Game-Theoretic Optimal Portfolios in Continuous Time

Alex Garivaltis

TL;DR

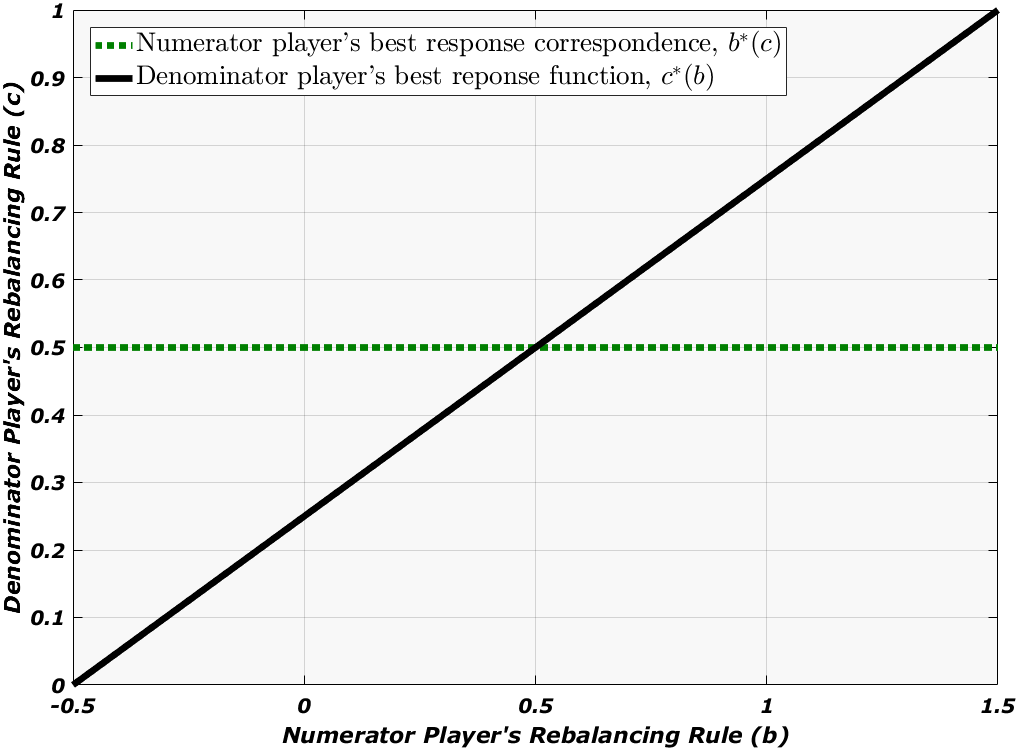

This paper models a continuous-time trading game where two players choose rebalancing rules, revealing that the Nash equilibrium involves both adopting the Kelly rule, aligning with discrete-time results.

Contribution

It demonstrates that in a continuous-time game, the Nash equilibrium involves both players using the Kelly rule, extending discrete-time game results to continuous time.

Findings

Nash equilibrium involves both players using Kelly rule.

The Kelly rule is optimal even over short time intervals.

Results align with Bell and Cover's discrete-time findings.

Abstract

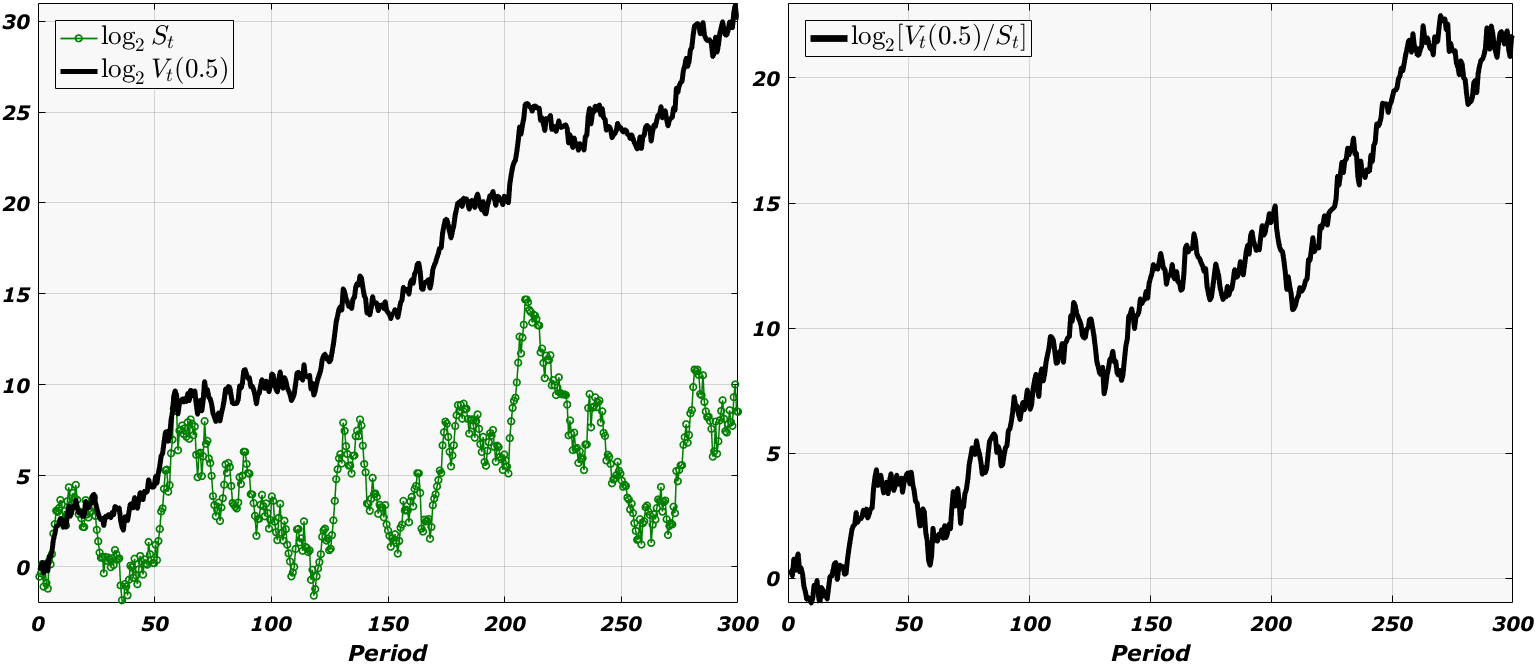

We consider a two-person trading game in continuous time whereby each player chooses a constant rebalancing rule that he must adhere to over . If denotes the final wealth of the rebalancing rule , then Player 1 (the `numerator player') picks so as to maximize , while Player 2 (the `denominator player') picks so as to minimize it. In the unique Nash equilibrium, both players use the continuous-time Kelly rule , where is the covariance of instantaneous returns per unit time, is the drift vector of the stock market, and is a vector of ones. Thus, even over very short intervals of time , the desire to perform well relative to other traders leads one to adopt the Kelly rule, which is ordinarily derived by maximizing the asymptotic exponential growth rate of…

Click any figure to enlarge with its caption.

Figure 1

Figure 1 Figure 2

Figure 2Peer Reviews

No public reviews on file for this paper yet. If you reviewed it on a platform where reviews are public (OpenReview, ICLR, NeurIPS, ICML), you can paste yours below so the community can read it here.

Videos

No videos yet. Explain this paper in a talk, walkthrough, or lecture? Add one.

Taxonomy

TopicsFinancial Markets and Investment Strategies · Stochastic processes and financial applications · Economic theories and models