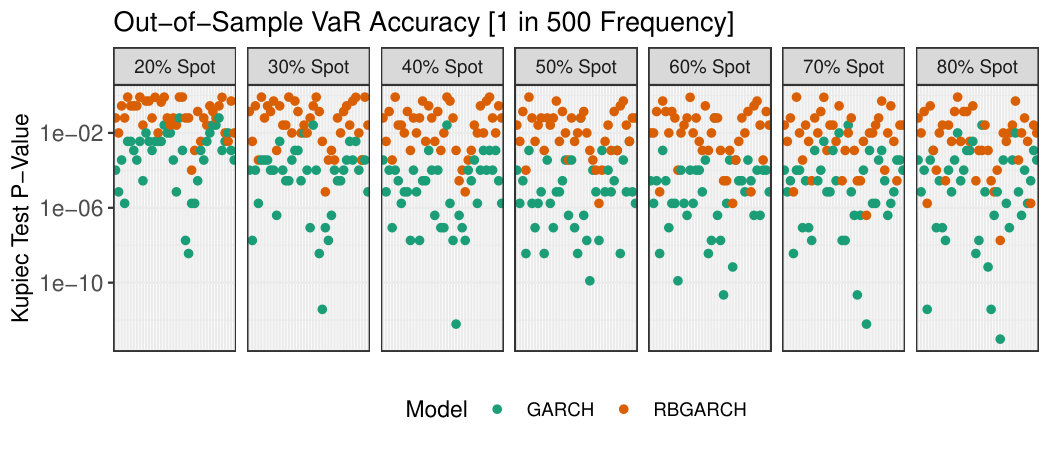

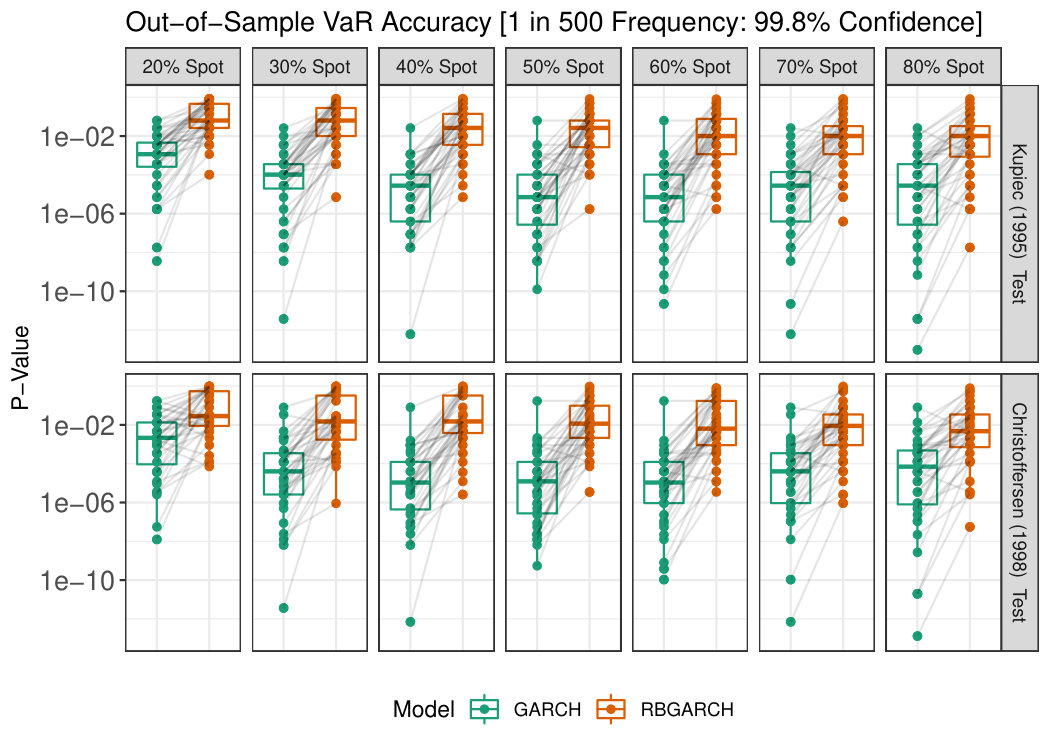

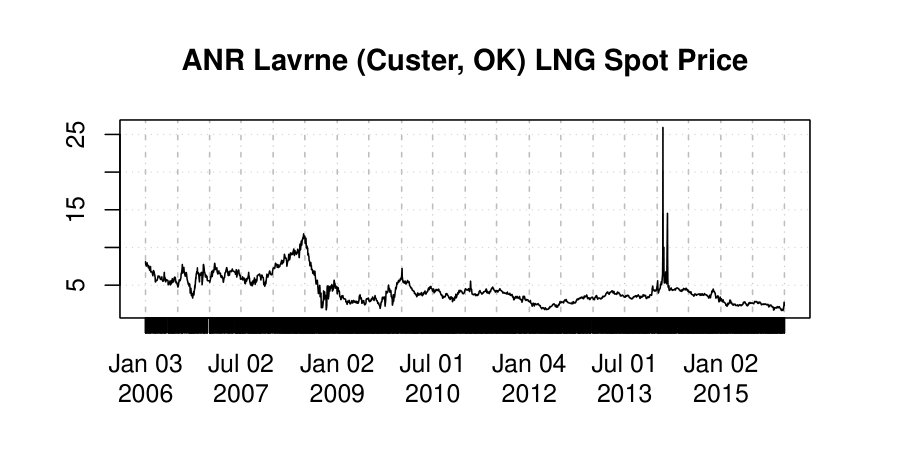

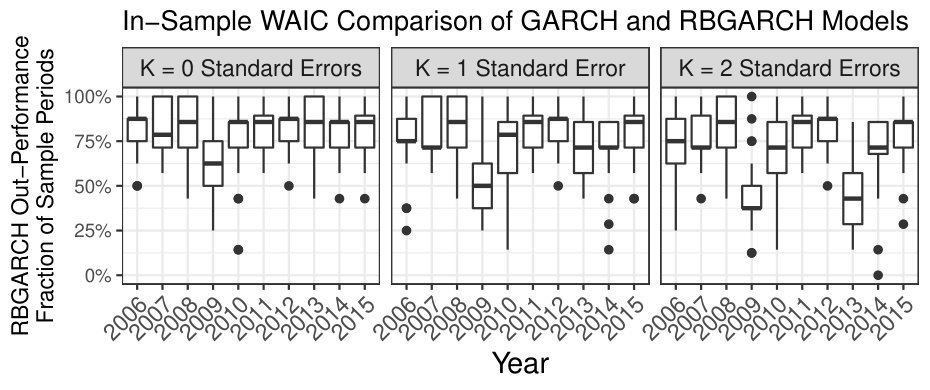

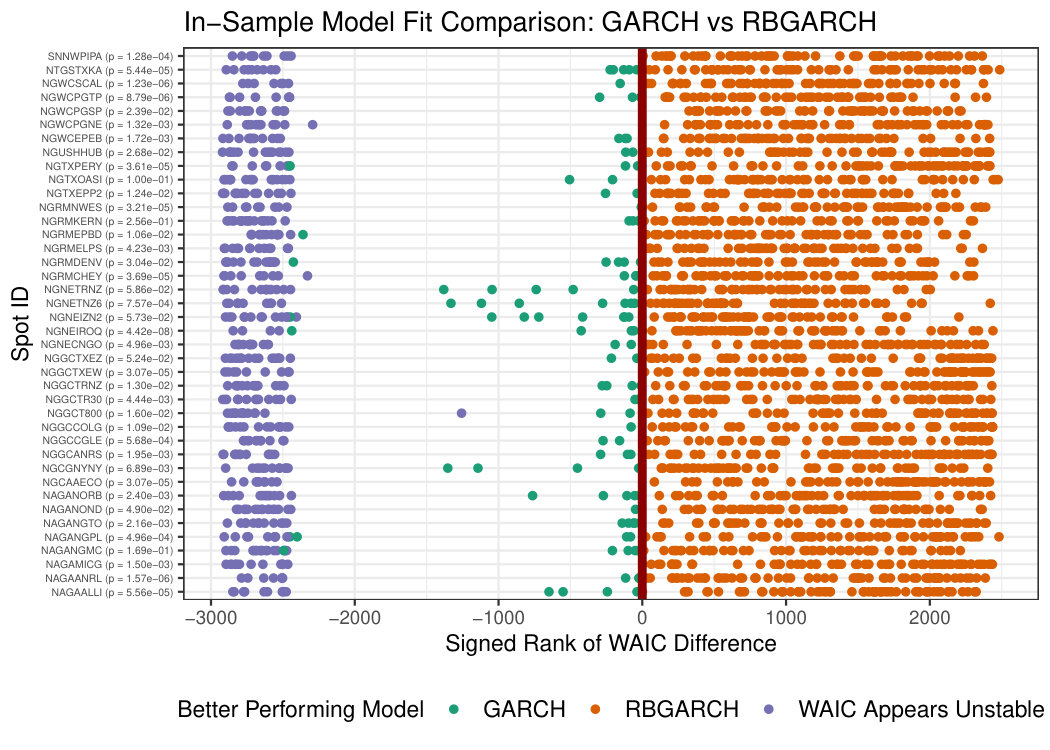

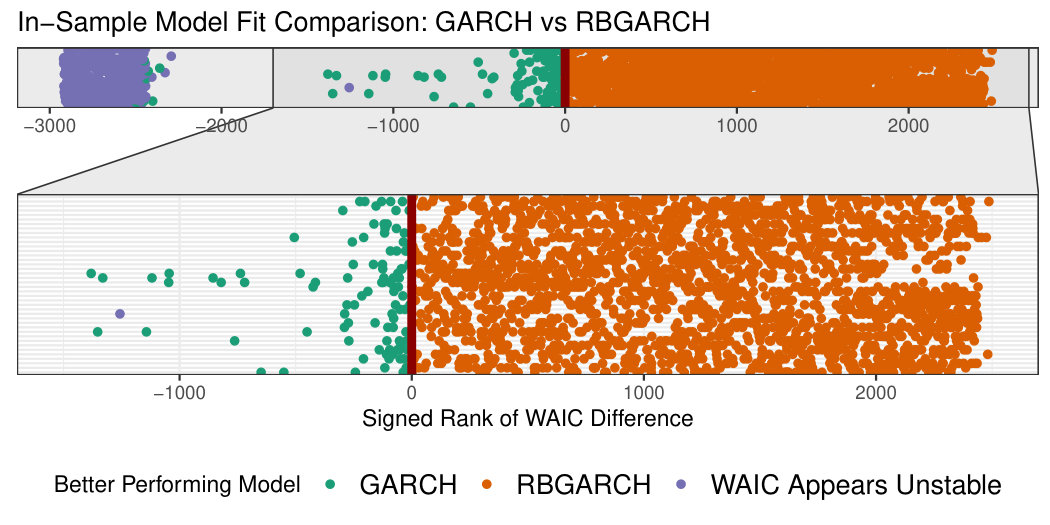

Financial markets for Liquified Natural Gas (LNG) are an important and rapidly-growing segment of commodities markets. Like other commodities markets, there is an inherent spatial structure to LNG markets, with different price dynamics for different points of delivery hubs. Certain hubs support highly liquid markets, allowing efficient and robust price discovery, while others are highly illiquid, limiting the effectiveness of standard risk management techniques. We propose a joint modeling strategy, which uses high-frequency information from thickly-traded hubs to improve volatility estimation and risk management at thinly traded hubs. The resulting model has superior in- and out-of-sample predictive performance, particularly for several commonly used risk management metrics, demonstrating that joint modeling is indeed possible and useful. To improve estimation, a Bayesian estimation…

Click any figure to enlarge with its caption.

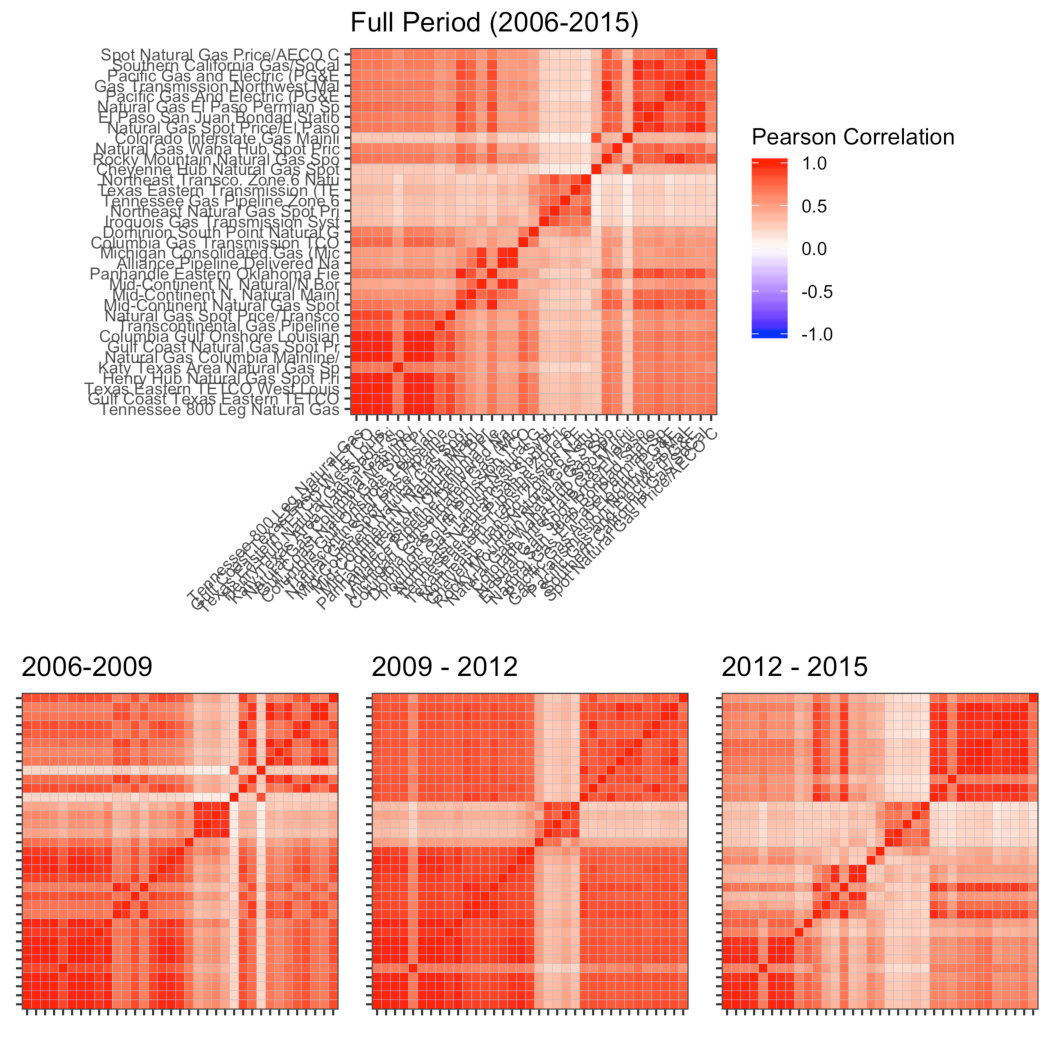

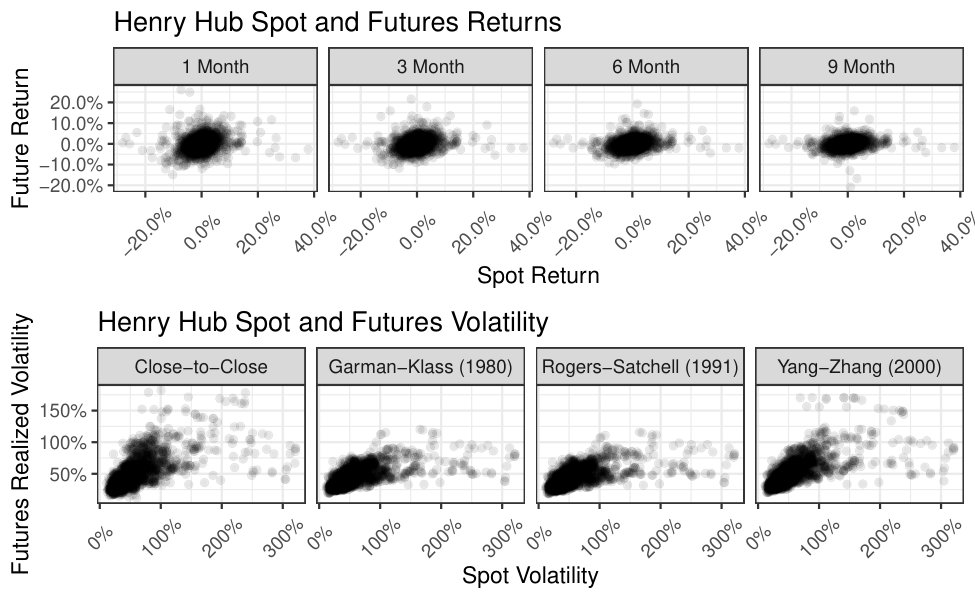

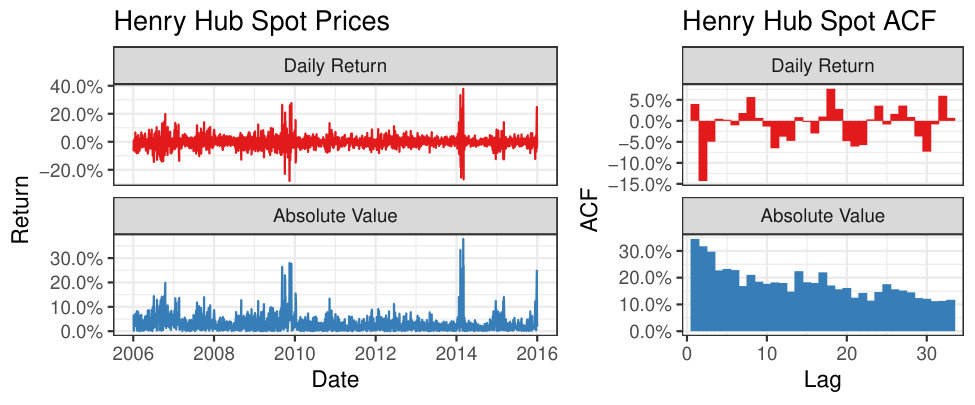

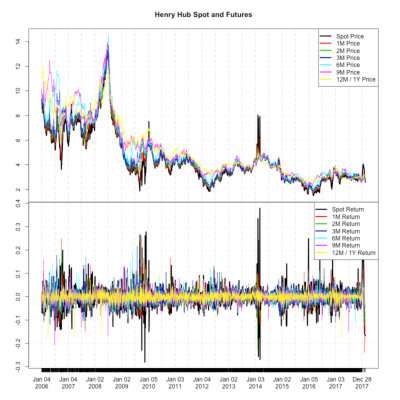

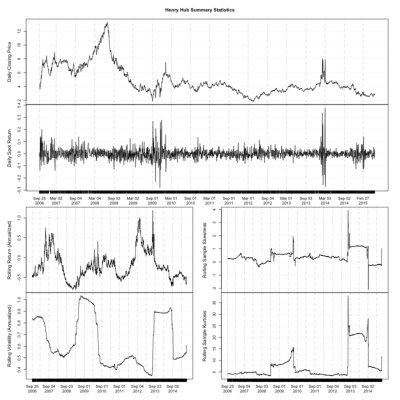

Figure 1

Figure 1 Figure 2

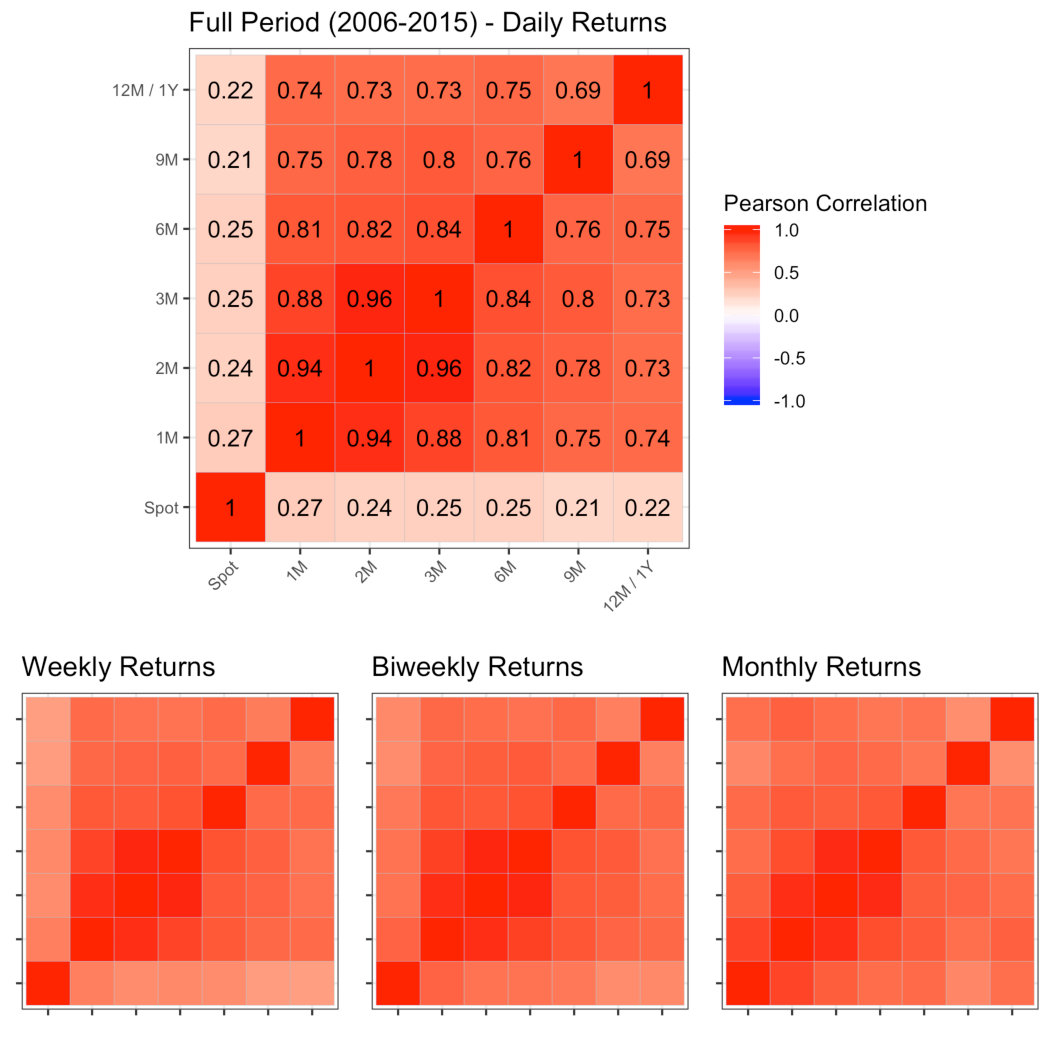

Figure 2 Figure 3

Figure 3 Figure 4

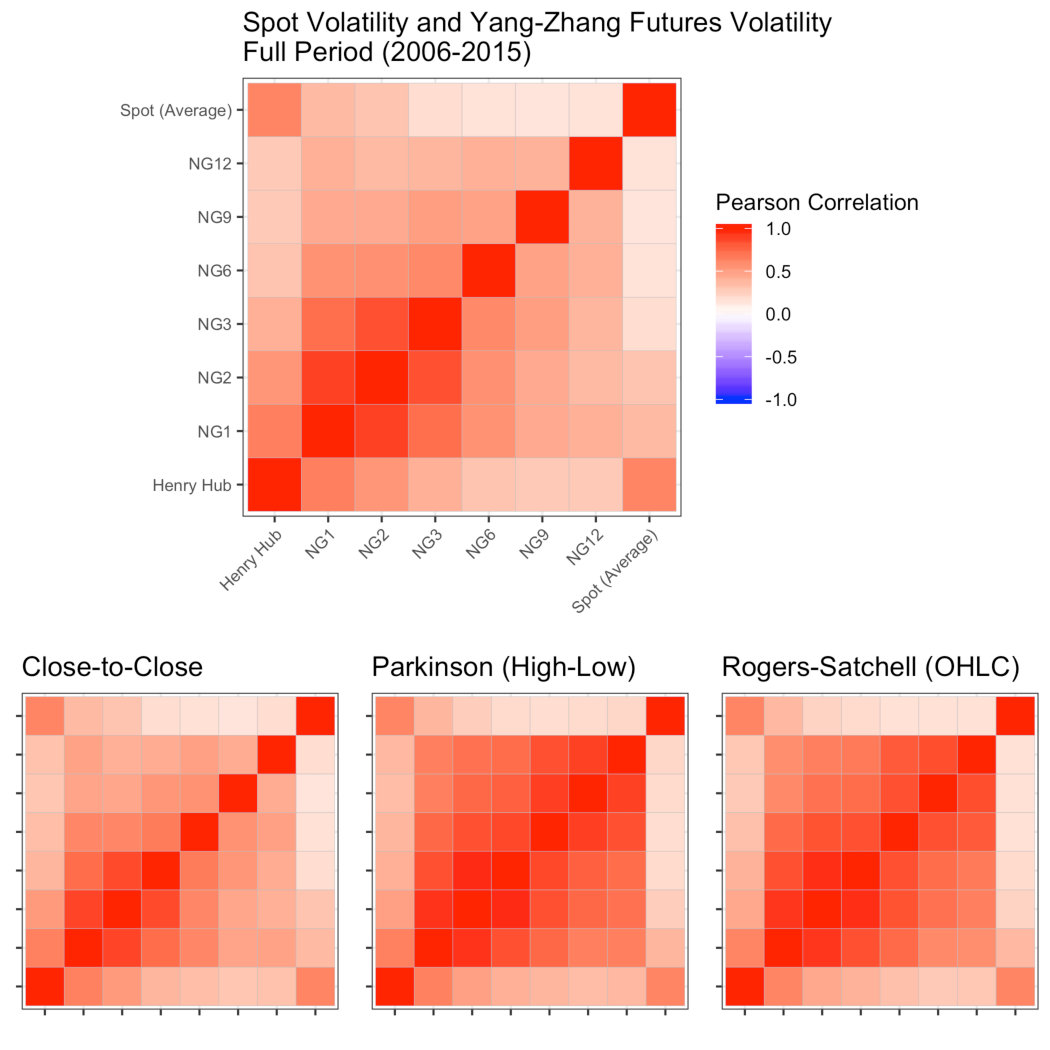

Figure 4 Figure 5

Figure 5 Figure 6

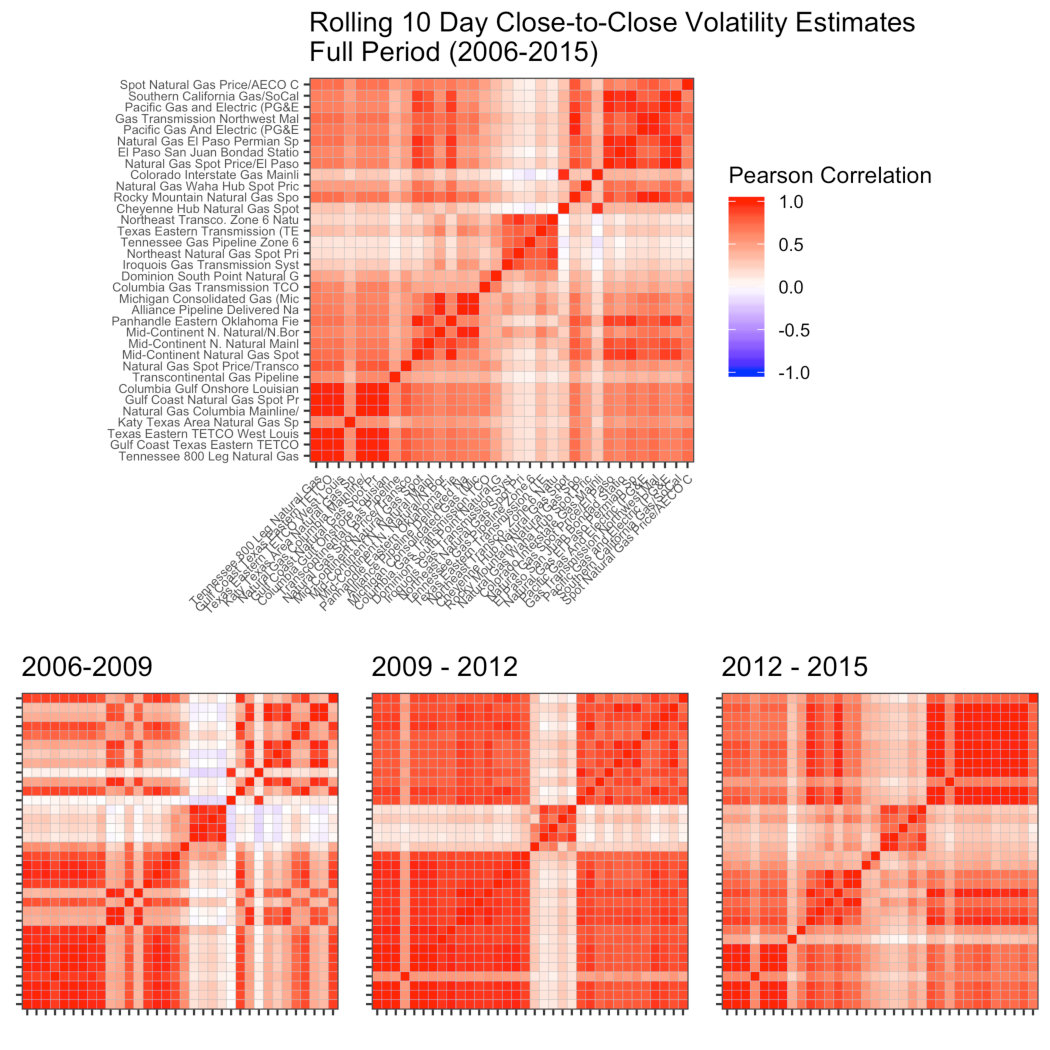

Figure 6 Figure 7

Figure 7 Figure 8

Figure 8 Figure 9

Figure 9 Figure 10

Figure 10 Figure 11

Figure 11 Figure 12

Figure 12 Figure 13

Figure 13 Figure 14

Figure 14 Figure 15

Figure 15 Figure 16

Figure 16 Figure 17

Figure 17 Figure 18

Figure 18 Figure 19

Figure 19 Figure 20

Figure 20 Figure 21

Figure 21 Figure 22

Figure 22 Figure 23

Figure 23 Figure 24

Figure 24 Figure 25

Figure 25 Figure 26

Figure 26 Figure 27

Figure 27Peer Reviews

No public reviews on file for this paper yet. If you reviewed it on a platform where reviews are public (OpenReview, ICLR, NeurIPS, ICML), you can paste yours below so the community can read it here.

Videos

No videos yet. Explain this paper in a talk, walkthrough, or lecture? Add one.

Taxonomy

TopicsMarket Dynamics and Volatility · Monetary Policy and Economic Impact · Reservoir Engineering and Simulation Methods

\xpatchbibmacro

name:andothers\bibstringandothers\bibstring[*]*andothers

11affiliationtext: Department of Statistics, Rice University 22affiliationtext: Center for Computational Finance and Economic Systems, Rice University

Multivariate Modeling of Natural Gas Spot Trading Hubs Incorporating Futures Market Realized Volatility

Michael Weylandt111To whom correspondence should be addressed: [email protected].

Yu Han

Katherine B. Ensor

(Last Updated: )

Abstract

Financial markets for Liquified Natural Gas (LNG) are an important and rapidly-growing segment of commodities markets. Like other commodities markets, there is an inherent spatial structure to LNG markets, with different price dynamics for different points of delivery hubs. Certain hubs support highly liquid markets, allowing efficient and robust price discovery, while others are highly illiquid, limiting the effectiveness of standard risk management techniques. We propose a joint modeling strategy, which uses high-frequency information from thickly-traded hubs to improve volatility estimation and risk management at thinly traded hubs. The resulting model has superior in- and out-of-sample predictive performance, particularly for several commonly used risk management metrics, demonstrating that joint modeling is indeed possible and useful. To improve estimation, a Bayesian estimation strategy is employed and data-driven weakly informative priors are suggested. Our model is robust to sparse data and can be effectively used in any market with similar irregular patterns of data availability.