Market fragmentation and market consolidation: Multiple steady states in systems of adaptive traders choosing where to trade

Aleksandra Alori\'c, Peter Sollich

TL;DR

This paper models how adaptive traders choose trading venues, revealing conditions that lead to either fragmented or consolidated markets and analyzing the stability and dynamics of these states.

Contribution

It provides a quantitative analysis of market fragmentation versus consolidation, identifying conditions for steady states based on aggregate venue parameters.

Findings

Long memory promotes consolidated steady states.

Fragmented states are metastable with long memory.

Finite memory leads to long-term consolidation despite metastability.

Abstract

Technological progress is leading to proliferation and diversification of trading venues, thus increasing the relevance of the long-standing question of market fragmentation versus consolidation. To address this issue quantitatively, we analyse systems of adaptive traders that choose where to trade based on their previous experience. We demonstrate that only based on aggregate parameters about trading venues, such as the demand to supply ratio, we can assess whether a population of traders will prefer fragmentation or specialization towards a single venue. We investigate what conditions lead to market fragmentation for populations with a long memory and analyse the stability and other properties of both fragmented and consolidated steady states. Finally we investigate the dynamics of populations with finite memory; when this memory is long the true long-time steady states are…

Click any figure to enlarge with its caption.

Figure 10

Figure 10 Figure 11

Figure 11 Figure 12

Figure 12 Figure 13

Figure 13 Figure 14

Figure 14 Figure 15

Figure 15 Figure 16

Figure 16 Figure 1

Figure 1 Figure 2

Figure 2 Figure 3

Figure 3 Figure 4

Figure 4 Figure 5

Figure 5 Figure 6

Figure 6 Figure 7

Figure 7 Figure 8

Figure 8 Figure 9

Figure 9 Figure 17

Figure 17 Figure 10

Figure 10 Figure 11

Figure 11 Figure 12

Figure 12 Figure 13

Figure 13 Figure 14

Figure 14 Figure 15

Figure 15 Figure 16

Figure 16 Figure 1

Figure 1 Figure 2

Figure 2 Figure 3

Figure 3 Figure 4

Figure 4 Figure 5

Figure 5 Figure 6

Figure 6 Figure 7

Figure 7 Figure 8

Figure 8 Figure 9

Figure 9 Figure 34

Figure 34Peer Reviews

No public reviews on file for this paper yet. If you reviewed it on a platform where reviews are public (OpenReview, ICLR, NeurIPS, ICML), you can paste yours below so the community can read it here.

Videos

No videos yet. Explain this paper in a talk, walkthrough, or lecture? Add one.

Market fragmentation and market consolidation: multiple steady states in systems of adaptive traders choosing where to trade

Aleksandra Alorić

Scientific Computing Laboratory, Center for the Study of Complex Systems

Institute of Physics Belgrade, University of Belgrade, Pregrevica 118, 11080 Belgrade, Serbia

Peter Sollich

Institut fur Theoretische Physik, Georg-August-Universität Göttingen

Friedrich-Hund-Platz 1, D-37077 Göttingen, Germany

Disordered Systems Group, Department of Mathematics, King’s College London, Strand, London WC2R 2LS, UK

Abstract

Technological progress is leading to proliferation and diversification of trading venues, thus increasing the relevance of the long-standing question of market fragmentation versus consolidation. To address this issue quantitatively, we analyse systems of adaptive traders that choose where to trade based on their previous experience. We demonstrate that only based on aggregate parameters about trading venues, such as the demand to supply ratio, we can assess whether a population of traders will prefer fragmentation or specialization towards a single venue. We investigate what conditions lead to market fragmentation for populations with a long memory and analyse the stability and other properties of both fragmented and consolidated steady states. Finally we investigate the dynamics of populations with finite memory; when this memory is long the true long-time steady states are consolidated but fragmented states are strongly metastable, dominating the behaviour out to long times.

††preprint: APS/123-QED

I Introduction

Whether a consolidated or a fragmented market is more beneficial to a population of traders is a long-standing debate Mendelson (1987); Chowdhry and Nanda (1991); Madhavan (1995); Biais et al. (2005); Bennett and Wei (2006); Degryse et al. (2015). In a consolidated or concentrated market, the majority of trades occurs in one (or a few) as opposed to numerous trading venues. With technological advances we have seen a proliferation of trading venues such as online marketplaces. Even more recently alternative or dark trading venues have appeared, e.g. dark pools. These are popular not least for their lack of transparency, which makes them interesting for trading large quantities of shares without strongly influencing the price, see e.g. Buti et al. (2016); Degryse et al. (2015).

The emergence of collective behaviour in systems of autonomous agents is a research topic that has seen widespread interest among physicists in the last couple of decades. The main reason for this is the recognition that statistical physics techniques, which contributed to the understanding of macroscopic phenomena arising in large systems of interacting microscopic entities, can be applied to a range of biological, economic and social systems. A large body of work exists in the physics literature on collective effects in socio-economic systems Castellano et al. (2009); Bouchaud (2019), e.g. mass movement of people Helbing and Molnar (1995); Moussaïd et al. (2011), herd behaviour of traders Tedeschi et al. (2012), voting patterns Galam et al. (1982); Fernández-Gracia et al. (2014) etc. One of the most prominent examples is the minority game, which continues to attract interest due to its simplicity and its ability to reproduce at least “stylized” facts about financial markets Challet et al. (2001); Challet and Marsili (2003); extensions of the model also predict interesting grouping phenomena when multiple assets are available to agents Huang et al. (2012). In a similar vein, in this paper, we investigate whether fragmentation and consolidation can arise solely as a consequence of interactions at the level of the agents, combined with individual adaptation.

Some studies of stylized models of market competitions already exist, often pointing out the emergence of monopolies whereby the majority of trades occurs in one trading venue. Pagano Pagano (1989) argues that when markets are identical (in terms of their transaction costs), risk averse traders will concentrate in a single market. On the other hand, when there is asymmetry, fragmentation might arise with traders being clustered based on the sizes of their desired transactions. Chowdhry and Nanda Chowdhry and Nanda (1991) reach the same conclusion in a system with asymmetrically informed traders and a general number of markets.

Ellison et al. Ellison et al. (2004) and Shi et al. Shi et al. (2013) also study competition among markets and the conditions under which such competition can lead either to monopolies or to coexistence of multiple markets. The authors name two significant effects in a competition of double auction trading venues. One of them is the positive size effect, i.e. agents prefer to trade in a market where there are already many traders of the opposite type. As an example, sellers like trading at markets where there are many buyers as this gives them a wider choice of offers. The authors of Refs. Ellison et al. (2004); Shi et al. (2013) also suggest the existence of a negative size effect in a double auction market: agents will prefer being in the minority group of traders more often, with e.g. buyers benefiting from trading at a market where there are not many other buyers, see e.g. Caillaud and Jullien (2003)). Ellison et al. Ellison et al. (2004) point out that such negative size effects can enable the coexistence of many markets. On the other hand Shi et al. Shi et al. (2013) investigate which of the two effects is stronger and find that due to more substantial positive effects, a monopoly will be the favoured end-state in many situations. The authors of Shi et al. (2013) argue that market coexistence remains a possibility when there is strong market differentiation, especially for markets that have different pricing policies: one market might charge a fixed participation fee while another might take a profit fee. A common feature of the studies mentioned above is that some form of Nash equilibrium analysis was used, assuming perfect information about the activity of all traders and maximisation of an underlying utility function for the agents.

The increased proportion of trades that take place in dark trading venues – 15% of the US share market volume was traded in dark pools in 2013 Shorter and Miller (2014) – suggests increased fragmentation at least between traditional and dark trading. Calling for more research on reasons behind market fragmentation, Gomber et al. Gomber et al. (2017) suggest the heterogeneity of traders and their needs as one of the main drivers of market fragmentation. However, studies of similar effects such as the emergence of market loyalty in fish markets Kirman and Vriend (2000), herding Tedeschi et al. (2012) and grouping of agents in multi-resource minority games Huang et al. (2012) show that fragmentation-like phenomena may also be emergent. Nonetheless, existing models for such emergent fragmentation often assume a considerable amount of structure, e.g. in the connectivity among agents, the information available about the actions of other players, the rules of interaction via the market mechanism, the asymmetry between buyers and sellers, etc. In contrast, we study here a model in which initially homogeneous agents adapt only to their private information, and show that even in such a system both market fragmentation and consolidation can occur depending on global system parameters.

Based on observations from the CAT tournament Cai et al. (2009), where the spontaneous emergence of long-lived market loyalties was seen in complicated systems of adaptive markets and traders, we hypothesize that the reason for fragmentation may not lie in the intricacies of different market mechanisms or trading strategies. Instead, we conjecture that fragmentation is a collective phenomenon arising as a consequence of the continuous adaptation of the individual agents to an evolving system. To test this hypothesis, we developed a stylised model of double auctions and adaptive traders (Alorić et al., 2015, 2016) that does indeed predict emergent fragmentation under minimal assumptions on the complexity of market and trading mechanisms. The model also shows market consolidation under some circumstances. Our focus in this study is to pin down under what conditions fragmentation and consolidation occur, and what relative benefits they bring for the tradners. As we will see the behaviour of the model is remarkably rich in spite of its simplicity, with multiple steady states coexisting in the limit of long agent memory. For finite memory length, this can lead to the existence of long-lived metastable states that dominate before the true steady state is reached eventually.

We start with a short description of the model Alorić et al. (2016) in section II and then proceed to the large memory limit analysis of small systems with and 4 agents in section III. These can be thought of as two- and four-player games. They are convenient as we can easily track each trader’s adaptation. At the same time they already reveal qualitative phenomena related to those we find later in large systems, in particular coordination at the same market (for ) and onset of fragmentation via pairwise coordination (for ). Moving on to the large population limit (), we then first analyse a population with homogeneous buying preferences IV.1. We develop the relevant mathematical framework and techniques of analysis here and then generalise the results to systems with separate buyer and seller agent types. Finally we study the system dynamics in some detail to go beyond the steady state analysis in section V.

Overall we follow a typical statistical physics philosophy in using a model that reduces the underlying market choice dynamics to its key ingredients, allowing us to obtain detailed insights into the origins of the resulting collective behaviour. The analysis also relies significantly on statistical physics concepts and methods: we focus mostly on the thermodynamic limit of large agent populations, where we exploit the fact that the behaviour of interacting agents for can be captured by the dynamics of a single agent subject to self-consistently determined population-level order parameters. The main outcome from this physical point of view is the emergence of multiple non-trivial steady states in the large interacting non-equilibrium systems that we study.

II Model

Here we summarize basic assumptions and properties of the model introduced in Alorić et al. (2015, 2016), which is the foundation for the analysis in this paper.

Learning. In the model, agents choose among the available markets once in every trading period and submit their order to the chosen market. A key assumption is that agents base their decision of where to trade on their previous experience at the different markets. Agents rely on the following reinforcement rule, which is based on the experience-weighted attraction rule Camerer and Ho (1999); Ho et al. (2007) but neglects knowledge about the other markets (via so-called fictitious payoffs):

[TABLE]

Here is agent ’s attraction to market at trading period given his/her score or return, , obtained in the previous trading period (see below) and the previous attraction . To understand the role of one can write down the resulting general expression for the attraction at trading round :

[TABLE]

where the Kronecker restricts updates to rounds where the agent’s chosen market is the one () being considered. The factor in this expression is a weight that decays exponentially into the past, becoming small once is of order . Thus each agent effectively averages scores over a sliding window into the past of length , so that can be thought of as setting the length of the agents’ memory.

To choose a market at each trading round, an agent translates the learned attractions into probabilities of choosing each markets, using the multinomial logit or softmax function:

[TABLE]

This aspect of the model is also in line with the experience-weighted attraction literature Camerer and Ho (1999); Ho et al. (2007); is the intensity of choice and regulates how strongly the agents bias their preferences towards actions with high attractions. For the agents choose the option with the highest attraction, while for they choose randomly and with equal probabilities among all options.

We study agents whose choice of the type of trading order (to buy or to sell) is not adaptive but rather set by a fixed buying preferences . This assumption simplifies the analysis while still allowing both consolidation and fragmentation behaviour as shown previously Alorić et al. (2016).

Trading strategies. Agents do not have sophisticated trading strategies in our model and are essentially zero-intelligence traders Gode and Sunder (1993); Duffy (2006); Ladley (2012). Their orders to buy (bid) or sell (ask) a single unit of the underlying good at a certain price are independent of previous returns or other information. We assume specifically that bids, , and asks, , are normally distributed as and , where we fix as in Alorić et al. (2016). After each round of trading each agent receives a score, reflecting their payoff in the trade. This depends on the global trading price set by a chosen market as well as the order the agent has submitted. The scores of agents who do trade are assigned as in previous studies Gode and Sunder (1993); Anufriev et al. (2013): buyers value paying less than they offered (), and so their score is . Sellers value trading for more than their ask (), and so is a reasonable model for their payoff; in both cases is the trading price.

Market mechanism. In the spirit of keeping the model as simple as possible we consider double auction markets in discrete time, counted as before in trading rounds. In every round the global trading price is set by the market: once all orders have arrived, these are used to determine the average bid and average ask and set the price:

[TABLE]

where fixes the price closer to the average bid () or the average ask (), as in Alorić et al. (2015). This parameter thus represents the bias of the market towards buyers or sellers. Once the trading price has been set, all bids below this price, and all asks above it, are marked as invalid orders as they cannot be executed at the current trading price. The remaining orders are executed by randomly pairing buyers and sellers. Excess buyers or sellers, i.e. those that cannot be paired, receive zero score, as do the agents who submitted invalid orders.

Note that traders are not informed about the market biases, nor the market mechanism in general. The only information they have at their disposal in order to adapt their market preferences is their personal score.

III Finite N

III.1 Two traders: coordination

To understand collective effects in trading systems, we first build up some intuition by looking at a very simple model with only one buyer and one seller. The traders have a choice between two markets with different biases. As the system consists of only two agents and two markets, fragmentation (or segregation as introduced previously Alorić et al. (2016)), in which a population will split into distinctive groups favouring one option, is not feasible. However, we can investigate if long lasting loyalty to a single market emerges, which can signal market consolidation.

To make trading possible the two agents effectively need to coordinate, i.e. to submit orders to the same market. This can lead to one of the agents earning less than they could have done at the other market. One question of interest concerns the conditions under which the agents prefer random decisions of who will be a winner or loser in this manner, as opposed to settling in these roles over longer periods of time. Thus we will focus on the existence of coordination of traders and investigate for which parameter settings agents develop strong preferences for the same market. Intriguingly, this two player analysis ends up being largely similar to the work by Hanaki et al. Hanaki et al. (2011) where a two-agent case was likewise studied as a first step to understanding collective effects. (In Hanaki et al. (2011) these concerned specialization behaviour of agents searching for parking spots.)

For the analysis it is convenient to label the two players as and similarly for the two markets. We use the following specific parameter settings:

- •

Of the two players, player always buys while player always sells (, ).

- •

Bids/asks are deterministic, i.e. , , with their difference being fixed to .

- •

The trading price at each market is set as defined in Alorić et al. (2015), .

- •

We assume that the market biases are symmetric: where .

The simplification over our previous work Alorić et al. (2015, 2016) of making bids and asks deterministic allows us to focus solely on the coordination of the market choices and does not change the behaviour of the system qualitatively. The determinstic order prices then also make the trading prices deterministic: .

We can summarize the attraction update rule 1 as

[TABLE]

with the convention that if market was not chosen by agent in round . This generalized score is fully determined by the market choice of the opposite player:

[TABLE]

where denotes the market of choice of the (co)player during trade and

[TABLE]

encodes the relevant nonzero score values that depend on the type of market and agent. The logit assignment (2) by which agents choose a market simplifies for to

[TABLE]

where is the logistic sigmoid. The choice probabilities do not depend on the attractions to the two markets individually but only on their difference . The latter is updated as

[TABLE]

The stochastic variable thus depends on the choices the agents make in trading round , and , which are drawn from distributions that depends on and . This situation simplifies in the long memory limit , where the attraction differences change sufficiently slowly to average out stochastic fluctuations. One can then effectively replace by its expected value (and similarly for and other market choices) in the score (4). This gives

[TABLE]

which can be further simplified into:

[TABLE]

The finite difference on the l.h.s. becomes a derivative in the limit of small if we switch to the rescaled time , for which a unit time interval corresponds to trading periods:

[TABLE]

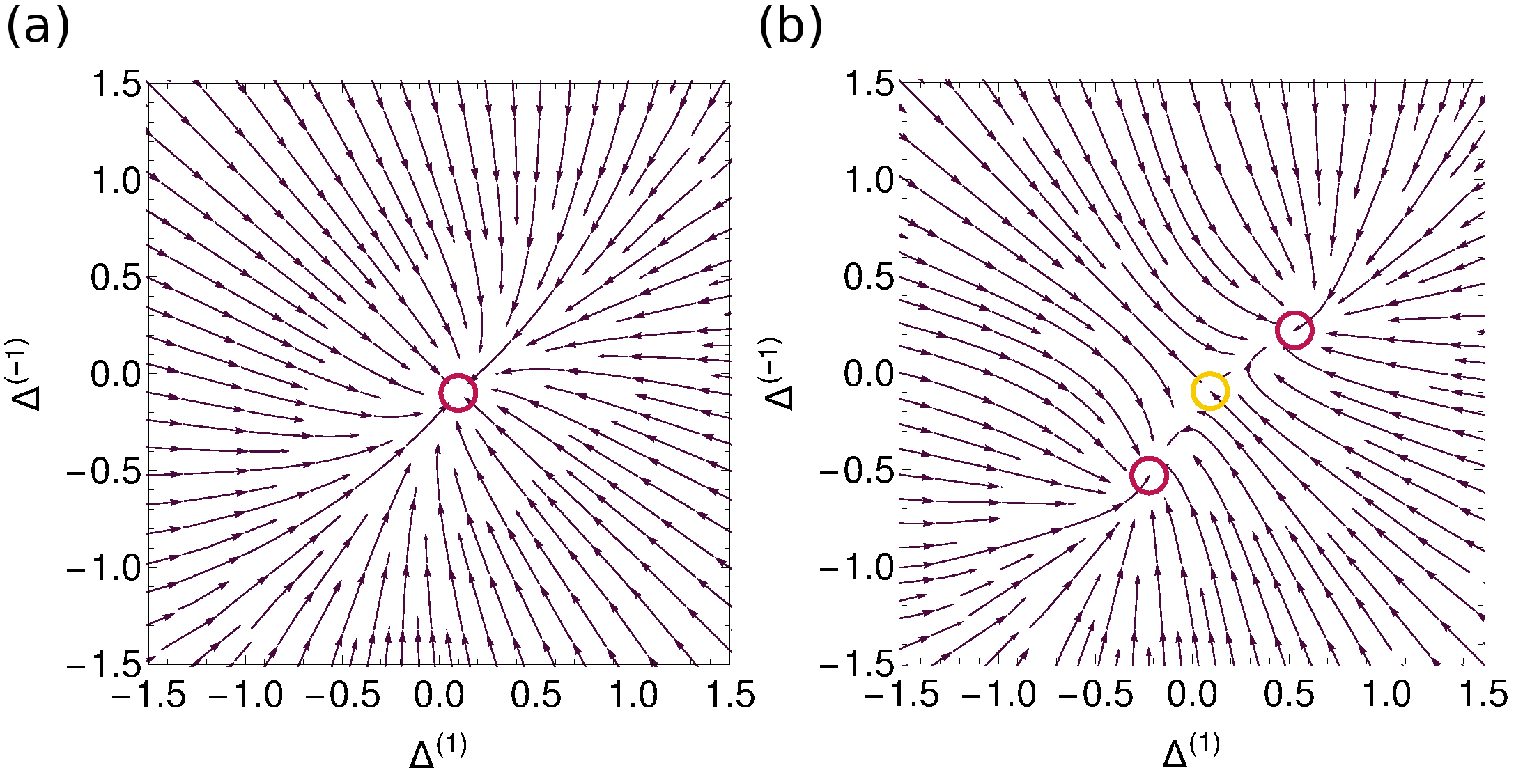

A convenient change in variables that simplifies this pair of differential equations is and , which after some algebra and exploiting the market symmetry gives

[TABLE]

Note that describes the average of the attraction differences of the two agents, while captures the deviation between them.

To understand the dynamics we first consider its fixed points, which need to satisfy

[TABLE]

The first of these equations is always satisfied if , and in that case the equation for has a unique solution whose sign depends on the sign of . When market 1 is favourable towards buyers (), will be positive. As , this can be interpreted as a state where buyers and sellers learn which market is good for them, and thus have preferences for opposite markets. ( is positive meaning that player 1, the buyer, prefers market 1, which is good for buyers.) As we shall see shortly this solution is only stable for low intensities of choice where the agents’ market choice dynamics remains largely random. The intuition for the appearance of an instability with increasing is that, if agents were to follow through fully on their attractions towards opposite markets, they would never get to trade.

The stability of the solution can be studied by linearizing the dynamical equations (6), resulting in the stability criterion

[TABLE]

Expressed in the original variables , the solution with is stable as long as

[TABLE]

This stability condition is exactly the same as in Ref. Hanaki et al. (2011) because the learning dynamics we follow is essentially the same and differs only in the details of the deterministic returns.

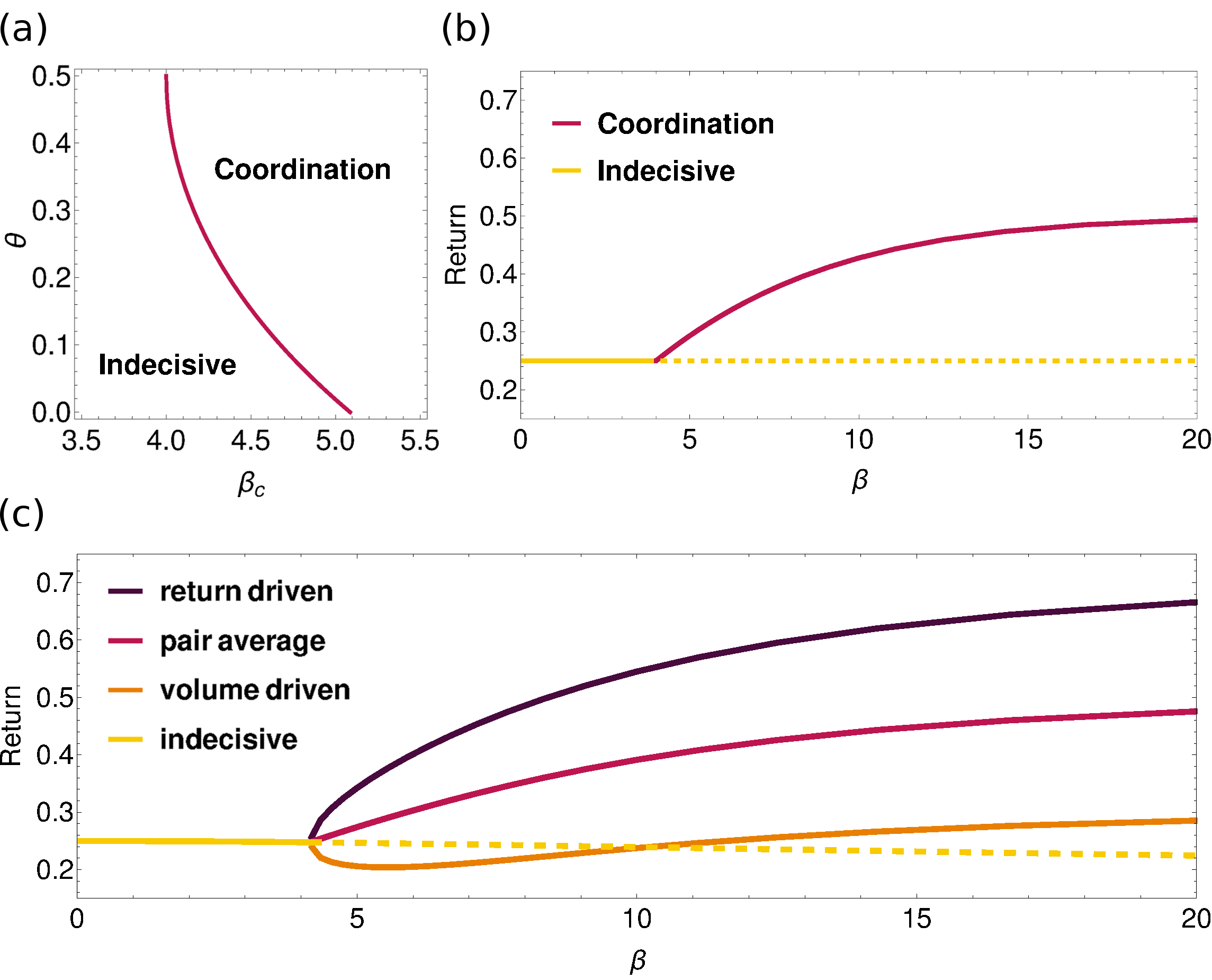

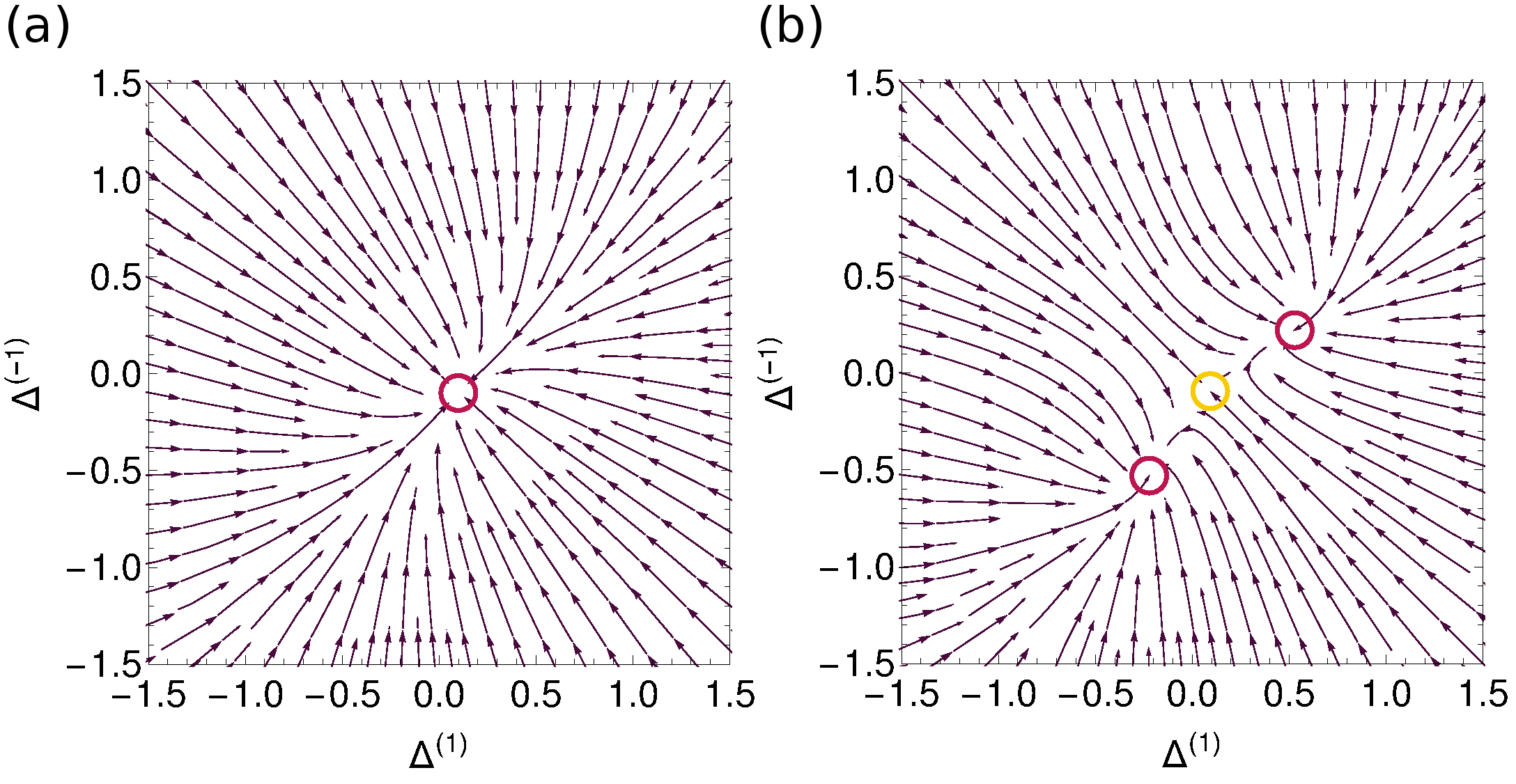

We illustrate in Figure 1 that for low intensities of choice, where the stability criterion (8) is satisfied, the fixed point discussed so far is the only one. At higher the criterion is violated and two new stable fixed points appear. Here the agents’ attraction differences are of the same sign, i.e. they prefer going to the same market. This happens even though market favours buyers while market favours sellers.

At first sight it may seem puzzling that for high intensity of choice, one of the agents decides to settle for less in persistently choosing the market where (s)he will be awarded lower scores. However, this pattern of behaviour in fact maximizes the number of trades that take place. In the low- regime, all four pairings of market choices are equally probable: but only the first and the last enable trading. On the other hand, in the high regime, when both agents persistently choose the same market, they always get to trade, although one of the traders always receives a lower return. For the market parameters used in Fig. 1, , the agent who settles for a lower score then receives a score of , while the other one obtains 0.7. This has to be compared to the average payoff at low , which by averaging over the four market choice pairings is seen to be . Hence both agents clearly earn more in the coordinated regime than by choosing randomly.

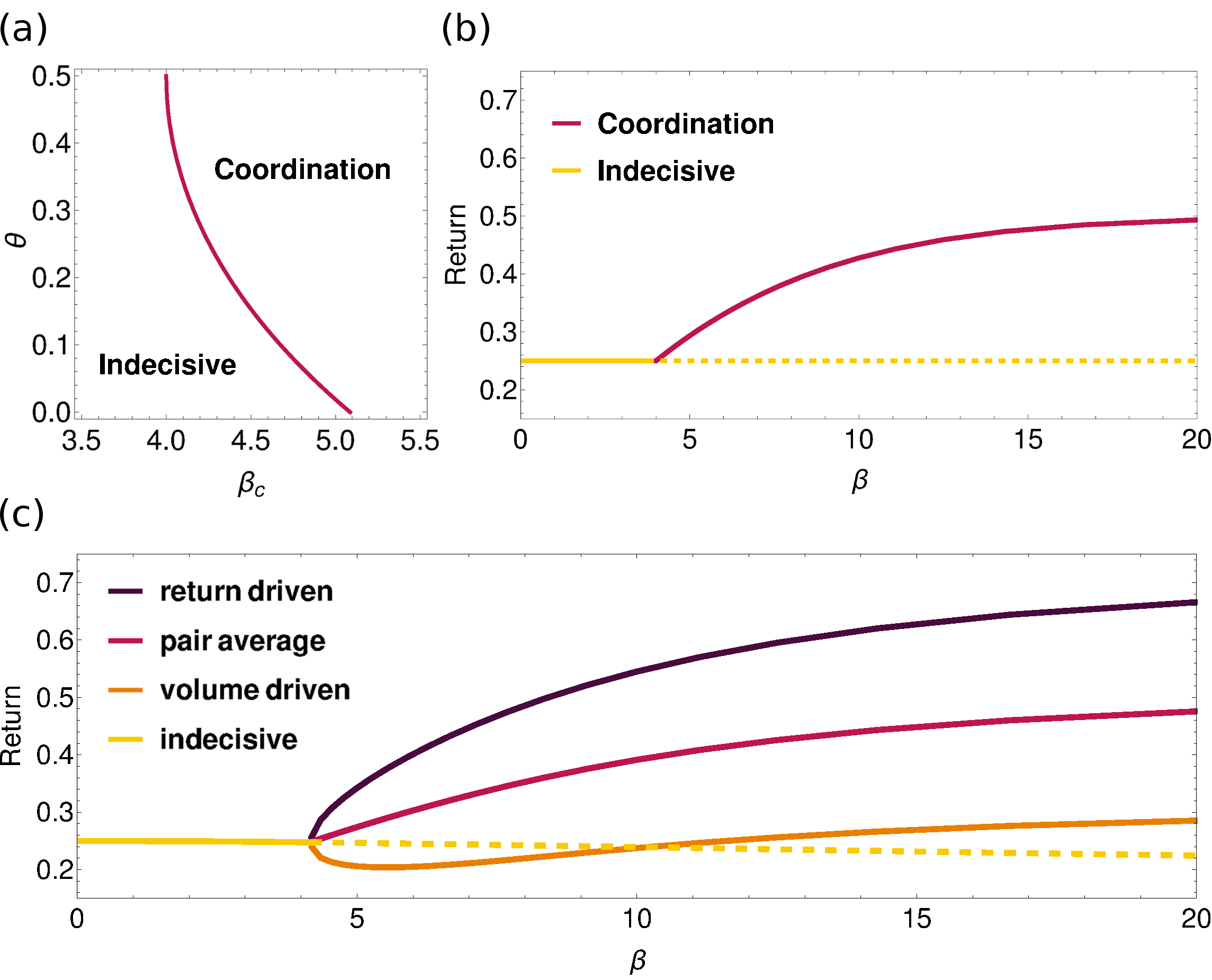

We can find the domain of parameters and where the agents will coordinate (Figure 2 (a)) by starting from the regime of agents choosing largely randomly and tracking where the stability condition (8) is first violated as is increased. As in the case of large populations Alorić et al. (2016), we observe that increases with increased market difference or bias. The symmetry breaking between markets that coordination requires is therefore not driven by the difference between the markets. In fact the coordination threshold is lowest for a system with two identical markets (). One can rationalize this by saying that the agents are happiest to coordinate at one of the markets in this limit as neither needs to settle for less. We show average returns for this setup – a pair of traders choosing between two unbiased markets – as a function of in Figure 2 (b). One observes the expected average score of for low ; as is increased, the agents effectively realize that coordination at a single market enables more trades and consequently higher average returns.

In the panel (c) of Figure 2 we show analogous results for the case of two biased markets (). We plot the individual agents’ payoffs and their average in the state where they coordinate at one market, and compare this to the payoff in the largely random low- state. As a reference we also plot the continuation of the latter to larger , where it is unstable. It is notable that returns decrease with on this branch: the more the agents act on their preference for opposite markets, the less often they manage to meet at the same market. This results in more and more trading rounds where both receive a return of zero, dragging down average returns.

By contrast, in the coordinated state the average return increases with , i.e. as the agents make more and more definite choices. Interestingly, Figure 2 (c) shows that this increase in the average return is accompanied by a growing difference between the returns of the individual agents. These payoff differences can occur in our model because agents are unaware of the opposite player’s return, making decisions only on the basis of their own scores. Borrowing terminology from the large system limit Alorić et al. (2016) we will call the agent with the higher return return driven and the other volume driven. It is notable in Figure 2 (c) that there is a range of where the volume driven agent receives an average return that is lower not only than that of the return oriented agent, but also than the hypothetical return both agents would achieve in the (unstable) uncoordinated state; this regime grows as the markets become more biased.

Intuitively, the return driven player develops a strong preference for the market where (s)he can earn more. The other agent will occasionally try the other market, but typically not get to trade there. As this results in a zero return, (s)he is better off persisting with the coordinated choice, which offers a low but at least nonzero return.

The two agent systems studied so far can be mapped to two player games: the symmetric pure coordination game when the markets are unbiased, and the battle of the sexes when markets are symmetrically biased. For these games it is known that the two coordinated states correspond to pure Nash equilibria, see e.g. Easley and Kleinberg (2010). In the symmetric pure coordination game, both of these are envy free (i.e. both agents earn the same), but not so in the battle of the sexes – this is consistent with the differences we saw between unbiased and biased markets, and the Nash equilibria correspond to the limit of the coordinated states. There are also mixed Nash equilibria. These correspond to the continuation to of our uncoordinated state for the symmetric pure coordination game, but not otherwise. A full correspondence to Nash equilibria could be obtained by modifying the learning rule so that the attractions to markets that were not chosen are kept unchanged. This can be interpreted as “fictitious play” and is discussed in more detail in Nicole and Sollich (2018).

The results described above can be generalized to a pair of traders who do not have strict buyer and seller roles but instead decide to buy with some probability. We assume symmetric preferences for buying, . For a trade to occur, agents now need to be at the same market and need to submit opposite (buy and sell) orders. As the buying preferences are fixed, this only changes from (5) to

[TABLE]

To see this, note that agent receives a buyer payoff when (s)he assumes the role of a buyer (with prob ) while the opposite player acts as seller; (s)he also receives a seller payoff in the opposite configuration. Repeating the calculation above one then finds that the fixed point conditions (7) both acquire a factor of on the r.h.s., while the stability condition (8) is multiplied by the same factor.

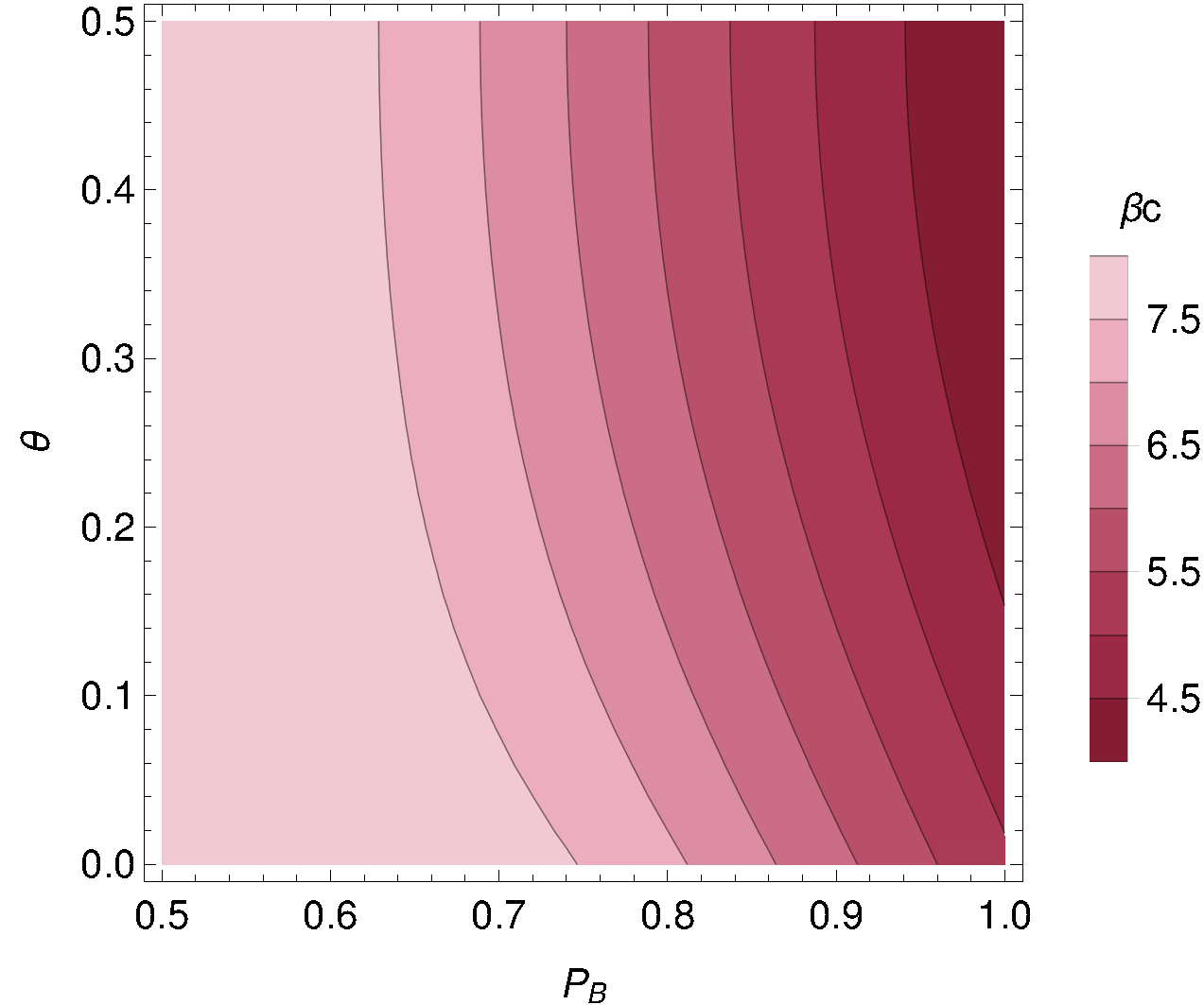

Figure 3 shows contours of the resulting critical for coordination. We note that the coordination threshold increases as approaches 1/2: agents without strong buy/sell preferences need higher intensities of choice to benefit from the coordinated state. This makes sense because agents with closer to derive a lower benefit from coordinating at a market: as they need to assume buyer and seller roles, trades at the same market happen only with some probability, specifically in our setting, which approaches one half for .

III.2 Four traders: onset of fragmentation

The two player system studied above already exhibited an interesting collective phenomenon – coordination at a market to enable more trades, sometimes even to the detriment of an individual agent. Turning to fragmentation, where otherwise homogeneous agents nonetheless learn to adopt different policies, the minimal system size where we can expect a similar effect is . We first study two identical buyers and two identical sellers, choosing agents with deterministic buy/sell behaviour ( or 1) for simplicity. A system with four agents is small enough so that we can still easily write down deterministic equations for the evolution of market attractions, but large enough for the first signals of fragmented states to appear as agents can split across the markets in pairs. We consider again symmetrically biased markets, . As before, the market choice behaviour of each agent is determined by his/her market attraction difference . Here the index denotes the agent group (buyers or sellers) while labels agents within each group. For small the attraction differences again obey deterministic time evolution equations that can be derived by following the reasoning in the previous subsection. The only difference lies in the calculation of the return at a chosen market, which now depends on the choices made by all other players:

[TABLE]

In the expression above, denotes the deterministic part of the return, which only depends on the chosen market and the agent type , by analogy with the two player case in Eq. (9). The Kronecker -symbols ensure other agents are present at the same market . The first term describes the situation where both agents of the same type go to a single market ; the return is then zero if no agents of the opposite type are at the same market, if there are two, and if there is only one (as our chosen agent then only has probability of being allowed to trade). On the other hand, when the second player of the same type is not at the same market, the player receives the full return if there is at least one trader of the opposite group present. This is described by the second term. The deterministic equations for then take the form

[TABLE]

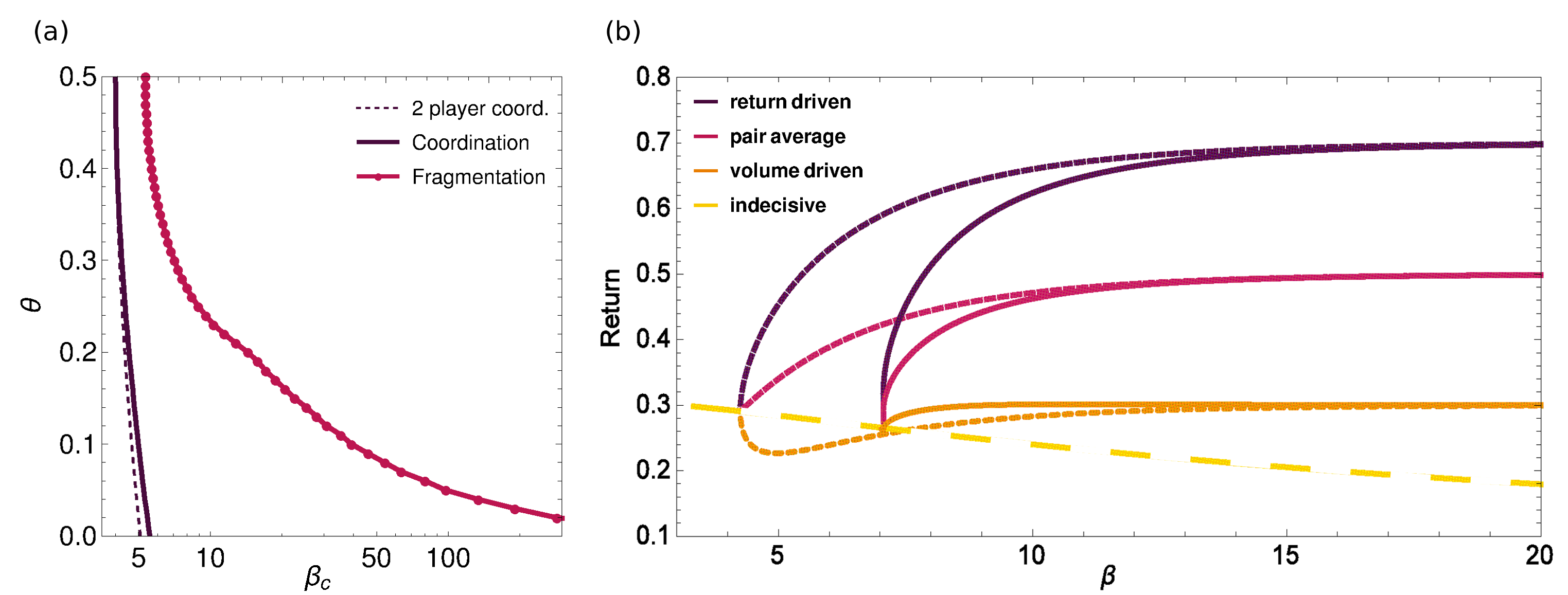

where has the meaning of returns averaged over a long time window so that the Kronecker deltas in are replaced with their expected values, exactly as in the derivation for two players. We solve these equations numerically and find that for low and intermediate intensity of choice the behaviour is analogous to that for , showing a transition from a single uncoordinated fixed point to two coordinated fixed points as increases; throughout this range the agents within each group have identical market attractions. The novel feature of the system is that, when is increased yet further, four new stable states appear. We call these fragmented as each group of agents now “fragments” into two individuals with distinct – and essentially opposite – market preferences. Both markets are then populated by a pair of traders, one from each group. The fragmented fixed points appear in stable/unstable pairs and for high enough value of unstable fragmented fixed points become partially fragmented, e.g. only one group splits across the markets, while the other group specialize for one market. As these fixed points are not stable we do not show this transition line in Figure 4.

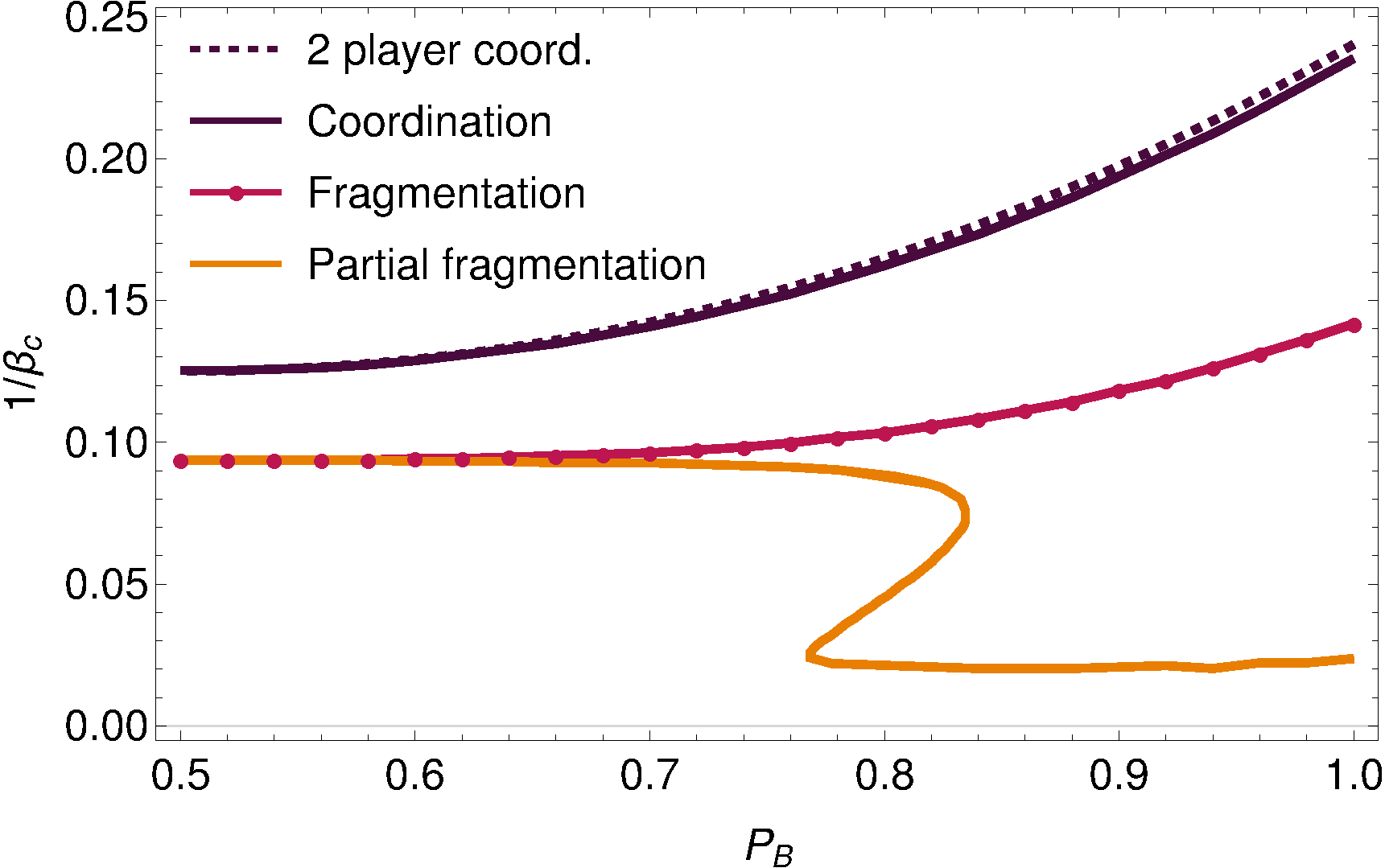

In Figure 4 we show the two critical lines (the coordination and the fragmentation threshold) as a function of the market bias , for the above scenario of four players with strict buy/sell roles. The coordination line is very close to the one for two players, which is included for comparison. Both the coordination and fragmentation lines follow the same trend, with the threshold in increasing as departs from .

The right panel of Figure 4 shows return lines for different intensities of choice : dashed lines correspond to coordinated states, while solid lines are averages in the fragmented state. Note that the difference in returns in the coordinate state is between groups of agents, with all agents in a group either return driven or volume driven. In the fragmented states there is one return driven and one volume driven agent in each group, on the other hand. We note that in the large limit the returns achieved in coordinated and fragmented states become identical. This is because with either pattern of market choices, if these choices are made deterministically then all agents are guaranteed to be able to trade. For finite , returns in the coordinated state are generally higher than for fragmentation.

Note that the four fragmented states arise because in each agent group there are two ways for assigning the two agents to the two markets. For agents, one therefore expects such states. This number grows very rapidly with while the number of coordinated states remains at two.

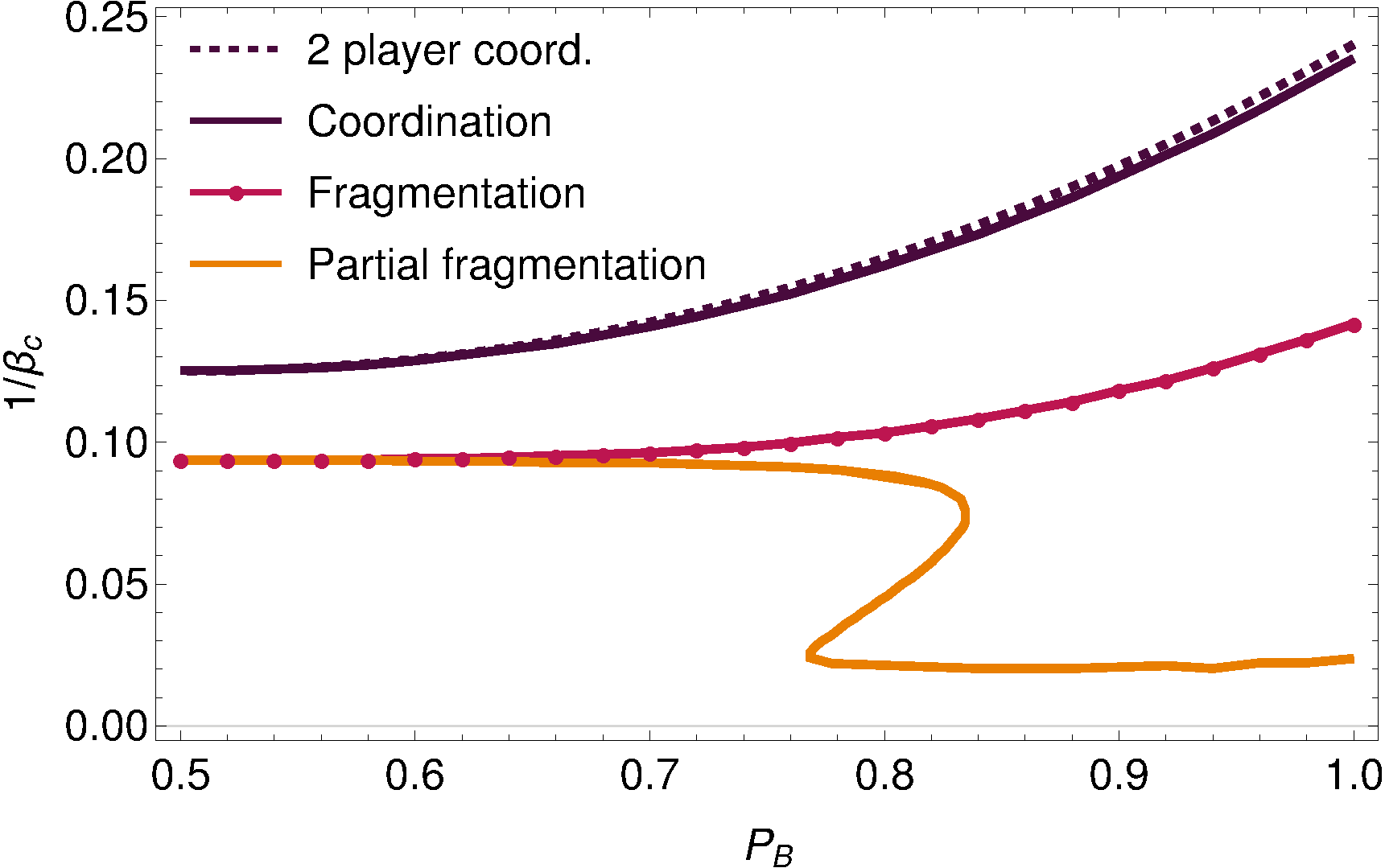

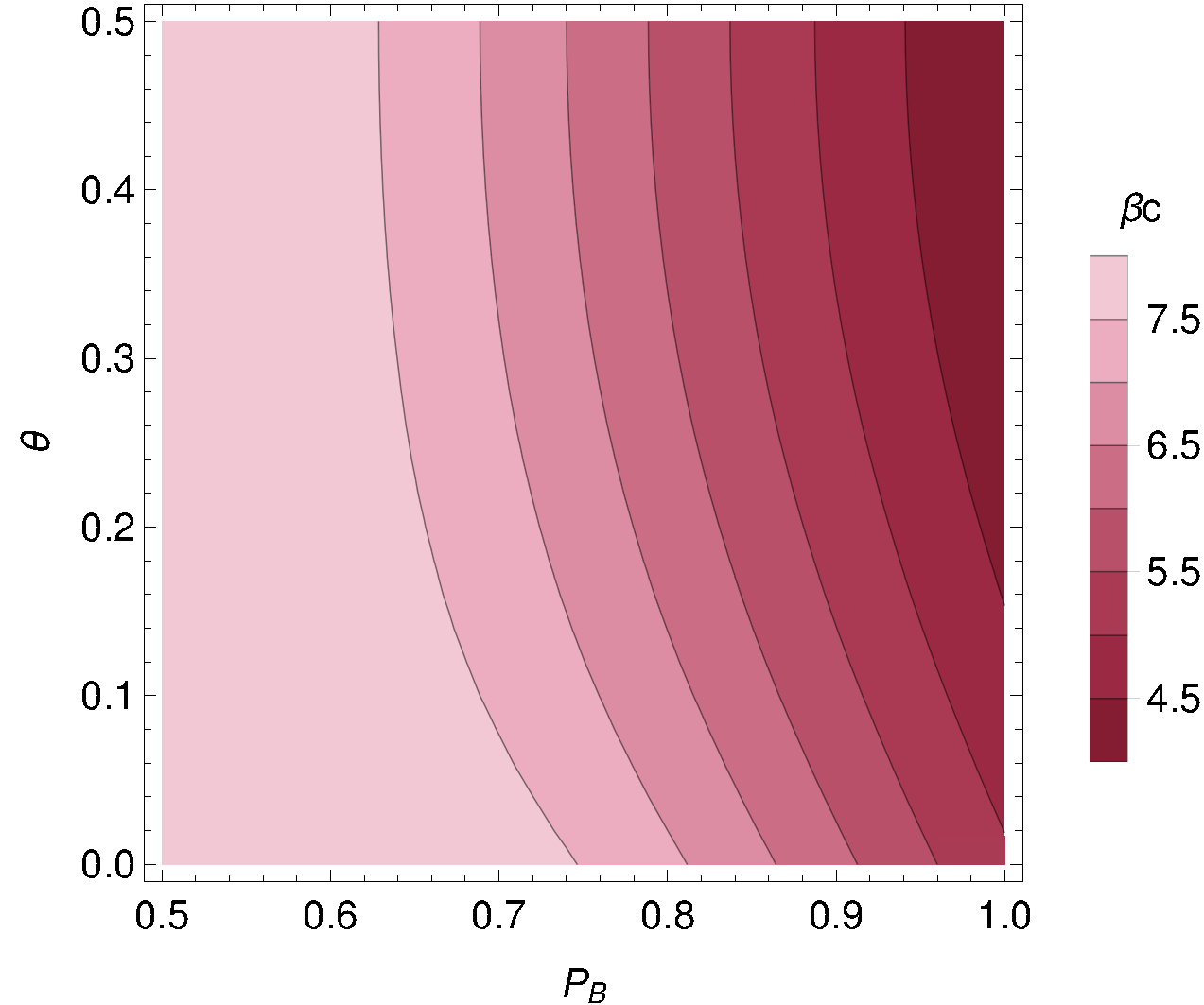

Finally, as in the analysis of the two agent system we can generalise the results by allowing agents to assume the role of buyer with some group dependent probability . We again take these probabilities as symmetric between groups, . The deterministic part of the agents’ returns is then modified in a manner directly analogous to Eq. (9), and one can determine the effect on the existence of the various steady states. Figure 5 shows the results for the symmetric markets and symmetric groups. As in the system with only two agents, when the traders’ preferences for buying are similar () they have a weaker incentive to coordinate, resulting in a higher coordination threshold for (for the sake of clearer visualisation we use on the y-axis). The same behaviour is seen also for the fragmentation threshold.

We indicate in Figure 5 also the regime where a further type of fixed point exists: partially fragmented states. In these states there is a single agent whose market preference is the opposite of that of the other three players, so that only one agent group is fragmented. These states evolve for high enough out of unstable fragmented states, which themselves appear in pairs with the stable fragmented states at the onset of fragmentation. As we will see below, partially fragmented states exist in the large population limit too, though in a limited region of parameter space. In the small system here they are unstable. Intuitively this is likely to be due to the smaller number of trades: in the large limit of a partially fragmented fixed point, there will be at most one trade per trading period (only two out of the three agents going to one market will be able to trade) while both fragmented and coordinated states lead to two trades.

IV Large population limit

IV.1 Population with a fixed buying preference

In studying systems with a small number of agents we have already encountered a rich phenomenology: coordination of agents at a single market, pairwise fragmentation across two markets and even some mixed states where one group fragments while the other specialises in trading at a single market. We now complement and generalise these results by investigating the possible types of steady state in the large population limit. We start with a simple setting, a population in which all agents have identical preferences for buying . The assumption of population homogeneity is a strong one, but these traders still undergo fragmentation for a broad range of parameters, while the system is simpler to analyse. Thus it is a useful prelude to the analysis of a population consisting of two or more groups with distinct buying preferences.

To describe the steady states of such an initially homogeneous agent population we follow the distribution of attraction differences () across the population Alorić et al. (2016). The state of each market enters via the probability with which buy () and sell () orders are executed successfully Alorić et al. (2016); Alorić (2017):

[TABLE]

Here the factors are the probabilities for submitted buy/sell orders to be valid, i.e. on the right side of the trading price; the explicit expressions are given in Appendix A). Note that whereas for small systems we simplified to deterministic order prices, we return here to the full model where bids, , and asks, , are stochastic and the trading price is calculated as in Eq. 3. (As explained in Sec. II we choose Gaussian distributions for bids and asks, and ; for numerical evaluations we set , ) The are demand-to-supply ratios, defined as the number of buyers over number of sellers at market . For small , the attraction difference distribution evolves according to a Fokker-Planck equation

[TABLE]

where the drift and diffusion both depend on the buying preference of the agents and on the four trading probabilities . (We use as the generic label for a combination of order type and market choice .) The drift term is (see Appendix A for details and for the explicit expression of the return distribution from which is calculated)

[TABLE]

where the sum runs over markets and order types and we use the convention . The strength of the diffusion term is

[TABLE]

The steady state of the Fokker-Planck equation is (see e.g. van Kampen (1992)):

[TABLE]

where

[TABLE]

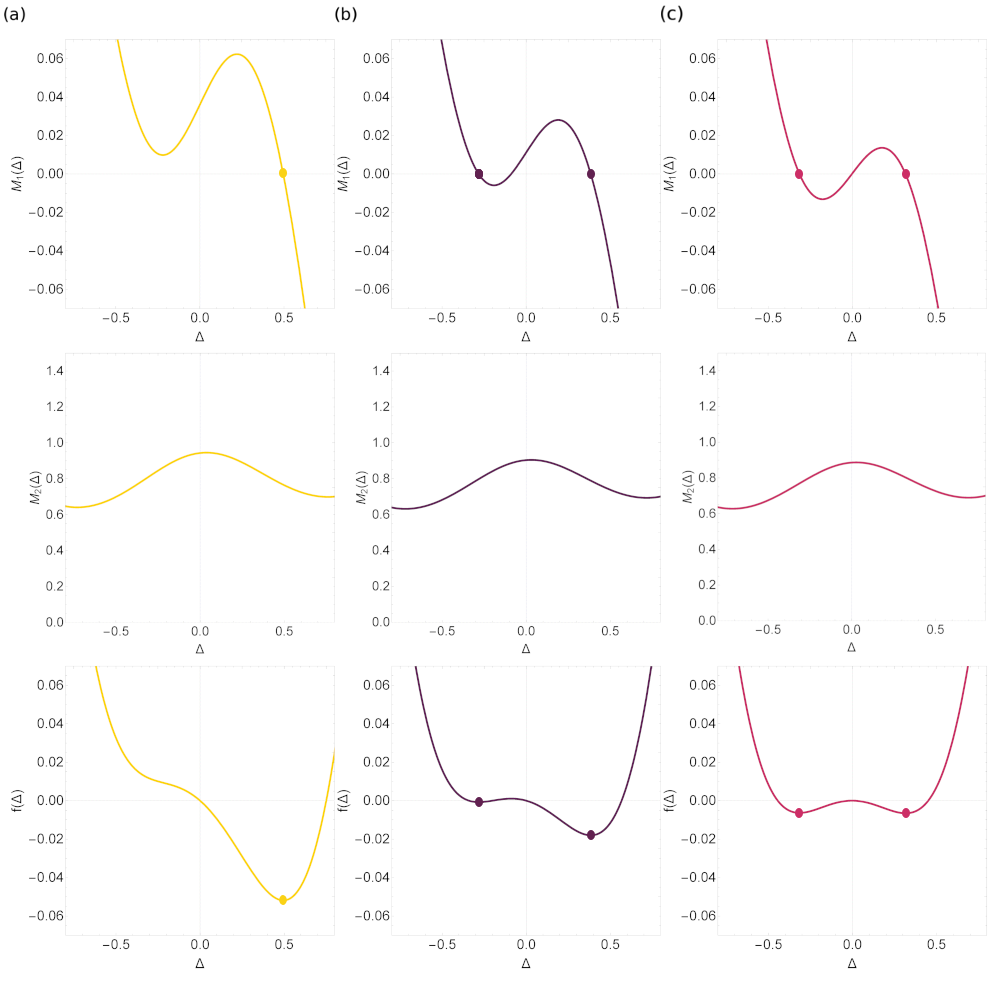

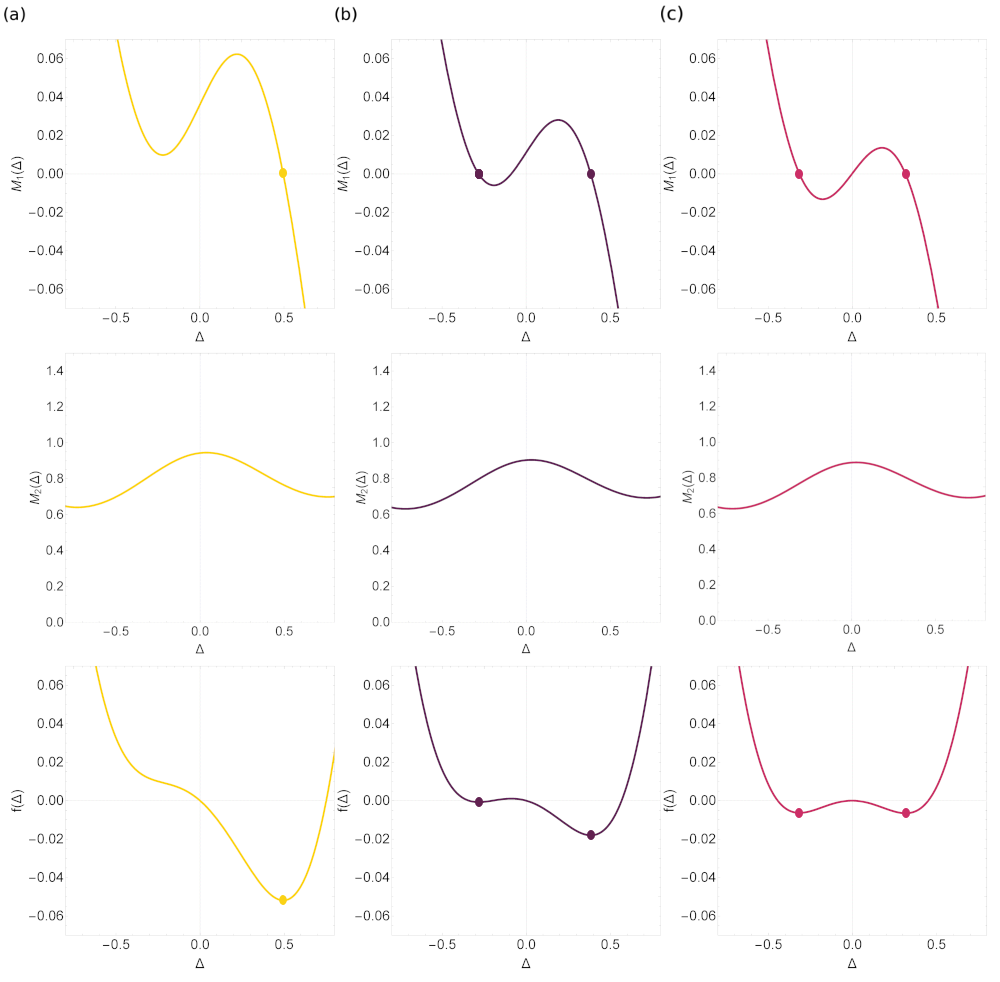

plays a role analogous to a free energy in thermodynamics. When has a single minimum, will approach a narrow peak at this location for and we have an unfragmented state. Otherwise as many peaks as there are local minima in will appear, corresponding to a fragmented state: each peak represents a subgroup of agents following a distinct market choice strategy.

Note that in the Fokker-Planck description, the market order parameters that determine the trading probabilities have to be calculated self-consistently from Alorić et al. (2016); Alorić (2017). The same self-consistency condition then also needs to hold at a steady state. Initially we will treat the order parameters as fixed exogenously, however. Such a situation could arise if, for example, our agents are just a very small fraction of the overall trading cohort, with the latter fixing the demand-to-supply ratio.

Fragmentation for

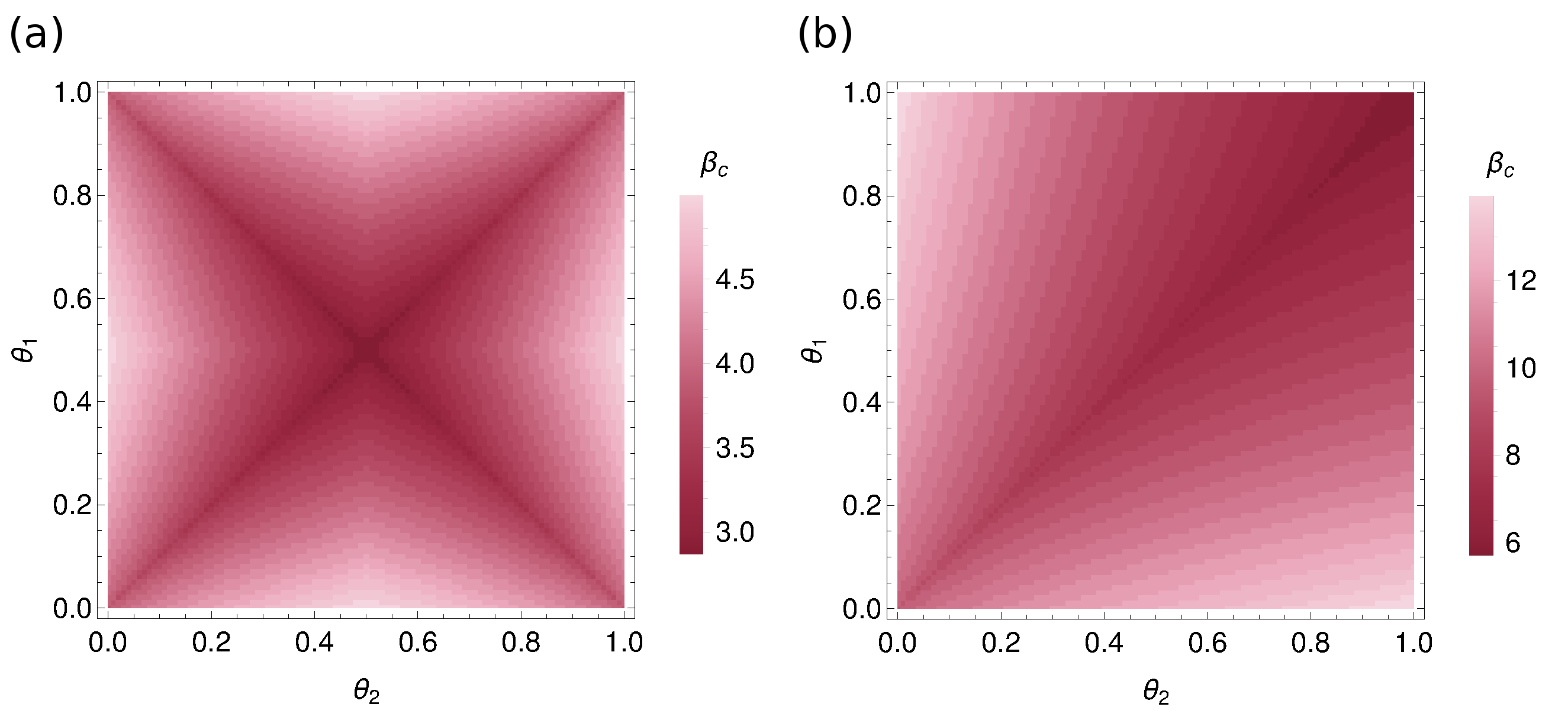

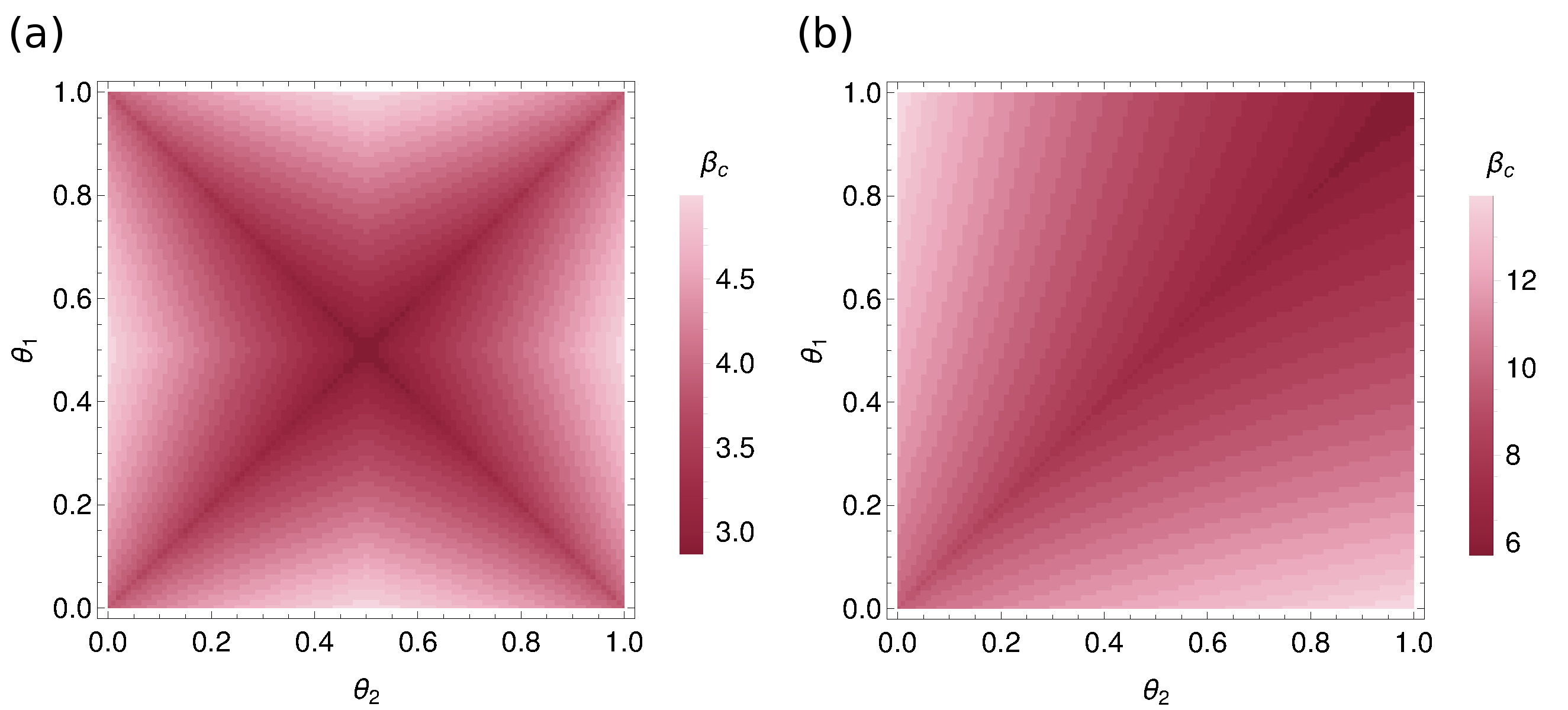

In Figure 6 we show how the treshold value of the intensity of choice depends on the market biases for different agent populations, one “indecisive” () and one made up of “decisive” buyers (); for this calculation we set the order parameters to their “endogenous” value following the self consistent procedure outlined in (19). We see that for every pair of market biases there is a finite threshold above which fragmentation sets in. When agents are indecisive with regards to buying and selling, the region where fragmentation occurs is greatest when markets are identical or symmetrically biased. For decisive buyers (), on the other hand, the fragmentation threshold is lowest when the markets are identical. Intermediate values of provide a smooth interpolation between these two situations.

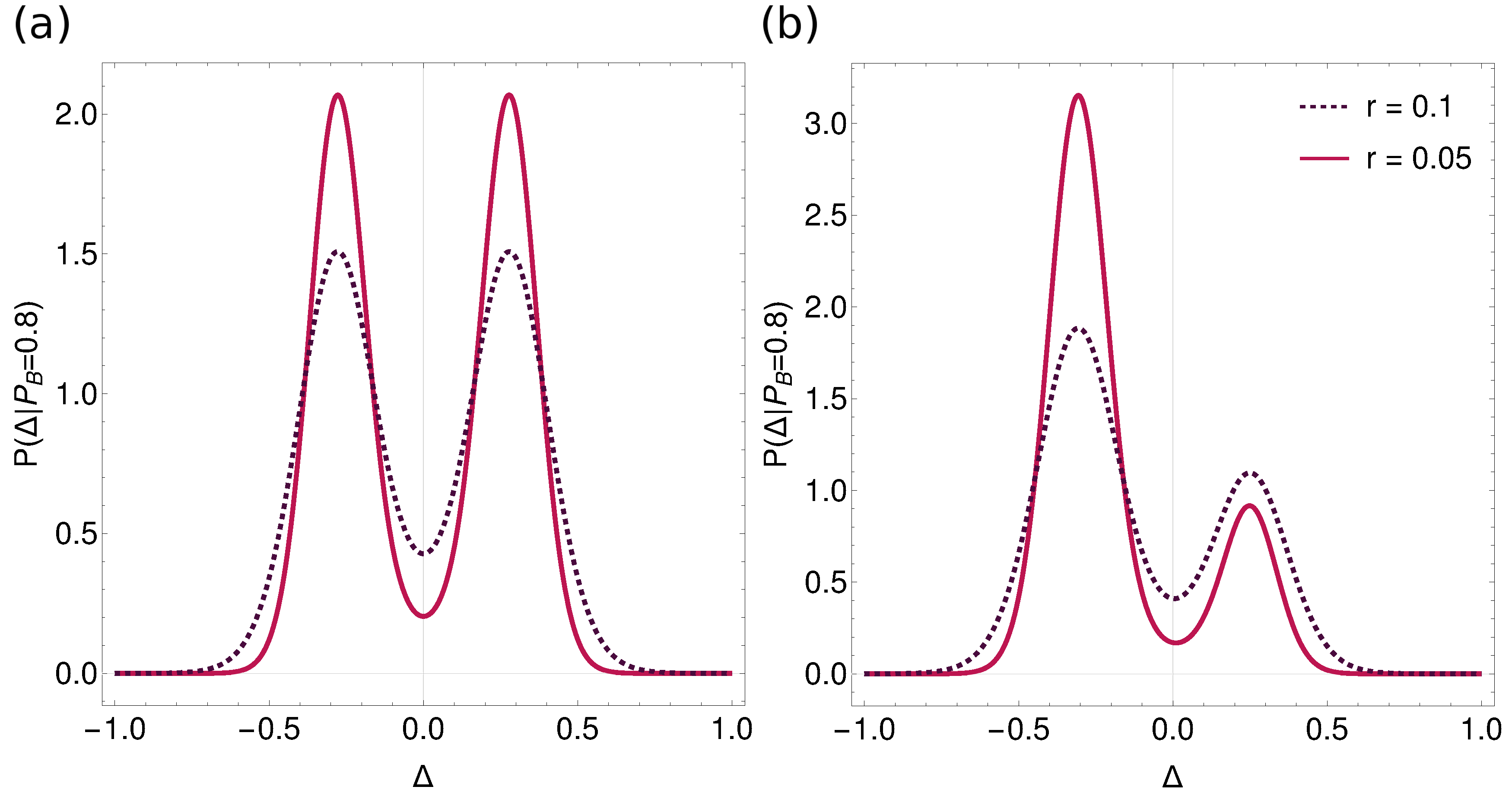

To understand more closely the properties of the fragmented states, we show in Fig. 7 the steady state distributions of traders with when faced with the choice between two unbiased or two symmetrically biased markets. To understand the trend with , we show the distributions for two different values of in each case. As expected from (14) the peak width decreases as with decreasing , but in Figure 7 (b) we see that the relative peak heights also depend on . In fact, if the peaks are located at attraction differences and then the peak height ratio can be written as

[TABLE]

This ratio can stay finite for only when

[TABLE]

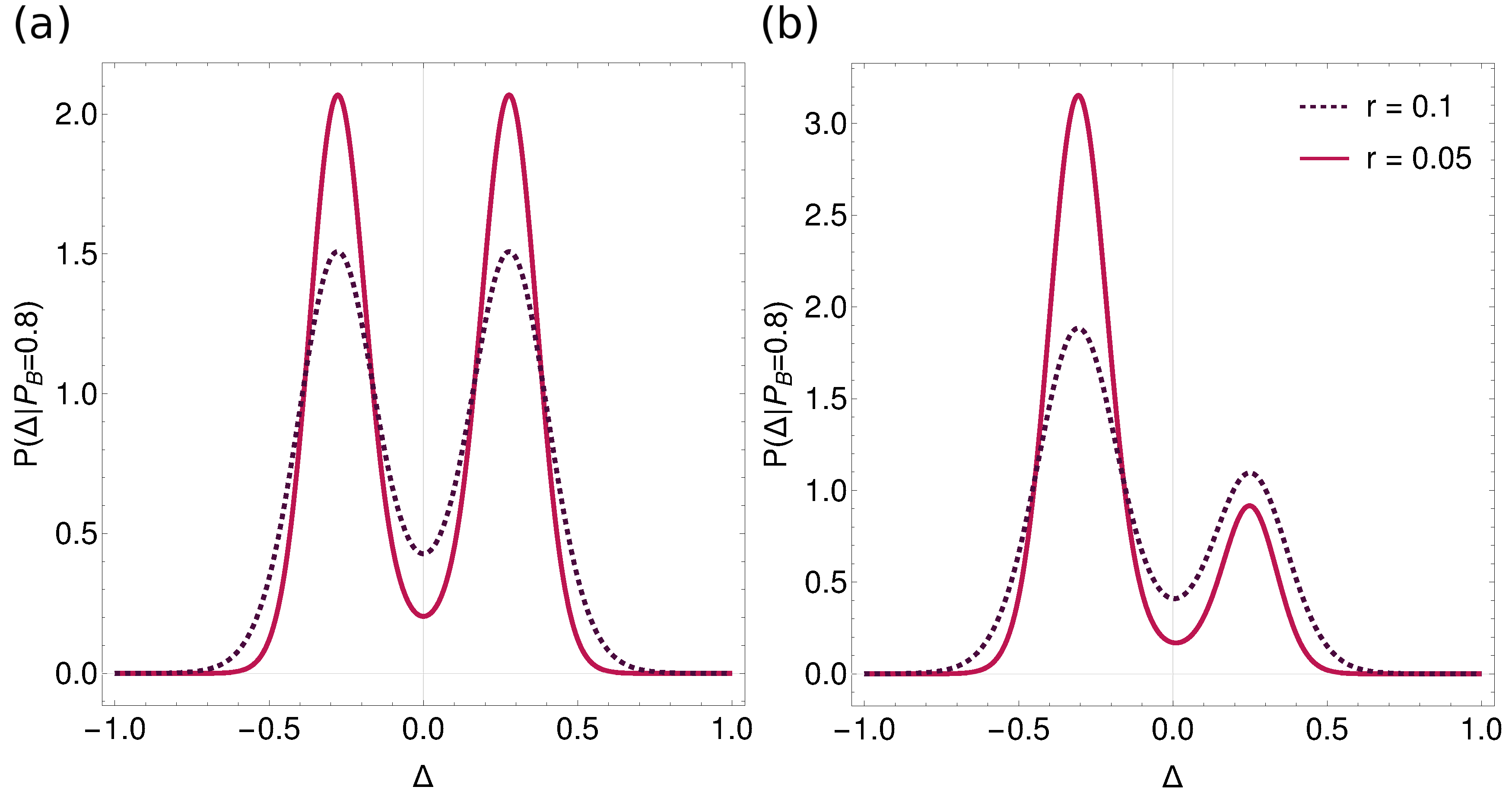

and we call this situation strong (S) fragmentation as it survives even in the limit. This is the situation in Figure 7 (a). If the free energies at the two peaks are unequal, on the other hand, one continues to have two peaks in for any nonzero but the height of one peak decreases (exponentially in ) as goes to zero. We call this behaviour, which is illustrated in Fig. 7 (b), weak (W) fragmentation because the lower peak may become unobservably small for low ; in the strict limit , the distribution becomes unimodal again. The strong-weak distinction as defined applies literally only to this limit; at nonzero it becomes a crossover between fragmented states where the emergent subgroups have roughly even (strong) or very different (weak) sizes. At the weakly fragmented state most of the trades happen at a single market (increasingly so as decreases) we relate this state to market consolidation, thus the question of fragmentation versus consolidation becomes question of strong versus weak fragmentation in our set up.

Now that we have a method for finding steady states and classifying them we return to the space of market order parameters and investigate where fragmentation occurs. In Figure 8 we show where weakly (coloured region) and strongly (solid lines inside these regions) fragmented states appear, at a fixed intensity of choice . We compare again indecisive () and decisive buyers (), for three different market setups. We first note that the weak fragmentation region encompasses a very wide range of market conditions (order parameters ) for indecisive buyers, but shrinks significantly when the agents have stronger preferences for buying. Looking at the dependence on market setup, an obvious feature is that for two unbiased markets (shown in (c)), equal demand-to-supply ratios ( line) produce strong fragmentation for both types of agents. This makes sense as the markets are then identical both in their setup and in the prevailing market conditions, making it easy for groups of agents with opposite market preferences to coexist. For the indecisive agents who will act as buyers or sellers with equal probability, the same situation arises when the markets have exactly opposite demand-to-supply ratios () and therefore still offer them identical average returns.

With increasing market biases (Figure 8, (a) and (b)) the picture obtained for two unbiased markets changes largely smoothly, though note that for decisive buyers (top row) the two crossing lines of strong fragmentation detach into two separate lines ((b) top), with one eventually disappearing out of range.

Market order parameters.

So far we have looked at fragmentation behaviour driven by exogenously set market conditions (demand-to-supply ratios). We now return to our model as originally set out, where only the adaptive agents we describe trade at the two markets. This leads to the question: will a population endogenously create market conditions needed for its fragmentation?

For the case of traders with homogeneous buying preferences this question can be answered relatively straightforwardly. If the steady state distribution of attraction differences is , then the fractions of the whole population buying and selling at market are:

[TABLE]

The demand-to-supply ratio then does not in fact depend on the market preference distribution

[TABLE]

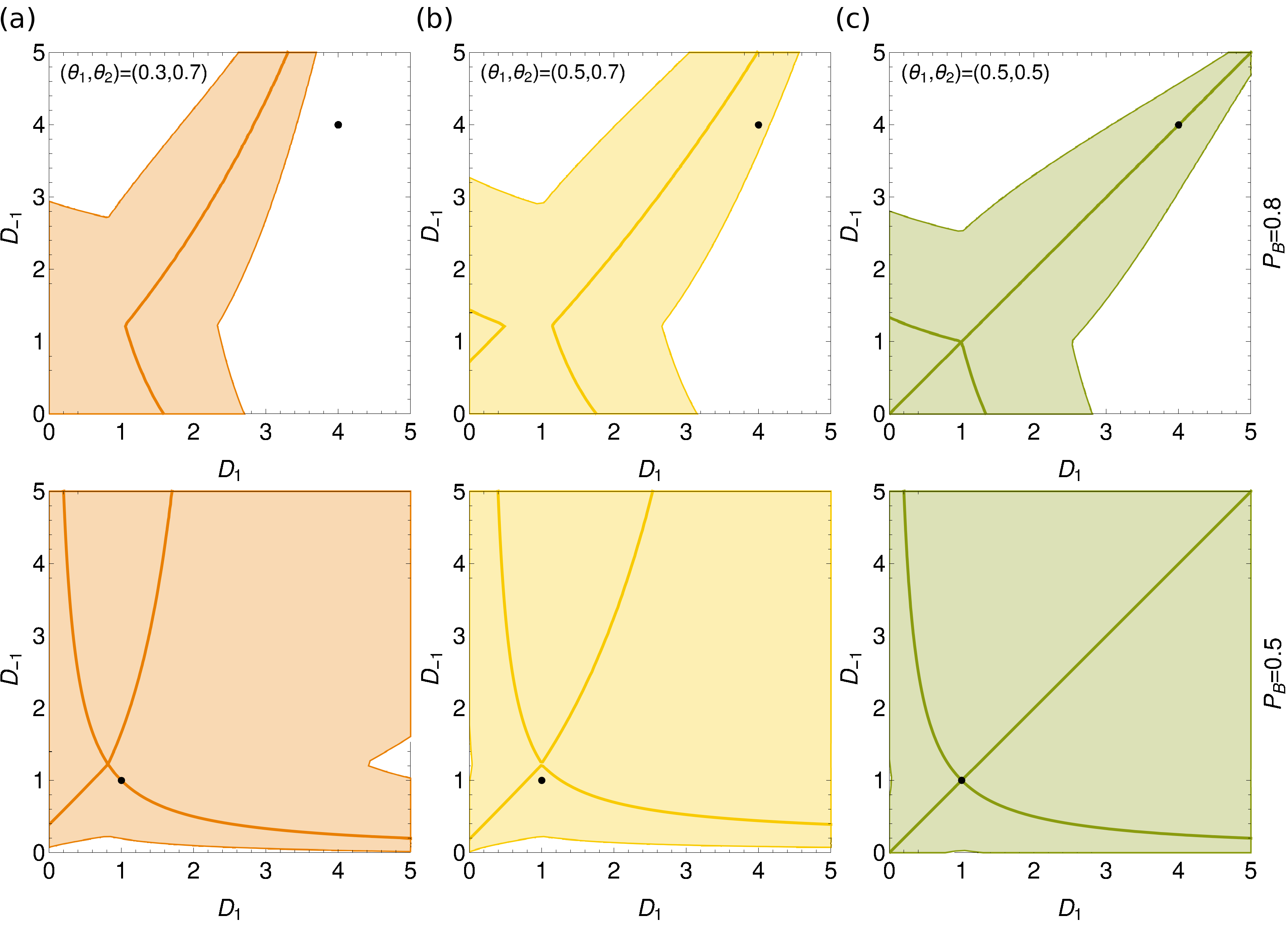

and is fully determined by . In the space of market order parameters in Figure 8, this endogenous set of market conditions is marked with a black dot. We see that – at high enough – the population of indecisive buyers fragments strongly when the markets are unbiased or symmetrically biased, and one can check that these results hold independently of the specific market biases used in the figure. Decisive buyers, on the other hand, fragment strongly only if the markets are equal (the figure shows only but the statement is true for general ). Otherwise weak fragmentation occurs, although – see Figure 8 (top (c)) – when the markets are very different at a above that used in Figure 8.

With these insights it is worth revisiting Fig. 6. It shows the existence of the fragmentation threshold for all market biases, and we recall that this threshold is defined as the point where first acquires two peaks. From what we have seen above we now understand that for most combinations of market biases, the steady state one finds above is a weakly fragmented one. The exceptions are the dark lines in Fig. 6, which indicate equal () or symmetrically biased () markets.

V Two group population

So far in our analysis of the large size limit of a homogeneous population of traders with buying preference , we showed how for any given pair of market order parameters we can determine the population steady state. We identified three possible types of steady states: unfragmented (U), weakly fragmented (W) and strongly fragmented (S). We now generalise the investigation to populations of agents consisting of groups with different buying preferences. We demonstrate the approach for the case of two groups of the same size, but the principles are general and can be extended to larger numbers of groups or different group sizes. We denote a steady state of a population consisting of two groups with a pair of letters (X,X’). Here X,X’ U,W,S indicates the type of steady state for each group, producing nine different types of population steady states.

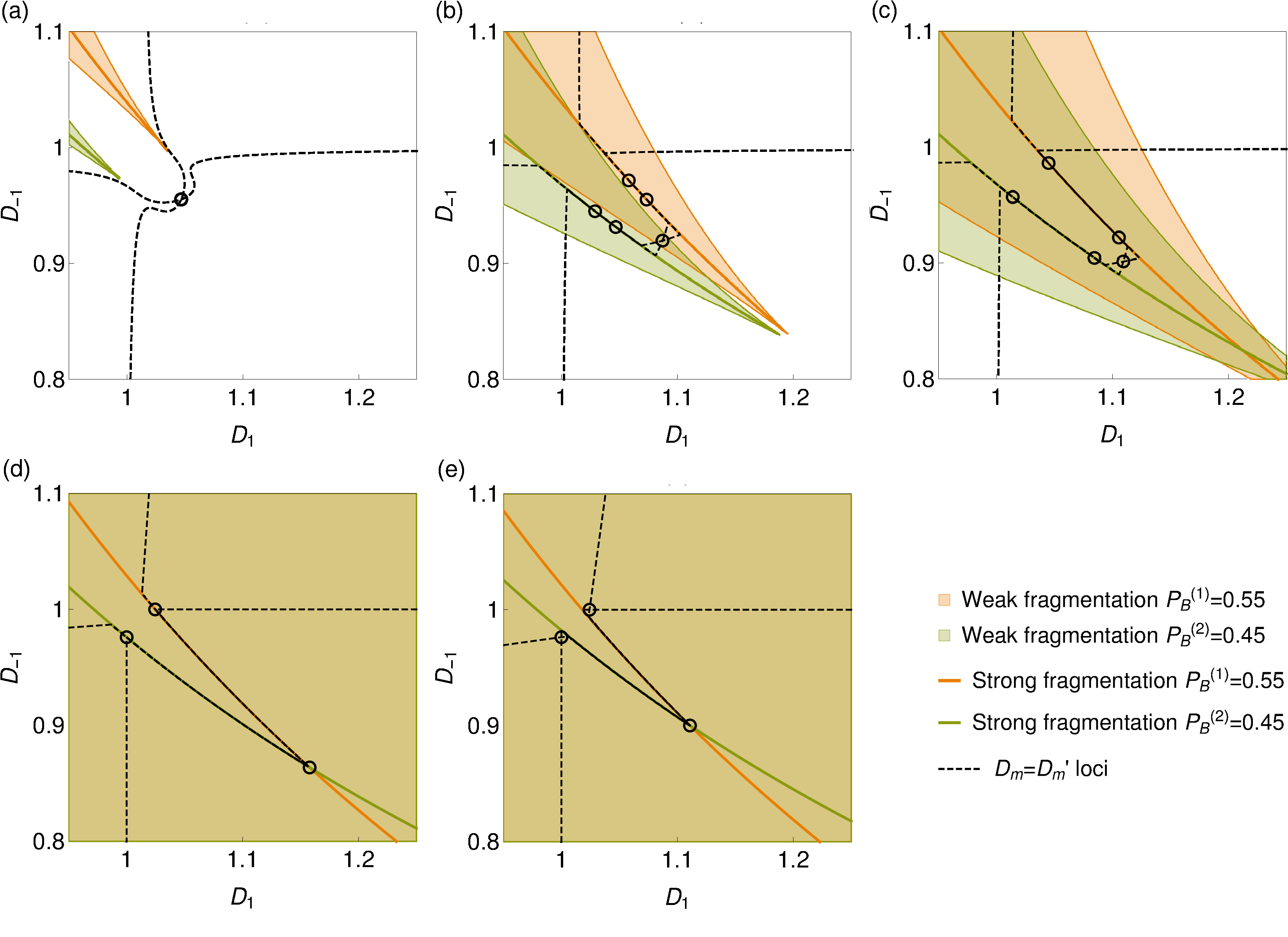

We can now find, in the space of market order parameters , the domains of different state types as we did in Figure 8. We can use the figure directly to read off the steady states at of a population of two groups with buying preferences . For example, when the market order parameters are (the top right corner of all the diagrams), the steady state of the two group-population is (U,W) when the markets are symmetrically biased or biased/unbiased (Fig. 8 left and centre) and (S,S) when both markets are unbiased (right diagrams). This simple analysis can be extended to any number of groups because, for market order parameters that are fixed exogeneously, the groups are independent.

Our primary interest, however, lies in the case of endogenous market conditions where the agents we model capture the entire trading population and thus define their own market order parameters. In this case, we need to find the steady states self-consistently. We have previously described a procedure for doing this, for nonzero Alorić et al. (2016): starting from some initial market order parameters one calculates the steady states and updates iteratively, converging eventually to a self consistent set of order parameters. Here we aim to get a complete picture of all possible steady states, independently of initial conditions. To do this, we start from the update equation for the market order parameters from the iterative approach. These are simply the definitions of the market order parameters (Eqs. 18,19) extended to two groups:

[TABLE]

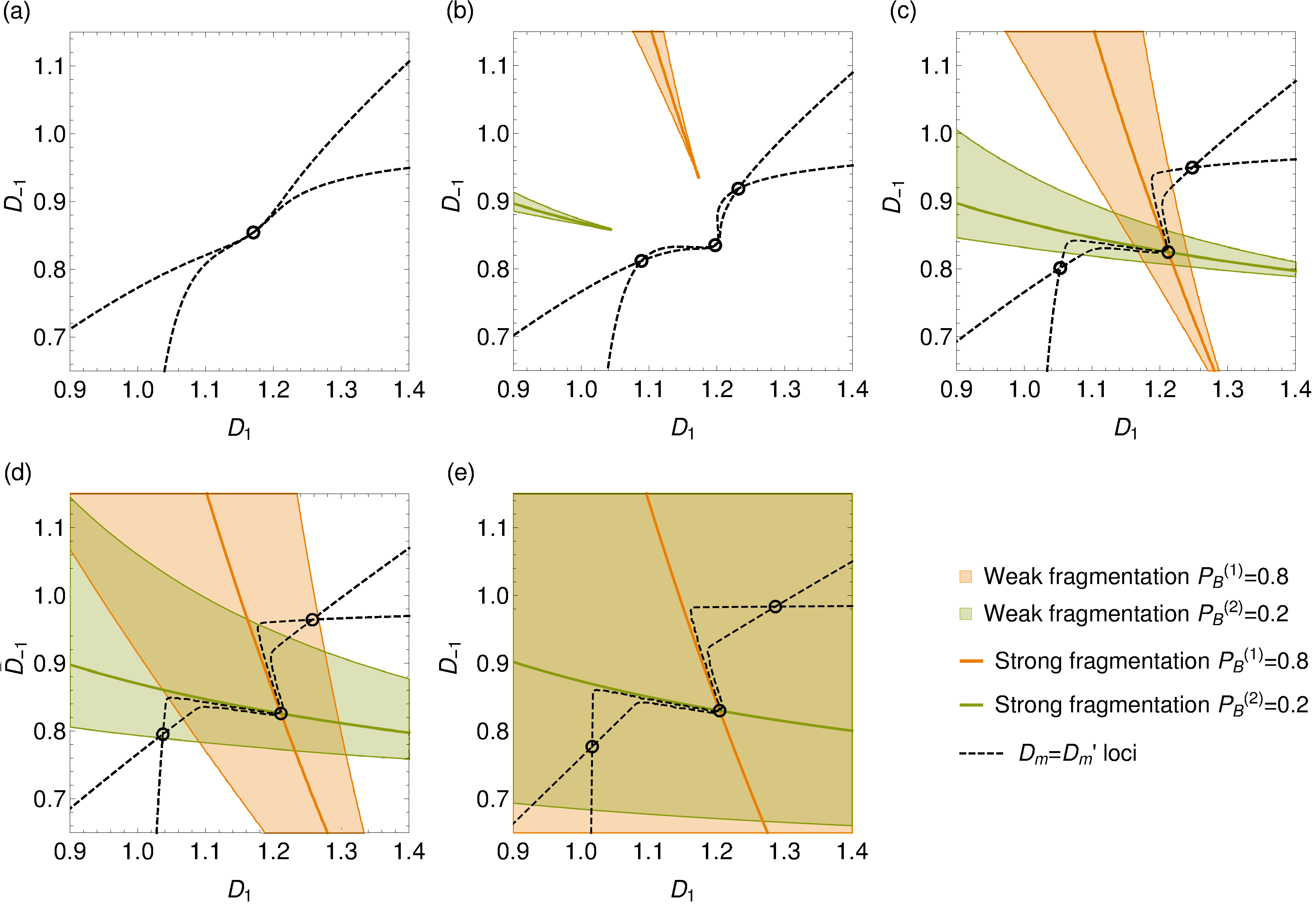

We can now define, in the market order parameter space, the two loci where and , respectively, meaning that one of the order parameters is already self-consistent. The intersection of these loci (two lines, for our case of two markets) then gives us all the self-consistent sets of market order parameters. To distinguish weak and strong fragmentation the limit ought to be taken. To avoid numerical issues we use here instead a small nonzero to determine the attraction difference distributions from which the are calculated. In most of what follows we focus on symmetric market setups () and symmetric agent buying preferences (). To avoid having too many parameters to vary we will fix the market biases to the default values ()=(0.3,0.7) unless stated otherwise.

V.1 Transitions in populations of decisive and indecisive traders.

As shown in previous sections, the intensity of choice is a crucial parameter determining whether the steady state in a system is fragmented or consolidated. Here we build upon this analysis by investigating how the nature of steady states changes as is increased. We start this section with examples of steady states of a population with “decisive” traders as well as one with largely “indecisive” traders . We then generalize these results to a full phase diagram for the limit, giving the number and type of steady states as a function of the intensity of choice and the buying preference .

V.1.1 Decisive traders.

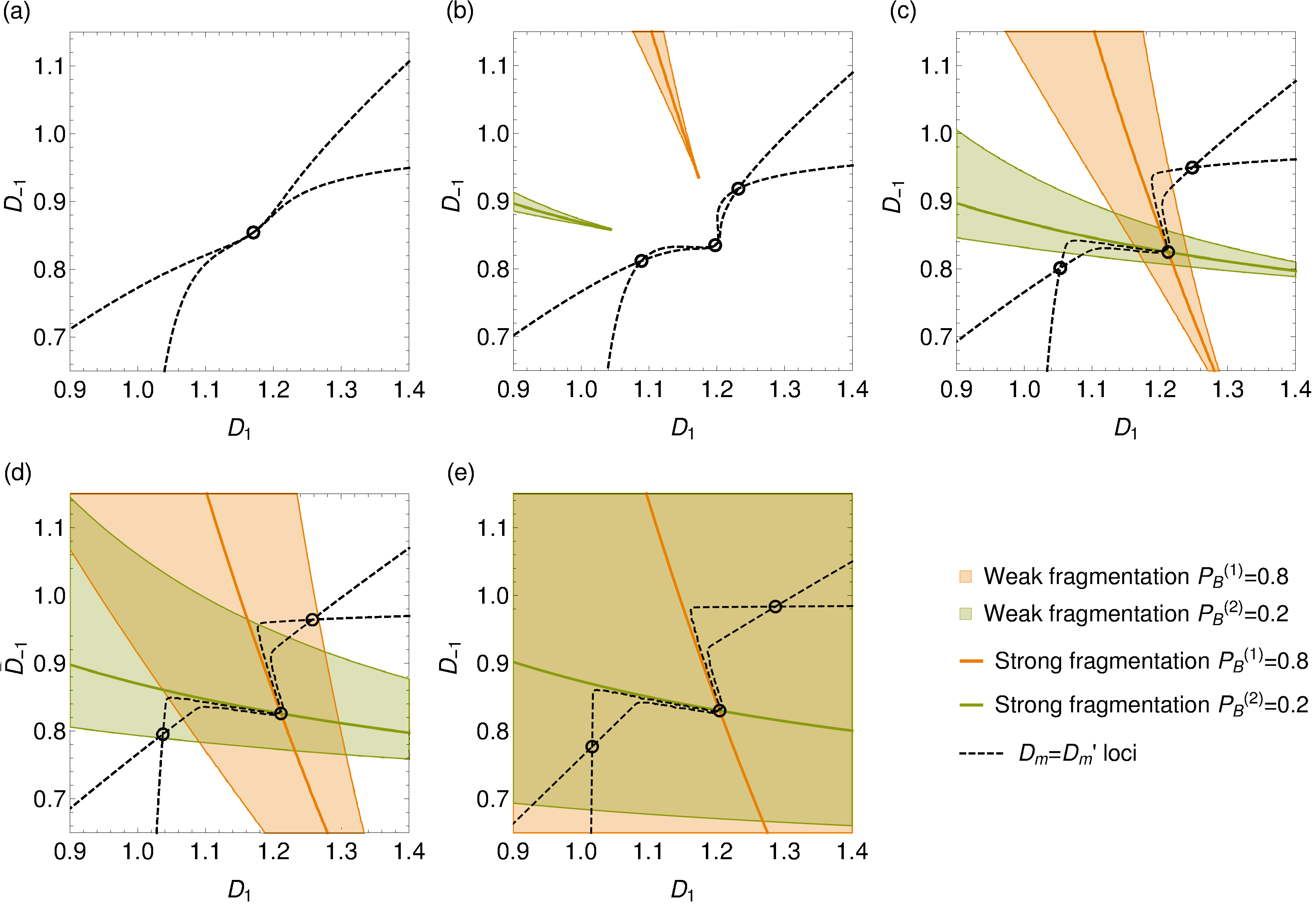

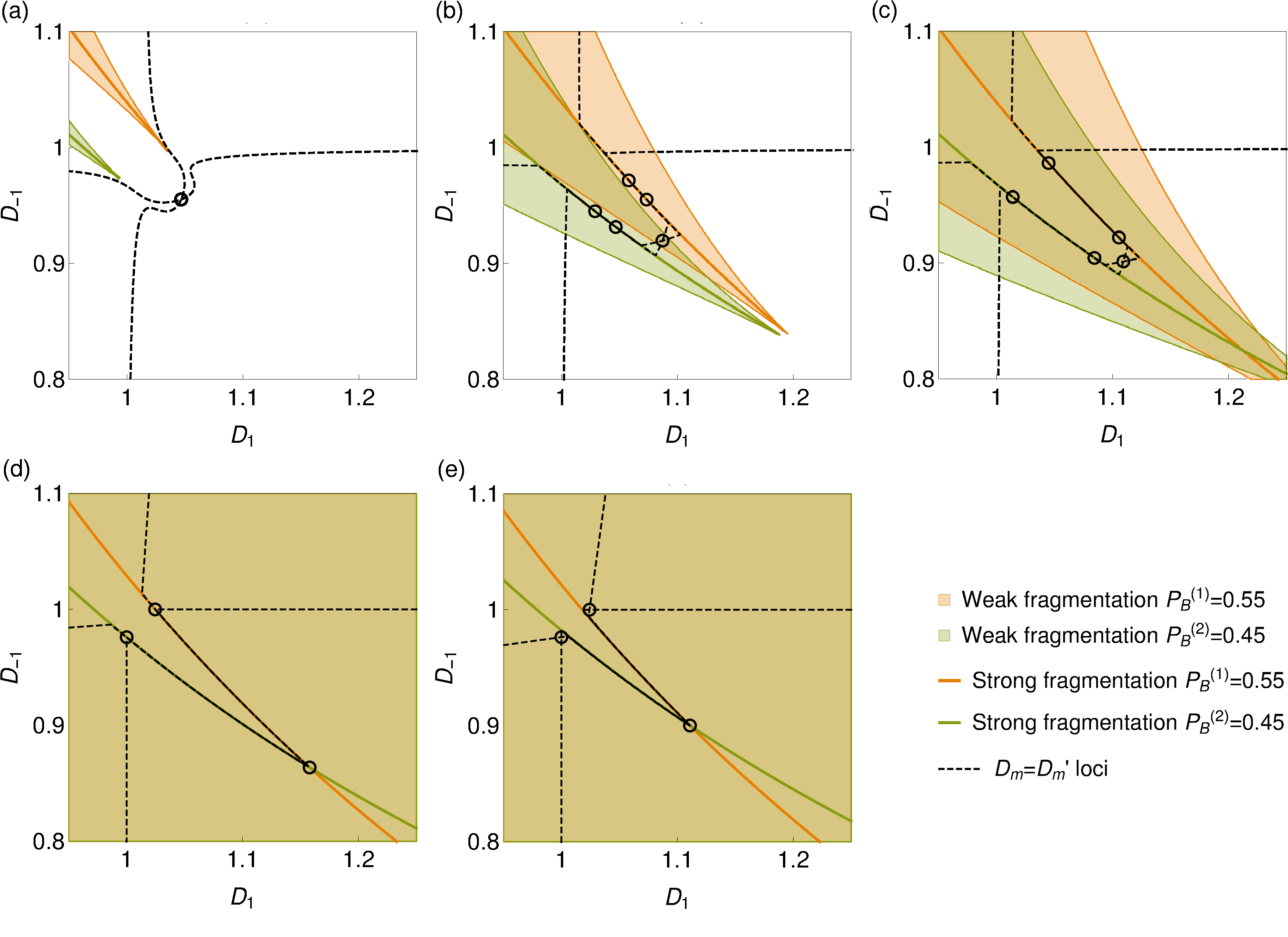

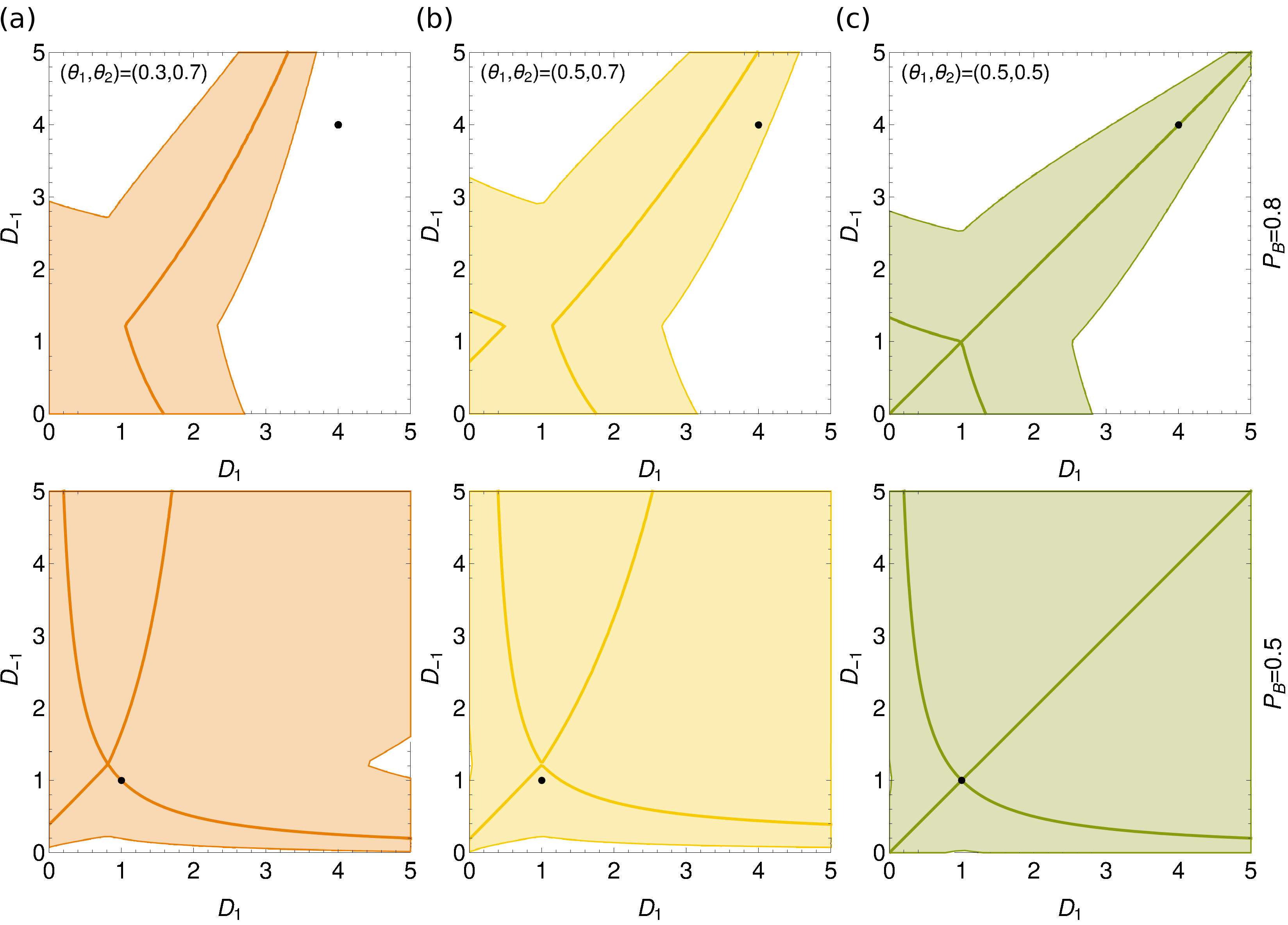

In Figure 9 we show, for a series of different , the market order parameter space with the weak fragmentation region and the strong fragmentation line marked for both groups of a population with . The order parameter self-consistency lines are also shown.

In panel (a) of Figure 9, we show the low regime (), just before the onset of fragmentation. Note that for this , the steady states of both groups are unfragmented across the entire range of market order parameters shown. The unique intersection of the loci identifies a single steady state of type (U,U). Panel (b) shows a just slightly increased where most market order parameters settings still give unfragmented states but there are now three intersections of the self-consistency loci, giving as many (U,U) steady states. In the steady state that is a continuation of the low solution the agents show only mild preferences among the markets, with buyers slightly preferring the market that gives higher returns for buyers and similarly for sellers. The other two unfragmented solutions correspond to coordination at one of the two markets so that overall the situation is similar to the one we saw for and .

Increasing further (Fig. 9(c)) one crosses the threshold ( here) where one of the unfragmented solutions first fragments – the continuation of the low state is now in the strongly fragmented domain of both groups, while the other two steady states remain unfragmented. Note that since the weak fragmentation regions surround the strong fragemtation lines for both agent groups, there must in fact be a narrow range of slightly lower -values where the fragmentation is weak: the low- solution must change from (U,U) through (W,W) to (S,S) as increases.

In Fig. 9(d,e) one observes that with increasing the fragmentation regions keep growing. This results in the two unfragmented (U,U) solutions changing first into (U,W) and finally (W,W).

We note that inferences about stability from diagrams like Fig. 9 are in general unwarranted; e.g. the initial pitchfork bifurcation from one to three (U,U) states in Fig. 9(a,b) does not necessarily imply that the middle solution is unstable. It would be unstable under repeated updating from to . However, Eq. (20) shows that this is not the real dynamics but would correspond to a scenario where the dynamics of the order parameters is slowed down artificially so that agents always have time to equilibrate their attraction difference distributions to the current order parameter values.

We highlight one further feature of Fig. 9: for small as used in the figure, the order parameter self-consistency lines tend to follow segments of the strong segregation lines before emerging on either side into a weak segregation region. This can be understood by noting that the self-consistency line for e.g. is the zero contour of the function in the order parameter plane. This function varies steeply as a strong segregation line is crossed, developing discontinuities that look like cliff edges for . A contour line that hits such a cliff must follow the line of the cliff before returning to the smooth parts of the landscape, which is the effect we see in Fig. 9.

The cliff edges themselves arise because on a segregation line, the free energy function in Eq. (16) has two minima of equal height. A small change of in or will cause similar small changes in the height of these minima, but from Eq. (16) this is enough to cause the weight ratio between the two peaks in to shift by a factor of order unity. Changes larger than this will transfer all weight from one peak to the other, and correspondingly modify by a finite amount. For the required order parameter changes become infinitesimal, leading to the cliff edge structure of and analogously .

V.1.2 Indecisive traders.

We now compare the results above with those for a population consisting of two agent groups with only weak preferences for buying and selling, . The motivation for this comes from the fact that agents with only mild buy/sell preferences should develop weaker preferences for markets that offer higher returns for buyers or sellers. They will also not be penalized much if only a single group populates a market, as such an arrangement will still sustain a large number of trades.

In Figure 10 we observe several differences compared to the situation in Figure 9 for decisive traders, most notably with regards to the number of solutions. Specifically, as can just be discerned from Figure 10, on crossing the fragmentation threshold four new states appear. These states are also different in nature: they are partially fragmented in the sense that one group of agents is strongly fragmented and thus retains a bimodal distribution of attraction differences for while the other is either weakly fragmented or unfragmented. We have seen a similar state in the systems with four agents although there it was unstable because it reduced the number of possible trades. In the large population limit, having one fragmented and one unfragmented group of agents still leaves many possibilities for trading, especially for indecisive agents where roughly half of each group of agents will probabilistically assume the role of buyer or seller in each trading round. On the general grounds discussed above, the appearance of the partially fragmented (U,S) states is expected to proceed via (U,W) states, though again the -range where the latter appear is numerically small.

When the intensity of choice is increased beyond that in Fig 10(a), the low- solution transitions from (U,U) to (W,W) (panel (b)) and eventually (S,S) (panel (d)), i.e. both agent groups fragment first weakly then strongly. Comparing the partially fragmented solutions in panels (b) and (c) we see that they change from (U,S) to (W,S); finally two of them merge with the uncoordinated (W,W) state into an (S,S) state. The other two partially fragmented states eventually transition into (W,W) states; as in the case of decisive traders, these represent coordination of the agents at a single market.

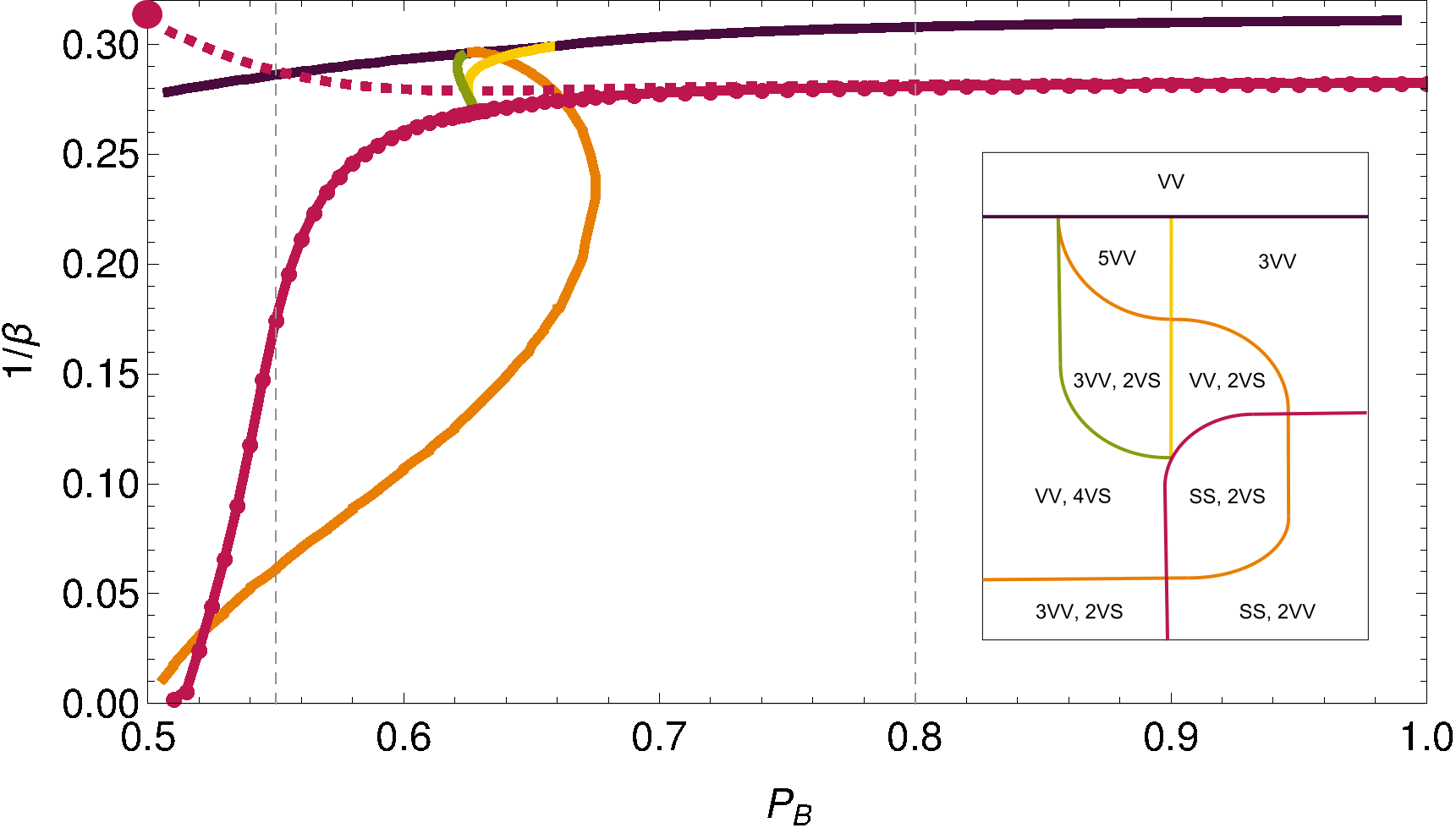

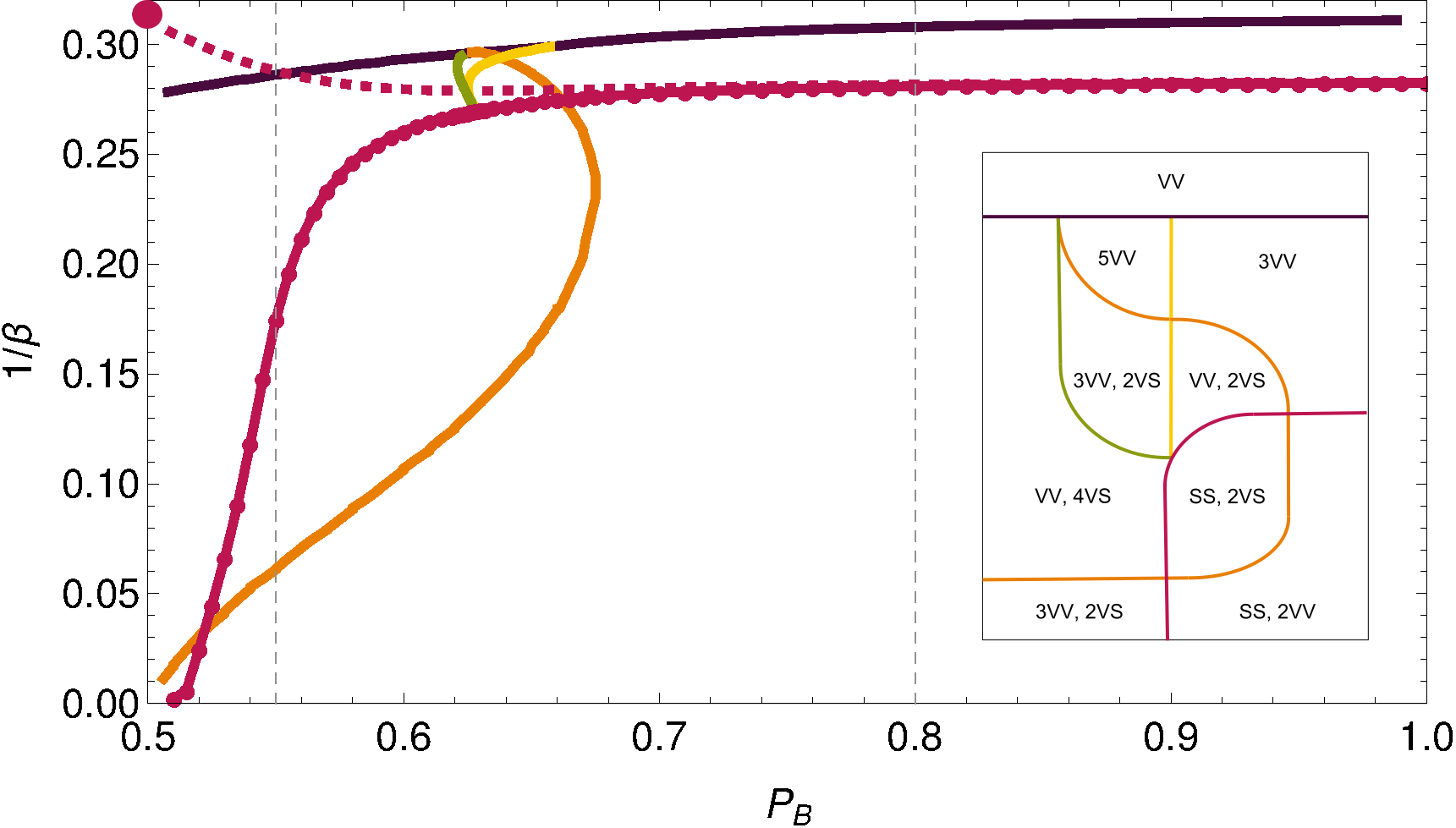

V.2 Phase Diagram

We have observed both market consolidation and fragmentation when a population is faced with a choice of two symmetric markets, depending on the different choice of system parameters (). We next vary these parameters systematically to construct a detailed phase diagram and study the regions where one finds the various states that we described above. The size of these regions then also gives an indication of how typical the different scenarios are. We continue to focus on symmetric markets with but note that calculations for other (symmetric) market settings give qualitatively similar results. In Figure 11 we show the phase diagram in the space of intensity of choice and group preference for buying . This diagram is the large population analogue of the diagram for four agents () shown in Fig. 5. There we had identified regions with states that are unfragmented and indecisive (low ), unfragmented and coordinated, fragmented, and partially fragmented. Broadly these types of states persist in the large population limit, but they have additional structure that makes for a richer phase diagram.

To help visualize the structure of the phase diagram, we show an additional version as an inset that has been distorted to preserve the topology but make even small regions in the phase diagram visible. Also, to avoid having too many separate regions we do not distinguish in the diagram between unfragmented (U) and weakly fragmented (W) states, which both have distributions of market preferences that become unimodal for . We label such states collectively V to separate them from strongly fragmented states (S) with their bimodal market preference distributions. Two vertical dashed lines mark the two scenarios of decisive and indecisive traders studied above (see Figs. 9 and 10).

We now look in more detail at the structure of Figure 11. Crossing any line in the phase diagram either changes the number of population solutions or the nature of the steady state for one or both agent groups. We note that due to the symmetry of the system we consider, many of the changes for the two groups happen simultaneously. In the insert, regions of the parameter space are laid out according to the number of solutions – five solutions on the left and three on the right, with a single solution in the small region at the top.

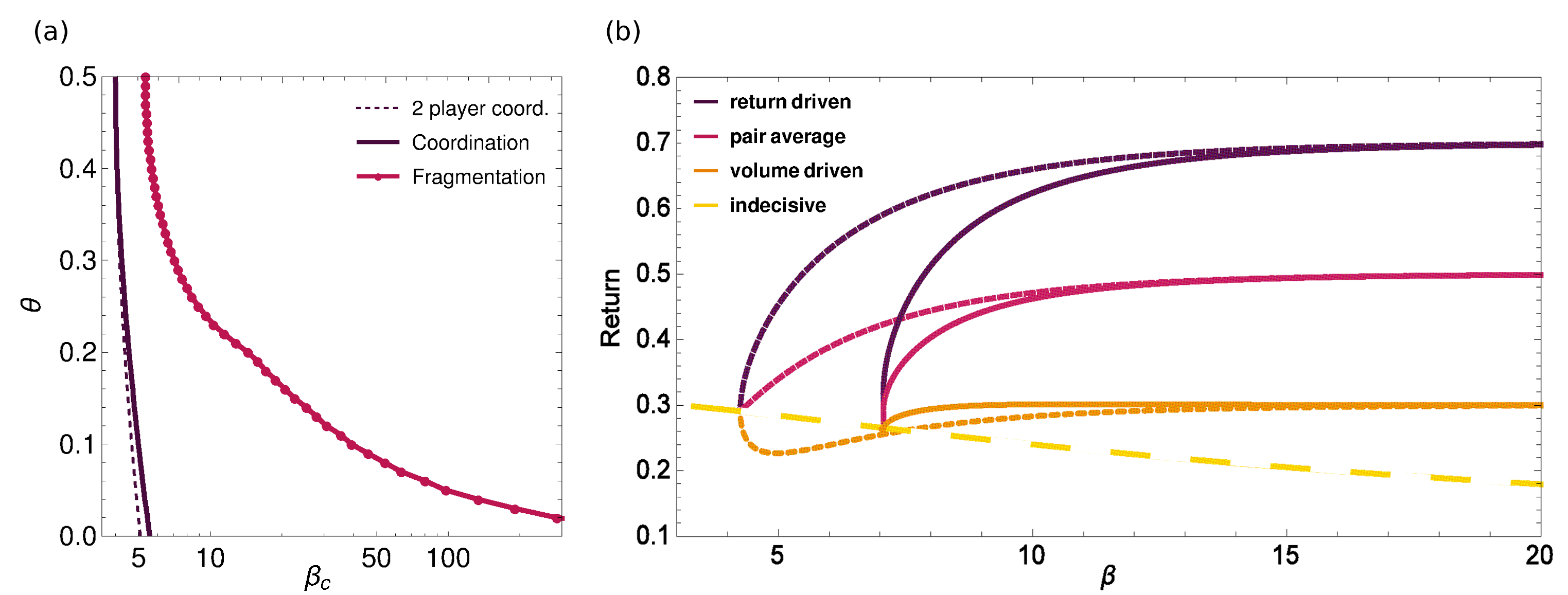

The dark violet line in Figure 11 is the line where the multiplicity of states changes from one to three or five. Looking at the order parameter self-consistency lines shows that this transition takes place via a pitchfork bifurcation in the former case, and two symmetric saddle-node bifurcations in the latter. The dark violet line is an analogue of the line shown in the same colour in the phase diagram (Fig. 5) of the system with players. The region of multiple solutions has grown for large , but the inverse critical intensity of choice is still an increasing function of .

As in Fig. 5, the pink line with circles in Figure 11 marks the appearance of a steady state where both groups are strongly fragmented. We observe that the critical intensity of choice where this happens diverges () as , i.e. the region of strong fragmentation shrinks as the difference between the groups’ buying preferences diminishes. Further lines in the phase diagram show where the solution multiplicity changes directly from three to five (yellow line), and where partial fragmentation occurs (green and orange line) as individual solutions transition from (V,V) to (V,S). Note that in the large population limit such partially fragmented states appear only for populations with moderate preferences for buying, in contrast to the system with agents (Fig. 5) where they exist for all .

We mark one further line (dashed pink) in the main graph of Figure 11, showing the transition within the small- (V,V) solution from the unfragmented (U,U) to the weakly fragmented (W,W) state. With this we make an explicit connection to results reported previously (Figure 7 in Alorić et al. (2016)) where we investigated the appearance of (weak) fragmentation with increasing intensity of choice. We note that for the system of our first case study the thresholds for weak and strong fragmentation almost overlap – the region of the weakly fragmented indecisive state is very narrow for this choice of parameters and in general for above , while it becomes larger for indecisive traders. The pink circle on the -axis marks the end of the weak fragmentation line. It turns out that this is the strong fragmentation threshold of the homogeneous population with even preference for buying and selling (), with the change from weak to strong fragmentation caused by the additional symmetry between the two groups for this value of .

Interestingly, there are two distinct regions in the phase diagram of Figure 11 where we observe three (V,V) and two (V,S) states, i.e. three unfragmented and two partially fragmented solutions. It turns out that in the region at lower (higher ) the partially fragmented solutions are coordinated, in so far as both groups of agents have an overall preference for the same market. For high one has the opposite situation, and it is those uncoordinated (V,S) solutions together with an unfragmented (V,V) solution that then merge into a single (S,S) state as is increased.

We note briefly that the various lines shown in Fig. 11 were detected by solution tracking, e.g. by carefully varying and tracking the number and type of solutions; further details can be found in Appendix B. The tracking approach is chosen as it is numerically faster and more reliable than the finite procedure we used in previous figures, avoiding e.g. the numerical noise visible in the two loci in Fig. 10. It is important to remember that the results only provide information about the existence of steady states, not their stability; the latter can be probed only using actual dynamics as discussed below. Fig. 11 also relates to fixed market biases so trends with changes in these biases cannot be seen; we have checked, however, that the overall structure of the phase diagram remains intact as long as market biases are symmetric. Quantitative trends were explored in our previous work Alorić et al. (2016), where we saw that the fragmentation region shrinks as markets become increasingly different.

In summary, the diagram in Fig. 11 shows that for systems with two symmetric markets and two groups of traders with symmetric buying preferences both fragmented and coordinated (or consolidated) steady states exist across a substantial range of values for the intensity of choice . Single market dominance happens when the steady state is either unfragmented or weakly/partially fragmented but coordinated: the majority of trades then happen at a single market. On the other hand, markets can coexist, receiving a roughly even share of trades, when the steady state is strongly fragmentated or weakly/partially fragmented but uncoordinated. In the former case both markets are visited by both groups while in the later case an effective market/group loyalty appears. In the following sections we analyse these different steady states further, with regards to the average population returns they produce and their stability in simmulated systems with finite and .

V.3 Average Population Returns

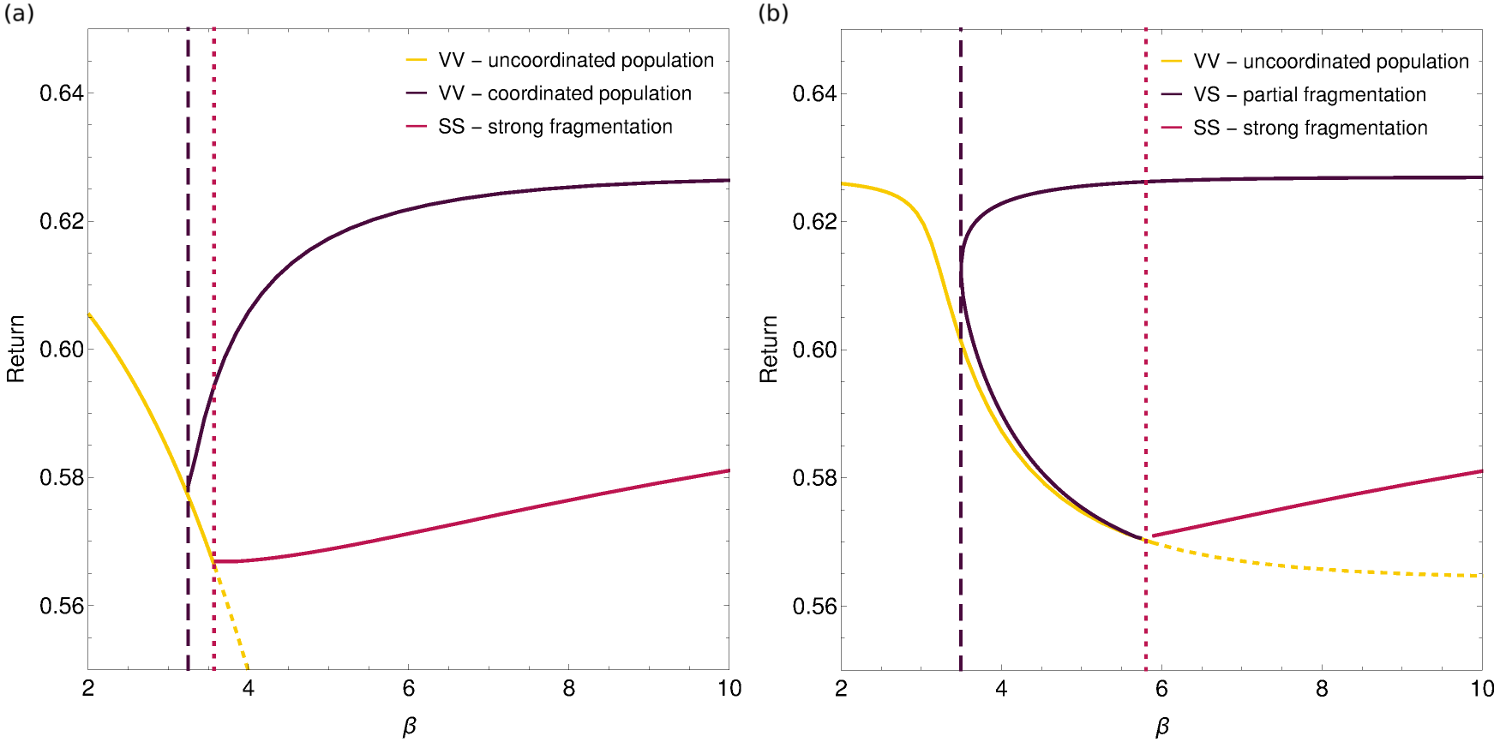

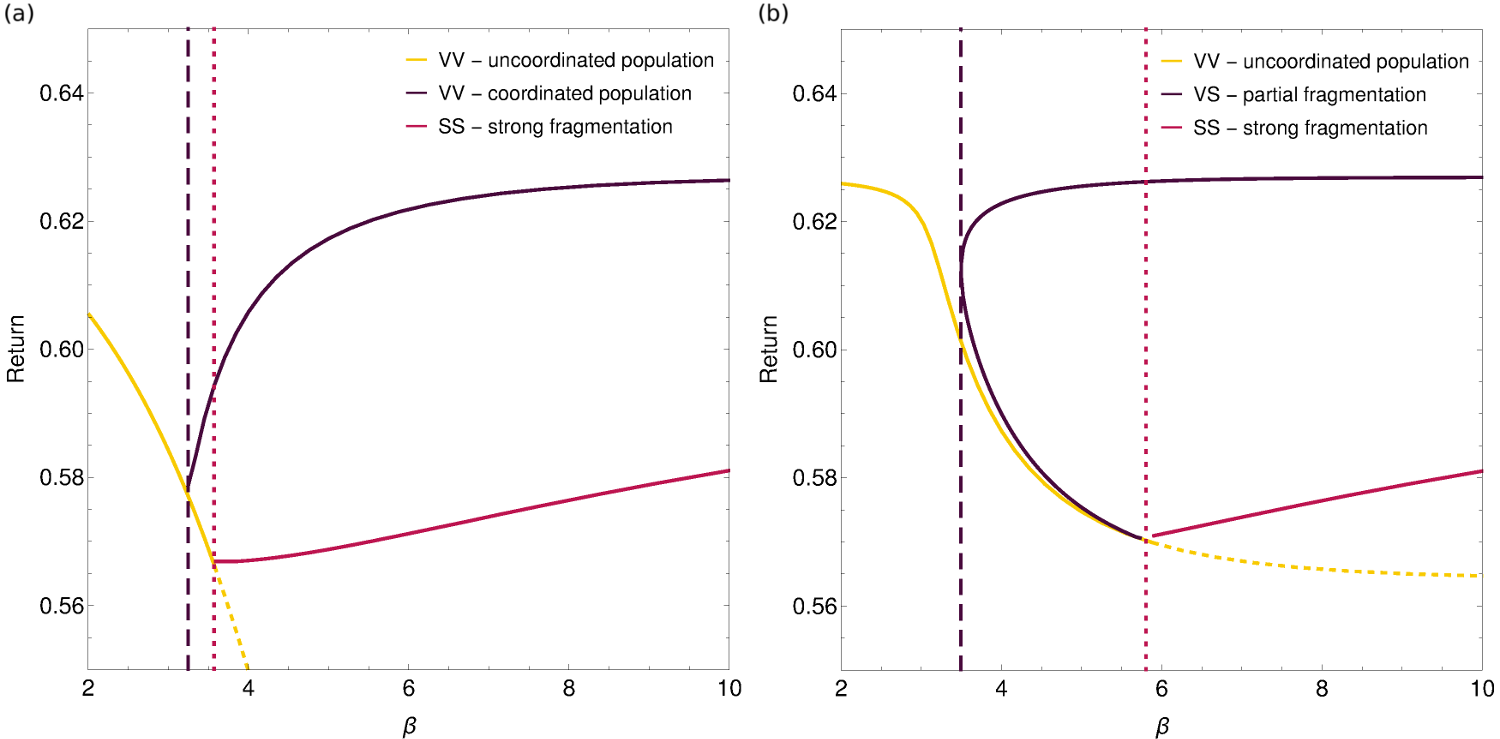

The phase diagram in Figure 11 reveals a plethora of possible steady states in the system of two markets and a large population of traders, depending on the traders’ learning parameter and their propensity to act as buyers . We now investigate whether these steady states induce differences in average population returns as we saw in small systems, e.g. Figs 2 and 4. We look at the average population return per trading round, where we count also zero returns that arise from an order being invalid or no trading partner being available.

In Figure 12, we show average population returns for the two scenarios of decisive (, panel (a)) and indecisive (, panel (b)) traders. The -dependences reflect the transitions between solution types we saw earlier (in Figures 9, 10 and the phase diagram Fig. 11). The overall trends resemble those for finite . First, we note that the return of the uncoordinated, low solution (marked in yellow in Fig. 12) is the lowest among the alternatives once multiple solutions exist. Second, the coordinated states (dark violet) lead to the highest average return. Interestingly, this is not influenced by the type of fragmentation, i.e. it is true for both weakly fragmented and partially fragmented states as long as a majority of the population develops a preference for a single market. By comparison, the strongly fragmented state (pink) always leads to a lower average population return.

The differences in the returns achieved by populations of decisive and indecisive traders, respectively, are driven mainly by the fact that indecisive groups can sustain more trades without requiring the presence of other groups at a market. This is particularly visible in the higher population average return for low ; in this range the decisive population suffers from the group-specific market preferences that tend to separate traders towards different markets and consequently result in a lower number of trades. Additionally, the continuation of the low solution is a viable steady state for a broader range of intensities of choice for the indecisive population. The dashed yellow line marks the region of for which this fixed point is no longer a genuine steady state, as the free energy has multiple minima when evaluated at the order parameters calculated for this fixed point. Along this line the indecisive population return again does not drop as far as it does in the case of a more decisive population.

In the right panel of Fig. 12 we note the occurence of the saddle node biffurcation in the transition of the indecisive population, with four new (V,S)-solutions (which come in two pairs giving identical returns) emerging at once. The top branch corresponds to the average population returns at the coordinated partially fragmented states; for greater values of (outside the range shown) these states smoothly transition into weakly fragmented, coordinated, states. The bottom branch relates to uncoordinated partially fragmented states that merge into the strongly fragmented (S,S) state for greater .

Interestingly, the average population return in the high limit of the coordinated state also corresponds to the average population return when all traders choose randomly (i.e. ). This is true because in both limits the average number of agents trading at each market is equal. Intriguingly, this means that when learning is introduced, for low intensities of choice, an agent who takes decisions based on their previous history may be worse off than an agent who plays at random. This effect disappears again only in the large limit of the weakly fragmented state, though note that in the latter case one group earns more than the other. Returning to the strongly fragmented state, despite indications that for a given this is best among the states that do not distinguish between groups in the long run (see Fig 6 of Alorić et al. (2016)), in terms of average population return this state is outperformed by random traders ().

V.4 Dynamics

We now ask what effect the existence of multiple steady states, as predicted by theory for infinite populations, has on the dynamics. We simulate the dynamics numerically, necessarily for finite and with learning rate , i.e. for finite memory length . In previous work we have already shown that the theory predicts the steady state properties of finite populations quite well (see e.g. Figure 4 in Alorić et al. (2016)). The role of is more important as this can shift phase boundaries Alorić et al. (2016). (Conceptually, the precise distinction for between weakly and strongly fragmented states is also lost for and becomes a crossover.)

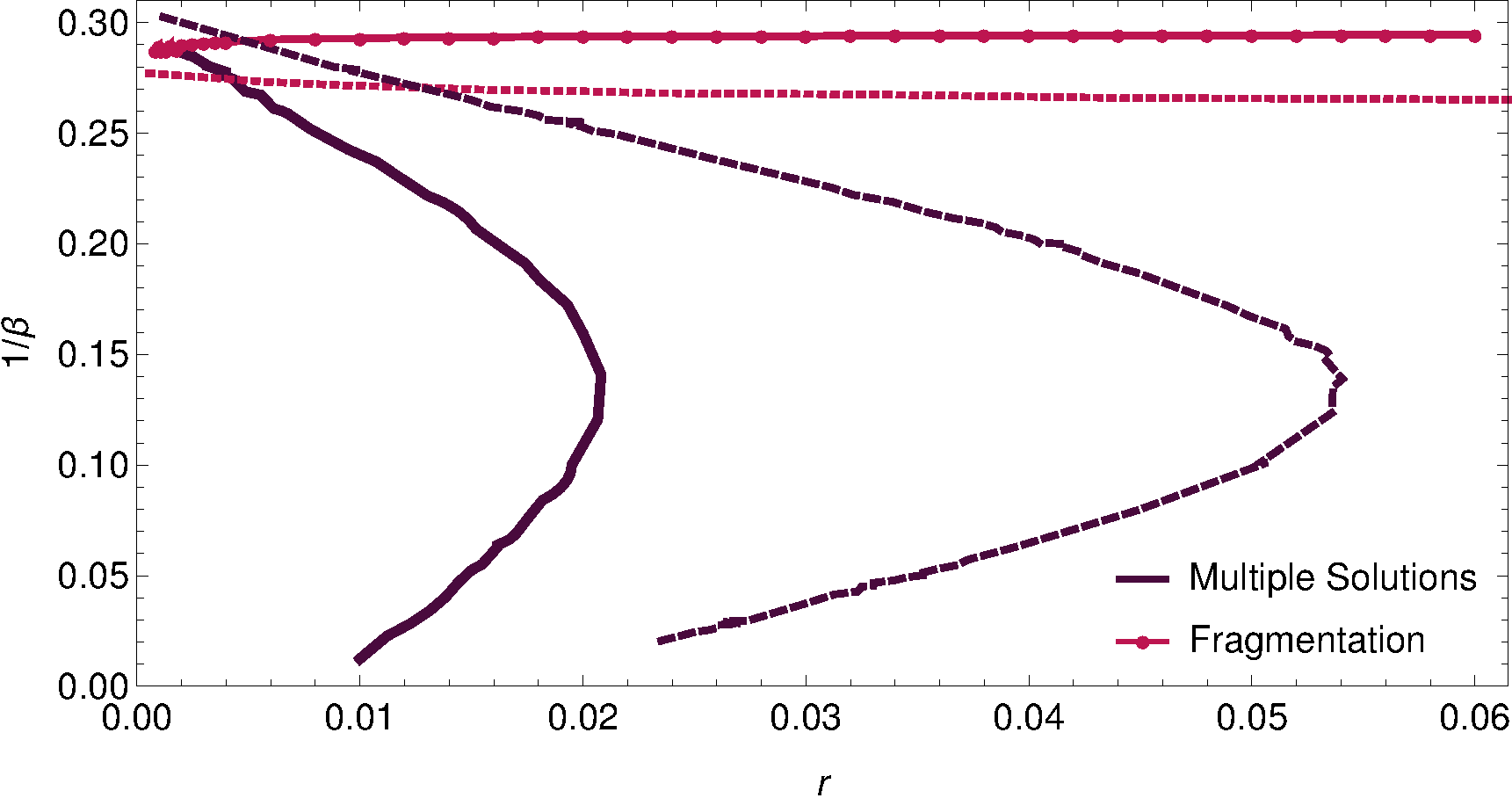

In Figure 13 we illustrate the -dependence of two key phase boundaries, for the two populations we have mainly considered so far (decisive and indecisive ). We note that the region of multiple steady states shrinks with increasing for both populations while the fragmentation line is only weakly -dependent. The lines are related to the lines of the same color in the phase diagram in Fig. 11 and the dashed grey lines marked in Fig. 11 correspond to the limit of the phase diagram in Fig. 13.

Overall, Figure 13 tells us that we need to use reasonably small , certainly below for , to see multiple steady states in numerical simulations. As smaller slow the dynamics, we choose in practice values of that are as large as possible while staying well within the multiple states regime.

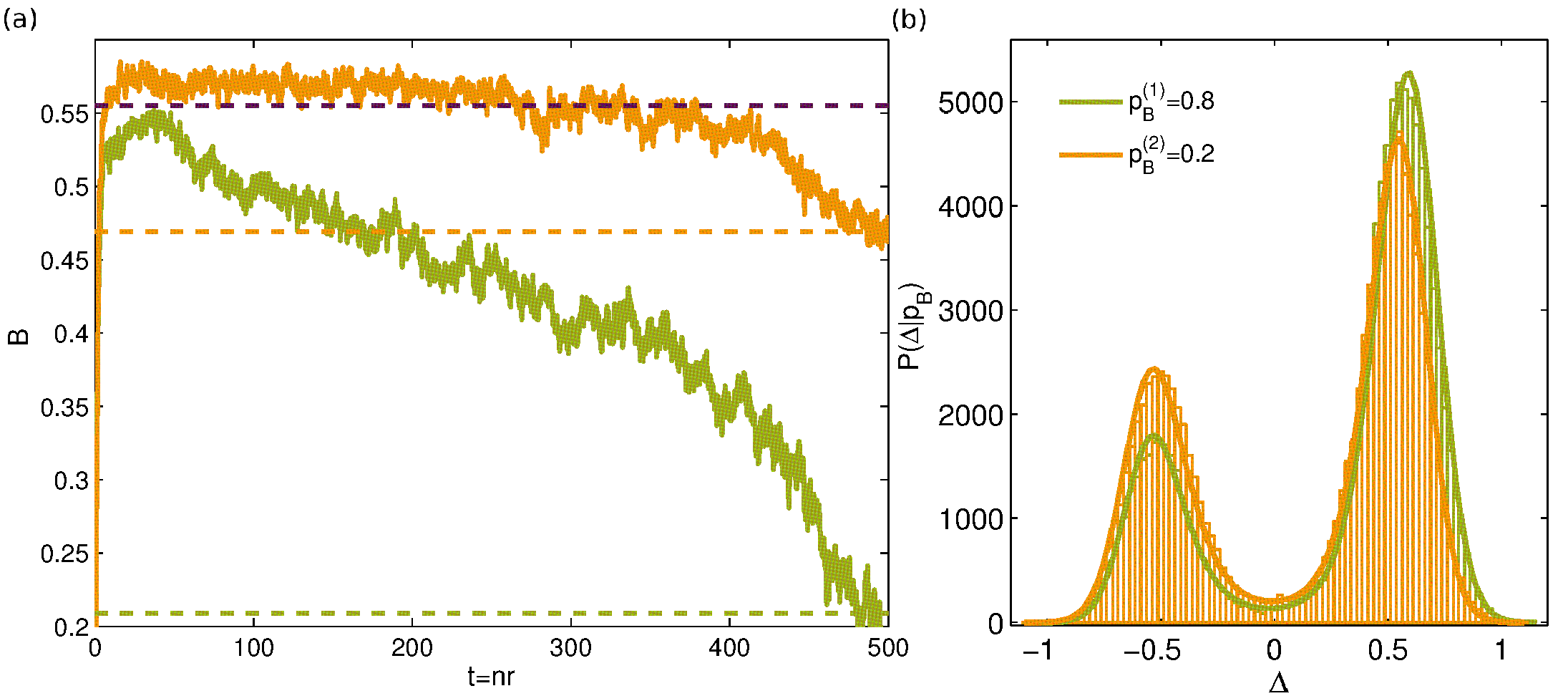

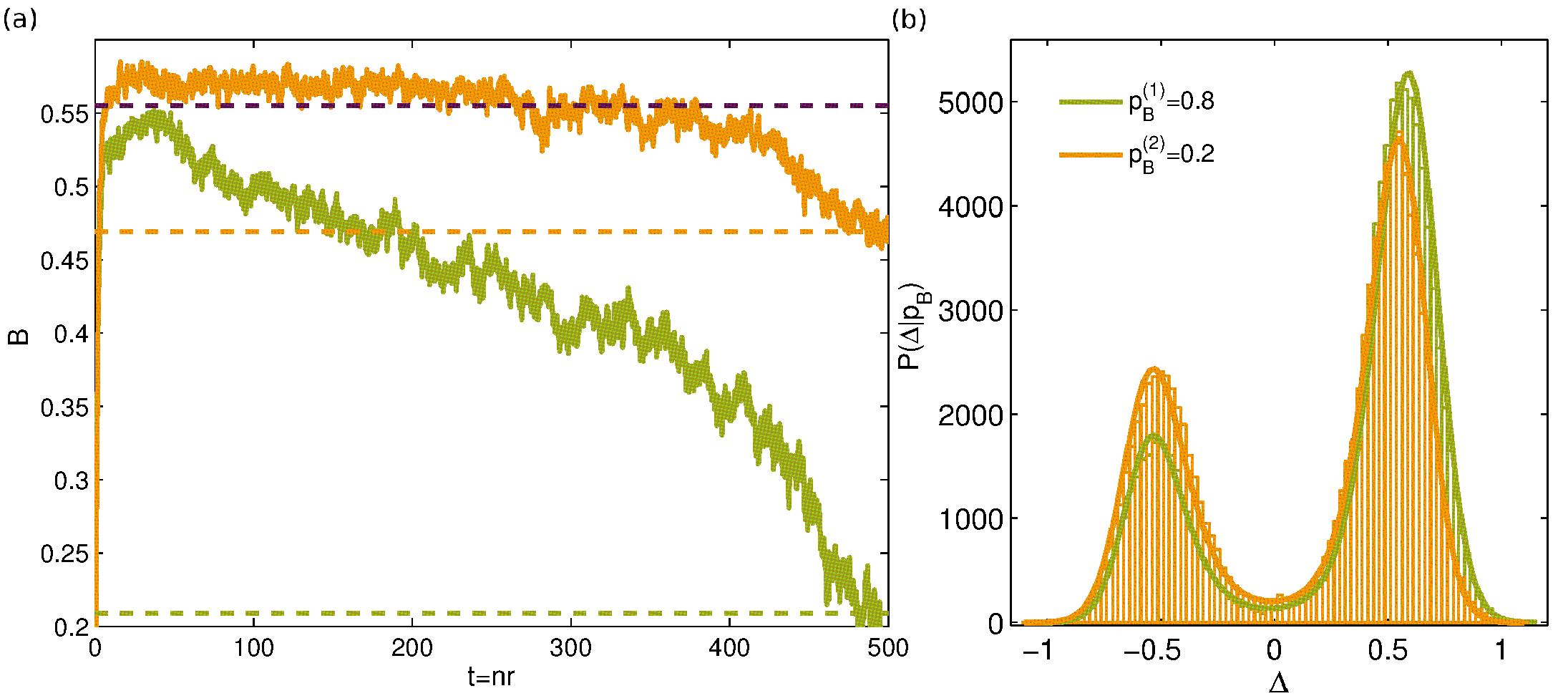

In Figure 14 we show numerical data for the actual dynamics of a system of decisive tradners at our standard market parameters , taken from a single run for a population with traders (see Alorić (2017) for simulation details) using learning rate and inverse decision strength . For these parameters the phase diagram of Fig. 13 predicts the existence of three steady states, two weakly fragmented states (with the majority of both groups coordinated at the same market, or ) and a strongly fragmented state (this state was studied in Alorić et al. (2016), see Fig. 3 there; it is the unique steady state for the larger used in Alorić et al. (2016)). As a global summary statistic of the shape of the attraction distributions of the two groups of agents we use the Binder cumulant Binder (1981)

[TABLE]

and plot this over time (see further discussion in Alorić et al. (2016); Alorić (2017)). Away from the strongly fragmented state the attraction distributions of the two groups are not related by a symmetry so we plot their Binder cumulants separately.

Figure 14 shows that the system quickly reaches the strongly fragmented state, with the Binder cumulants being close to the theoretically predicted value; the slight deviation can be attributed to the finite population size. The dynamics then branches off from the theoretical prediction at , showing that the strongly fragmented state is, for finite , only metastable. The departure is led by one of the agent groups and reaches one of the theoretically expected weakly fragmented states at , as shown in Figure 14 by the agreement both of the relevant Binder cumulants and the full attraction distributions (b).

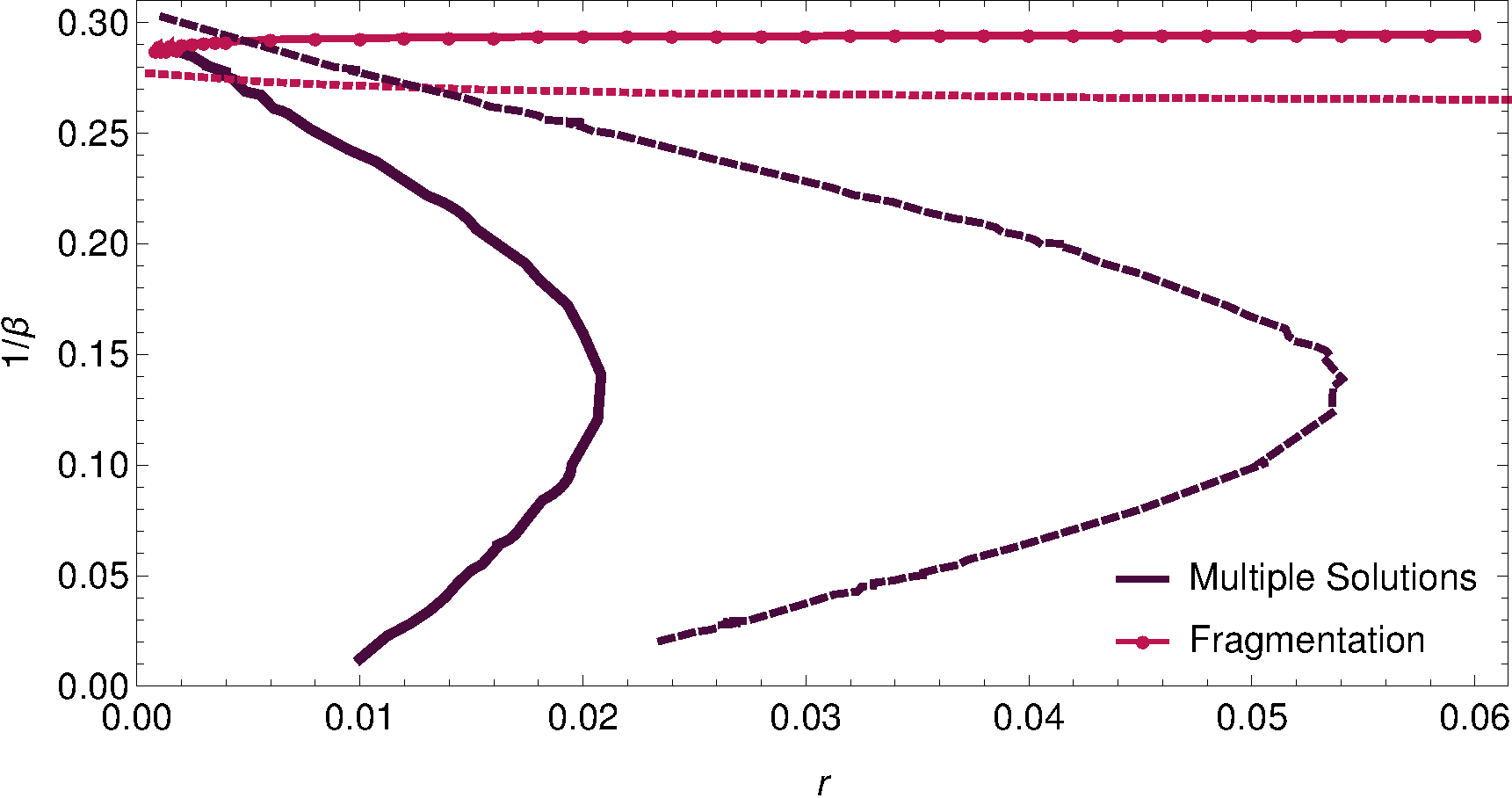

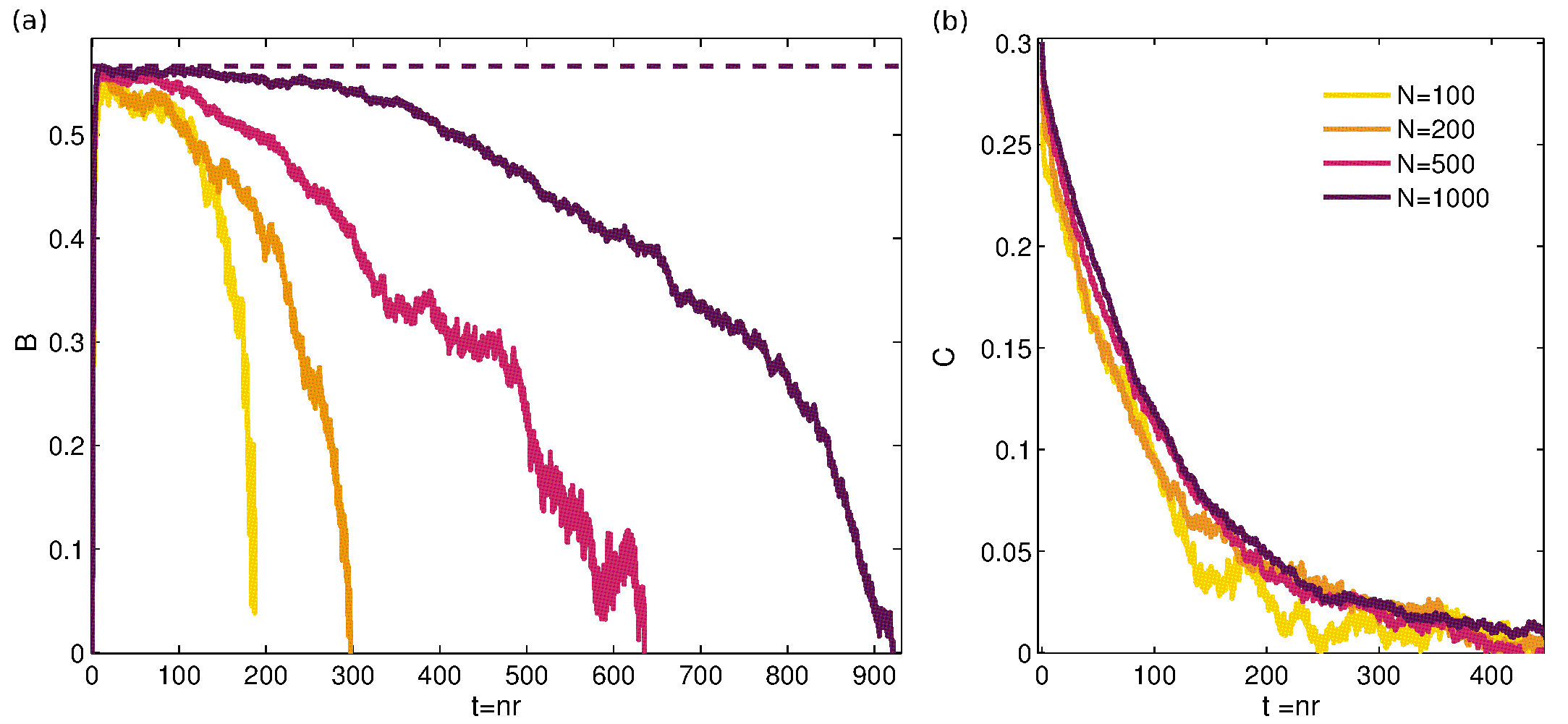

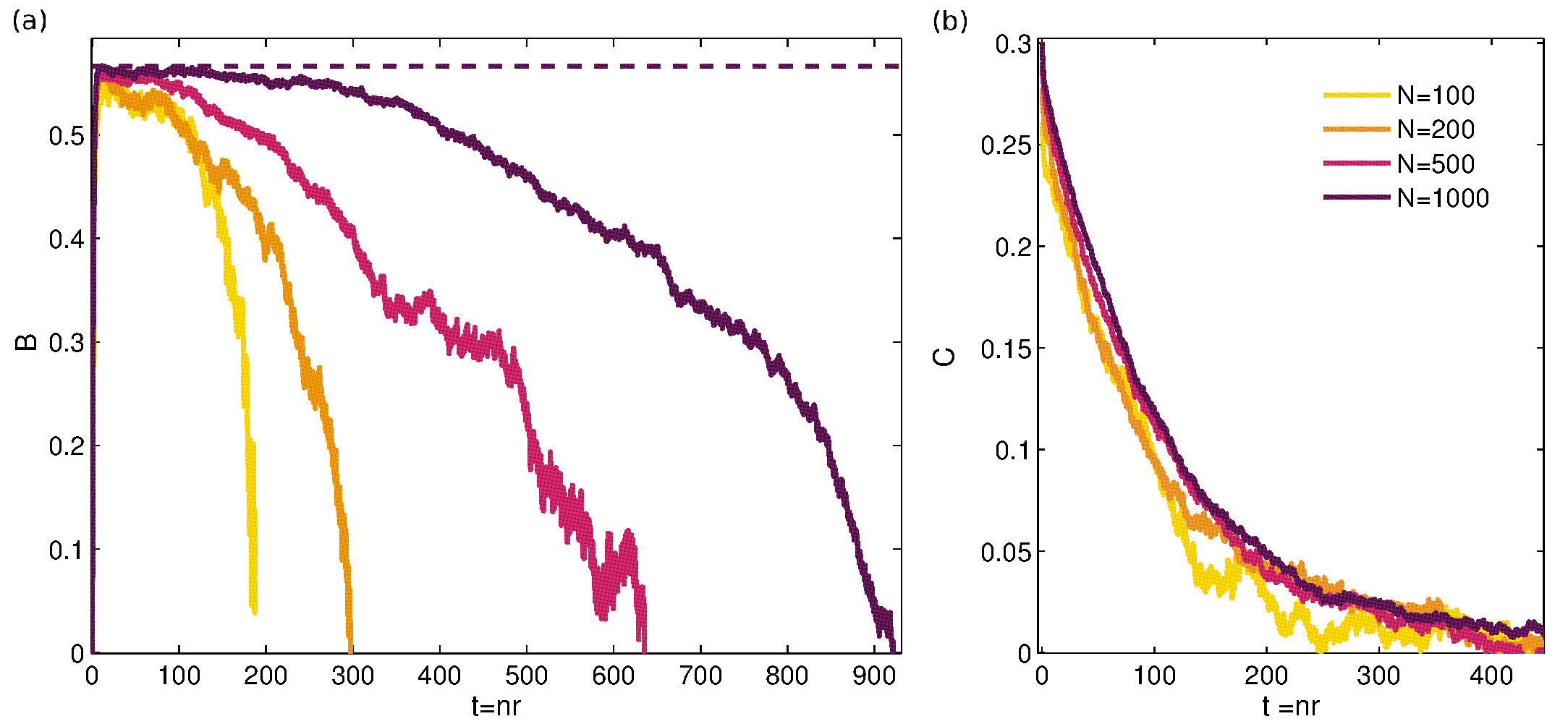

We proceed in Fig. 15 (a) to analyse the life time of the strongly fragmented steady state in more detail. The figure displays Binder cumulant time series for different population sizes at the same learning parameters and shows that the lifetime increases with system size (we have not analysed the -dependence in detail; in the range shown it is approximately linear). We can compare this with the time correlations of the attraction difference for individual agents: Fig 15 (b) graphs this correlation function, measured from the point in time when the strongly fragmented state is first reached. One sees clearly that the single agent correlation time is essentially independent of while the lifetime of the strongly fragmented state grows significantly with system size . The conclusion is that strong fragmentation is a long-lived state of the population for large , within which single agents effectively “equilibrate” by losing all memory of their initial preferences.

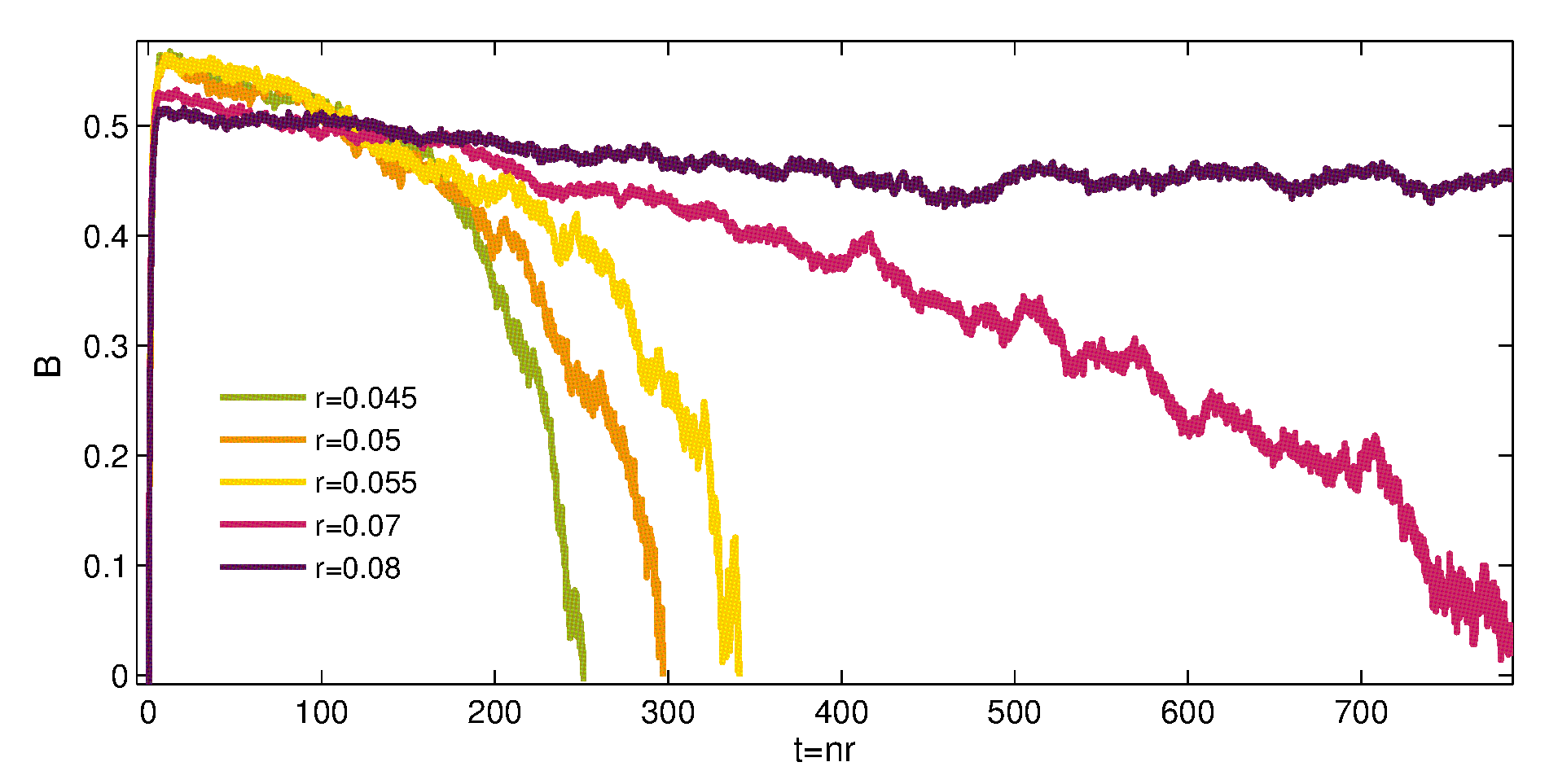

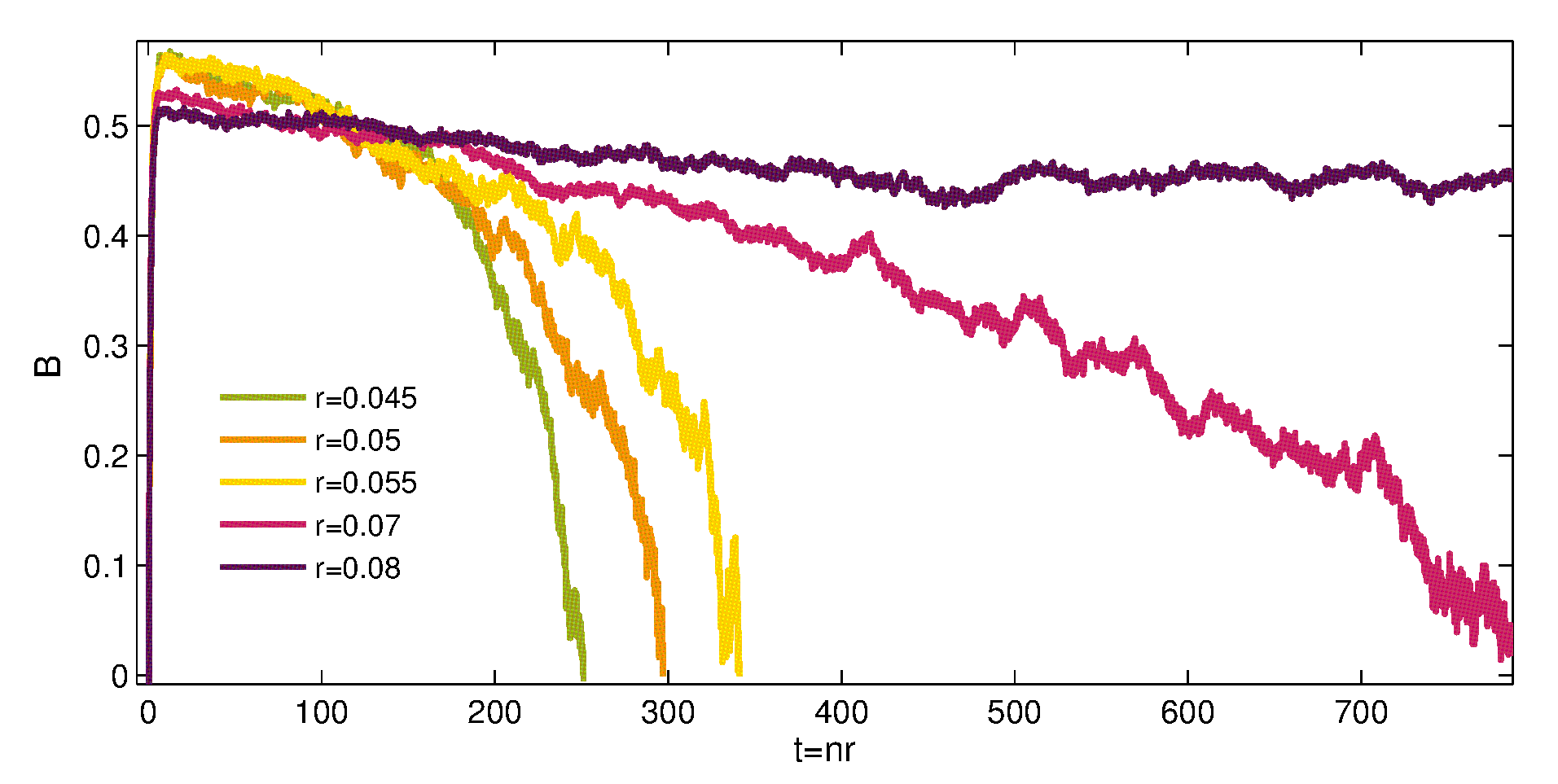

In Figure 16 we move to the -dependence of the lifetime of the strongly fragmented state, showing Binder cumulants for a small system for different -values at fixed . For all values of , rapid initial convergence to the strongly fragmented state is observed. Within this state the Binder cumulants depend weakly on as has been noted previously Alorić et al. (2016)), reflecting the -dependence of the attraction distributions. The lifetime of the strongly fragmented state, set by the decay of the Binder cumulant to lower values, increases with . This is consistent with the results of Fig. 13, which showed that above some -dependent threshold value for the strongly fragmented state is the only steady state and thus must be stable, corresponding to an infinite lifetime. For the value in Fig. 16, theory predicts this threshold to be . Numerically we see that the strongly fragmented state has a finite lifetime up to , presumably due to finite population effects for the relatively small used in the figure.

We find qualitatively the same features as above also in numerical simulations of the dynamics of a system of indecisive traders, with populations first reaching a long-lived (for large ) strongly fragmented state and eventually decaying into a partially fragmented state. This is the behaviour when such multiple steady states are predicted by our theory, i.e. for small ; for larger (above , see Fig. 13) strong fragmentation is the only steady state. Quantitatively, we find that where strong fragmentation is metastable its lifetimes are significantly longer than for the decisive traders, exceeding our maximal simulation times of trading rounds () for the largest .

We comment finally on the role of initial conditions. In the dynamical simulations shown so far we used for these , corresponding to the reasonable assumption that the agents have no initial preference for either market. We also explored Gaussian initial distributions for the attraction differences, . Where there is only a single steady state we then find, as expected, that this state is reached irrespective of the chosen initial condition. On the other hand, where the theory predicts multiple steady states, the initial conditions do matter. We observe that the metastable strongly fragmented state continues to be reached whenever the mean initial attraction difference is small enough, irrespective of the standard deviation . As is increased we see that the dynamics “misses” the metastable strongly fragmented state and rapidly moves to a final weakly or partially fragmented state. This is consistent with the intuition that these states break the symmetry between markets, and hence are favoured when the population already starts off with an overall initial preference for one of the markets.

VI Discussion & Conclusions

In this paper, our aim was to investigate the existence of coordinated and fragmented steady states in a system of agents choosing adaptively between two markets. We focussed primarily on the long memory limit, where the transition to fragmentation is sharp. We first studied two traders who learn how to coordinate at a market and maximise their average return even though one of them will necessarily earn less. Moving to a four player system we observed fragmentation in addition to coordination. Interestingly, we found that coordinated and fragmented states lead to the same average population return for high intensity of choice , in spite of the presence of two different types of agents (buyers and sellers). In the coordinated state one of the agent types will always earn less, while in the fragmented state both types have the same average, but one agent from each group is less satisfied. Thus at the fragmented state, average returns do not discriminate between types of agents.

We then introduced a general method for determining the type and number of steady states in the limit of large populations with long memory. This can be done in our setup with only a single order parameter per market. After a preliminary analysis for exogenously determined order parameters, we saw that in the general case a self-consistency criterion determines the order parameters in the steady state. Analysing a quantity analogous to a free energy then allows one to say whether a population (or one of its groups) is fragmented and whether this fragmentation is strong or weak.

Already for small system sizes we noticed that the agents’ preference for buying, , is an important system parameter. Not only does it influence the critical intensity of choice on for the onset of fragmentation, but for it also qualitatively affects the nature of the steady states. This remains true also for the limit, where we find a rich variety of steady states in the diagram, in spite of the simplified nature of our models for markets and traders. These include: market coexistence - where both markets attract both types of traders (S,S), and where market/trader specialisation occurred (W,W) (uncoordinated weakly fragmented state for moderately indecisive traders); single market dominance (W,W) (coordinated weakly fragmented states); market indifference (U,U) (e.g. for low ); general vs. specialised markets (e.g. (U,S), where a single market attracts both groups of agents while the other can be viewed as specializing towards only one group). Interestingly, all these different steady states arise without imposing any heterogeneity onto the agents (in contrast to assumptions elsewhere Gomber et al. (2017)) and fragmentation is the preferred state even when the markets have identical properties (contrary to views expressed in Pagano (1989); Chowdhry and Nanda (1991)).

To interpret our results for the prevalence of fragmentation more broadly we can draw on the work of Cheung et al. Cheung and Friedman (1997), who use evidence from Behavioural Game Theory to suggest that values of are consistent across games but increase in more informative environments. The authors also argue that a parameter closely analogous to increases with the trustworthiness of information in the system. Bearing in mind the results shown in Fig. 13, where for large and large the only steady state is the fragmented one, this suggests that more informative environments, or ones where information is more trustworthy because e.g. of stability over long timescales, might naturally lead to fragmented states. The prevalence of the strongly fragmented state is clear also from Figure 11, which shows that this state exists for all populations with groups symmetrically biased towards buying and selling, respectively.

One of the non-trivial predictions of our theory is the existence of partiallay fragmented states, where one group of agents (e.g. those who have a preference for buying) fragments while the other (where agents prefer to sell) does not. We saw that the region in the phase diagram where such states appear increases with for indecisive traders and shrinks for decisive traders (compare Fig. 5 for and Fig. 11 for ).