Game-Theoretic Optimal Portfolios for Jump Diffusions

Alex Garivaltis

TL;DR

This paper extends the Kelly portfolio optimization to jump diffusion models in a two-player game setting, showing that the optimal strategy for outperforming others is the leveraged Kelly rule.

Contribution

It introduces a game-theoretic framework for jump diffusion markets and proves the Kelly rule as the unique saddle point strategy.

Findings

Kelly rule remains optimal in jump diffusion settings

Players' optimal strategies are characterized by the Kelly rule

The framework generalizes previous models to include jumps

Abstract

This paper studies a two-person trading game in continuous time that generalizes Garivaltis (2018) to allow for stock prices that both jump and diffuse. Analogous to Bell and Cover (1988) in discrete time, the players start by choosing fair randomizations of the initial dollar, by exchanging it for a random wealth whose mean is at most 1. Each player then deposits the resulting capital into some continuously-rebalanced portfolio that must be adhered to over . We solve the corresponding `investment -game,' namely the zero-sum game with payoff kernel , where is player 's fair randomization, is the final wealth that accrues to a one dollar deposit into the rebalancing rule , and is any increasing function meant to measure relative performance. We show that the unique…

Click any figure to enlarge with its caption.

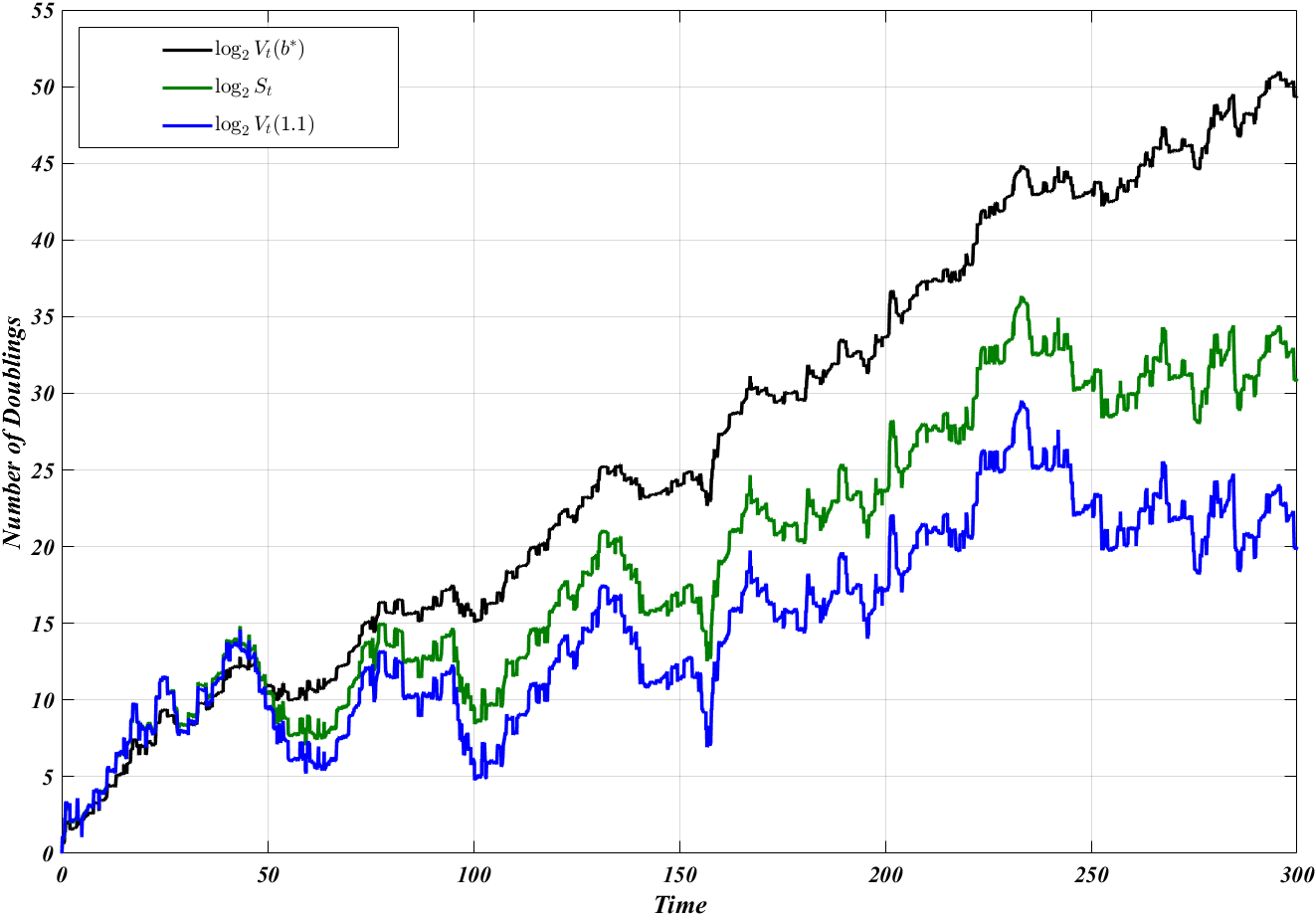

Figure 1

Figure 1 Figure 2

Figure 2 Figure 3

Figure 3 Figure 4

Figure 4 Figure 5

Figure 5Peer Reviews

No public reviews on file for this paper yet. If you reviewed it on a platform where reviews are public (OpenReview, ICLR, NeurIPS, ICML), you can paste yours below so the community can read it here.

Videos

No videos yet. Explain this paper in a talk, walkthrough, or lecture? Add one.

Taxonomy

TopicsFinancial Markets and Investment Strategies · Stochastic processes and financial applications · Advanced Bandit Algorithms Research