Optimal Contract Design for Incentive-Based Demand Response

Donya G. Dobakhshari, Vijay Gupta

TL;DR

This paper develops an optimal contract framework for demand response programs that incentivizes truthful load reduction reporting and maximal effort from customers, addressing strategic misreporting issues.

Contribution

It introduces a novel contract design that balances effort incentives and truthful reporting in incentive-based demand response settings.

Findings

Optimal contract includes load reduction-based payments and profit sharing.

The proposed contract aligns customer incentives with the DRA's objectives.

Solution addresses strategic misreporting by customers.

Abstract

We design an optimal contract between a demand response aggregator (DRA) and a customer for incentive-based demand response. We consider a setting in which the customer is asked to reduce her consumption by the DRA and she is compensated for this reduction. However, since the DRA must supply the customer with as much power as she desires, a strategic customer can temporarily increase her base load to report a larger reduction as a part of the demand response event. The DRA wishes to incentivize the customer both to make the maximal effort in reducing the load and to not falsify the base load. We model the problem of designing the contract by the DRA for the customer as a management contract design problem and present a solution. The optimal contract consists of two parts: a part that depends on (the possibly inflated) load reduction as measured and another that provides a share of the…

Click any figure to enlarge with its caption.

Figure 1

Figure 1Peer Reviews

No public reviews on file for this paper yet. If you reviewed it on a platform where reviews are public (OpenReview, ICLR, NeurIPS, ICML), you can paste yours below so the community can read it here.

Videos

No videos yet. Explain this paper in a talk, walkthrough, or lecture? Add one.

Taxonomy

TopicsSmart Grid Energy Management · Electric Vehicles and Infrastructure · Supply Chain and Inventory Management

Optimal Contract Design for Incentive-Based

Demand Response

Donya G. Dobakhshari and Vijay Gupta The authors are with the Department of Electrical Engineering, University of Notre Dame, IN, USA. Email: (dghavide, vgupta2)@nd.edu. The work was supported in part by NSF award 1550016, 1239224 and 1544724. This work has been submitted to the IEEE for possible publication. Copyright may be transferred without notice, after which this version may no longer be accessible.

Abstract

We design an optimal contract between a demand response aggregator (DRA) and a customer for incentive-based demand response. We consider a setting in which the customer is asked to reduce her consumption by the DRA and she is compensated for this reduction. However, since the DRA must supply the customer with as much power as she desires, a strategic customer can temporarily increase her base load to report a larger reduction as a part of the demand response event. The DRA wishes to incentivize the customer both to make the maximal effort in reducing the load and to not falsify the base load. We model the problem of designing the contract by the DRA for the customer as a management contract design problem and present a solution. The optimal contract consists of two parts: a part that depends on (the possibly inflated) load reduction as measured and another that provides a share of the profit that ensues to the DRA through the demand response event to the customer.

I INTRODUCTION

Demand response, in which a utility company or an aggregator motivates customers to curtail their power usage, has now become an acceptable method in situations when high peaks in demand occur. Demand Response (DR) can be defined as the change in electric usage by end-use customers from their normal consumption patterns in response to changes in the price of electricity or any other incentive [1, 2] and [3].

Generally, DR programs are divided into two main categories: Incentive Based Programs (IBP) and Price Based Programs (PBP). PBPs provide time of usage based electricity prices and the consumers are expected to adjust their demand in response to such a price profile. On the other hand, IBPs offer incentives to customers to reduce their demand. These incentives may be constant and based only on customer participation in the program (classical) or dynamic in the sense that they vary with the amount of load reduction that a customer achieves (market-based). There exists a rich literature (e.g, in [4, 5, 6, 7, 8] and the references therein) studying issues such as social welfare maximization, minimization of electricity generation and delivery costs, and reducing renewable energy supply uncertainty for incentive-based demand response.

In this paper, we consider an incentive based DR scenario where participants are rewarded financially by the demand response aggregator (which role can also be filled by a utility company) for the amount of load reduction provided by consumers during DR events. However, unlike the existing literature, we consider a strategic customer that maximizes her own profit by predicting the impact of her actions and the information she transmits. Specifically, by taking advantage of the fact that the demand response aggregator (DRA) must supply as much power as the customer desires, a strategic customer can artificially inflate her base load before an expected DR event. Then, during the DR event, for the same nominal load reduction, the customer can report more measured load reduction and gain more financial reward from the DRA.

In such a scenario, we wish to find a contract that incentivizes the strategic customer to achieve the maximum nominal load reduction possible. The main contribution of our work is to characterize an optimal contract for this DR problem. Our solution is similar to a managerial contract model studied e.g. in [9, 10]; however, we do not assume accurate knowledge of the profit achieved by the DRA as a result of the load reduction by the customer. The optimal contract consists of two parts: a part that depends on the reported load reduction and another that provides a share of the profit for the DRA through the demand response event to the customer.

One interesting result is that the optimal contract leads to under-reporting of load reduction by the customer up to a specific value of nominal load reduction and over-reporting of reduction above that value. In other words, if the strategic customer wishes to maximize her profit, she may sometimes decrease her base load before the DR event to under-report her power reduction. Furthermore, if the expected difference between the nominal reduction with the true base load and the reported one with the inflated or deflated base load is positive, the DRA’s expected profit is an increasing function with respect to the share provided to the customer. Finally, the analysis implies that it is always optimal (from the DRA’s viewpoint) to assign some positive share of the profit to the customer.

The paper is organized as follows. In Section II, the problem statement is presented. In Section III, the solution to the optimization problem is presented. Next, we discuss the optimal contract structure and its properties in Section IV. The final section concludes the paper by pointing out some directions for future work.

Notation

(which is often simplified to ) and denote the probability distribution function (pdf) and cumulative distribution function (cdf) of random variable given the event respectively. Gaussian distribution is denoted by where is the mean and is the standard deviation. Derivative of a function with respect to a variable is denoted as or if the variable is clear from the context. For two functions and , denotes the convolution between and . denotes expectation of random variable . By abusing notation, we sometimes write the expectation as .

II Problem Statement

We model a demand response event as beginning when the DRA calls on a customer to decrease her power consumption. A strategic customer, anticipating such a call, can increase her base load, or the load before the demand response event. This pre-increase allows the customer to reduce the load by a larger amount than would have been possible in the absence of such an increase. The customer potentially gains from this larger reduction if the market based DR entails payment of an incentive proportional to the load reduction by the customer during the DR event. On the other hand, a contract must make the payment proportional to the load reduction to exert the maximal effort for reducing the load by as much amount as possible (See Example 1 below).

Remark: It is worth pointing out that the falsification of the load reduction reported to the DRA happens even though the load at the customer is being monitored constantly and accurately. Further, the DRA can not find the ‘true’ base load by considering the load used by the customer at some arbitrary time before the DR event. For one, this simply shifts the problem of customer manipulation of the load to an earlier time. Second, some of the increase in the base load may be due to true shifts in customer need due to, e.g., increased temperature.

II-A Problem Formulation

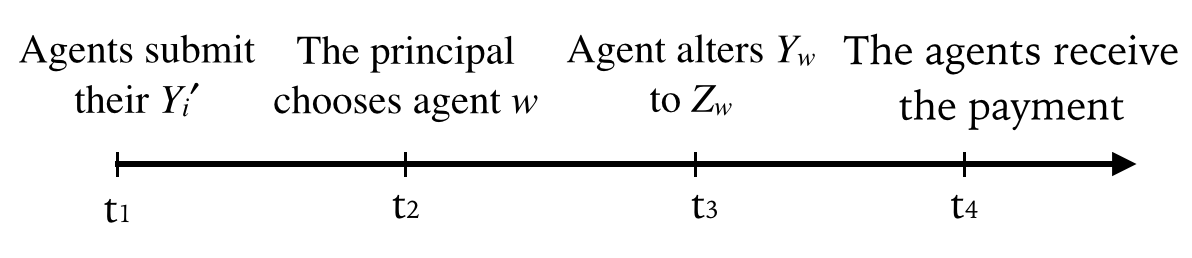

Refer to the timeline shown in Figure 1. The true base load (without any manipulation) is given by . At time , the customer calculates the effort she is willing to put in for achieving the load reduction during the DR event. The load reduction is according to the probability density function which is public knowledge. We assume that an effort costs the customer ( is convex and ). Further, this effort and the planned load reduction depends on private knowledge at the customer and hence can be calculated by the customer, but not by the DRA. For instance, a factory might be able to induce a large load reduction with a small effort based on its assembly line requirements given the orders it has to fulfill. After this calculation, the customer at time may increase (or decrease) the load by an amount in anticipation of the DR event.

At time , the DR event begins and the DRA calls on the customer to decrease her load. The customer now makes the effort yielding a reduction of the load by . The DR event ends at with the customer having decreased the load by an amount (which is often simplified to ). Note that the planned reduction in the load is , while the false reported load reduction is . We also show the times , and in the timeline in Figure 1. At time (much before ), the contract is signed between the DRA and the customer, while at times and , the customer is paid by the DRA according to the contract we will propose in the sequel. We note that is sufficiently early, so that at , the customer does not know the local conditions and must consider her expected utility according to the probability density function .

The time is sufficiently close to the DR event, so that, the realized value of is not known at time to the DRA. The customer needs to be paid at least in part at to incentivize her to participate in the DR event. However, at some (much) later time , the DRA may be able to estimate the realized value of , possibly with some error. This noisy estimate can be obtained by, e.g., large scale data analysis on all similar customers on that day or historical behavioral of the same customer. We denote this estimate by where . We assume that the random variables and are independent and .

We model the falsification cost incurred by the customer (e.g. extra charge paid for boosting her consumption) by a quadratic function for simplicity and denote this cost as .

The problem is for the DRA to design a contract that maximizes his own profit. Since this profit depends on the load reduction by the customer, the contract must induce a rational customer to choose an action and a report that are optimal for the DRA. The profit for the DRA occurs due to the load reduction by the customer, modulo any payments made to the customer as part of her contract. We discuss the intuition for the proposed contract through some examples.

Example 1

Consider a contract that provides a constant incentive to the customer for decreasing her load. Then, the customer’s utility is given by:

[TABLE]

where is the unit step function. The DRA’s utility is given by

[TABLE]

In this case, the customer seeking to maximize her utility, independent of the value of , will choose and respectively (i.e., no action and no true load reduction) but (i.e., minimal load reduction). This implies that to induce positive load reduction, a contract must make at least part of the payment proportional to the load reduction.

Example 2

Consider a contract in which the DRA provides an incentive to the customer in response to the reported reduction (which is all that she has access to at ). Then, the customer’s utility is given by:

[TABLE]

while the DRA’s utility is given by

[TABLE]

The DRA seeks to optimize over assuming that the customer will choose and to maximize . However, irrespective of the optimization, a customer again can take no action, i.e. , and report to gain the positive profit . Thus, a good contract must entail some payments that depends on the DRA’s estimated profit .

Next, we propose a contract structure free from the shortcomings of these intuitive contracts.

II-B Contract Structure

Inspired by managerial contracts studied e.g. in [9, 10], we propose a contract of the form in which refers to the share of his own profit that the DRA provides to the customer, while refers to the payment made in proportion to the reported reduction . Referring to Figure 1, to incentivize the customers to participate in the program, is paid at . However, the shares (even though they are allotted at ) can be encashed only at a much later time when an estimated value of the profit can be calculated and revealed. Note that the portion of the payment corresponding to the share is calculated on the basis of the noisy estimate of . Thus, the customer’s utility is given by

[TABLE]

while the DRA utility is given by

[TABLE]

It is worth pointing out that the customer will report a load reduction to realize ; therefore, is a function of , not .

Thus, the optimization problem to be solved by DRA (subject to participation and rationality constraints for customer) is given by

[TABLE]

We now describe the constraints for the optimization problem in (3).

Rationality in the choice of effort: The first assumption is that the customer chooses the level of effort to maximize her expected utility . Thus, the first two constraints are given by and where the expectation is taken with respect to and . 2. 2.

Ex ante individual rationality: The expected utility of the customer must be positive to ensure that she participates in the DR event. This implies a constraint of the form . 3. 3.

Interim individual rationality: We impose that the customer must be incentivized to continue even though she can choose to leave after she makes effort and sees her comfort reduced. We impose this constraint as

[TABLE] 4. 4.

Incentive compatibility: We impose two further constraints and as incentive compatibility constraints that ensure truthtelling by the customer in the conditional direct revelation contract [9].

Thus, the optimization problem can be rewritten as

[TABLE]

subject to:

[TABLE]

We will present the optimal contract in Section III. The solution depends on the properties of the pdfs that describes the planned reduction based on effort of the customer and which is the pdf of the estimation error in the knowledge of in the long term. We make the following assumptions about these functions :

Assumption : The cdf of is strictly decreasing, convex and continuously differentiable in for all and for all . This is a natural assumption implying that higher customer effort induces a first-order stochastic improvement in the distribution of load reduction and results in diminishing marginal returns from effort. 2. 2.

Assumption : for all and . Further, there exists such that for all and and . 3. 3.

Assumption : for all . This assumption implies that positive values of load reduction are more likely than zero values of load reduction. 4. 4.

Assumption : is strictly concave in for all and is strictly convex in for all where

[TABLE]

Assumption is provided for the proof of corollary 3 (in section IV) where we restrict to Gaussian distribution for and for simplicity.

Lemma 1

The properties encapsulated in assumptions - hold for the probability density function and the corresponding CDF as well.

Proof:

We present the proof for assumption , the proofs for rest of assumptions are similar.

By definition, and are related as . Thus, and can be derived as follows:

[TABLE]

[TABLE]

[TABLE]

According to (9) and noting that is a probability distribution function and positive everywhere,

[TABLE]

Thus, if is strictly decreasing, will be strictly decreasing too. For convexity, since is strictly decreasing, it is enough to only prove . Now, given (9),

[TABLE]

Therefore, Assumption holds for .

∎

III Optimal contract Structure

In this section, we present the solution of the optimization problem stated in (5). Consider the argument being optimized in (5). We begin with the case when . We can rewrite the expected utility of the DRA as:

[TABLE]

We can define to rewrite the optimization problem as

[TABLE]

subject to and the constraints in (6a)-(6d). This is an optimal control problem where the state variable is and is the control input. We can solve this problem using the standard Hamiltonian approach. For now, we drop the second constraint (6d) and will add this constraint later to the contract. Also we note the following result that was proved in [9] and implies that the second order condition in (6a) is non-binding.

Lemma 2

Given the distribution assumptions , is strictly negative for any optimal contract.

Thus, we can form the Hamiltonian

[TABLE]

and the corresponding Lagrangian

[TABLE]

where is the co-state variable (considering ), is , is the state variable, and is the control input. Further, , , and are all non-negative multipliers included for considering the constraints (6a), (6b), and (6c) respectively.

We can now provide the structure of the optimal contract in the following result.

Theorem 1

Given the assumptions -, if there exist a piecewise continuous function , constraint multipliers , and , and a contract that satisfy :

[TABLE]

then is an optimal conditional contract that solves the optimization problem in (5) and (6).

Proof:

The proof follows readily from [11, Chapter 6, Theorem 1] by substituting , , . ∎

This characterization can be used to determine the optimal values of the share and bonus on one hand, and the resulting effort and reporting function that are induced on the other. For illustration, we present the result for the reporting function below. The results for the other quantities can be derived similarly; we present insights on their forms in the next section.

Definition 1

Define as the solution of the equation .

The first equation in (6d) and the fact that the function is a quadratic function implies that can be obtained as

[TABLE]

The reporting function induced by the optimal contract is presented in the following result.

Theorem 2

The optimal reporting function is given as

[TABLE]

Proof:

The proof follows along the lines outlined in [9] using the conditions in (14a)-(14g) and the fact that . ∎

IV Discussion of Results

We now interpret the results obtained in the previous section. For ease of interpretation and without loss of generality, we scale down to the range .

IV-A Form of the reporting function

We can obtain a clearer interpretation of over-reporting (inflation of base load) and underreporting (reduction of base load) through the following result that specifies the form of the reporting function.

Corollary 1

There exists , with given in (15) such that the optimal reporting function satisfies the following relation

[TABLE]

Proof:

From equation (16), we see that for , , which is always less than . As increases, we appeal to assumption , its generalization to in Lemma 1 and the fact that , to obtain that the function

[TABLE]

is strictly concave in for all . Thus, is an increasing function of and for a high enough value of , the sign of will become positive [9]. This value is which is clearly larger than . ∎

The form of the reporting function is illustrated in Figure 2. The result clarifies how the customer will falsify the load reduction by changing the base load. For nominal load reduction above , , i.e. the customer first increases the base load and then lowers it by the amount . However, if , . This implies that in this case, the customer lowers the demand at the beginning (or reports that she was going to reduce the demand even without the DR event) and then decreases the demand by again when called. This non-intuitive behavior can be understood if we remember that although granted to customer is decreased through under-reporting, the share of the profit assigned to the customer to incentivize her to participate is larger in this case and this share compensates for the decrease in .

IV-B Optimal Compensation

In order to study the optimal compensation, we first present the following result without proof.

Lemma 3

In an optimal contract, and are 0 for and is greater than zero for .

We notice that the bonus can be considered to be a function of the savings and written as . Further, the bonus is related to as

[TABLE]

Corollary 2

The optimal satisfies the relation

[TABLE]

Proof:

When , . Since, , we observe that . Similarly, for

[TABLE]

Using this result along with the relation leads to

[TABLE]

Combining the two, cases we have

[TABLE]

While if , for , the sign of depends on the sign of (since for ). Thus, combining (22) with (17) yields the desired result. ∎

This result once again sheds light on the structure of the two counteracting incentives provided to the customer. As increases, the bonus decreases up to the level . In this range, the customer chooses to rely on the long term share and under-reports the load reduction she has made. For large enough, the bonus is an increasing function. In this range, the bonus is large enough and hence the customer chooses to boost her bonus by over-reporting her load reduction.

IV-C Impact of Estimation Error

In order to compare the optimal reporting as a function of the noise in the estimation of the profit made due to the reduction of load, we need to investigate the optimal reporting function for the cases when is realized at exactly and with some error. Equation (16) shows the relation between the optimal reporting function and the true profit with estimation error. In the absence of any error, the expression reduces to

[TABLE]

For simplicity, we assume for the next result that and It is worth pointing out that assumptions hold in this case (for Gaussian distribution). By definition, will be a Gaussian random variable and . Notice when there is no error and , in the case of noise; however, so . Accordingly, suppose and represent the pdf of in the absence and presence of noise. Comparing and for a variable , we obtain:

[TABLE]

where .

Corollary 3

Suppose the profit is estimated with an estimation error. If and the constraint multiplier in (16) is [math], the optimal contract induces the customer to do less underreporting (in the sense that the customer under-reports for a narrower range of load reduction) in the presence of estimation error as compared to the case without error.

Proof:

Given the distribution assumptions on and , will be a Gaussian random variable and its variance will be less than . Therefore, and . Based on (24), it can be noted that if , for , . Thus, if ,

[TABLE]

Therefore, comparing (23) and (16) for and , the customer does less underreporting when there exists noise in the estimation in an optimal contract. ∎

Remark 1

Comparing the two cases, we see that is identical in the two cases. However, will decrease in the case when . .

IV-D Optimal Share Allocated to the Customer

The following result shows that the optimal contract must utilize the option of giving shares to the customer.

Corollary 4

The value of is strictly positive in the optimal contract.

Proof:

Differentiating with respect to yields

[TABLE]

which can be reduced to

[TABLE]

This implies that if the expectation of the distortion of the load is positive (respectively negative), will be increasing (respectively decreasing) with respect to . If , is equal to [math] for and positive for (based on assumption and its generalization to in Lemma 1,

[TABLE]

is strictly concave). Thus, given that is continuous, is strictly positive. As increases, (16) indicates that the curve of shifts down, so that for . Consequently, decreases as increases. Thus, for a large enough , we have that . For this critical value of , (27) implies that . Further, this is clearly a maxima. ∎

V CONCLUSIONS

In this paper, we designed an optimal contract between a demand response aggregator (DRA) and a customer for incentive-based demand response. In this set up, the DRA asks the customer to reduce her demand and compensates her for this reduction. However, since the DRA must supply the customer with as much power as she desires, a strategic customer can temporarily increase her base load to report a larger reduction after the demand response event. Based on management contract design problem, we proposed an optimal contract that maximizes DRA’s utility by incentivizing the customer both to make the maximal effort in reducing the load and not to falsify the base load. The proposed optimal contract consists of two parts: a share of the DRA’s profit in demand response event and a part that is compensation paid to customer depending on load reduction as measured. Further, some properties of the customer share of the profit and the compensation paid to her were discussed.

Future work will involve considering the dynamic problem, impact of pricing, and also the multiple customers and ownership case. Relating this work to the game theoretic set ups in [13] and [14] is also of interest.

ACKNOWLEDGMENT

We would like to thank Dr. Thomas A.Gresik from Department of Economics in the University of Notre Dame for his insights and comments.

The reference list from the paper itself. Each links out to its DOI / PubMed record.

- 1[1] J. S. Vardakas, N. Zorba, and C. V. Verikoukis, “A survey on demand response programs in smart grids: Pricing methods and optimization algorithms,” Communications Surveys & Tutorials, IEEE , vol. 17, no. 1, pp. 152–178, 2015.

- 2[2] R. Deng, Z. Yang, M.-Y. Chow, and J. Chen, “A survey on demand response in smart grids: Mathematical models and approaches,” Industrial Informatics, IEEE Transactions on , vol. 11, no. 3, pp. 570–582, 2015.

- 3[3] M. H. Albadi and E. El-Saadany, “Demand response in electricity markets: An overview,” in IEEE power engineering society general meeting , vol. 2007, 2007, pp. 1–5.

- 4[4] F. A. Qureshi, T. T. Gorecki, and C. Jones, “Model predictive control for market-based demand response participation,” in 19th World Congress of the International Federation of Automatic Control , no. EPFL-CONF-197950, 2014.

- 5[5] A.-H. Mohsenian-Rad, V. W. Wong, J. Jatskevich, and R. Schober, “Optimal and autonomous incentive-based energy consumption scheduling algorithm for smart grid,” in Innovative Smart Grid Technologies (ISGT), 2010 . IEEE, 2010, pp. 1–6.

- 6[6] P. Samadi, A.-H. Mohsenian-Rad, R. Schober, V. W. Wong, and J. Jatskevich, “Optimal real-time pricing algorithm based on utility maximization for smart grid,” in Smart Grid Communications (Smart Grid Comm), 2010 First IEEE International Conference on . IEEE, 2010, pp. 415–420.

- 7[7] A. J. Roscoe and G. Ault, “Supporting high penetrations of renewable generation via implementation of real-time electricity pricing and demand response,” IET Renewable Power Generation , vol. 4, no. 4, pp. 369–382, 2010.

- 8[8] Q. Wang, M. Liu, and R. Jain, “Dynamic pricing of power in smart-grid networks,” in Decision and Control (CDC), 2012 IEEE 51st Annual Conference on . IEEE, 2012, pp. 1099–1104.