Driving an Ornstein--Uhlenbeck Process to Desired First-Passage Time Statistics

Khem Raj Ghusinga, Vaibhav Srivastava, Abhyudai Singh

TL;DR

This paper investigates how to control the first-passage time distribution of an Ornstein-Uhlenbeck process with two boundaries, enabling independent adjustment of mean and variability through specific control strategies.

Contribution

It reveals the scale invariance of the FPT distribution with respect to the drift and proposes methods to tune control parameters for desired FPT moments and distribution shape.

Findings

FPT distribution is scale invariant with respect to drift

Mean and CV of FPT can be controlled independently

Optimal control parameters can minimize distribution distance

Abstract

First-passage time (FPT) of an Ornstein-Uhlenbeck (OU) process is of immense interest in a variety of contexts. This paper considers an OU process with two boundaries, one of which is absorbing while the other one could be either reflecting or absorbing, and studies the control strategies that can lead to desired FPT moments. Our analysis shows that the FPT distribution of an OU process is scale invariant with respect to the drift parameter, i.e., the drift parameter just controls the mean FPT and doesn't affect the shape of the distribution. This allows to independently control the mean and coefficient of variation (CV) of the FPT. We show that that increasing the threshold may increase or decrease CV of the FPT, depending upon whether or not one of the threshold is reflecting. We also explore the effect of control parameters on the FPT distribution, and find parameters that minimize…

Click any figure to enlarge with its caption.

Figure 1

Figure 1 Figure 1

Figure 1 Figure 2

Figure 2 Figure 3

Figure 3 Figure 5

Figure 5Peer Reviews

No public reviews on file for this paper yet. If you reviewed it on a platform where reviews are public (OpenReview, ICLR, NeurIPS, ICML), you can paste yours below so the community can read it here.

Videos

No videos yet. Explain this paper in a talk, walkthrough, or lecture? Add one.

Driving an Ornstein–Uhlenbeck Process to Desired

First-Passage Time Statistics

Khem Raj Ghusinga1, Vaibhav Srivastava2, and Abhyudai Singh1 1 Khem Raj Ghusinga and Abhyudai Singh are with the Department of Electrical and Computer Engineering, University of Delaware, Newark, DE, USA. {khem,absingh}@udel.edu2 Vaibhav Srivastava is with the Department of Electrical and Computer Engineering, Michigan State University, East Lansing, MI, USA. [email protected]

Abstract

First-passage time (FPT) of an Ornstein-Uhlenbeck (OU) process is of immense interest in a variety of contexts. This paper considers an OU process with two boundaries, one of which is absorbing while the other one could be either reflecting or absorbing, and studies the control strategies that can lead to desired FPT moments. Our analysis shows that the FPT distribution of an OU process is scale invariant with respect to the drift parameter, i.e., the drift parameter just controls the mean FPT and doesn’t affect the shape of the distribution. This allows to independently control the mean and coefficient of variation (CV) of the FPT. We show that that increasing the threshold may increase or decrease CV of the FPT, depending upon whether or not one of the threshold is reflecting. We also explore the effect of control parameters on the FPT distribution, and find parameters that minimize the distance between the FPT distribution and a desired distribution.

I INTRODUCTION

The first passage time (FPT) is the earliest time at which a trajectory of a stochastic process initially inside a bounded region leaves the region. The FPTs are extensively used across disciplines, including neuroscience [1], biology [2, 3, 4], finance [5], ecology [6], engineering [7], statistical physics [8], finance [9], and health science [10] to model several interesting phenomena. For example, the FPT of diffusion processes is used to model human decision-making [1], animal foraging [6], financial markets [9], and clock synchronization [7].

In this paper, we study control of the FPT statistics of an Ornstein-Uhlenbeck (OU) process between two fixed boundaries; one of which is absorbing, and the other can be absorbing or reflecting. An OU process belongs to the class of diffusion processes and is a generalization of drift-diffusion process. The OU process is also a continuum approximation to several discrete time Markov models. For biological phenomena modeled by FPTs, the analysis in this paper can provide insights into the mechanisms these systems employ to cope with uncertainty and ensure resilient performance. For example, how attention and memory is modulated in human decision-making, or how a gene’s expression is regulated to control timing of its response, or how animals regulate their foraging activity. For engineered systems, these analysis may provide insights into optimal control laws that delay an undesired event such as epidemic outbreak, or optimal control laws that achieve a desired distribution for time to certain event such as adoption of a product by certain fraction of population.

The problem of steering a linear stochastic system to a desired final distribution has been studied [11]. However, computing and controlling FPT distribution is significantly more complicated than controlling the evolution of trajectories without boundaries. Indeed, the Fokker-Plank equation for the OU process is nonlinear and has limited tractability [12]. Control of FPT distribution for OU process has been studied in [13], wherein the boundary of the region is controlled to steer the FPT distribution to a Gamma distribution. Loosely speaking, this problem can be thought of as a boundary control of a PDE [14], where underlying PDE is the Fokker-Planck equation.

In our recent work [15], similar problems were explored in the context of gene expression. Therein the stochastic process is a continuous-time discrete-state process defined on positive integers, with a reflecting boundary at [math] and a fixed absorbing boundary. The results showed that the best strategy to minimize the coefficient of variation (CV) of FPT for a fixed mean FPT is a constant rate of production (forward hopping) and no decay (backward hopping). These results interpreted in continuum limit would mean that the optimal stochastic process (within OU processes) for minimizing the CV of FPT for a given mean is the drift-diffusion process. In other words, the optimal control is a feedforward controller and requires no state feedback. In this paper, we explore this control problem in more detail.

Although the FPT properties of OU processes have been extensively studied in the literature [16], a control theoretic analysis of how the process can be steered to some desired FPT statistics is lacking. This paper provides an unified approach based on characteristic functions to find control parameters that lead to desired FPT distributions. The approach is analytically and numerically tractable and provides important insights into the FPT behavior of the OU process. The major contributions of this paper are threefold. First, we show that the FPT distribution for OU process is scale-invariant with respect to drift parameter, which facilitates independent tuning of the mean and CV of the FPT. Second, using the characteristic function of the FPT, we explore the space of control parameters to understand the variation of the FPT statistics with these parameters. Third, we determine optimal control parameters to achieve desired FPT statistics.

The paper is organized as follows. Section II introduces the problem. Section III presents background results on the characteristic function for the FPT of an OU process. Section IV uses the characteristic function to find properties of moments of the FPT, and optimal parameters that lead to desired moments. A more general control problem that explores the parameter space to reach a desired FPT distribution is studied in Section V. Finally, conclusions and future work are discussed in Section VI.

II PROBLEM DESCRIPTION

Consider an OU process defined by the following stochastic differential equation

[TABLE]

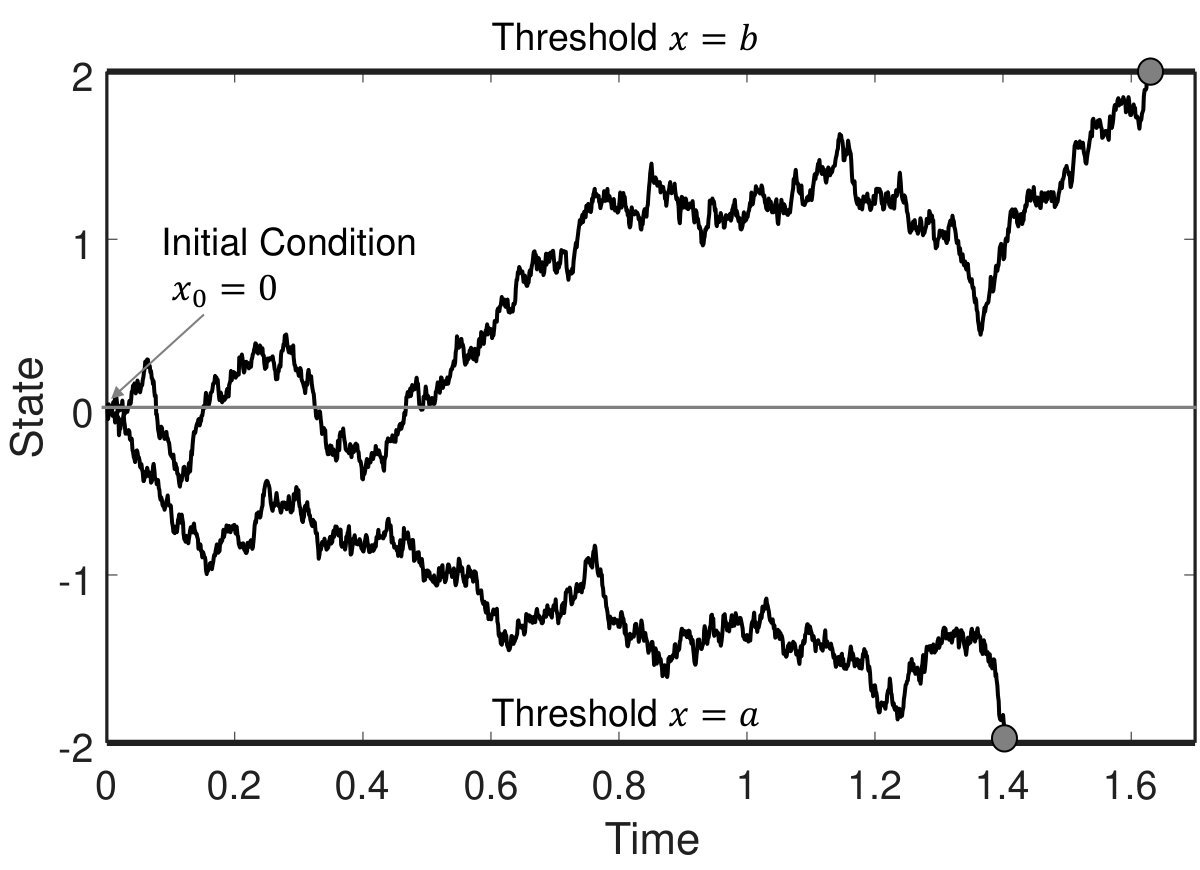

Here is the state, , and are parameters, and are i.i.d. Wiener increments. We will refer to as the drift and as the relative noise strength. Let and denote two thresholds such that . The FPT, , for to cross either of these thresholds is mathematically defined as

[TABLE]

Our aim is to investigate optimal drift and relative noise strength that lead to desired FPT moments. Such problems could be of relevance in many contexts wherein a desired mean FPT and at least a tolerable CV is required. This problem can be generalized further by demanding a FPT distribution that is as close to a desired distribution as it could be. The thresholds and could be both absorbing, or one absorbing and the other reflecting.

To handle these problems in an unified manner, we propose to use the characteristic function of the OU process. Not only the moments can be easily computed from the characteristic function, but it also provides a useful way to characterize the distance between two probability distribution functions. To be more specific, the characteristic function, , of the FPT, , is defined as

[TABLE]

A -th order moment can be computed as

[TABLE]

Furthermore, the following result due to Parseval–Plancherel provides a metric to quantify the difference between two probability density functions in terms of their characteristic functions: Let denote the probability density function of the FPT, and be a desired probability distribution function. The distance between these functions can be quantified in terms of their characteristic functions and as

[TABLE]

provided that the integrals exist [17].

III BACKGROUND RESULTS ON FPT OF AN OU PROCESS

In this section, we provide background results on FPT of the OU process (1). For completeness, we provide detailed computation of the characteristic function using standard tools from the theory of stochastic processes (see, [16, 18, 19, 12, 5]). We consider two thresholds at and , both of which could be absorbing or one of them could be reflecting.

III-A When both thresholds are absorbing

To derive the characteristic function, , for the OU process in (1), we define as

[TABLE]

where represents an initial condition, and denotes the FPT starting from an initial condition . Note that the characteristic function is related with as . The computation of using first principles is discussed below.

Consider the evolution of the OU process starting from in an infinitesimal time interval . Denote . It follows that

[TABLE]

Taking the limit results in

[TABLE]

We are interested in the solution to the above differential equation which can be obtained using the series method. Let

[TABLE]

Plugging this in (8) results in

[TABLE]

It is straightforward to see that (10) results in the following recursive relation in the coefficients

[TABLE]

The above recursion yields the following solution

[TABLE]

where is the Gamma function. A general solution to (8) can be given by (9), with the coefficients given by (12). Simplifying the series in (9) via symbolic manipulation in Mathematica yields

[TABLE]

where represents the Kummer’s confluent hypergeometric function.

The solution in (13) consists of two unknown coefficients and which can be computed using the boundary conditions. When both thresholds and are absorbing, the boundary conditions are given by and . Using these boundary values, and can be determined by solving

[TABLE]

Using these coefficients in (13) and evaluating results in the following for the characteristic function

[TABLE]

The hypergeometric functions can be converted to other special functions, such as Hermite functions, parabolic cylinder functions, etc. [20]. Results on FPT of OU are presented in some of these forms in standard texts [16].

Remark 1

If the FPT characteristic function is desired for a single threshold, it could be computed as a special case of the two threshold case analyzed here. There are two possibilities: either the initial condition is above the threshold, or below it. If the initial condition is above the threshold, then we may analyze this case as two thresholds case by letting the threshold at , and considering as our threshold of interest. In the other case when the initial condition is below the threshold, then we let and assume the threshold of interest at .

Remark 2

Recall our definition of the FPT for two threshold case given in (2). The initial condition there is assumed to lie between the thresholds and . If that were not the case, then the thresholds problem also becomes a single threshold problem. More specifically, if , then the process will always reach before . Therefore, the FPT is same as that for a single threshold at . Analogously, if , then the process will hit the threshold before the threshold , and the FPT is same as that for reaching a single threshold at .

III-B When one of the threshold is reflecting

Another possible situation of interest arises when one of the thresholds is reflecting. For example, we could assume that the threshold at is not absorbing and the process is reflected back as soon as it hits . We are interested in computing the characteristic function of the first time at which the process reaches the threshold .

The computation follows the same principles as those for the two threshold case, and therefore reduces to solving the differential equation (8) for . The general form of the solution in (13) can be used in this case, with appropriate boundary conditions given by and (see [19, 12] for more details). Note that if the absorbing threshold is at and is the reflecting threshold, then we will have the boundary conditions and . We do not analyze this case here.

Let us denote the FPT characteristic function . Using the initial conditions to compute and in (13) and then evaluating results in the following for the characteristic function

[TABLE]

So far we have computed the characteristic functions for FPT of OU process in various scenarios. The characteristic function can now be used to explore how various parameters affect the FPT statistics, and how they could be tuned to achieve desired FPT behavior.

IV OPTIMAL PARAMETERS FOR DESIRED FPT MOMENTS

In this section, we investigate the effect of various parameters of the OU process on the FPT moments. Then, we examine how the parameters could be tuned so as to get a desired FPT moments.

IV-A Scale invariance of the FPT distribution

In the previous section, we derived characteristic functions of FPT distribution of the OU process under different scenarios (both thresholds absorbing or one of them reflecting). More generally, the characteristic function for other scenarios can also be derived from the generalized form in (13), with appropriate boundary conditions. An important point to note is that in both (15) and (16), the drift parameter always appears with (as in ). Therefore, if we consider the rescaled variable , and find a general form similar to (13), it would be given by

[TABLE]

Thus, the general solution for the rescaled variable would not depend on . As the coefficients and above are obtained from boundary conditions, they would also be independent of .

An alternate way to infer this feature is to look at (1). As is of the order of , we can rescale time by (as in ) and rewrite (1) as

[TABLE]

Because does not appear in the new time scale, the characteristic function of the FPT with this rescaling should be independent of as well.

To understand the implications of this property, consider the characteristic function of the rescaled variable

[TABLE]

Since does not appear in the above characteristic function, all moments of are independent of . Furthermore, because , we have that

[TABLE]

Since does not depend upon upon , this implies that

[TABLE]

and appropriately scaled moments of the FPT, , are independent of . It follows that if we operate with normalized higher statistical moments such as the coefficient of variation (CV), skewness, kurtosis, etc, then changing the drift parameter only changes the mean FPT . The scale invariance has been observed in distributions of other quantities [21], and also of FPTs in other contexts [5, 22, 23].

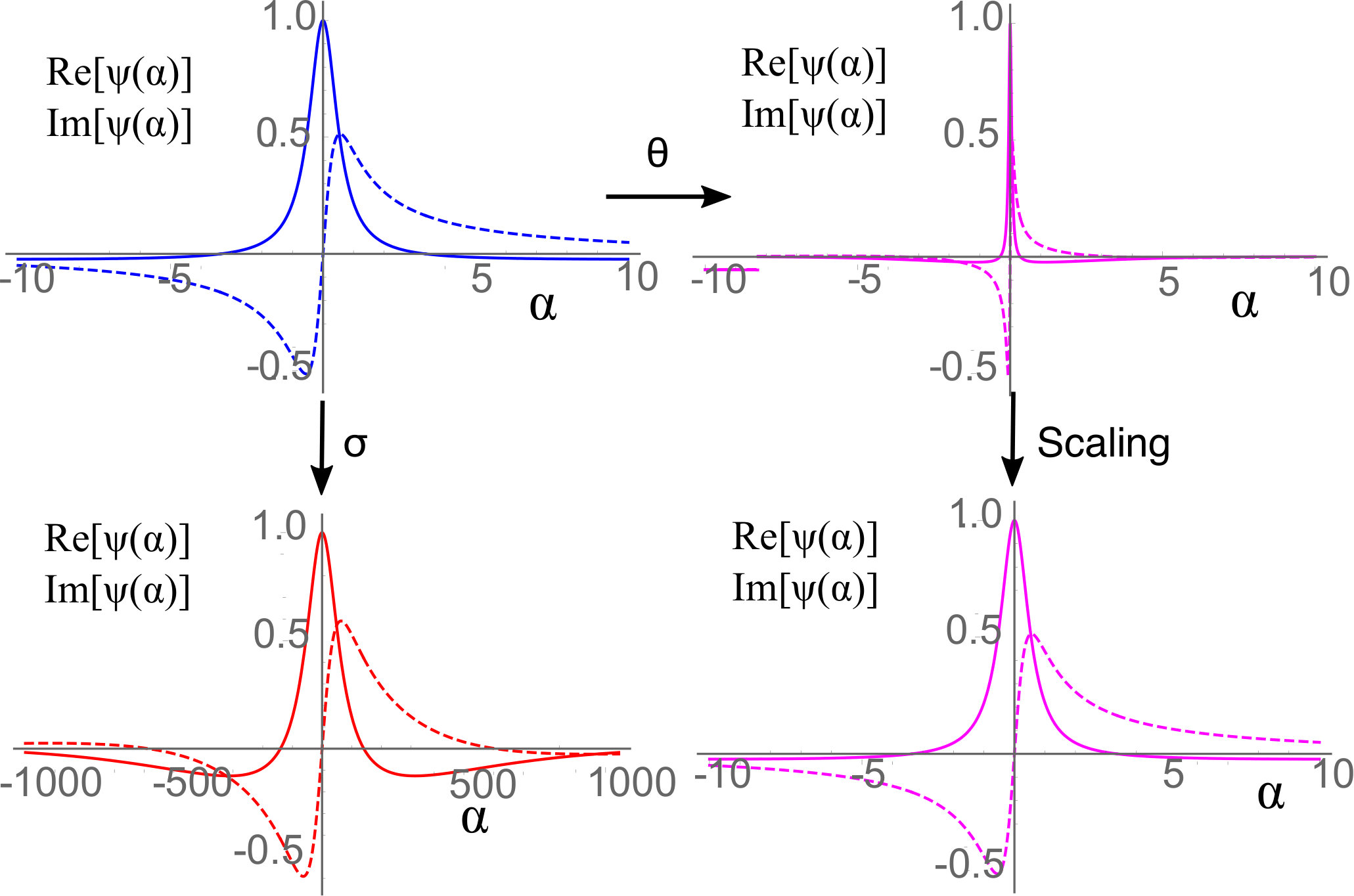

In terms of the characteristic function, we illustrate the scale invariance property in Fig. 1 for the case when both thresholds are absorbing. The real and imaginary parts of the characteristic function are plotted for the FPT. By varying the drift parameter , the characteristic function does not change in shape and just scales with respect to the axis. However, changing the relative noise strength affects the shape of the characteristic function. Similar behavior is also seen in the case when one of the thresholds is reflecting, though the results are not shown in order to avoid repetition.

IV-B Tuning FPT moments

Recall the form of (1). Suppose that we are interested in tuning the two parameters ( and ) of the process so as to get desired moments of the FPT. Since only changes the mean, and the other quantities of interest (such as coefficient of variation (CV), skewness etc.) are independent of it, one could independently tune the mean FPT and one other quantity. Typically, the CV is the other quantity of interest because it represents the noise in the FPT.

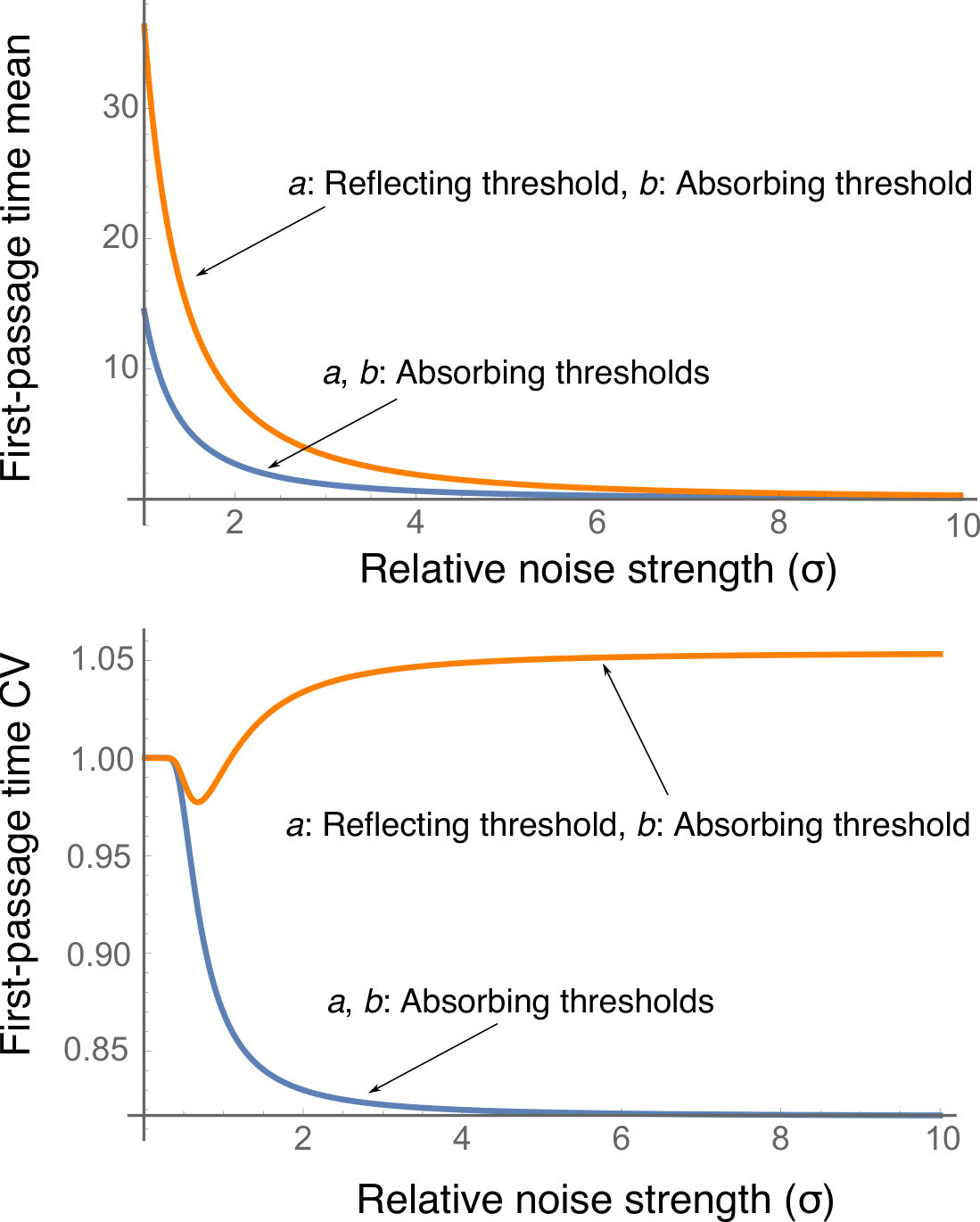

What remains to be seen is how the relative noise strength affects the mean and CV of the FPT. One could then choose appropriate such that the CV is at a desired level, and then tune to get the desired mean. It turns out that both the mean and CV are decreasing functions of for the two absorbing thresholds case. The CV eventually approaches to a limiting value

[TABLE]

which corresponds to the CV of the FPT for a diffusion with zero drift. In case when the threshold at is reflecting, the mean still decreases with increase in . The CV, on the other hand, shows a slight dip before increasing to a limiting value

[TABLE]

that corresponds to the CV of the FPT for a diffusion with zero drift.

Collectively, these results show that if one were to tune , and then any desired mean FPT could be achieved, but there is a limit to the achievable CV. Achieving a low CV in the double thresholds case requires a high value of whereas for the case when one the barriers is reflecting, there is an optimal that minimizes the CV.

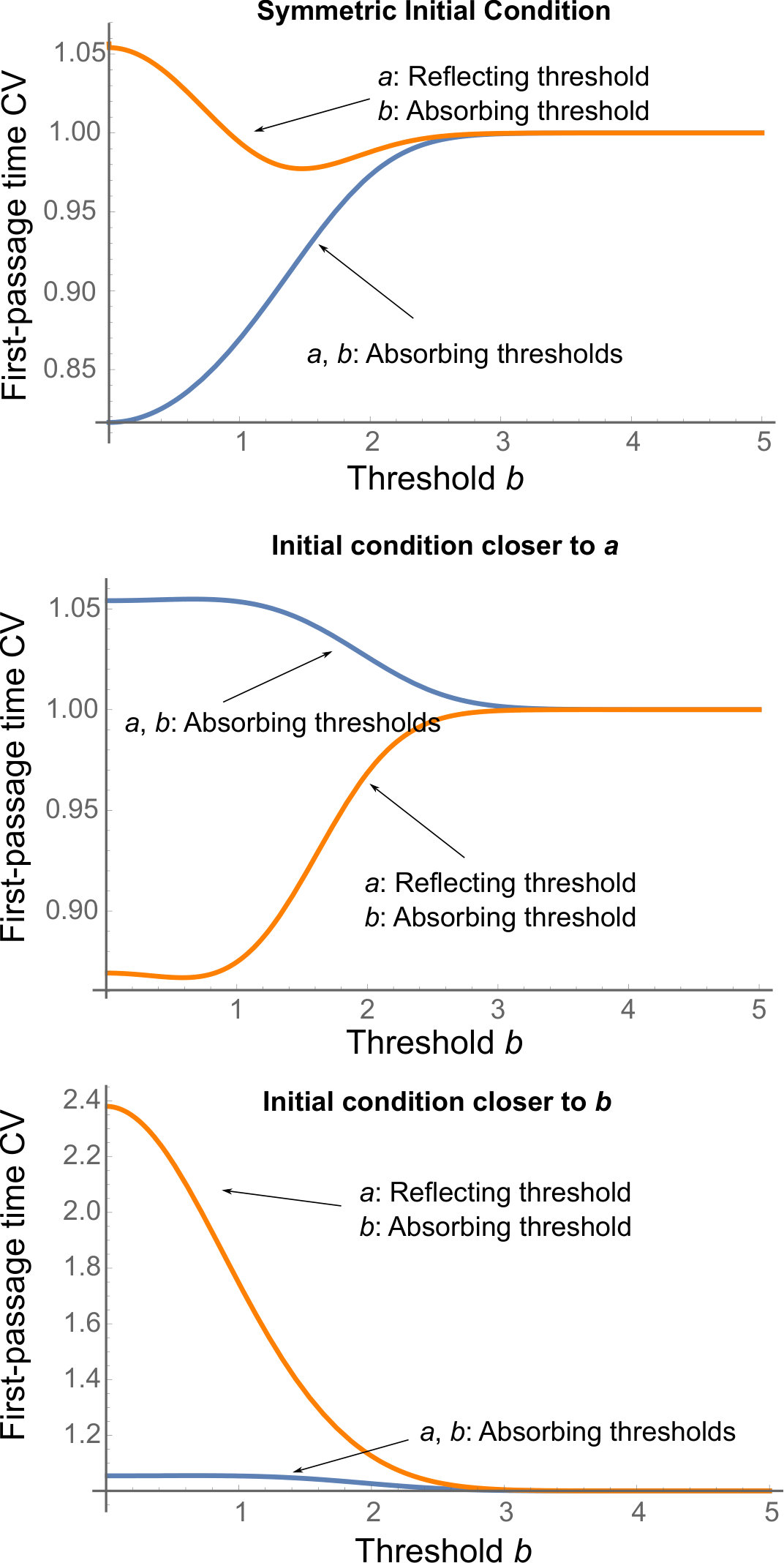

IV-C Effect of thresholds and initial condition

Our analysis thus far has assumed fixed thresholds and a given initial condition. In Fig. 3, we examine how the results change when one of these parameters are changed. As a first case, we consider a symmetric thresholds, i.e., , and the initial condition to be at . In this case, increasing leads to increase in CV of FPT if both thresholds are absorbing. In contrast, if is considered to be reflecting, then there is an optimal threshold at which the CV hits a minimum. Increasing the threshold beyond a certain point does not affect the CV anymore. This corresponds to the situation when the absorbing threshold(s) is far from the initial condition and crossing it is dominated purely by noise (see Fig. 3, top).

Next, we consider the case when the initial condition is not symmetric. Assuming the threshold to be , we take two cases: and . When both and are absorbing, increasing the threshold decreases CV of FPT and the CV seems to approach the limit of symmetric initial condition (Fig. 3, middle and bottom). However, when the threshold is taken as reflecting, then the CV properties change depending upon . More specifically, when is near the reflecting threshold, then increasing the threshold increases CV. In contrast, when is near the absorbing threshold, then increasing the threshold leads to reduction in CV of FPT.

To sum up, the FPT distribution for an OU process is scale invariant with respect to the drift parameter, and thereby allows independent tuning of the mean FPT and another statistical quantity that consists of appropriately scaled moments of the FPT. If one is interested in obtaining a FPT distribution that matches more than two statistical quantities of interest, it is not possible. A question of interest at this point is how close can the FPT distribution get to a given distribution?

V OPTIMAL PARAMETERS FOR DESIRED FPT DISTRIBUTION

Suppose that instead of tuning the moments, we are interested in tuning the distribution of the FPT itself. More specifically, we are interested in choosing the parameters such that the FPT distribution is as close to a desired distribution as possible. In this section, we discuss the tuning of OU process to achieve such behavior.

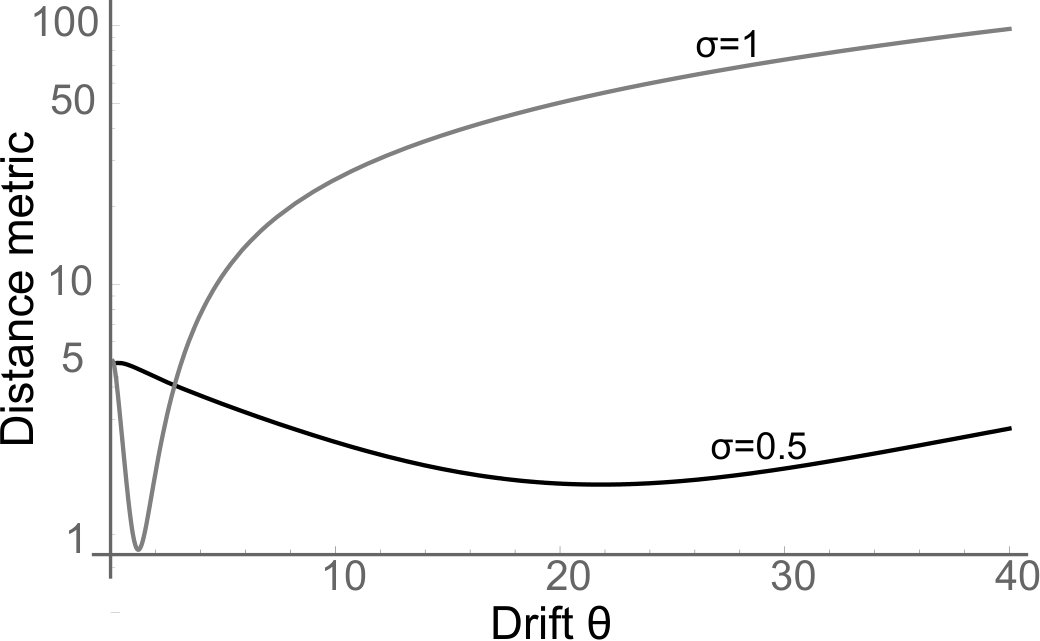

To this end, we consider the relation between probability density function and the characteristic function stated in (5). Although the desired distribution could be specified as any distribution of interest, we consider the Gamma distribution here. The rationale behind this is that the Gamma distribution is that it is the distribution of a summation of exponential random variables and in a limiting case, it can even represent a degenerate (deterministic) distribution.

In Fig. 4, we assume both thresholds to be absorbing and plot the distance metric between the desired distribution and the FPT distribution as a function of . The value of is taken to be fixed. It can be seen that there is an optimal value of that minimizes the distance metric. Furthermore, if is increased and this process is iterated, we see that the optimal value of decreases, and the minimum of the distance metric decreases as well. Referring to Fig. 1, it can be seen that fixing the value of basically fixes the shape of the characteristic function, and then by changing , an appropriate scale is chosen so that the characteristic function matches with the desired one. By iterating over , we change the shape of the characteristic function and find the optimal shape that matches the desired characteristic function with appropriate scaling . Even in the case when one of the boundary is reflecting, we get optimal parameters that minimize the distance metric. The results are not presented here to avoid redundancy.

VI CONCLUSION

The OU process is used to model stochastic phenomena in a variety of contexts. In particular, the FPT of OU process has been used to study decision-making [1], animal foraging [6], financial markets [9], and synchronization of clocks [7]. In this paper, we consider OU process with two thresholds. Both of the thresholds could be absorbing, or one of them could be reflecting while the other one is absorbing. We analyze the effect of OU process parameters on its FPT statistics, and how the parameters could be chosen to obtain a desired FPT statistics.

Future work will focus on analyzing the optimal parameters by not restricting to be positive, and thereby allowing the OU process to not just be mean reverting. Given the numerical tractability of characteristic functions, it would also be interesting to explore other stochastic processes the approach presented here and explore optimal/sub-optimal control strategies that result in desired FPT statistics.

The reference list from the paper itself. Each links out to its DOI / PubMed record.

- 1[1] R. Bogacz, E. Brown, J. Moehlis, P. Holmes, and J. D. Cohen, “The physics of optimal decision making: a formal analysis of models of performance in two-alternative forced-choice tasks.” Psychological review , vol. 113, p. 700, 2006.

- 2[2] H. C. Tuckwell and F. Y. M. Wan, “First passage time to detection in stochastic population dynamical models for HIV-1,” Applied Mathematics Letters , vol. 13, no. 5, pp. 79–83, 2000.

- 3[3] G. Vahedi, B. Faryabi, J. Chamberland, A. Datta, and E. R. Dougherty, “Intervention in gene regulatory networks via a stationary mean-first-passage-time control policy,” IEEE Transactions on Biomedical Engineering , vol. 55, no. 10, pp. 2319–2331, 2008.

- 4[4] S. Singh, D. J. Schneider, and C. R. Myers, “Using multitype branching processes to quantify statistics of disease outbreaks in zoonotic epidemics,” Physical Review E , vol. 89, no. 3, p. 032702, 2014.

- 5[5] S. Redner, A guide to first-passage processes . Cambridge University Press, 2001.

- 6[6] O. Bénichou, M. Coppey, M. Moreau, P. Suet, and R. Voituriez, “Optimal search strategies for hidden targets,” Physical Review Letters , vol. 94, no. 19, p. 198101, 2005.

- 7[7] W. Suwansantisuk, M. Z. Win, and L. A. Shepp, “First passage time problems with applications to synchronization,” in IEEE International Conference on Communications , 2012, pp. 2580–2584.

- 8[8] Z. Farkas and T. Fulop, “One-dimensional drift-diffusion between two absorbing boundaries: application to granular segregation,” Journal of Physics A: Mathematical and General , vol. 34, no. 15, pp. 3191–3198, 2001.