Using Aggregated Relational Data to feasibly identify network structure without network data

Emily Breza, Arun G. Chandrasekhar, Tyler H. McCormick, Mengjie Pan

TL;DR

This paper introduces a cost-effective method using Aggregated Relational Data (ARD) to infer network structures and statistics without collecting detailed network data, enabling broader research applications.

Contribution

The authors develop a novel approach that leverages ARD to estimate network parameters and characteristics, reducing costs and resource requirements compared to traditional network data collection.

Findings

Method accurately recovers network statistics in simulations.

Replicates results of field experiments using ARD alone.

ARD surveys are 80% cheaper than full network surveys in rural India.

Abstract

Social network data is often prohibitively expensive to collect, limiting empirical network research. Typical economic network mapping requires (1) enumerating a census, (2) eliciting the names of all network links for each individual, (3) matching the list of social connections to the census, and (4) repeating (1)-(3) across many networks. In settings requiring field surveys, steps (2)-(3) can be very expensive. In other network populations such as financial intermediaries or high-risk groups, proprietary data and privacy concerns may render (2)-(3) impossible. Both restrict the accessibility of high-quality networks research to investigators with considerable resources. We propose an inexpensive and feasible strategy for network elicitation using Aggregated Relational Data (ARD) -- responses to questions of the form "How many of your social connections have trait k?" Our method uses…

Click any figure to enlarge with its caption.

Figure 1

Figure 1 Figure 2

Figure 2 Figure 3

Figure 3 Figure 4

Figure 4 Figure 5

Figure 5 Figure 6

Figure 6 Figure 7

Figure 7 Figure 8

Figure 8 Figure 9

Figure 9 Figure 10

Figure 10 Figure 11

Figure 11 Figure 12

Figure 12 Figure 13

Figure 13 Figure 14

Figure 14 Figure 15

Figure 15 Figure 16

Figure 16 Figure 17

Figure 17 Figure 18

Figure 18 Figure 19

Figure 19 Figure 20

Figure 20 Figure 21

Figure 21 Figure 22

Figure 22 Figure 23

Figure 23 Figure 24

Figure 24 Figure 25

Figure 25 Figure 26

Figure 26 Figure 27

Figure 27 Figure 28

Figure 28 Figure 29

Figure 29 Figure 30

Figure 30 Figure 31

Figure 31 Figure 32

Figure 32 Figure 33

Figure 33 Figure 34

Figure 34 Figure 35

Figure 35 Figure 36

Figure 36 Figure 37

Figure 37 Figure 38

Figure 38 Figure 39

Figure 39 Figure 40

Figure 40| Estimated top decile | ||||

| Yes | No | |||

| True top decile | Yes | 18.16 | 6.84 | 25 |

| No | 6.84 | 218.16 | 225 | |

| 25 | 225 | 250 | ||

| Estimated top decile | ||||

| Yes | No | |||

| True top decile | Yes | 234 | 271 | 505 |

| No | 271 | 4012 | 4283 | |

| 505 | 4283 | 4788 | ||

| Estimated top decile | ||||

| Yes | No | |||

| True top decile | Yes | 234 | 271 | 505 |

| No | 271 | 4012 | 4283 | |

| 505 | 4283 | 4788 | ||

| Estimated top decile | ||||

| Yes | No | |||

| True top decile | Yes | 470 | 1167 | 1637 |

| No | 1167 | 13262 | 14429 | |

| 1637 | 14429 | 16066 | ||

| (1) | (2) | |

| Log Total Ending Savings | Log Total Ending Savings | |

| Signaling value of monitor with full network data (), Standardized | 0.248 | |

| (0.0931) | ||

| Predicted signaling value of monitor with ARD (), Standardized | 0.181 | |

| (0.0888) | ||

| Observations | 422 | 422 |

| Number of villages | 30 | 30 |

| (1) | (2) | |

| Belief about saver’s responsibility | Belief about saver’s responsibility | |

| Monitor centrality with full network data, Standardized | 0.0500 | |

| (0.0142) | ||

| Predicted monitor centrality with ARD, Standardized | 0.0340 | |

| (0.0161) | ||

| Observations | 4,743 | 4,743 |

| Number of villages | 30 | 30 |

| (1) | (2) | (3) | |

| Percent Supported (Data) | Percent Supported (Estimate) | Graph-level Proximity (Estimate) | |

| Treatment Neighborhood | -0.0655 | -0.0892 | -0.0463 |

| (0.0318) | (0.0532) | (0.0144) | |

| Constant | 0.4427 | 0.4404 | 0.4485 |

| (0.0644) | (0.0935) | (0.0096) | |

| Mean of the response variable | 0.3880 | 0.3129 | 0.4238 |

| Observations | 3,514 | 3,598 | 62 |

Peer Reviews

No public reviews on file for this paper yet. If you reviewed it on a platform where reviews are public (OpenReview, ICLR, NeurIPS, ICML), you can paste yours below so the community can read it here.

Videos

No videos yet. Explain this paper in a talk, walkthrough, or lecture? Add one.

Taxonomy

TopicsComplex Network Analysis Techniques · Social Capital and Networks

Social network data is often prohibitively expensive to collect, limiting empirical network research. We propose an inexpensive and feasible strategy for network elicitation using Aggregated Relational Data (ARD) – responses to questions of the form “how many of your links have trait ?” Our method uses ARD to recover parameters of a network formation model, which permits the estimation of any arbitrary node- or graph-level statistic. We characterize both theoretically and empirically for which network features the procedure works. In simulated and real-world graphs, the method performs well at matching a range of network characteristics. We replicate the results of two field experiments that used network data, and draw similar conclusions with ARD alone.

JEL Classification Codes: D85, C83, L14

Keywords: Social Networks, Bayesian methods, Partially observed networks

Using Aggregated Relational Data to feasibly identify network structure without network data

Emily Breza*†*

,

Arun G. Chandrasekhar*‡*

,

Tyler H. McCormick*§*

and

Mengjie Pan*⋆*

(Date: This version .)

We thank Liran Einav, Paul Goldsmith-Pinkham, Abhijit Banerjee, Esther Duflo, Axel Gandy, Ben Golub, Rema Hanna, Guy Harling, Jeff Eaton, Matthew Jackson, Michael Kremer, Rachael Meager, Betsy Ogburn, Elie Tamer, Tian Zheng and participants at various seminars/conferences who provided helpful comments. We also thank Shobha Dundi, Varun Kapoor, Devika Lakhote, Ambika Sharma, Sneha Stephen, Tithee Mukhopadhyay, and Gowri Nagraj for outstanding research assistance. This work is partially supported by grant SES-1559778 from the National Science foundation and grant number K01 HD078452 from the National Institute of Child Health and Human Development (NICHD). This material is based upon work supported by, or in part by, the U.S. Army Research Laboratory and the U.S. Army Research Office under grant number W911NF-12-1-0379.

*†*Department of Economics, Harvard University; J-PAL; NBER. [email protected]

*‡*Department of Economics, Stanford University; J-PAL; NBER. [email protected]

*§*Departments of Statistics and Sociology, University of Washington. [email protected]

*⋆*Department of Statistics, University of Washington. [email protected]

1. Introduction

There has been a groundswell of empirical research on social and economic networks.111See, e.g., Karlan, Mobius, Rosenblat, and Szeidl (2009); Centola (2010); Tontarawongsa, Mahajan, and Tarozzi (2011); Ligon and Schechter (2012); Cai, deJanvry, and Sadoulet (2013); Carrell, Sacerdote, and West (2013); Beaman, BenYishay, Magruder, and Mobarak (2016); Blumenstock, Eagle, and Fafchamps (2016); Alatas, Banerjee, Chandrasekhar, Hanna, and Olken (2016). Also see Chuang and Schechter (2015); Aral (2016); Boucher and Fortin (2016); Breza (2016) for overviews of empirical work using network data. Nonetheless, a major barrier to entry into this space is access to network data, which is often extremely costly to collect. A typical network elicitation exercise requires, (1) enumerating every member of the network in a census, (2) asking each subject to name those individuals with whom they have a relationship and in what capacity, and (3) matching each individual’s list of social connections back to the census. In field work, this can be difficult and expensive. Further, in other contexts, such as measuring networks of financial intermediaries or high-risk populations, proprietary data and privacy concerns may render steps (2) and (3) impossible. Moreover, this process needs to be repeated across many networks to conduct convincing inference. These barriers place significant limitations on conducting high-quality work in this space and discourage research, especially by those without access to considerable resources.

The contribution of this paper is to present a technique that makes network research scalable and accessible on a budget. We propose that researchers collect aggregated relational data (ARD). ARD are responses to questions of the form

“Think of all of the households in your village with whom you ¡¡INSERT ACTIVITY¿¿. How many of these have trait ?”

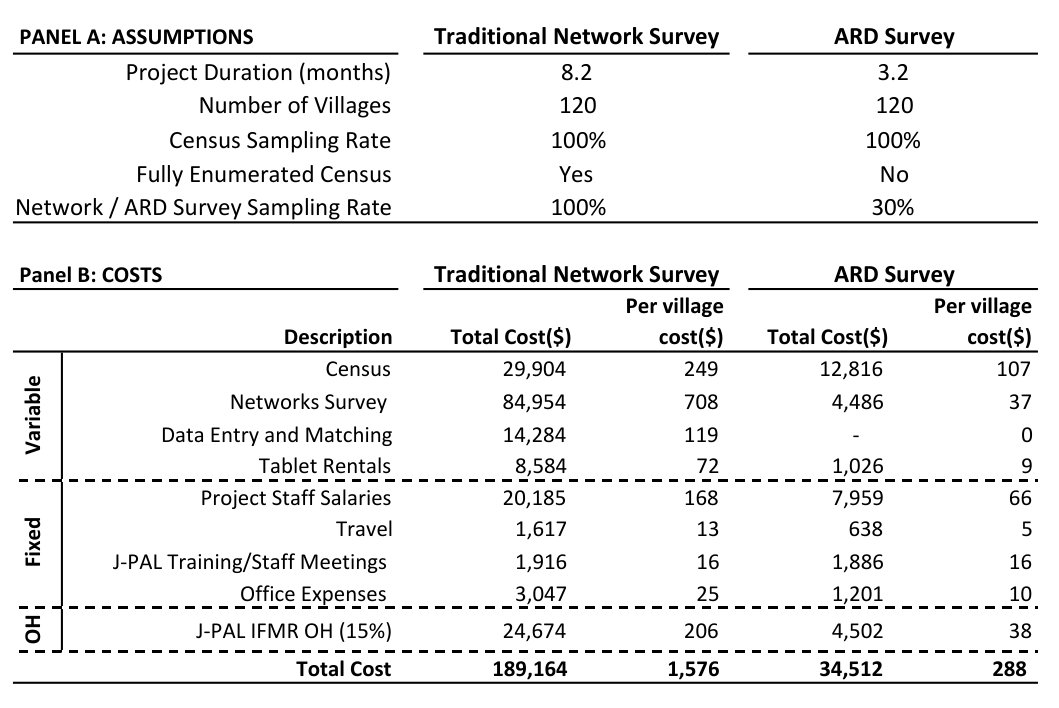

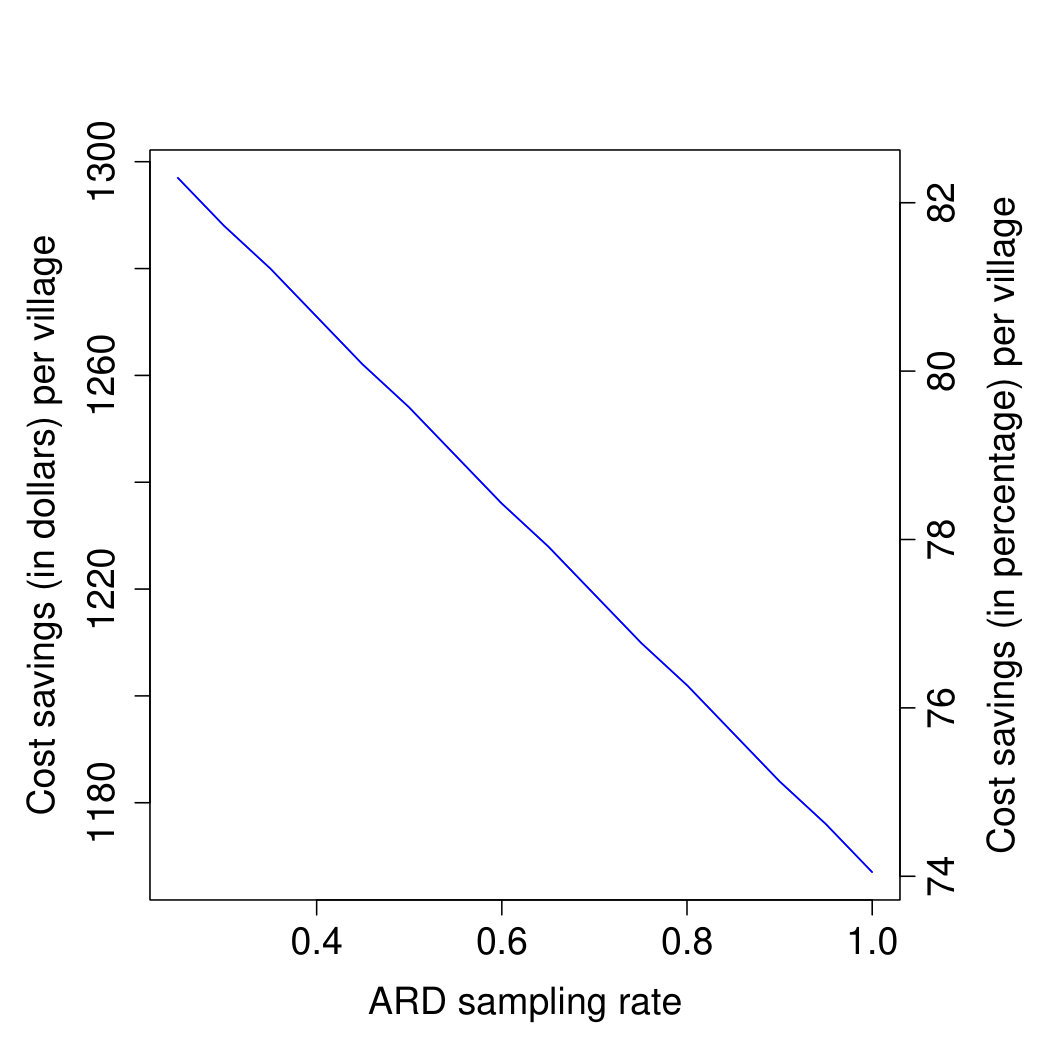

ARD is considerably cheaper to obtain than full or even partial-network data. We show, using J-PAL South Asia cost estimates, that collecting ARD leads to a 70-80% cost reduction.222While we present empirical evidence from village and neighborhood networks in India, the method can also be extended to other settings. See Section 8 for a discussion of applications to firm and banking networks.

Our proposed method is intuitive and comes down to the following three simple observations. First, ARD is considerably cheaper and easier to collect than network data. Second, ARD provides the researcher with enough information to identify parameters of an oft-used and standard network formation model in the statistics literature (see e.g. Hoff et al. (2002)). The argument builds on prior work by McCormick and Zheng (2015), which shows how the network formation model is related to a likelihood that depends only on ARD. We describe this and present an identification argument. Third, this parametric model of network formation is sufficiently rich to capture a number of features of real-world network structures, as we demonstrate through myriad simulations and empirical exercises. We characterize both theoretically and empirically for which network features the procedure works well.

We examine the performance of our method for estimating functions of the graph in several ways. First, develop a straightforward theoretical taxonomy, confirmed by empirical evaluation, that gives intuition about when the method will work under correct specification. Using a battery of simulations we show that we are able to guess what the underlying network structure looks like from the ARD, even as we vary the sparsity/density of the network, the size of the network, and the sampling share to a reasonable degree.

Of course, real-world network data need not have been generated by the data generating process of our network-formation model. So we next consider an example where we have complete network data in nearly 16,500 households across 75 villages in Karnataka, India (Banerjee, Chandrasekhar, Duflo, and Jackson, 2016c). We show that had we collected ARD in these villages, even on a sample of 30%, we would have been able to estimate reasonably-well a variety of features of the network that economists care about.

We then provide two examples of recent research where either full or partial network data had been collected. Breza and Chandrasekhar (2016) study how the observation of one’s savings behavior by more central individuals in the network leads to greater savings in order to maintain a reputation for being responsible. We show with constructed ARD, we can replicate the paper’s findings. Banerjee, Breza, Duflo, and Kinnan (2016a) use partial network data to study how exposure to microcredit erodes social capital by reducing support. The authors in part collected survey ARD in this sample, and we show we can replicate the findings. Further, the ARD enables conclusions about how microcredit exposure affected the neighborhood-level informal financial network structure. These examples show the effectiveness of our approach across different contexts and how ARD would have helped in policy-relevant empirical work. Researchers could have reached their conclusions without collecting full network data, which also means that the financial barrier to entry for such research would be considerably lower, thereby democratizing in part this research frontier.

We present a sample budget for survey data collection of full network data in 120 villages. Collecting ARD reduces the costs by approximately 70-80%, depending on the sampling rate, using budgets prepared by J-PAL South Asia. While direct measurements of the network are always preferable to any estimation protocol, our calculations demonstrate that our proposed method can substantially expand the scope for and access to empirical networks research.

Overview of method

For the bulk of the paper, we consider settings where we have ARD for a randomly-selected subset of nodes in the network and a basic vector of covariates for the full set of nodes. ARD counts the number of links an agent has to members of different subgroups in the population. The core insight of our approach is that by combining ARD with a network formation model, we can derive the posterior distribution for the graph. To do this, we assume a network formation model, which we refer to as the latent distance model, where the probability of a connection depends on individual heterogeneity and the positions of nodes in a latent social space (Hoff et al., 2002). The distance between nodes in the space is a pair-specific latent variable that is inversely related to the probability of a tie: nodes that are closer together in the latent space are more likely to form ties. The propensity to form ties across pairs is assumed conditionally independent given the latent variables. ARD gives us information on where different subgroups lie relative to one another in this latent space. That is, ARD allows us to triangulate the relative locations of nodes. In prior work, McCormick and Zheng (2015) show how to relate the network formation model to a likelihood that depends only on ARD. We extend that result and show how we can recover the parameters of the network formation model. In our case, this consists of both individual-level effects for every node in the sample as well as the location of all nodes in the latent-space. Using a Bayesian framework for inference, we show that the choice of prior distribution has minimal impact on our ability to accurately recover moments for a variety of network configurations. We note that, equipped with estimates of the degree distribution as well as the latent space locations in the ARD sample, we can use the demographic covariates for the entire sample to estimate the degree, fixed-effects, and latent locations for the entire population. We can then draw from the posterior distribution over graphs given the ARD response vector and compute network statistics based on these posterior samples.

Figure 1 provides a simple illustration from one neighborhood in Hyderabad, India, where we collected ARD. The figure plots the positions on the latent surface, here a sphere, of six characteristic groups: households with histories of arrests, remarriages, members working abroad (likely in the Middle East), government employees, and twins. Several patterns emerge in this example. First, people tend to have joint knowledge of households with arrests and remarriages, consistent with both characteristics carrying negative social stigma. Second, the arrested population is tightly correlated in space in comparison to other groups, indicating more extreme heterogeneity in the number of arrested individuals respondents know. Third, people who know individuals with government employment also often know people who have household members abroad, again consistent with the local context where both government jobs and foreign migration require connections and lead to higher incomes.

The attractive features of our approach are not without costs. Our approach is parametric, relying on guessing the network structure through the pseudo-true parameters of the latent distance formation model estimated from ARD. It can do no better than the best latent distance model at capturing the likely distribution that generated the network. It cannot, for example, represent clustering in a way that violates the triangle inequality.333For an example of a network formation model which can do this, see Chandrasekhar and Jackson (2016). To see this, consider a two-dimensional Euclidean space with four groups that have equal probability of cross group interaction. If the data generating process has this feature, we will not capture it well.

Relation to the literature

Our work contributes to and builds on several literatures. First, there is a nascent literature that seeks to apply the lessons from the economics of networks without having access to network data (e.g., Beaman et al. (2016), Banerjee et al. (2016c), and Chassang et al. (2017)). These methods are limited because they only speak to identifying central individuals or focus on proxies. Prior work shows that proxies such as geography or ethnic divisions do not capture the network well and augmenting sampled network data, which works, can still be expensive (Chandrasekhar and Lewis, 2016). Our approach does not restrict the researcher to inferences about one specific aspect of the data, instead providing a blueprint to recover a distribution over the entire graph at minimal cost.

Second, our work builds on a sizable literature on ARD, but expands both the context and inferential quantities of interest. In contrast to our work, most previous work on ARD focused on estimating the size of “hard-to-reach” populations (see e.g. Killworth et al. (1998) or Bernard et al. (2010)). These groups consist of individuals who are outside the sampling frame of most surveys. Rather than needing to reach these individuals directly, using ARD allows researchers to study individuals through their interactions with others who are captured by more traditional sampling strategies. Bernard et al. (2010) use ARD to estimate the number of individuals impacted by an earthquake whereas Kadushin et al. (2006) use ARD to estimate the number of individuals using heroine.444Perhaps the most common use of ARD is to estimate the number of individuals who are considered high risk for HIV/AIDS (e.g., Maghsoudi et al. (2014), Guo et al. (2013), Ezoe et al. (2012), Salganik et al. (2011)).

The primary tool for estimating population size with ARD is the Network Scale-up Method (N-Sum) and variations thereof. Say the goal is to estimate the number of injection drug users in the population. If a respondent reports knowing two injection drug users out of one-hundred total contacts, then approximately two percent of the respondent’s network consists of individuals who are injection drug users. If the respondent’s network is characteristic, then in a population of 300,000,000 individuals, this would mean there are about 6,000,000 injection drug users. Recent work has paid attention to estimating other features of the network555Zheng et al. (2006) estimate heterogeneity in the propensity to know members of groups, or overdispersion., but the majority of work on ARD still focuses on estimating population sizes. As we do not focus on populations that are hard-to-reach, we can ask directly about whether a respondent is a member of a group to estimate population sizes. This distinction is essential for “scaling” a respondent’s degree. If the size of each ARD group and the total population are known, we can use the N-Sum logic to estimate individuals’ degrees.

The closest related work from the ARD literature is McCormick and Zheng (2015) – here, we use the same network formation model and build on derivations that are the key contribution of that work. Specifically, McCormick and Zheng (2015) show that, for a specific formation model, it is possible to arrive at a likelihood that is informed by information in ARD. That is,they interpret and do inference on a likelihood for ARD. While we also have this likelihood, in our work it is merely an intermediate step. In our paper, we perform inferences about the parameters of the formation model itself. By explicitly making the link to the formation model, we can generate graphs and compute both graph and individual level statistics.

Third, our latent surface model666In the context where the goal is inference about a regression coefficient that varies based on network connections, Auerbach (2016) presents a more general framework that links network formation to a function of distance between unobservable social characteristics that drive formation. is closely related to the -model (Holland and Leinhardt, 1981; Hunter, 2004; Park and Newman, 2004; Blitzstein and Diaconis, 2011) and the properties examined in Chatterjee et al. (2010) and Graham (2017). Every node has a fixed-effect. Links form conditionally independently given the fixed effects of the nodes involved, modulated by a function of distance between the nodes in a latent space. Relative to the Graham (2017) and Chatterjee et al. (2010) models, our model places nodes in a latent space (as in Hoff et al. (2002)), which we are trying to estimate, whereas the former only allows for observable covariates, and the latter has none. Whereas previous approaches consider an asymptotic frame based on a growing graph, we consider an explicitly sampling-based framework. We empirically compare our proposed model to the beta model in Appendix E.

Organization

We begin with an overview of our method for an applied researcher in Section 2. Section 3 presents the full framework, model, and estimation algorithm. In Section 4 evaluates when, and how well, the method performs using simple theory and a variety of simulated graphs. Section 5 shows how our method works when we apply it to 75 village where we have complete network data. In Section 6, we apply our results to two empirical examples. Section 7 demonstrates the 70-80% cost-savings of ARD versus full network elicitation. Section 8 concludes.

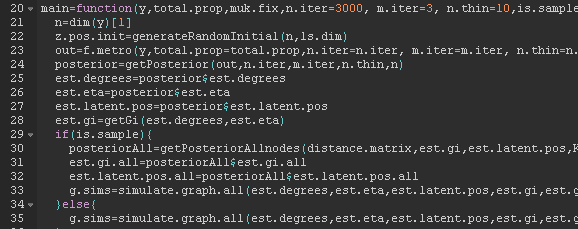

2. Overview of Method

We begin with a simple overview of the proposed method. Suppose that a researcher is interested in studying networks in a set of rural villages. A village network with households is given by , which is a collection of links where if and only if households and are linked and otherwise. To fix ideas, suppose that the researcher wants to learn how some outcome variable is related to a network statistic (or a vector of statistics) of interest . Or, perhaps the researcher is interested in how a treatment (such as exposure to microcredit) affects features of network structure, .

Our procedure takes five steps.

- I.

Conduct ARD survey: Sample a share (e.g., 30%) of households. Have each enumerate a list of their network links.777Note that this gives a direct estimate of the respondent’s degree. The method laid out in Section 3 does not require this and can also produce estimates for expected degree based on the ARD responses alone. Ask 5-8 ARD questions, such as

“How many households among your network list do you know where any adult has had typhoid, malaria, or cholera in the past six months?”

The ARD response for a household is

[TABLE]

where trait denotes the disease question. This just adds up all friends that have had the diseases over the last six months. We include a sample ARD questionnaire in Online Appendix B.4. 2. II.

Conduct census exercise: Obtain basic information about the full set of households in the village in a very rapid survey (denoted for all ).

- •

Minimal demographics: e.g., GPS coordinates, caste/subcaste.

- •

ARD traits: e.g., whether the household has had typhoid, malaria, or cholera in the past six months.

A sample census questionnaire is in Online Appendix B.3. 3. III.

Estimate network formation model with ARD: Use the information from the ARD survey and the population counts from the census to estimate the parameters of a network formation model. In this model, the probability that two households and are linked depends on household fixed effects () and distance in some latent space (latent locations ) with

[TABLE]

- •

Fit a model to predict using in the ARD sample.

- •

Predict using for all households in the census but not in the ARD sample.

Equipped with estimated fixed effects and latent locations for all households in the network, the probability of any network being drawn is fully computed. The code is freely available and discussed in Section B.5. 4. IV.

Compute network statistics of interest: Use the estimated probability model (using , fixed effects and latent locations ) to compute . The code is freely available and discussed in Section B.5.888Note that here, the method produces estimates of the latent locations of each node, which may themselves be useful for some research questions. 5. V.

Estimate economic parameter of interest: E.g., run regressions such as

[TABLE]

though clearly one can do more complex exercises once one has estimated the above network formation model.

3. Model and Estimation

In this section, we present formally the procedure outlined above. This includes defining ARD, introducing the network formation model, linking explicitly the formation model to the ARD, and finally, outlining how to generate graphs from that network formation model.

3.1. Setup

We begin by describing the underlying graph and the ARD. Let be an undirected, unweighted graph with vertex set and edge set , with nodes. We let . We also assume that researchers have a vector of demographic characteristics, for every .

Finally, we assume that the researcher has an ARD sample of nodes which are selected uniformly at random (where we define ). These could be the whole sample, with , or a smaller share, and will depend on the context. It is useful to define to be the ARD sample set and .

Formally, an ARD response is a count to a question “How many households with trait do you know?” which we can write as

[TABLE]

where is the set of nodes with trait . That is, is a count of the number of households in group that person knows. Note that throughout we assume that we observe and, in some cases, additional information about the group of people with trait (e.g., the number of households with this trait in the population), but we do not observe any links in the network.

It is easy to see how this could be applied to firm or banking network data. In the firm case, is the directed, weighted supply-chain network, which is of course not observed by the researcher. would be set of firms in sector and would be the volume of transactions between firms and . Here and are the total volume of directed transactions (inputs/outputs) between firm and firms in sector . For the remainder of the paper, we proceed with the example of a social network survey, however.

3.2. Latent surface model

The setup and model we use is from McCormick and Zheng (2015), motivated by, among others, Hoff et al. (2002). We model the underlying network as

[TABLE]

where are person-specific random effects that capture heterogeneity in linking propensity.999While we develop our methodology for this specific network formation model, we should note that it is likely possible to use ARD and other components of our method alongside a range of other formation models. While generalizing the method is outside the scope of this paper, we do view it as an avenue for future work, especially in real-world settings where researchers have a strong preference for alternative models. The set of nodes occupy positions on the surface of a latent geometry. As in previous latent geometry models in the statistics and machine learning literatures, the distance between nodes on the latent surface is inversely proportional to their propensity for interaction, parsimoniously encoding homophily. Using a distance measure preserves the triangle inequality, thereby generating likely triadic closure. That is, if the position of node is close to that of node and node is close to node , then the triangle inequality limits the distance between and . As we show below, equipped with the latent space terms, the model has features akin to random geometric graphs where clusters of nodes that are nearby are more likely to link, capturing realistic clustering patterns (Penrose, 2003). For further discussion of the properties of this class of model see Hoff (2008). In our case, we use latent space positions on the surface of dimensional hypersphere, . As described below, the hypersphere has both conceptual and computational advantages when working with ARD. Finally, modulates the intensity of the latent component.

We use a Bayesian framework and, therefore, complete the model by specifying priors on the model components. We begin with the latent space. As in McCormick and Zheng (2015), we model priors for latent positions on as

[TABLE]

where denotes the von Mises-Fisher distribution across .101010Informally, the von Mises-Fisher distribution can be thought of as follows. If the concentration parameter is large. It is similar to a normal distribution on the sphere in that it is unimodal and symmetrically dissipating in distance from the center (though it should not be confused with the wrapped normal distribution or other projection of the normal to a sphere). If the concentration parameter is small, it is essentially uniform over the sphere’s surface. Here denotes the location on the sphere and is the intensity: means that the location is uniform at random, which makes sense since the ARD respondents are assumed to be drawn uniformly at random. The terms describe the latent positions of individuals who have a particular trait . For these groups, we estimate the center and spread of the distribution. The positions of these groups then triangulate the positions of individuals who have ARD. For individuals in the population without ARD data, we assign their positions based on the positions of individuals with ARD that have similar covariates.

Equipped with this, McCormick and Zheng (2015) show that the expected ARD response by for category can be expressed as

[TABLE]

where is the respondent degree and is the share of ties made with members of group , is the normalizing constant of the von Mises-Fisher distribution (which is a ratio depending on modified Bessel functions that is easy to compute with standard statistical software), is the angle between the two vectors (McCormick and Zheng, 2015). The expected number of nodes of type known by is roughly its expected degree scaled by the population share of the group, adjusted by a factor that captures the relative proximity of the node to the type in question in latent-space. Note that, in the above expression, both the distance between an individual and the center of the latent trait distributions and the concentration of the latent trait distribution influence the (expected) number of individuals know. Recall that our formation model only relies on the distance between individuals in the latent space. The positions of individuals, however, are estimated using the likelihood above, meaning that both the position and concentration are relevant for our formation model.

A key assumption in our formation model is that the propensities for individuals to form ties are conditionally independent given the latent variables. The likelihood for the formation model, conditional on the latent variables, is a Bernoulli trial for each pair. ARD, then, is the sum of (conditionally) independent Bernoulli trials, which we can approximate with a Poisson distribution. This allows us to compute the distribution of the ARD response, which will be distributed Poisson,

[TABLE]

Though the likelihood above relies only on ARD, it does not uniquely identify the formation model since estimates on the degree, , rather than the individual heterogeneity parameter . We can compute the expected degree as in (McCormick and Zheng, 2015),

[TABLE]

The virtue here is that this allows us to estimate for .111111Note that if in our ARD elicitation, we also collect information on each node’s degree, which we recommend, then we can use that information here, without needing to first estimate above. The logic is similar to that in Chatterjee et al. (2010) or Graham (2017): in a model like the -model, having a vector of degrees essentially provides the researcher with enough information to recover the vector of fixed-effects. If we take the above expression for each individual, then we have a system of equations with unknown terms ( terms and one ). Assuming that is well-approximated by the average of the ’s, we have a system with equations and unknowns and can, therefore recover individual terms using degree and the latent scaling term, .

To complete the model, we need priors for the remaining parameters. We propose Gamma priors for and with conjugate priors on the hyperparameters. Then if is the shorthand for all parameters, the posterior is

[TABLE]

Given the data, we can compute posteriors over degrees of nodes, their unobserved heterogeneity, population shares of categories, intensity of the latent space component in the network formation model, relative locations of categories on the sphere, and how intensely they are concentrated at these locations. So with any draw of , , and , we can generate a graph from the distribution in (3.1).

3.3. Identification

Before explaining how we go from the ARD sample to the full sample, we explain identification of the parameters in the model.121212Also see McCormick and Zheng (2015) for a discussion of identification as well as recommendations for the number of populations to fix based on the dimension of the hypersphere. Here we provide a simple intuition, followed by a formal statement with proof in the Appendix.

Figure 2 shows how the location and the concentration for category is intuitively identified assuming the latent geometry is a plane. Holding the location of three nodes fixed (here Tyler, Emily and Mengjie), and holding fixed their degree, the relative locations of categories (here Red, Green, and Blue) can be identified by placing their centers and controlling the concentration to match the Poisson rates observed in the ARD. To see that the concentrations of the Red, Green, and Blue trait groups are identified, consider what would happen if we changed the concentration of one of the groups. If we increased the concentration of the Blue group (i.e. decreased the variance), then we would need to move Mengjie (and Tyler and Emily) closer to the Blue group to preserve the overlap between Emily’s disc and the Blue group. Moving Emily closer to the Blue group, though, necessitates moving her away from the Red group, reducing her overlap with the Red group. We could try to compensate by decreasing the concentration (increasing the variance) of the Red group. We can’t do this, though, because doing so would change the overlap between Tyler’s disc and the Red group. Similarly the figure shows how the can be identified holding fixed the location and concentration of the various categories, since this affects . Because the likelihood only depends on the latent space through the distances between individuals and groups, we fix the location of the center a small number of groups to address the invariance to distance-preserving rotations.

The formal statement is as follows.

Theorem** 3.1****.**

For any by matrix of ARD responses , we have that only if , , , and .

We provide a formal proof of the theorem in Appendix A.1.

3.4. From ARD sample to Non-ARD sample

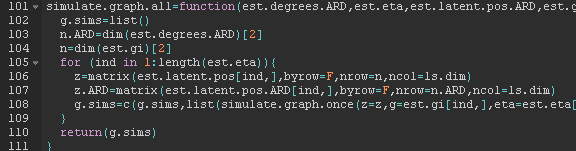

Thus far we only have posteriors for our ARD sample . We now turn to predicting and for . We use k-nearest neighbors to draw this distribution. Given demographic covariates for all , we define a distance between nodes in the feature space for . For each , we pick such that is among the k smallest distances. We then take a weighted average of and with weights inversely proportional to , to estimate and , respectively. We normalize such that to map it to the surface of the sphere. Thus, we have described a framework that a researcher can use with only ARD data and demographic covariates to take a sample of draws from a network formation latent surface model.

3.5. Drawing a graph

We now describe the algorithm used to generate a distribution of graphs . The algorithm for drawing graphs requires specifying the dimension of the latent hypersphere. Throughout the paper we follow McCormick and Zheng (2015) and use , for a three-dimensional hypersphere.131313We also investigate the performance of the method in real-world networks for in Appendix J and in Appendix K. This choice also facilitates visualizing latent structure. The posterior distribution is not available in closed form. We therefore use a Metropolis-within-Gibbs algorithm to obtain samples from the posterior. In the description below the jumping scale is tuned adaptively throughout the course of sampling. Specifically, every 50 draws we look at the acceptance rate of these draws and then adjust the scale of the jumping distribution. We follow the guidelines given in Gelman et al. (2013) and perform checks to ensure that our sampler has converged.

Algorithm** 1**** (Drawing Graphs).**

*Input: , .

Assume ARD groups, , such that . We propose fitting the model as follows (noting that steps 1 & 2 follow from McCormick and Zheng (2015)):*

- (1)

For a subset of the ARD groups, , fix . At each step we use these fixed positions in a Procrustes transformation141414Procrustes transformations are a class of transformation that use rotation, translation, or uniform scaling. Critically, they change the orientation and shape of an object but not the size.* (see Hoff et al. (2002)**) to rotate the latent space back to a common orientation.* 2. (2)

Repeat to convergence for

- (a)

For each , update using a random walk Metropolis step with proposal . Use the algorithm proposed by Wood (1994)* to simulate proposals.* 2. (b)

Update using a conditionally conjugate Gibbs step (Mardia and El-Atoum, 1976; Guttorp and Lockhart, 1988; Hornik and Grün, 2013). 3. (c)

*Update with a Metropolis step with *

. 4. (d)

Update with a Metropolis step with . 5. (e)

Update with a Metropolis step with . 6. (f)

Update with a Metropolis step with . 7. (g)

Update where . 8. (h)

Update where . 9. (i)

Update where . 10. (j)

Update where . 3. (3)

Repeat for

- (a)

Calculate such that satisfies . 2. (b)

Use method described in Section 3.4 to estimate and . 3. (c)

Sample graph using the the procedure described below.

Output:

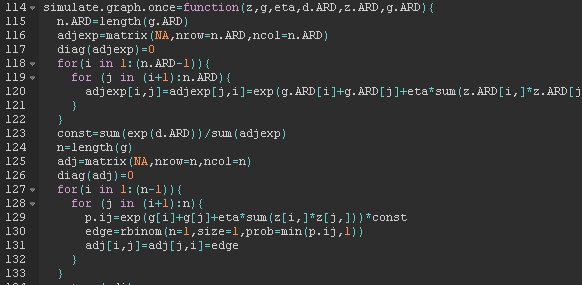

To generate graphs, recall that the formation model has . We estimate and using the likelihood derived in McCormick and Zheng (2015). The expression (3.3) relates degree to the unobserved gregariousness parameters, . If we approximate as the average of the ’s, then we can view (3.3) as a system with equations and unknowns and obtain estimates for for each respondent.

We then normalize the terms to produce probabilities. Define

[TABLE]

Normalizing in this way ensures Since the formation model assumes that the propensities to form a ties between pairs are conditionally independent given the latent variables, we can now generate graphs by taking draws from a Bernoulli distribution for each pair with probability defined by .

3.6. Discussion

3.6.1. Sensitivity to choice of prior distributions.

A natural question in any Bayesian analysis is how the modelers’ choices about prior distributions impact posterior inferences. In our context, the priors are influential in two settings. First, as explained above, we put priors directly on the parameters of the ARD likelihood. The ARD likelihood parameters then, in turn, determine the parameters for the network formation model. To evaluate the influence of the prior distributions on our ability to estimate the parameters of the ARD likelihood (and therefore formation model), we conduct a series of experiments presented in Appendix F. For the scalar and vector parameters (e.g., the individual degree, ) we examine the posterior distribution after varying the spread and center of the distribution of the prior. For the latent space locations, recall that we fix some population centers for identification. To ensure that our results are not sensitive to these choices, we perform experiments where we randomly choose both which ARD population centers we fix and where these groups are positioned on the sphere’s surface.

A second consideration in exploring our prior choices is the way that priors on the ARD likelihood parameters imply (via the formation model) priors on our network moments of interest. That is, we do not explicitly put a prior on centrality. The prior on centrality (and the other network moments) is, however, implied by the prior distribution placed on the parameters in the ARD likelihood. Appendix F presents a second set of results that show how the priors used for our model relate to the network moments of interest. We begin by simulating networks using the procedure above without any observed data. That is, we generate a series of networks entirely from the specified prior distributions. This series of networks demonstrates the wide range of possible networks that are supported by our formation model and the priors we specified. For context, we also plot the distribution of network moments from our estimated posterior distribution and from the observed data in Section 5.1.

3.6.2. Finite population and density

We have provided a simple algorithm to go from ARD questions to draws from the posterior distribution of the graph that would have given rise to ARD answers by respondents with characteristics similar to those we observed in the data. The model leverages a latent surface model similar to Hoff et al. (2002), used in McCormick and Zheng (2015), which is intimately related to the -model studied in Chatterjee and Diaconis (2011) and Graham (2017). One issue that has arisen from both the Bayesian and frequentest perspectives is the notion of density in the limit, or the rate at which the number of edges grows compared to the number of nodes. The Bayesian paradigm uses the Aldous-Hoover Theorem (Hoover, 1979; Aldous, 1981) for node-exchangeable graphs to justify representing dependence in the network through latent variables. This exchangeability assumption implies that a graph can be sparse if and only if it is empty (Lovász and Szegedy, 2006; Diaconis and Janson, 2007; Orbanz and Roy, 2015; Crane and Dempsey, 2015). From a frequentist perspective, Chatterjee and Diaconis (2011) show that the individual fixed effects (corresponding to, for example, gregariousness) can only be consistently estimated when the network sequence is dense.

In contrast to this previous work, however, we assume that our sample of egos arises from a population with fixed . That is, in our paradigm there is a network of finite size, , and we observe a small number of actors. We see the reliance on this assumption in, for example, our expression relating degree to the individual heterogeneity parameters, . Put a different way, there is no asymptotic sequence of networks. The number of edges in a graph still impacts estimation, however. Even when the number of nodes is large, we do not expect to uniformly converge to if the graph is not dense. This additional variability propagates through the model and inflates the posteriors of . These may be quite poor in practice, though it is difficult to derive the finite sample distribution. Nonetheless, what this suggests is that in cases where the network is too sparse, the ARD approach may be uninformative, and the researcher will see this plainly. This is the case for two reasons. First, by definition, anyone in the ARD sample will know fewer alters with trait since the network has fewer links on average. Second, there will be too much variation in our location estimates and degree estimates, which then will also affect our node heterogeneity estimates. This means that when the researcher faces rather diffuse posteriors, the network may be too sparse to convey much information. We explore these issues in simulations below.

4. How Well Does the Procedure Perform?

In this section we explore how well our procedure works under the assumption of correct specification. That is, we assume that the data-generating process is such that graphs are generated from the family of models described in (3.1). While taking a stand on the formation model permits tractability, it of course carries with it some well-understood limitations. We discuss these limitations and test the procedure in real-world network data from 75 Indian villages in Section 5. In Section 6, we further consider two different field experiments that used network data and ask whether using ARD alone would have allowed researchers to make similar conclusions.

Under the assumption of correct specification, and having demonstrated identification above, we cover two questions. The first is for which network statistics do we expect ARD to work well. That is, even if we knew the set of individual fixed effects and latent locations , when would we have sufficient information to recover the network statistics of interest or the economic parameters of interest in a regression. To do this, in Section 4.1 we develop the theory for a taxonomy of network features to classify when we would or would not expect recovery of the network features. We show a straightforward but informative result which says that if, for a sufficiently large graph, our statistic of interest for any random realization from the generating process will be close to its expectation, then we should expect the mean-squared error of our statistic to become negligible. We supplement this with simulations to show practical results as to which network statistics we can recover with low mean-squared error (MSE). Finally, we conduct a rich set of simulations to demonstrate across a number of network statistics how well the procedure works for a data-set that mimics real-world network data, in Section 4.2.

Second, our simulations explore the sensitivity of our results to important features of the environment. Empirical network data may vary in terms of their degree distribution: how sparse they are (the number of links on average relative to the network size) and whether they exhibit thick right-tails (there are some nodes who are extremely well-connected relative to all others). As such, in Section 4.3, our simulations explore the efficacy of our procedure as we vary sparsity and the inclusion of hyper-popular nodes.

Further, the researchers can decide how many nodes to include in their ARD samples. Accordingly, in Section 4.4, we look at how well the ARD procedures work as we vary the share of nodes that are sampled for the ARD questionnaire. We simulate networks from what we call a rural environment (a smaller graph of 200-500 nodes) and an urban setting (thousands of nodes) and vary the share of nodes for which we have ARD. This exercise helps to provide guidance for research designs incorporating ARD.

4.1. Theoretical insights on when ARD works

We first provide theoretical insights on which network features will be amenable to estimation using ARD. A core theme in this discussion is that the ARD model produces predicted probabilities of connections between pairs of individuals. To get network statistics, however, we must convert these probabilities into realizations of graphs and, therefore estimates of the expectations of graph characteristics across possible graphs. We investigate the impact of this feature of our procedure both theoretically and empirically.

For the theoretical exercise, we assume that data arise from a formation model of the form presented in (3.1). In addition, we assume that the ARD procedure tightly identifies the model parameters. 151515Recall our formal argument for identification in Section 3.3. These assumptions allow us to focus on when the expectation of the network statistic is sufficiently informative about any given graph realization. Under these assumptions, let denote the probability that nodes and are linked under the data generating process with parameter vector .

We separate our discussion into two cases: (1) the researcher has a single large network with nodes (or a handful of networks); (2) the researcher has many independent networks.

4.1.1. Single Large Network

We first consider the case where there is a single large network, and the researcher is interested in measuring a specific network statistic, for node computed on graph .161616This could easily be extended to functions of multiple nodes. For the purposes of this argument, there is one actual realization of the graph, . This realization is what we would have observed if we had collected information about all actual connections between members of the population, rather than collecting ARD. Importantly, the researcher collecting ARD cannot observe . This actual network realization does, however, come from a generative model that has parameters that can be estimated from the ARD. The researcher can, therefore, simulate graph realizations from the underlying data generating process under the true parameter vector, , and construct an estimate for . This expectation is over the possible graphs generated from the model with parameters . In practice, we will observe a matrix of ARD, , rather than . This expectation, then, is or, if part of the graph is observed as part of the data generating process (through e.g. an egocentric strategy), , where is missing completely at random with . As we describe in Section 3.3, the ARD data, , are sufficient to identify the generative parameters, . To simplify notation, we will omit the conditioning for the remainder of this section.

To recap, if a researcher collected information about all links in the population, she could compute directly. With ARD, however, she can recover an expectation over graphs generated with a given set of parameters, . We are interested in cases in which knowing is sufficient for learning about . That is, cases where, if we can get a good estimate for using ARD, we can say with confidence that we have recovered a statistic that is very similar to the statistic the researcher would have observed had she collected data on the entire graph. More formally, for any realized graph, , does

[TABLE]

If this condition holds, then when the population of individuals, , is large, the statistic of interest, , will be close to its expectation for any realization of the graph, including the one that is the researcher’s population of interest, . We have, therefore, that the statistic computed from the true graph and the statistic estimated using ARD are both close to the expectation and must, therefore, be close to each other and have small mean-squared error. Similarly, if the statistic from a given realization does not converge to its expectation, then even after more nodes are observed, there is not increasing information, and thus the mean-squared error of the estimate should not shrink. The key feature of the result is that we do not need to know the exact structure of the graph that the researcher would have observed using a network census, . Instead, we rely on the notion that the statistic will be close to its expectation for a sufficiently large graph and that this is true for any realization of the graph from a given generative process.

We formalize this intuition using the straightforward proposition below. Though the proposition is uncomplicated to prove, it cements the condition required of the statistic of interest for us to reasonably expect that our ARD estimates will be similar to what a researcher would have observed by directly computing the statistic from the fully-elicited graph. Further, it serves to demystify how ARD can work to recover network statistics with such limited information on the graph. The information in ARD, by the arguments in Section 3.3, is sufficient to estimate the parameters of the formation model. After proving the proposition, we provide examples of statistics where ARD should and should not perform well. We demonstrate our result for these statistics mathematically and confirm our intuition through simulations in Section 4.1.3.

Proposition** 4.1****.**

Consider a sequence of distributions of graphs on nodes given by our afore-described model and ARD . Assume is known. Let be the (unobserved) statistic of the underlying network and let be the same statistic computed from graph , drawn from the distribution with parameters . Finally, assume that

[TABLE]

Then the MSE is

[TABLE]

To clarify when this applies and when this fails, we provide several pedagogical examples. Our first example is a failure of Proposition 4.1.

Corollary** 4.1****.**

Under the aforementioned assumptions, given an (unobserved) graph of interest, , and non-degenerate linking probabilities , then the MSE for , a draw from the distribution of any single link is given by

[TABLE]

Note that irrespective of , this cannot tend to zero. When a link exists, the mean-squared error is and when it does not, the MSE is : these are just the complements of the Bernoulli probabilities.

Corollary** 4.2****.**

Under the aforementioned assumptions, given an (unobserved) graph of interest, , the MSE tends to zero with probability approaching 1 for the following statistics:

- (1)

Density (normalized degree):

[TABLE] 2. (2)

Diffusion centrality (nests eigenvector centrality and Katz-Bonacich centrality) for parameter sequence and any ,

[TABLE]

See Appendix A.2 for proofs of the proposition and corollaries.

A few remarks are worth mentioning. First, diffusion centrality is a more general form which nests eigenvector centrality when , and because the maximal eigenvalue is on the order of , this meets our condition. It also nests Katz-Bonacich centrality. In each of these, . It also captures a number of other features of finite-sample diffusion processes that have been used in applied work. Each of these notions relate to the eigenvectors of the network – objects that are ex-ante not obviously captured by the ARD procedure but ex-post work because the models are such that in large samples the statistics converge to their limits.

These results give us two practical extreme benchmarks. Our procedure should not perform well at all for estimating a realization of any given link in the network. In contrast, it should perform quite well for statistics such as degree or eigenvector centrality. Other statistics may fall somewhere in the middle of this spectrum. For example, a notion of centrality such as betweenness, which relies on the specifics of the exact realized paths in the network, is unlikely to work particularly well because even for large , the placement of specific nodes may radically change its value. Section 4.1.3 explores these predictions empirically using simulations.

4.1.2. Many Independent Networks

Now consider the setting where the researcher has independent networks each of size . We’ll take for simplicity, though the results presented here do not require this. We also have an ARD sample for every network . Every network is generated from a network formation process with true parameter . In this case of many networks, we consider how well the ARD procedure performs when the researcher wants to learn about network properties, aggregating across the graphs. This is the case we present empirically in Section 6.

Let be a network statistic from the unobserved graphs generating the ARD. For any given graph from the data generating process, define . For notational simplicity, we consider network-level statistics, but the argument can easily be extended to node, pair, or subset-based statistics.

Assume the goal of the researcher is to estimate some model

[TABLE]

and the economic parameter of interest is . As before, is unobserved because is unobserved and the researcher must make do with ARD, . The researcher instead estimates the expectation of the statistic given using ARD, . The regression then becomes:

[TABLE]

The arguments in Chandrasekhar and Lewis (2016) show that is still consistently estimated when using as a regressor rather than . We sketch out the argument here for completeness. First, It is easy to expand the error term,

[TABLE]

By iterated expectations we can see that

[TABLE]

This means that under standard regularity conditions, we can consistently estimate . The intuition is that the deviation of the conditional expectation from is by definition orthogonal to the conditional expectation and independent across . So one can think of the conditional expectation as an instrument of the true where the first-stage regression has a coefficient of 1.

Practically speaking, this means that even if we were interested in a regression of

[TABLE]

where whether nodes 1 and 2 are linked affects some outcome variable of interest, and we are interested in this across all networks, we can use instead in the regression to consistently estimate . Note that in contrast to the single network case, where we were interested in recovering itself, and even with large the MSE would not tend to zero, here simply having the conditional expectation is enough to be able to estimate the economic slope of interest, . Therefore, with many graphs, the ARD procedure should work well regardless of the properties of the given network statistic.

4.1.3. MSE Simulation Results

We next explore the results for a single large graph through a simulation exercise. We describe the simulation set-up we use here in full detail in the next section, but include the MSE results here as a demonstration that the intuition from the theoretical results in the previous section hold empirically. For this simulation, we use graphs with 250 nodes, which is a similar size to the data we describe in Section 5.1, simulated from the data generating process in Equation 3.1. In Figure 3, we plot the mean squared errors of our estimation procedure across a range of network statistics which are commonly used in applied economics. In order to make the MSEs comparable across statistics, we scale by . Panel A focuses on node level statistics while Panel B focuses on graph-level statistics.

The node level statistics are as follows: (1) degree (the number of links); (2) eigenvector centrality (the th entry of the eigenvector corresponding to the maximal eigenvalue of the adjacency matrix for node ); (3) betweenness centrality (the share of shortest paths between all pairs and that pass through ); (4) closeness centrality (the average inverse distance from over all other nodes); (5) clustering (the share of a node’s links that are themselves linked); (6) support (as defined in Jackson et al. (2012) – whether linked nodes have some as a link in common); (7) whether link exists; (8) closeness; (9) average path length; and (10) the average distance from a randomly chosen “seed” (as in an information diffusion experiment).

The graph level statistics are as follows: (1) diameter; (2) average path length; (3) average proximity (average of inverse of shortest paths); (4) share of nodes in the giant component; (5) number of components; (6) maximal eigenvalue; (7) clustering; and (8) the share of links across the two groups relative to within the two groups where the cut is taken from the sign of the Fiedler eigenvector (this reflects latent homophily in the graph).

Panel A of Figure 3 shows that the scaled MSEs in our simulations are quite small for most network statistics, including degree and (eigenvector) centrality, as predicted. Strikingly, the scaled MSE for the estimates of the existence of a link is extremely large and matches the computation in Corollary 4.1. Moreover, as argued above, betweenness also performs worse than the other statistics.

Panel B considers graph level statistics. The scaled MSEs tend to be small for all but one network statistic – the number of components in the graph. The number of components depends crucially on the existence of a small number of specific link realizations, calling upon the same intuition as the node-level existence of a link.

4.2. Core Simulations

We turn to a set of rich simulations which mimic real-world network data, but allow us to evaluate the efficacy of our procedure under correct specification.

4.2.1. Simulation Model

For each of our empirical investigations, we provide simulation evidence. We begin with a graph generated from the network formation model specified in Equation 3.1 and simulate the ARD on that graph.

The simulation procedure is as follows:

- (1)

We randomly generate locations on uniformly at random to get . 2. (2)

We randomly generate i.i.d. from a Normal distribution with parameters . 3. (3)

We generate a graph

[TABLE] 4. (4)

We then pick features which we maintain to be binary.

- (a)

Features are located with centers distributed uniformly at random over at sites . 2. (b)

Each feature is distributed with concentration parameter . 3. (c)

A given site at location receives feature i.i.d. with probability where is a uniform random variable and is the von Mises-Fisher density value at location . 5. (5)

Constructed ARD responses are built using features of one’s neighbors and the underlying graph.

Unless otherwise stated, we set , , , , and , which are chosen to generate graphs that resemble our empirical network data in terms of average degree 20, clustering 0.13, proximity (defined as the mean of the inverse of path lengths) 0.50, average path length 2.15, and the maximal eigenvalue 26.51 of the network.

We then run our proposed procedure to estimate a range of network characteristics at both the individual- and node-level.

4.2.2. Simulation results

Figure 4 presents the results of our procedure using synthetic ARD data from graphs generated at the parameters specified above. We see that the procedure works well. Throughout the paper, we look at the degree, eigenvector centrality, and clustering at the node level, as well as the maximal eigenvalue, average path length, clustering, and eigenvector cut at the graph-level.171717The eigenvector cut metric is defined by the eigenvector with the second smallest eigenvalue of the Laplacian matrix. Using the median of the eigenvector to partition the graph gives us two balanced groups of equal size. We plot the fraction of links that cross group boundaries. The figures also display an additional set of network characteristics including betweenness centrality, closeness centrality, support and distance from “seed” at the node level as well as diameter, the fraction of links in the largest connected component and the number of components at the graph level.181818We define support at the individual level to be the fraction of a node’s links that are linked to at least one other link of that node. For distance from “seed”, we arbitrarily choose one node in the graph and measure the minimum path length to that “seed” node for all other nodes.

The figure shows strong correlations between the true value in the simulations and that predicted by the ARD sample for almost all of the statistics examined here. We do note that the correlation is weak in the case of eigenvector cut. The eigenvector cut takes a narrow range of values in the underlying graph, however, because we simulate the locations of both individuals and groups uniformly across the surface of the sphere. That is, there is no cut structure in the underlying formation model. Appendix H presents plots of additional network measures. There, we note that the estimates are quite close to the true values for several integer-valued statistics including diameter, fraction in the giant component, and the number of components. For these three measures, there is very little variation in the true measures.

4.3. Varying sparsity

4.3.1. Varying

We next explore the performance of our procedure when we vary sparsity – the number of links relative to graph size. To do this, we hold all the parameters fixed, including at its original value, but vary the distribution of the node effects. In particular we change the mean of the effect , with . This varies the expected degree from 5 to 80, holding fixed .

We define the percentage error as the difference between the estimated and true measure divided by the true measure. At each sparsity level, we pool simulations and make plots of mean standard deviation of percent error. Figure 5 shows how well our algorithm estimates these measures at varying sparsity levels. As the graph becomes less sparse, we have smaller bias and variation in the estimation of degree and centrality. For maximum eigenvalue, proximity, and clustering, the bias in estimation has a monotone pattern. For proximity and clustering, we have less variation as the graph becomes less sparse. For eigenvector cut, the bias is very small at all sparsity levels and the variation decreases as the graph becomes less sparse.

4.3.2. Sparse with thick tails

Our next exercise is to approximate networks that exhibit heavy tails. That is, the network may mostly be sparse but some nodes may have extremely high degree. To operationalize this, we hold all the parameters fixed as before, but now draw from a Normal distribution with with probability and from a Normal distribution with with probability . The high centrality nodes have, on average, expected degrees of 40, while the rest have, on average, expected degrees of 5. We pick so the average number of high centrality nodes is 25, but the actual number may vary in each simulation. The goal of this exercise is to study whether we can pick out which members of the network have high eigenvector centrality, which is important in a diffusion process for instance, even though the graph is extremely sparse.

Table 1 shows the confusion matrix for this exercise—which presents true positives, true negatives, false positives, and false negatives—for the top decile eigenvector centrality estimation average over 50 simulations. With a true positive rate and a false positive rate, we successfully recover the majority of high centrality nodes. We note that the actual number of high centrality nodes varies in each simulation, which results in some noise in our estimation.

4.4. Varying network size and sampling share

Next we study what happens as we move from what we call a rural environment to an urban environment, exploring what happens as the number of nodes in the population gets larger, and when we have to reduce the ARD sampling share. In particular we vary . We also vary the share in the ARD sample, . When , we sample demographic features for all nodes with . We construct such that is in one of eight categories depending on the sign of each coordinate of .

Figure 6 presents estimation results when we vary and . When is fixed, in general we have less bias and variation as we increase . When is fixed, performances of degree and centrality estimation on ARD nodes are similar at various . As we expect, increasing the share of ARD nodes increases the precision of node level measures estimation for all nodes.

We underestimate maximum eigenvalue when we do not have 100% ARD sampling, and we overestimate maximum eigenvalue when we do have a ARD sample. We underestimate average path length at all and ; the bias in estimation decreases as we increase and . Our estimation of network level clustering is within of true value most of the time, and our estimation of the percentage of cross links using eigenvector cut is mostly within of the true values.

5. Simulations with Real-World Networks

The goal of this section is to take the technique to the field and see how well, in a real, empirically-relevant context, we might have done using ARD in place of full network data. After all, our ARD technique can only do as well as the latent surface model specified in Equation 3.1 does at capturing network structure.191919Here, we remind the reader that ARD information and other insights from our method could, in principle, be applied to other network formation models that may better suit certain applications. For instance, the sub-graph generated models (SUGMs) discussed in Chandrasekhar and Jackson (2016) allow for violations of the “triangle inequality” in latent space to generate a different distribution of triangles among nodes. We conjecture it is straightforward to identify SUGMs through ARD.

Our choice of a parametric model clearly has implications for the performance of the method and carries with it some of the limitations of random geometric graph sorts of models: conditional on locations on the surface, it is unlikely for very distant nodes to ever link, making so-called “short-cuts” rather rare events. Further, clustering in the network (e.g. homophily based on a given characteristic) is accomplished through the positions of particular individuals in the latent space.202020If a node is more likely to link to those whose locations are nearby, and the network neighbor is also more likely to link to those with close latent locations, then the initial node is also on average going to be in relatively close proximity to the neighbor’s friends on the latent space, leading to a higher linking probability and higher levels of clustering. If there is a clear cleavage in the network (and the ARD questions asked on the survey also make it possible to detect this), then our model will generate graphs that faithfully reflect this distinction. If, however, there is a weak preference for connection within rather than between groups, this will be more difficult to detect.

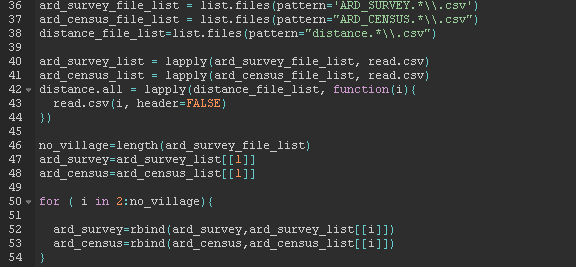

5.1. Setting and Data

We aim to show the potential for ARD to be used in place of detailed social network maps. To do this, we begin with the rich network data collected by Banerjee et al. (2016c). This consists of network data from 89% of 16,476 households across 75 villages in Karnataka, India. Thus, in the undirected, unweighted graph, we have information about 98% of all potential links. The survey asks about 12 types of interactions: (1) whose house the respondent visits; (2) who visits the respondent’s house; (3) kin in the village; (4) non-relatives with whom the respondent socializes; (5) who provides help on medical decisions; (6) from whom the respondent borrows money; (7) to whom the respondent lends money; (8) from whom the respondent borrows material goods such as kerosene or rice; (9) to whom the respondent lends such material goods; (10) from whom the respondent receives advice before an important decision; (11) to whom the respondent gives advice; and (12) with whom the respondent goes to temple, mosque or church. We use a graph which is undirected and unweighted, taking a link as the union over all the above dimensions. The ratio of average degree over network size ranges from 0.04 to 0.21, with a median of 0.08. The sparsity level is the same as our core simulation, where ratio of expected degree over network size is 20/250=0.08.

We asked 12 additional questions in a follow-up survey 12 months later to a random sample of approximately 30% of households, covering traits such as owning a tractor, having met with an accident, illness incidents, birth of twins, educational attainment and family composition. We use 8 of these 12 traits as the basis for the ARD analysis. The other four questions are deleted because they are rare or non-informative of sampled households’ positions in the network.

Our first goal is a proof of concept for the use of ARD and the latent distance model to generate a posterior distribution for each graph. To do this, we construct ARD responses for the 30% sample: what would be the aggregate counts these respondents would have given us had we asked them ARD questions? It also allows us to abstract from errors in knowledge or in recall by survey respondents.212121For example, we know the tractor ownership of each individual in the 30% sample. We can then construct the number of links of each ARD respondent to others in the ARD sample who have a tractor. This gives us the ARD responses for the induced subgraph. To estimate the number of links to tractor-owning households in the full graph, we can simply scale by the sampling rate.

For what follows, the 29% of the households with supplemental surveys form our ARD sample, while the remaining 71% of households are non-ARD nodes. Because we construct ARD responses for households who answer supplemental surveys in each village, the actual percentage of households with constructed ARD responses varies by village. One village only has a 6.7% sampling rate and therefore gets dropped, increasing the sampling rate across all villages used to 30%. Recall that we observe a set of demographic covariates collected in the census of Banerjee et al. (2016c) for all nodes and we can use these covariates to predict and for nodes not in the ARD sample.

5.2. Network Level Results

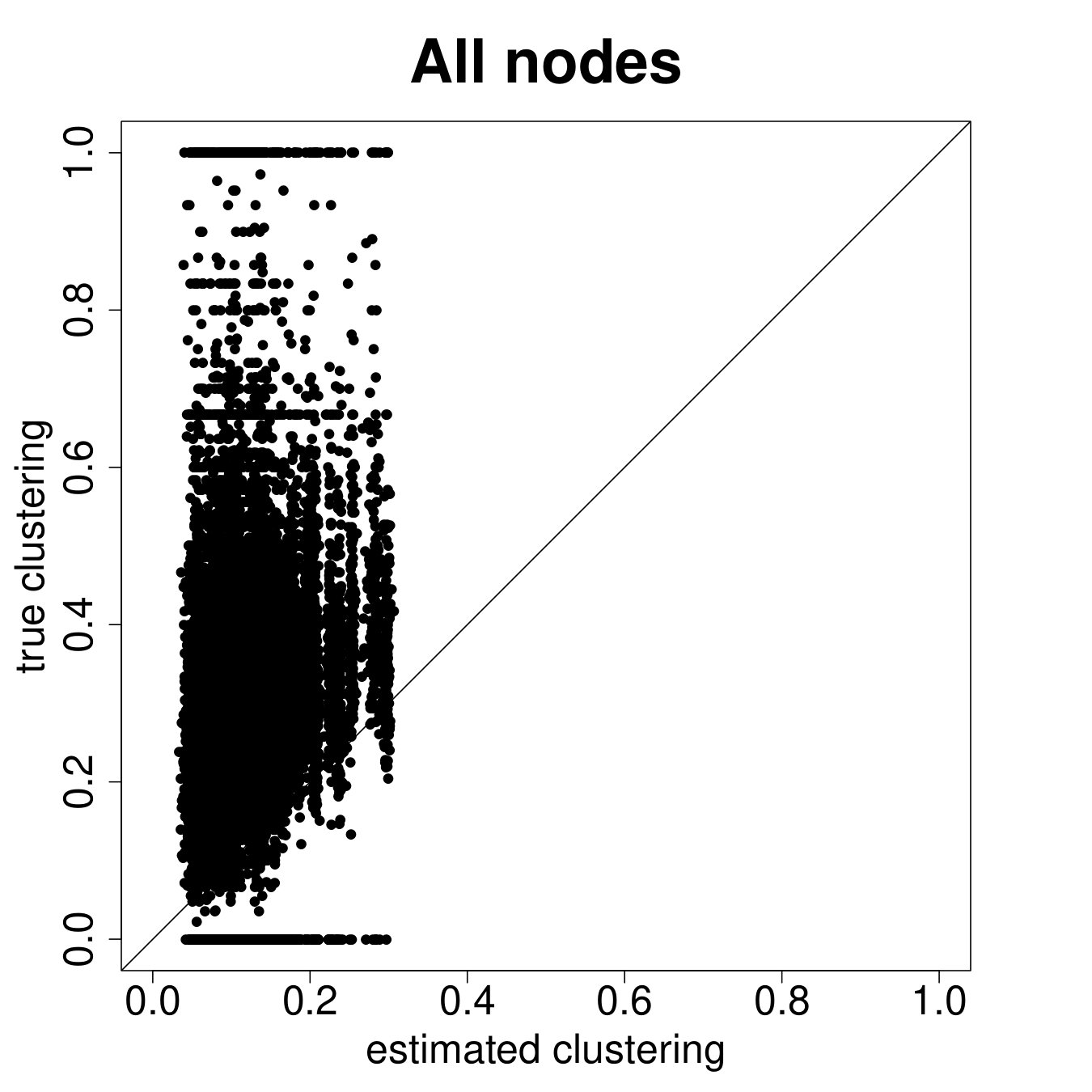

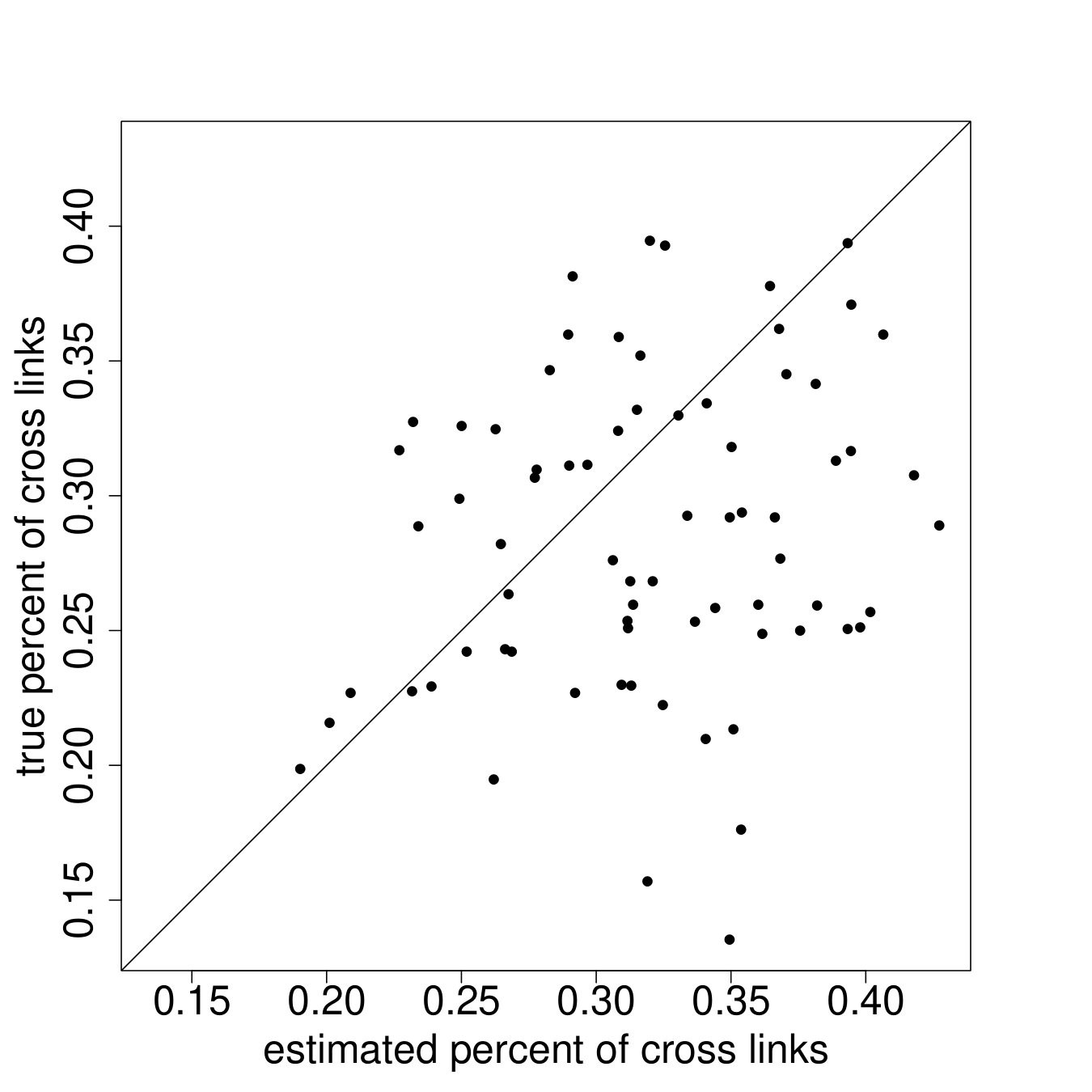

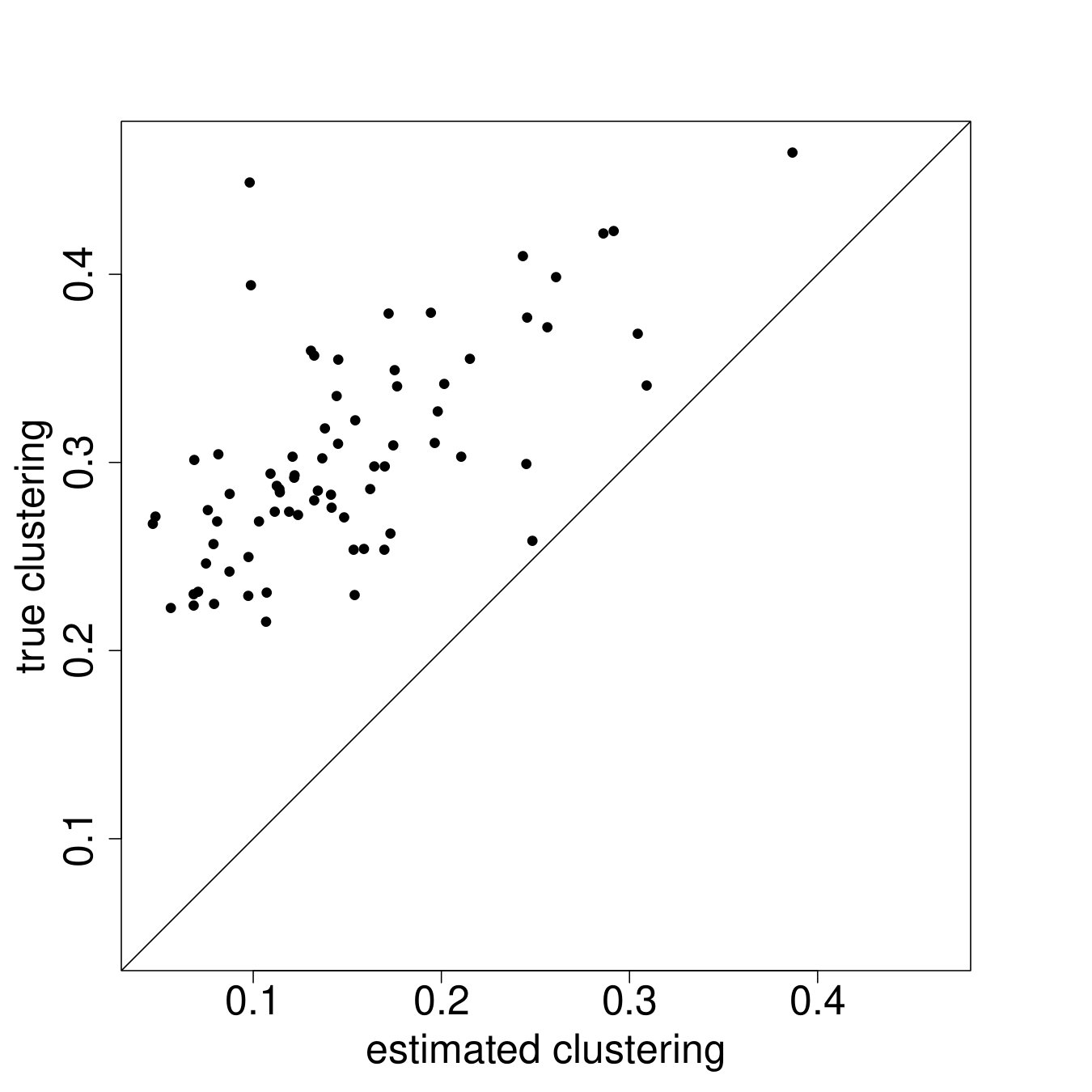

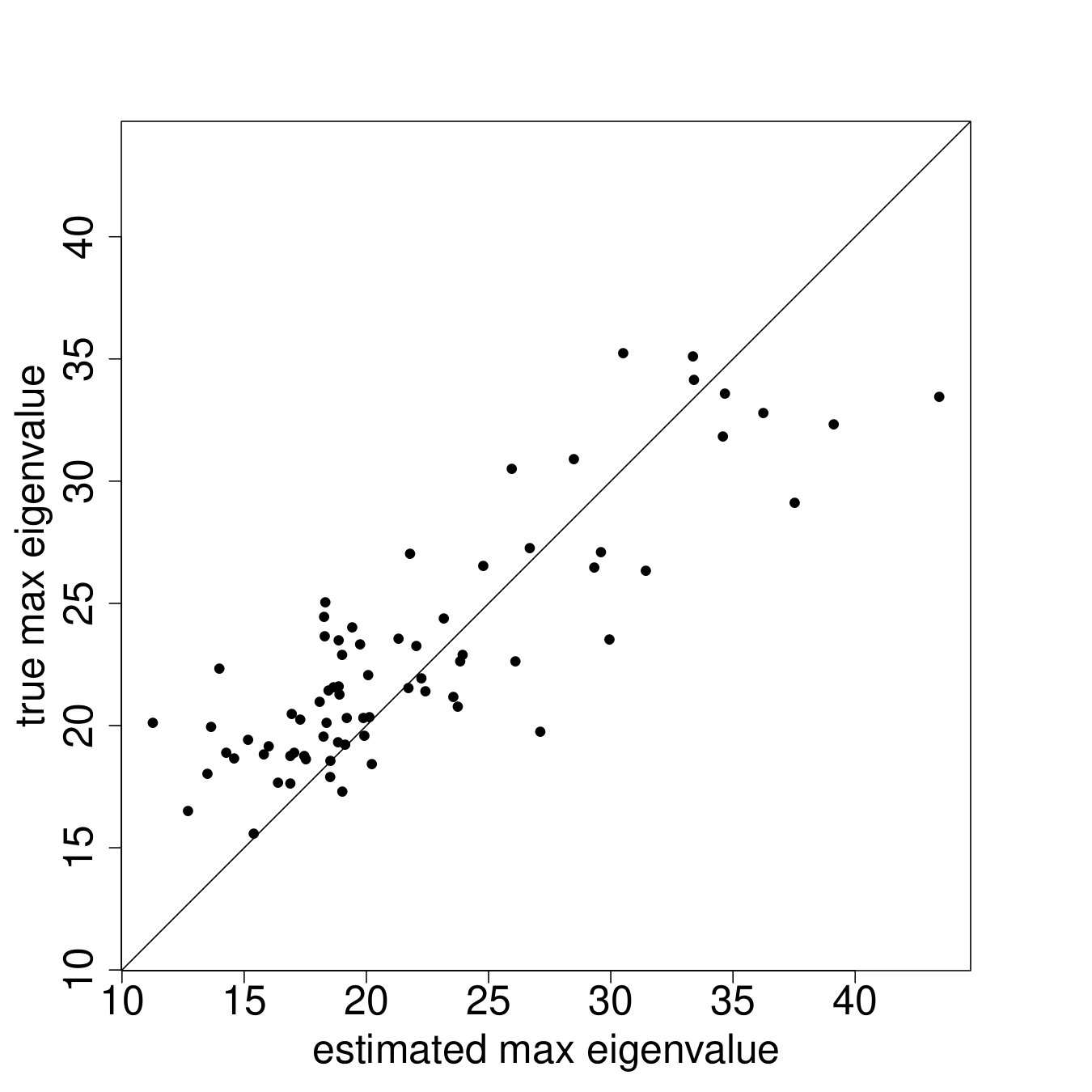

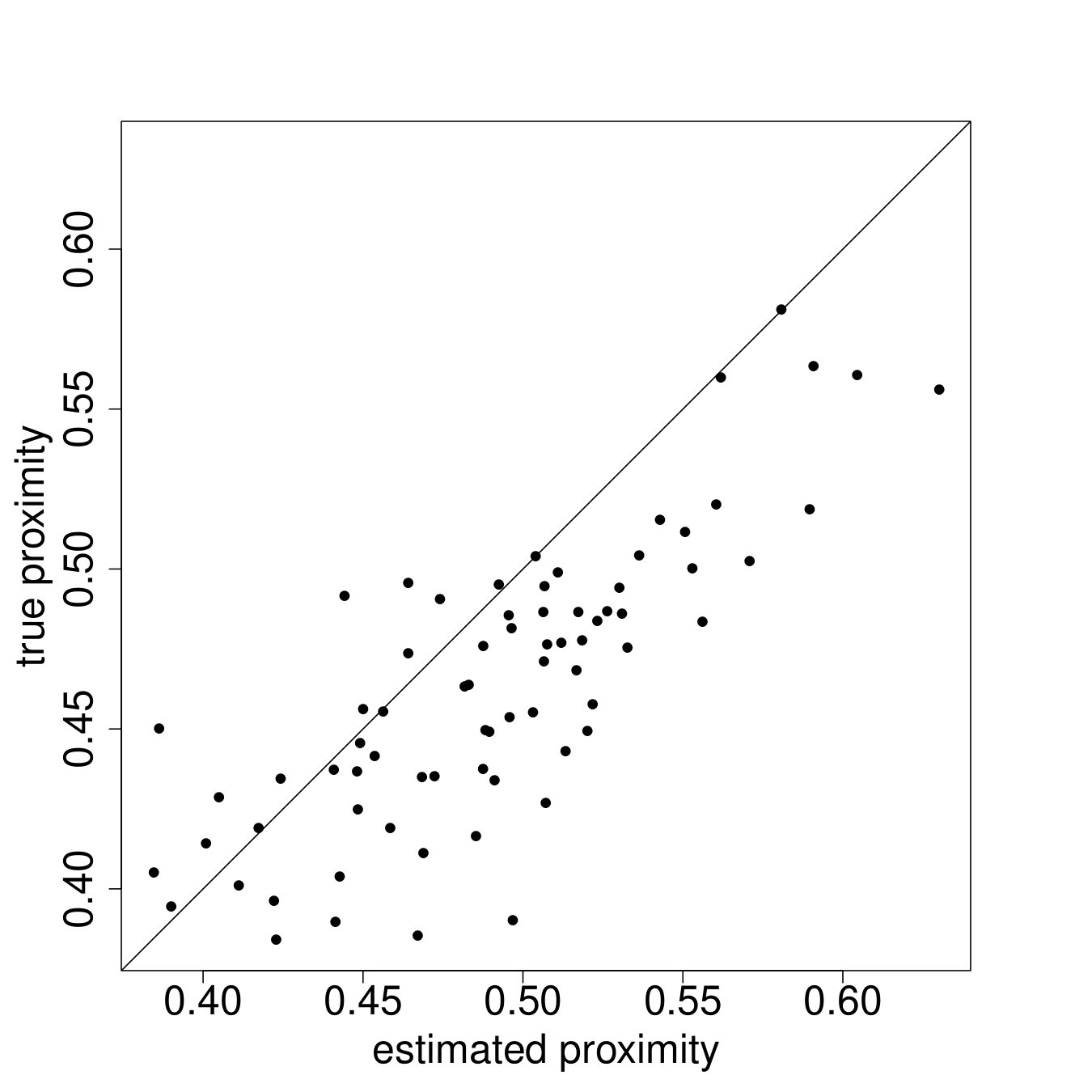

We begin by looking at the same network-level statistics that we have focused on throughout the paper: , social proximity, clustering, and eigenvector cut.

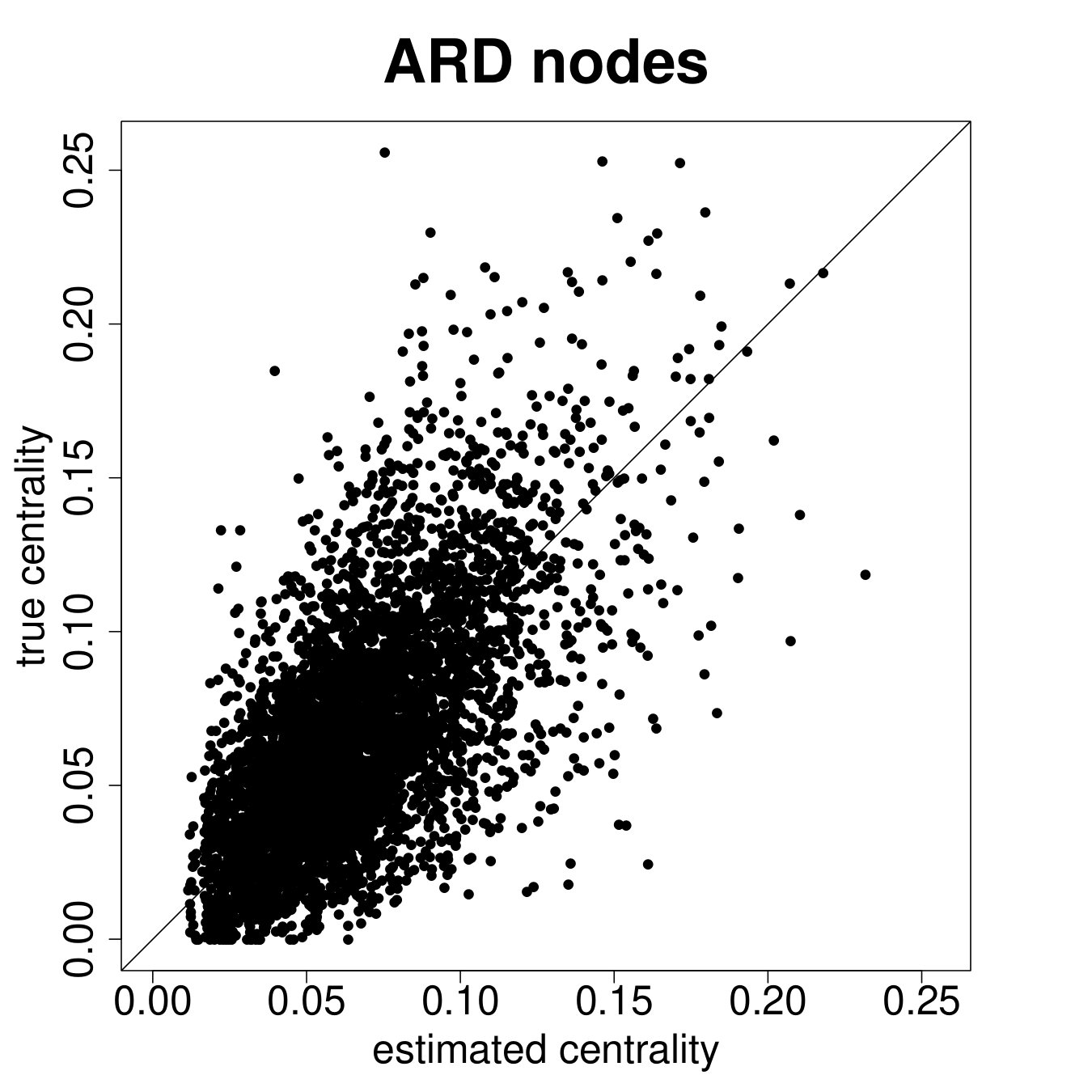

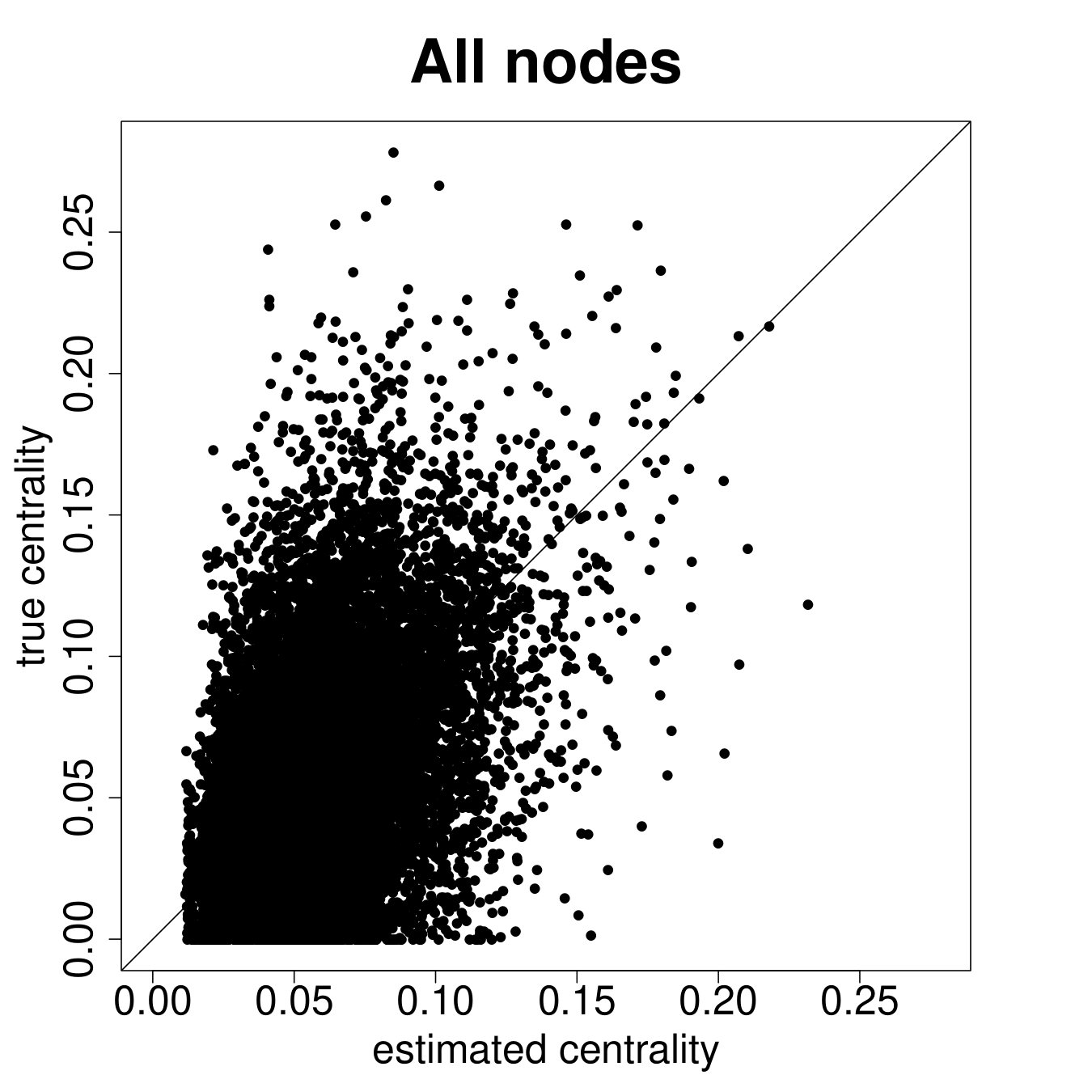

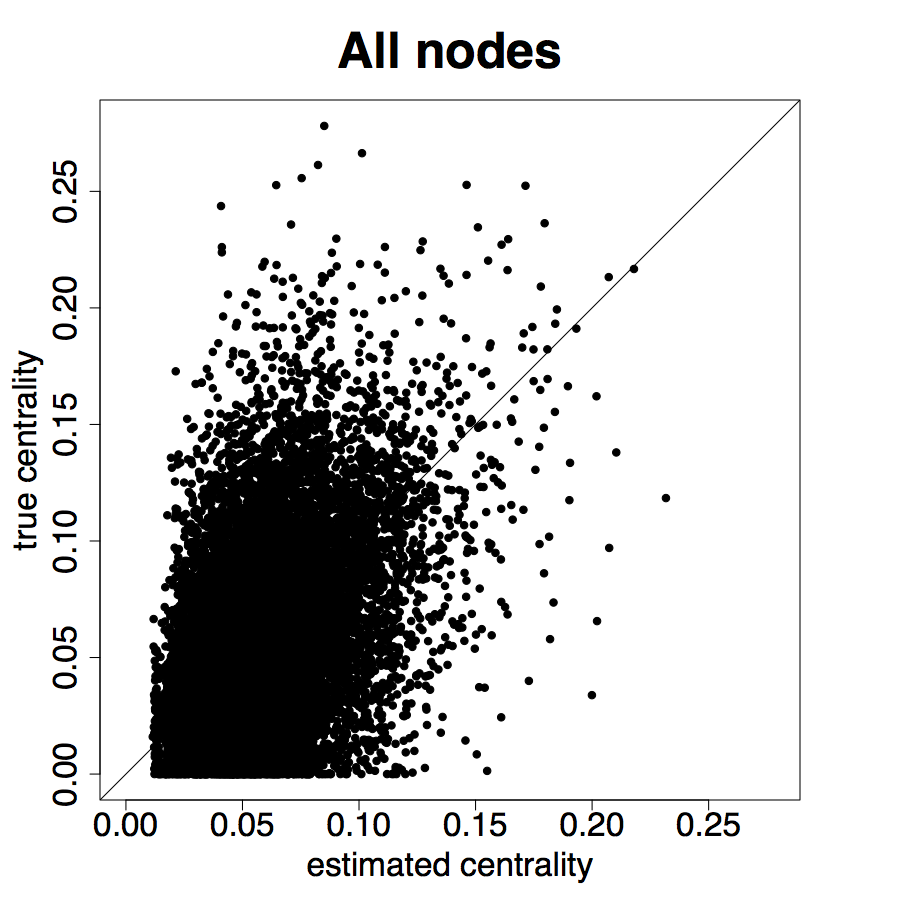

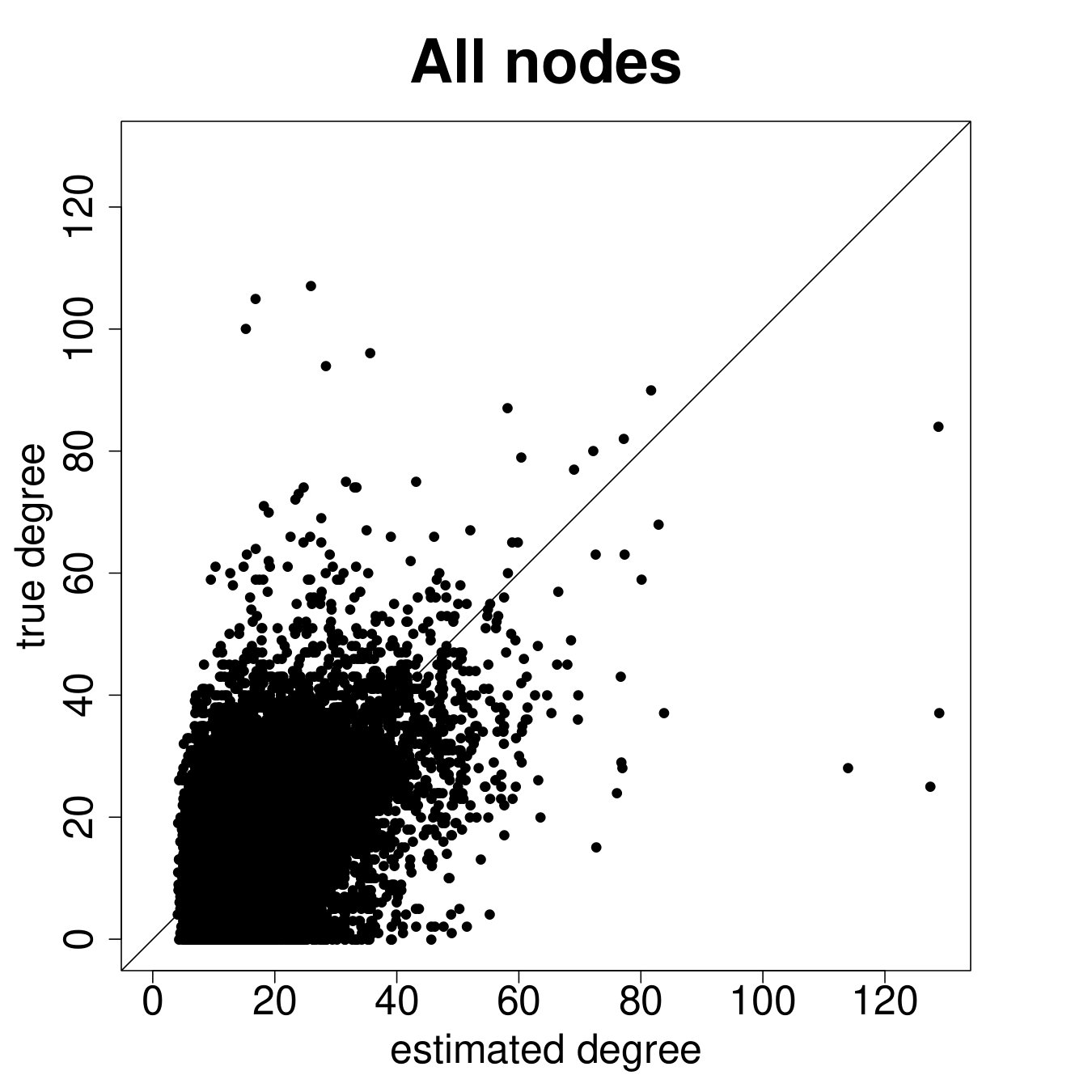

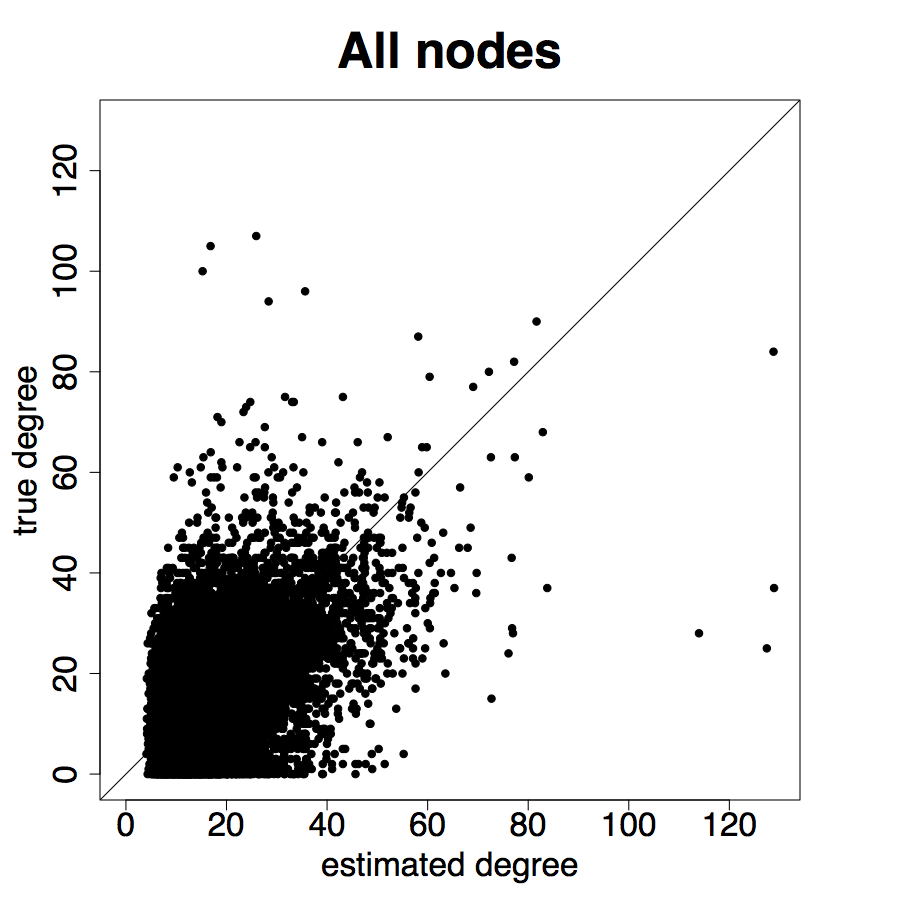

Figure 7 plots the results.222222See Appendix I for plots of additional network statistics at both the graph and node levels. In particular, each panel plots the posterior mean for the network statistic in question against the true value in the data, for each of the 75 villages. We see, rather remarkably, that these global network features are rather well-captured by the ARD procedure. The procedure is weakest for clustering but note that though there is clearly a bias, it is small and out-performs many off-the-shelf models of network formation (Chandrasekhar and Jackson, 2016).232323See Table 2 in the paper which compares the implied network level statistics (e.g., eigenvector cut, maximal eigenvalue, clustering, average path length) when we fit (1) a conditional edge independent model flexibly using a rich set of covariates and (2) the same conditional edge independent model but adding in node-level fixed effects (i.e., the model of Graham (2017)). Both of these miss across the board in terms of the relevant network statistics. Finally, prior work has demonstrated theoretical failures of consistency of ERGMs when links and triangles are introduced (as would be needed to model realistic data) and also slow (exponential) mixing times for MCMCs used in estimation (Shalizi and Rinaldo, 2013; Bhamidi et al., 2011). Therefore, our model out-performs, both theoretically and through simulations, conditional edge independent models, Graham (2017) which adds fixed effects but no latent locations, and non-trivial ERGMs.

5.3. Node Level Results

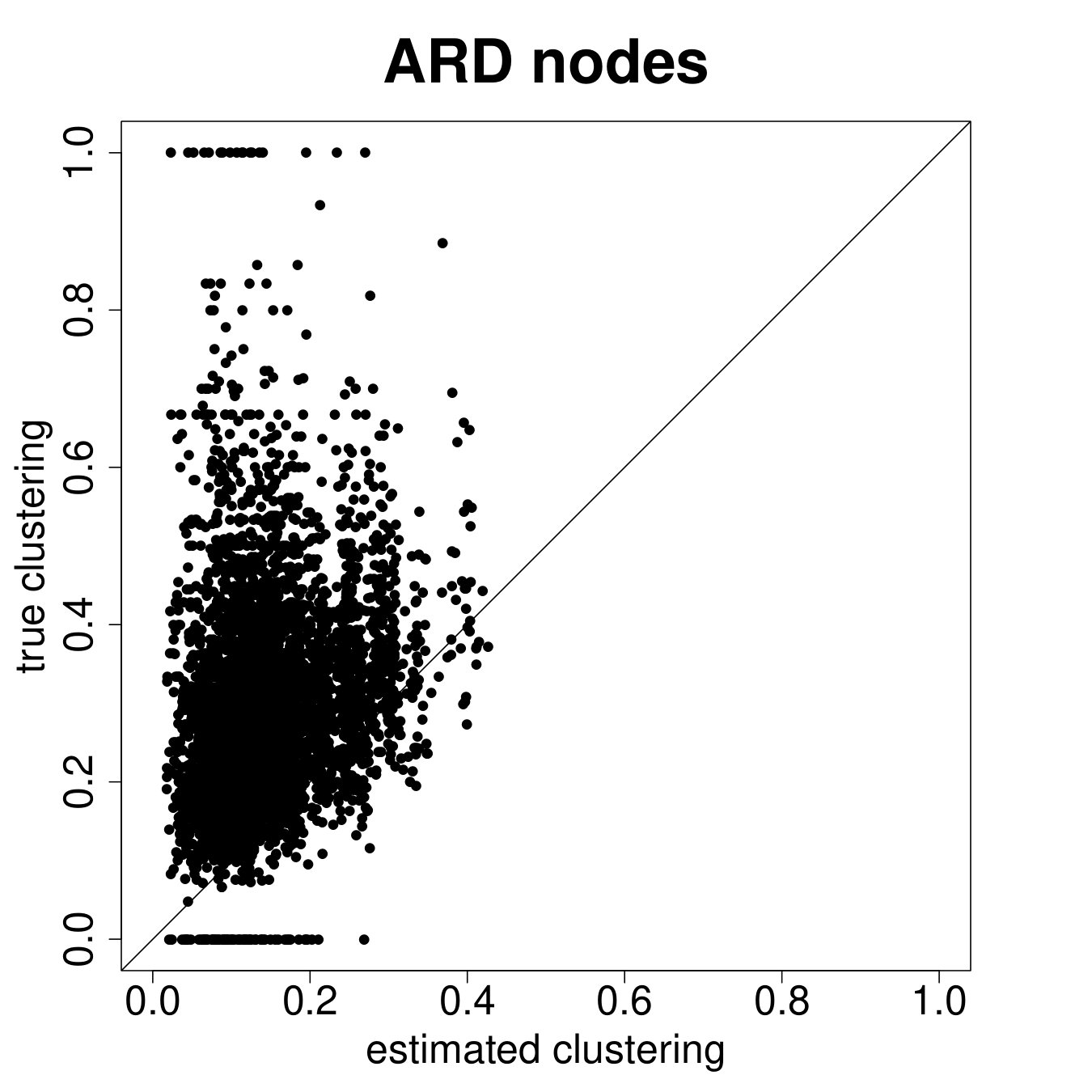

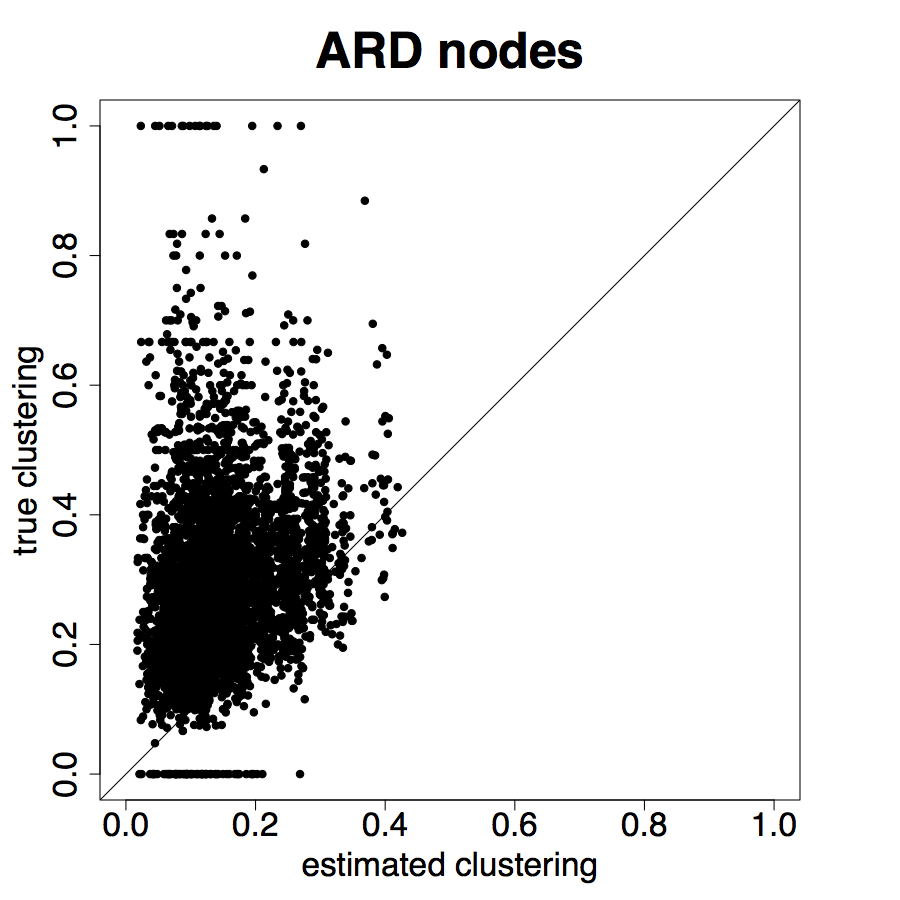

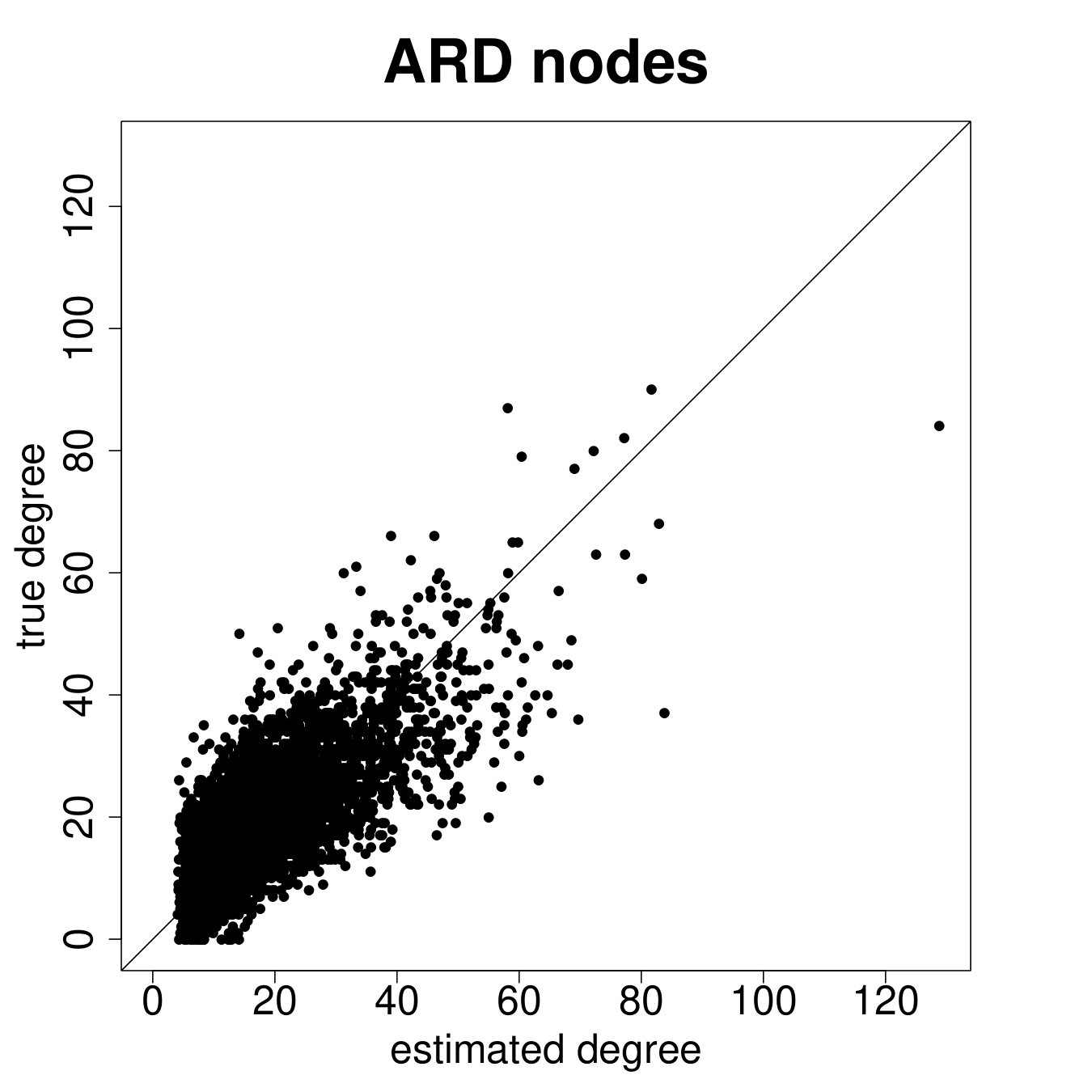

Next we turn to node-level results. We again focus on degree, eigenvector centrality, and clustering.

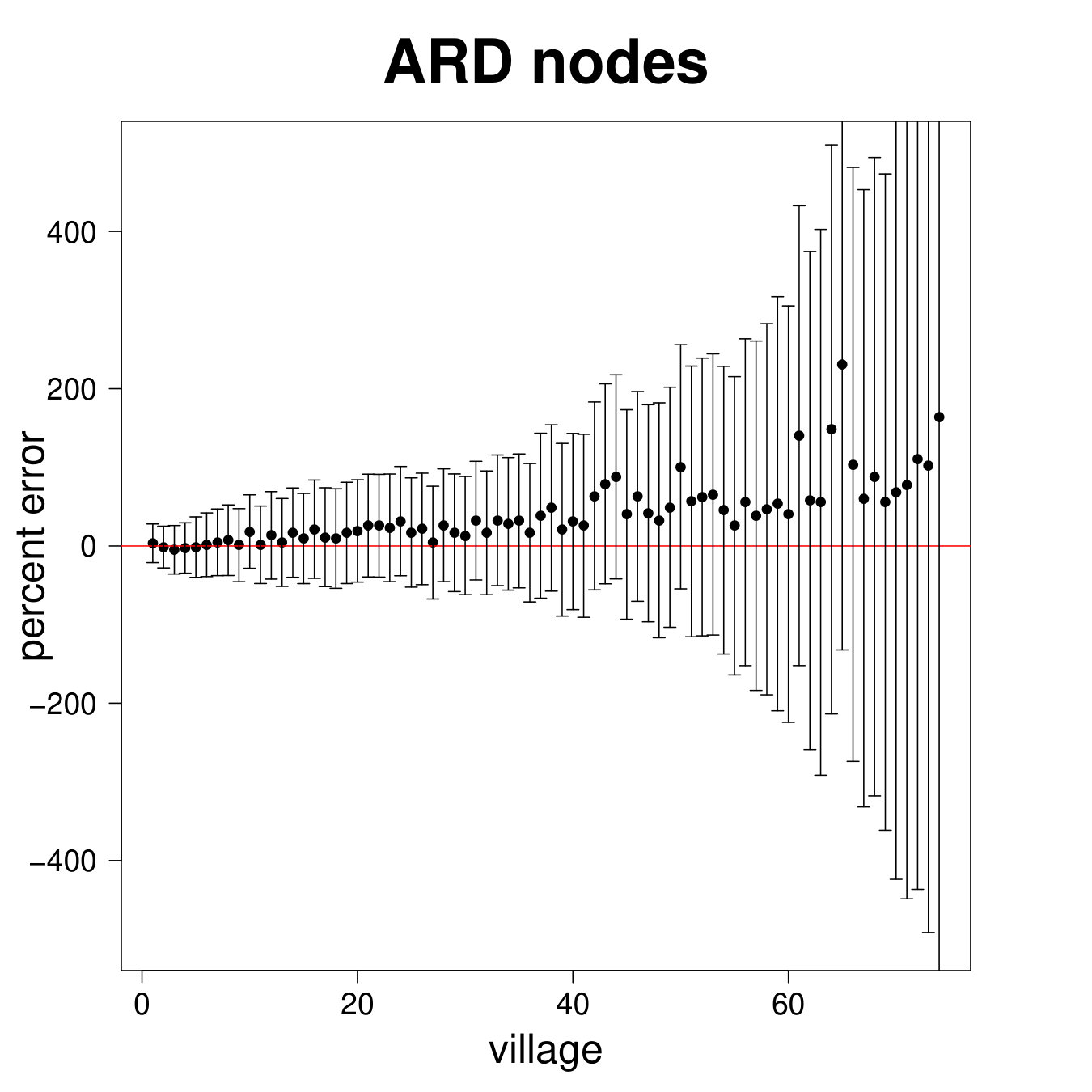

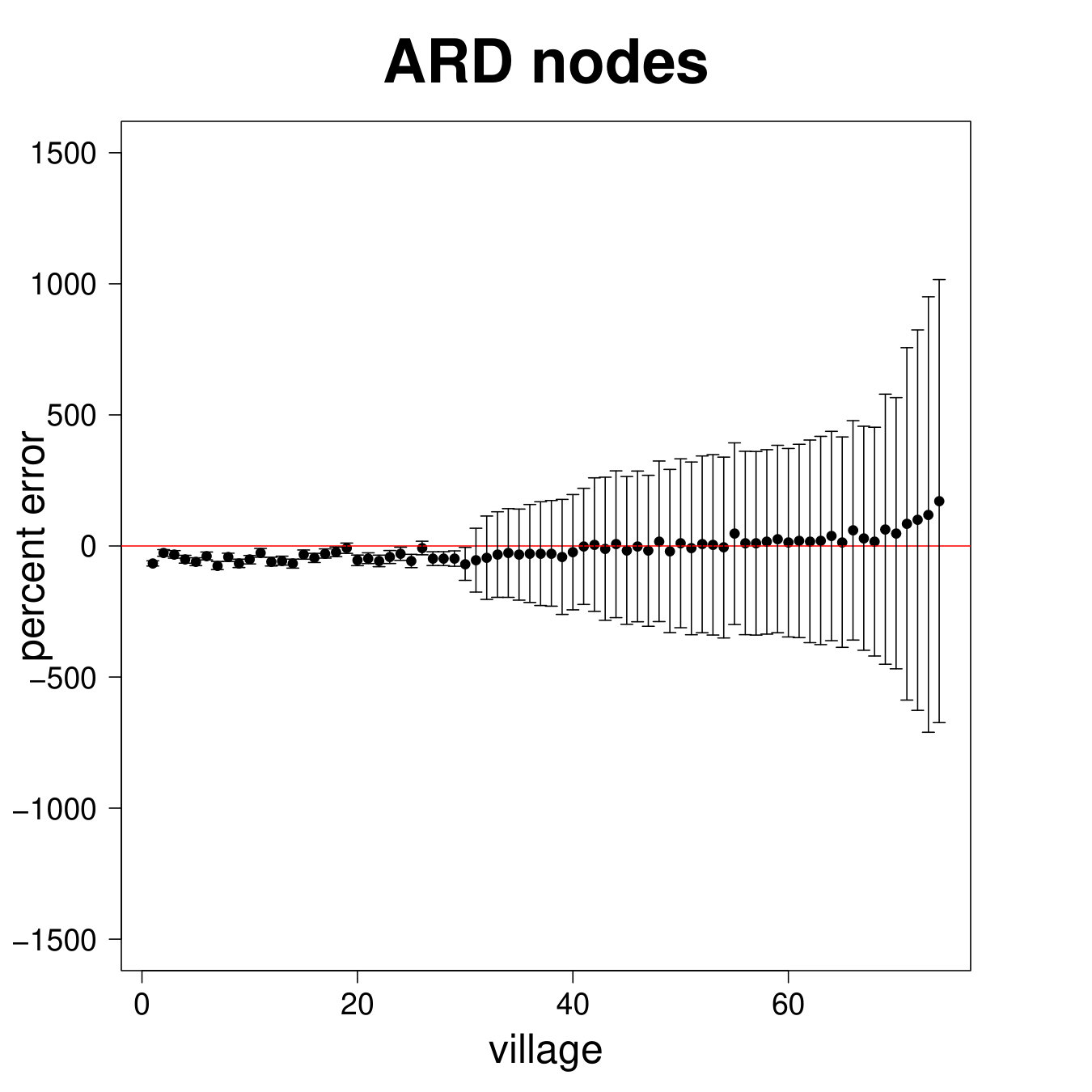

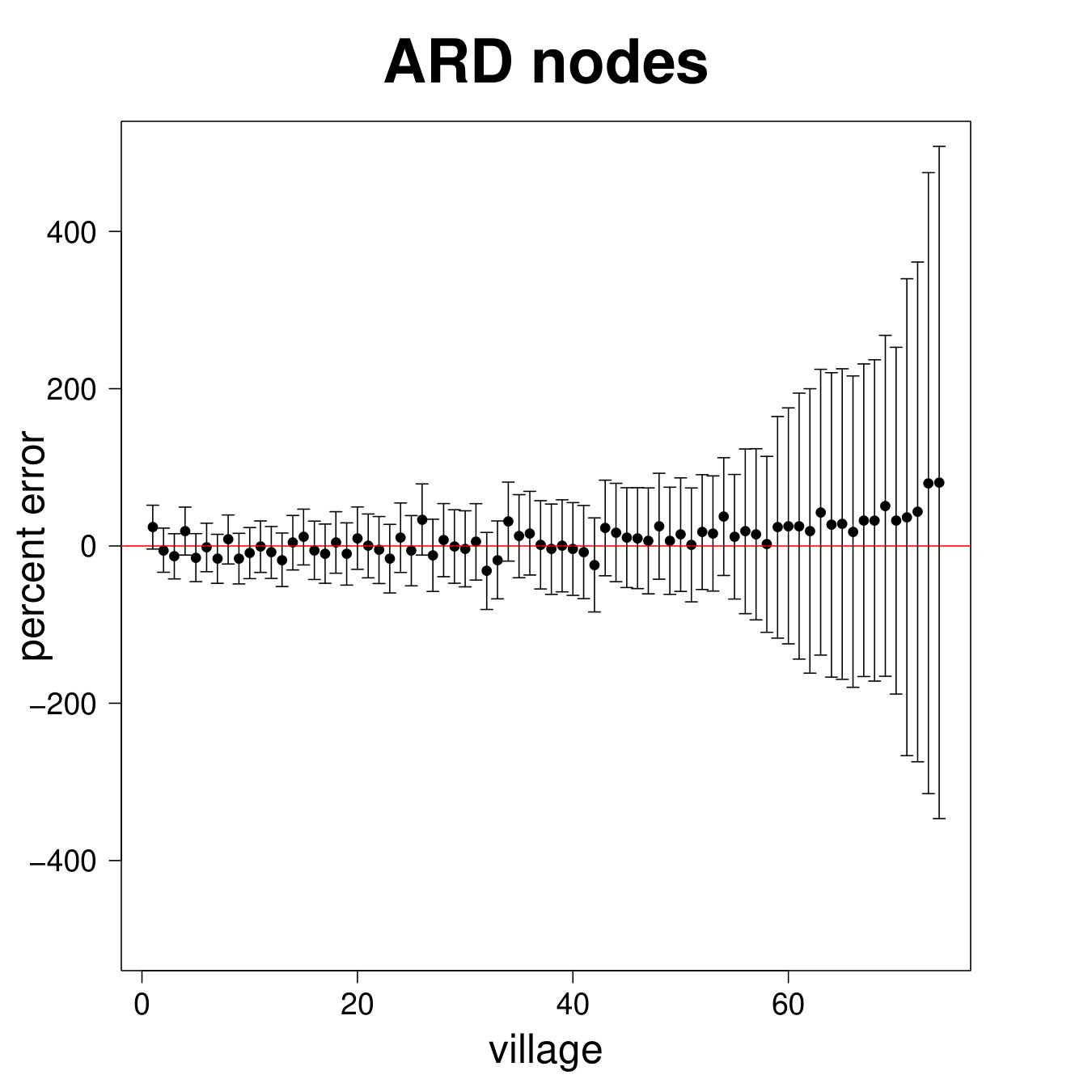

Figure 8 presents the results for the ARD sample and Figure 9 presents the results for the entire sample. We see from Figure 8 that the estimated degree, eigenvector centrality, and clustering coefficient are strongly correlated with the true values in the data (Panels A, B, C). Furthermore, in Panels D, E, and F we plot the percent error averaged over all nodes in the sample by village, plotted by village ordered by standard deviation of percent errors.

Table 2, Panel A presents a confusion matrix to look at the probability that a node picked by a researcher using ARD is in the top decile of the centrality distribution, which is a true positive rate. For comparison, this is a comparable rate to that in Banerjee et al. (2016c) using the “gossip survey” technique to elicit nominations from the village as to who is central if the nominee is also a social or political leader in the village.

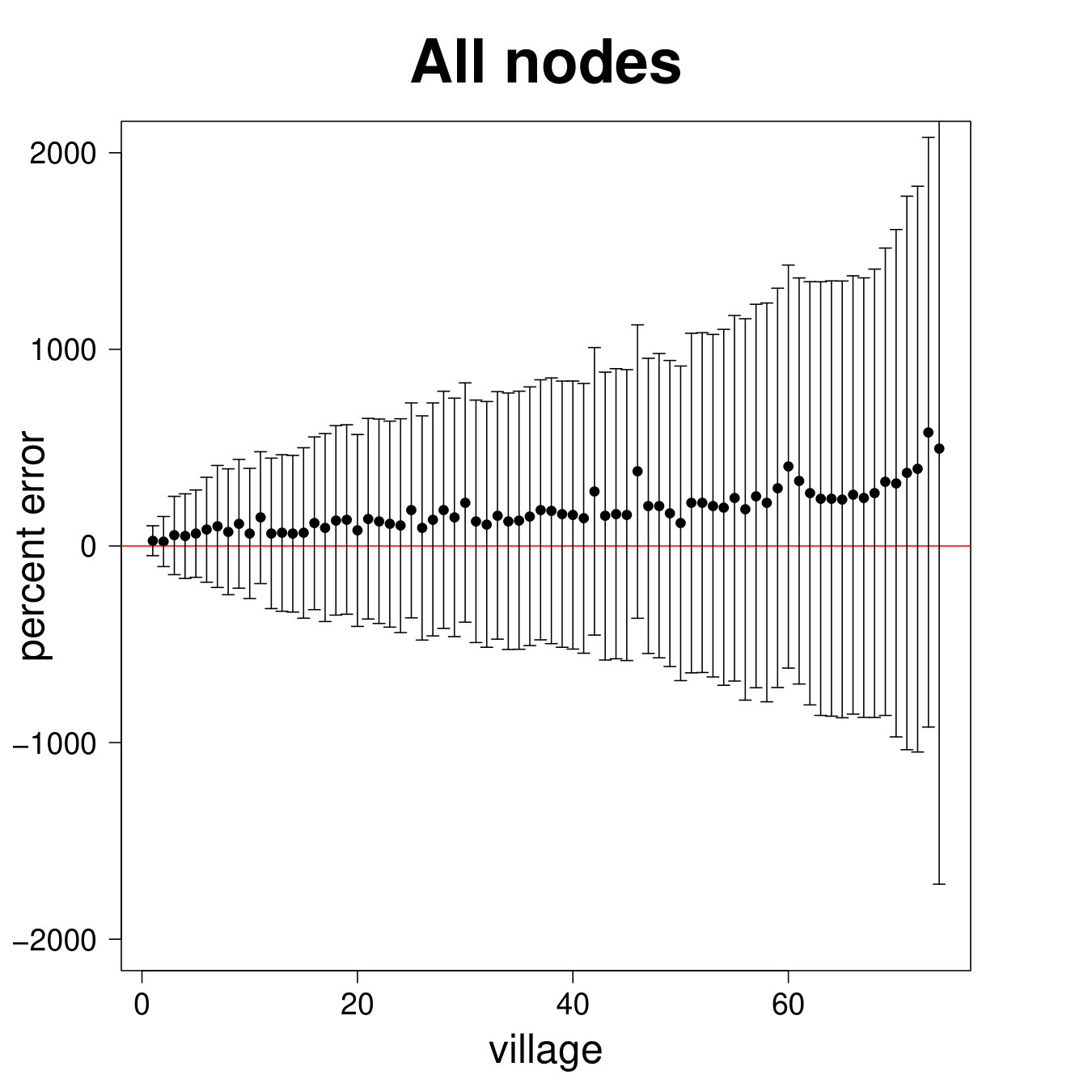

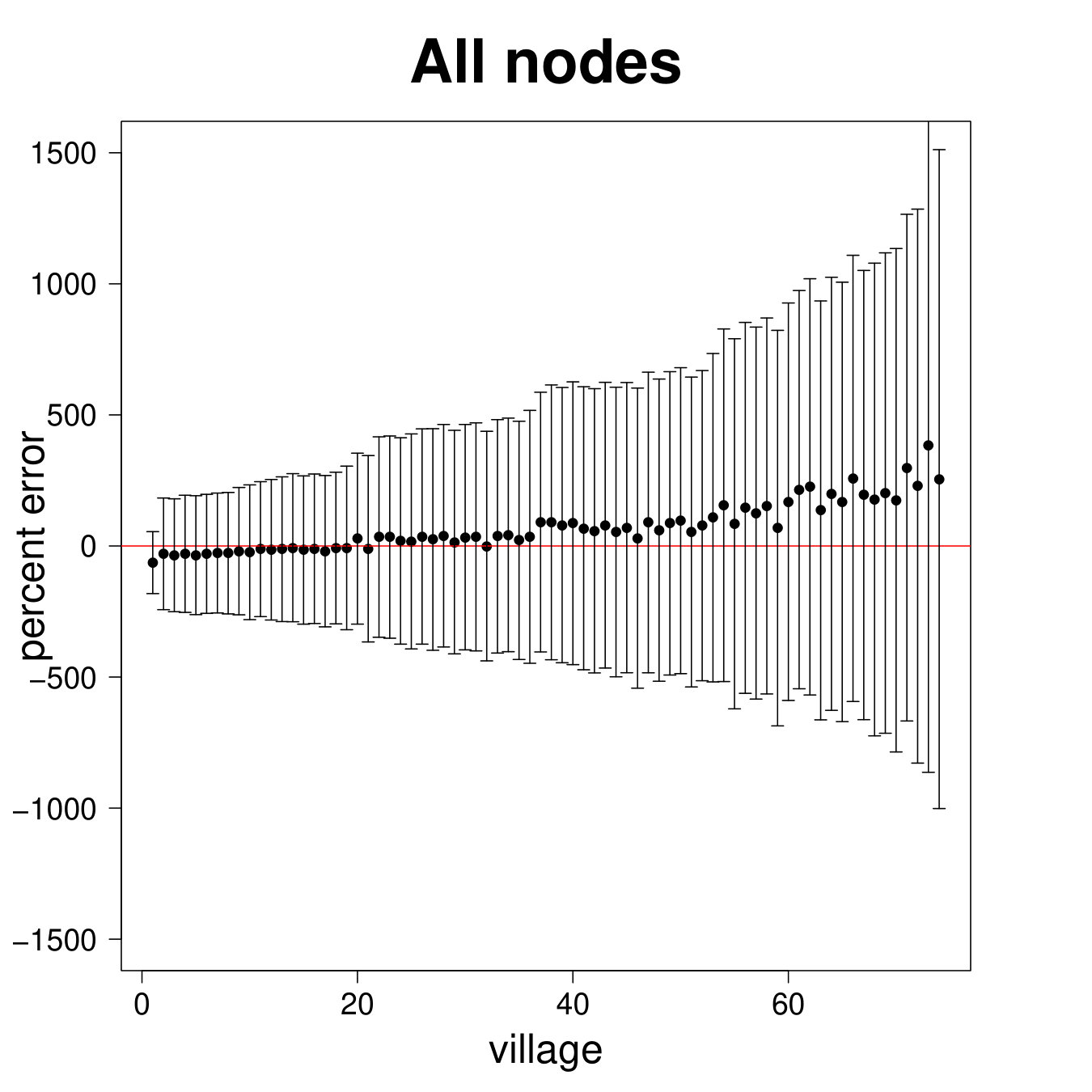

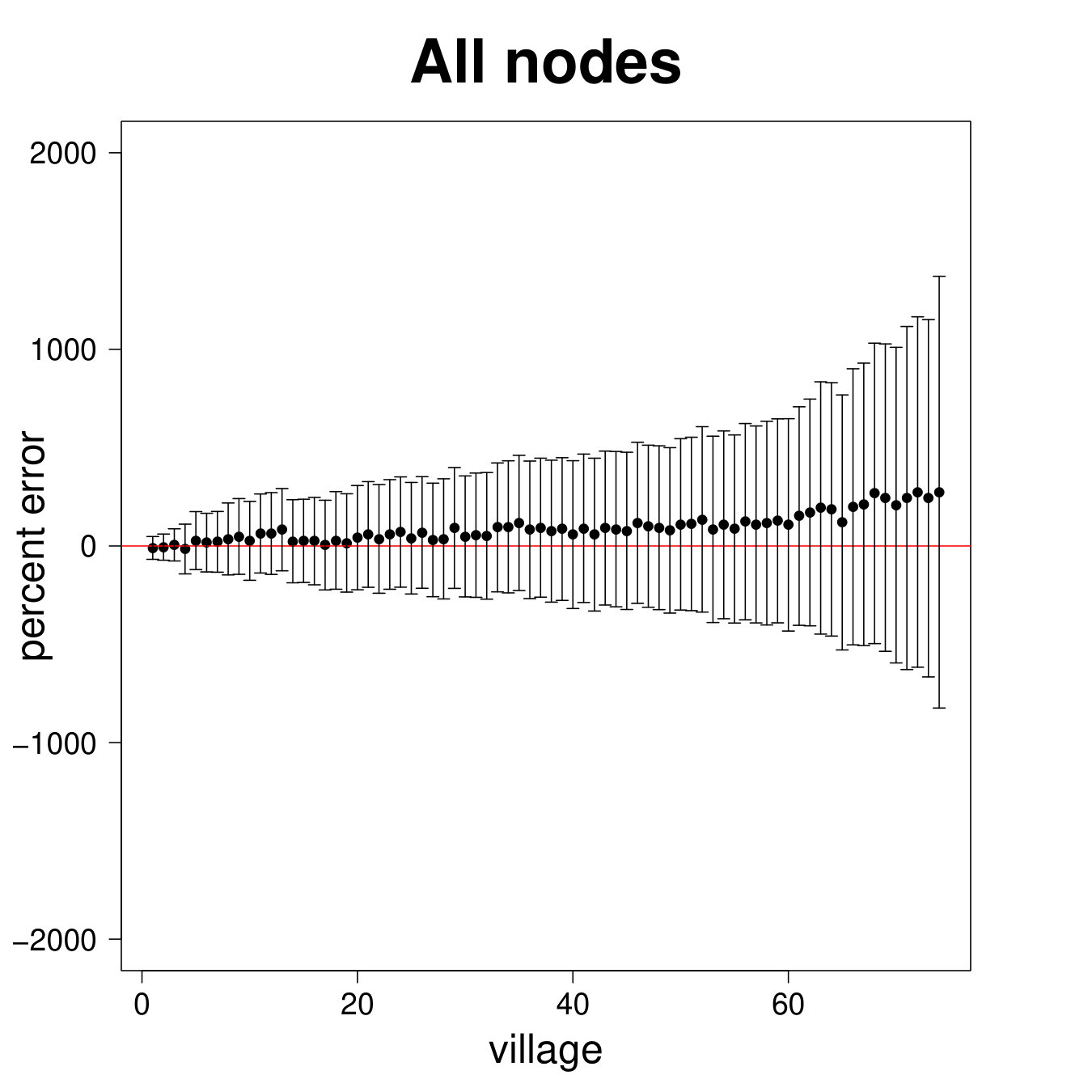

Figure 9 repeats the above results for the entire sample. The results are largely similar to the ARD sample alone, though clearly there is more noise, as expected, when including the non-ARD sample.

Table 2 Panel B presents the confusion matrix for the entire sample, with a true positive rate. We have a true positive rate even when we pick top decile centrality nodes from non-ARD sample. For context, this is about as high as a non-nominated leader (Banerjee et al., 2016c), whom a microfinance institution might specifically pick to diffuse information widely.

5.4. Discussion

Taken together, our results suggest that ARD with the latent distance model and the procedure proposed here is a useful tool because the researcher will have reasonable estimates of a number of network features. As is unsurprising for a model of the form specified here, it is a little bit weak when it comes to clustering.

6. Empirical Applications

We now present two empirical applications that use ARD techniques. They build upon prior work by the authors, in part. The goal is to illustrate here that a researcher could have done this sort of economic analysis using ARD only, equipped with our method.

The first example looks at what would have happened if the researchers had obtained ARD for an experiment on savings and reputation. The second example actually looks at a setting where survey ARD was collected.

6.1. Encouraging savings behavior in rural Karnataka