Diffusive and arrested-like dynamics in currency exchange markets

Joaquim Clara-Rahola, Antonio M. Puertas, Miguel Angel, Sanchez-Granero, Juan E. Trinidad-Segovia, F.Javier de las Nieves

TL;DR

This paper reveals a striking analogy between the fluctuation dynamics of the EURUSD currency market and colloidal particles in supercooled states, demonstrating that models from arrested physical systems can describe currency fluctuations.

Contribution

It introduces a novel analogy between financial market dynamics and physical systems, applying models of arrested states to describe currency exchange fluctuations.

Findings

EURUSD fluctuations resemble colloidal arrested states

Two-step mean squared price displacement observed during market closures

Models of arrested physical systems fit currency fluctuation data well

Abstract

This work studies the symmetry between colloidal dynamics and the dynamics of the Euro--US Dollar currency exchange market (EURUSD). We consider the EURUSD price in the time range between 2001 and 2015, where we find significant qualitative symmetry between fluctuation distributions from this market and the ones belonging to colloidal particles in supercooled or arrested states. In particular, we find that models used for arrested physical systems are suitable for describing the EURUSD fluctuation distributions. Whereas the corresponding mean squared price displacement (MSPD) to the EURUSD is diffusive for all years, when focusing in selected time frames within a day, we find a two-step MSPD when the New York Stock Exchange market closes, comparable to the dynamics in supercooled systems. This is corroborated by looking at the price correlation functions and non-Gaussian parameters, and…

Click any figure to enlarge with its caption.

Figure 1

Figure 1 Figure 2

Figure 2 Figure 3

Figure 3 Figure 4

Figure 4 Figure 5

Figure 5 Figure 6

Figure 6 Figure 7

Figure 7 Figure 8

Figure 8 Figure 9

Figure 9Peer Reviews

No public reviews on file for this paper yet. If you reviewed it on a platform where reviews are public (OpenReview, ICLR, NeurIPS, ICML), you can paste yours below so the community can read it here.

Videos

No videos yet. Explain this paper in a talk, walkthrough, or lecture? Add one.

Taxonomy

TopicsComplex Systems and Time Series Analysis · Advanced Thermodynamics and Statistical Mechanics · Ecosystem dynamics and resilience

Diffusive and arrested-like dynamics in currency exchange markets

J. Clara-Rahola

Department of Applied Physics, University of Almería, 04120, Almería, Spain

i2TiC Multidisciplinary Research Group, Open University of Catalonia, 08035, Barcelona, Spain

A.M. Puertas

[email protected], [email protected]

Department of Applied Physics, University of Almería, 04120, Almería, Spain

M.A. Sánchez-Granero

Department of Mathematics, University of Almería, 04120, Spain

J.E. Trinidad-Segovia

Department of Economics and Business, University of Almería, 04120, Spain

F.J. de las Nieves

Department of Applied Physics, University of Almería, 04120, Almería, Spain

(March 10, 2024)

Abstract

This work studies the symmetry between colloidal dynamics and the dynamics of the Euro–US Dollar currency exchange market (EURUSD). We consider the EURUSD price in the time range between 2001 and 2015, where we find significant qualitative symmetry between fluctuation distributions from this market and the ones belonging to colloidal particles in supercooled or arrested states. In particular, we find that models used for arrested physical systems are suitable for describing the EURUSD fluctuation distributions. Whereas the corresponding mean squared price displacement (MSPD) to the EURUSD is diffusive for all years, when focusing in selected time frames within a day, we find a two-step MSPD when the New York Stock Exchange market closes, comparable to the dynamics in supercooled systems. This is corroborated by looking at the price correlation functions and non-Gaussian parameters, and can be described by the theoretical model. We discuss the origin and implications of this analogy.

Slow dynamics is common to multiple physical systems such as atoms, granular, and soft-matter systems, as all of them exhibit universal features when approaching the transition towards glass or jammed states Dove (2003); Arimondo et al. (2015); Giordano and Ruta (2016); Franklin and Shattuck (2015); Josserand et al. (2000); Liu and Nagel (2001); Cipelletti and Ramos (2002). A particular hallmark of such framework is the transition towards fluctuation distributions far from Gaussian, usually characterized with long tails, that depict slow structural relaxations within such arrested systems de Vegvar and Fulton (1993); Castillo and Parsaeian (2007); Rygbyt and Roe (1990); Gardel et al. (2009); Duri et al. (2005); Sessoms et al. (2010). Different models have been proposed to reproduce these observations Chaudhuri et al. (2007); March and Tosi (1991). Within this regard, soft matter systems such as colloids, polymers or surfactants have been established as canonic in non equilibrium systems by their own right Fernandez-Nieves and Puertas (2016); Jones (2002), also exhibiting strong symmetries with many other fields, for example, with atomic or molecular systems Pusey and van Megen (1986); Crocker and Grier (1994); Pham et al. (2002). Such symmetry is originated because these are many-body systems of interacting particles, described by equilibrium and non-equilibrium statistical mechanics Poon (2004).

Another field that is strongly amenable to be described by statistical mechanics is financial markets Meyers (2011), where statistical mechanics has proven to be a useful tool. Louis Bachelier’s PhD Thesis, Theory of Speculation triggered, a century ago, an increasing interest for finance from a physical and mathematical point of view Bachelier (2006); Fama and Miller (1972); Fama (1976); Bouchaud and Potters (2000). The introduction of computational techniques allowed the development of models such as the fractal one from Mandelbrot, which in fact resembles fractal descriptions also appearing in colloidal structures Mandelbrot (1997); Peters (1996). However, it has been after the works by Stanley et al. Stanley et al. (1996) when the amount of research papers published by physicists, in economics in general and in finance in particular, has become relevant. Other achievements such as the GARCH model or the Black-Scholes equation helped in the rise of the field known as econophysics, which aims to employ physical theories and models in finance Black and Scholes (1973); Mantegna and Stanley (1996); Francq and Zakolan (2010); Mantegna and Stanley (2007); Richmond et al. (2013). Still, when considering a physical scope, market dynamics is not fully understood; usually stochastic processes, statistical mechanics or non-linear physics are considered when describing market dynamics, but an unified body that describes the equivalence between mass or lengths with financial magnitudes is lacking.

In this paper we study financial markets, namely foreign exchange markets focused on the Euro-US Dollar exchange rate (EURUSD), from a physical approach, typical of undercooled systems. We study the distribution of the variation of the EURUSD price, and analyze it with a theoretical model of supercooled colloids, where the particles are transiently trapped, but can escape on a large time scale. EURUSD dynamics is considered by computing the mean squared price displacement (MSPD), the analogous to the particle mean squared displacement (MSD). While yearly EURUSD fluctuation distributions can be described by the colloidal glass model, MSPDs are diffusive at all times, without a clear hallmark of glassy physics. Arrested states are however found in particular daily time frames, hallmarked by two steps in the evolution of the MSPD, the corresponding correlation function and also, by the equivalent to the non-Gaussian parameter. The description of the dynamics of colloids and the EURUSD exchange rate, poses the question of a symmetry or possible unification between both fields. Therefore, not only a descriptive approach but a physical origin to foreign exchange markets is proposed, where the EURUSD market, is analog to a supercooled colloidal system.

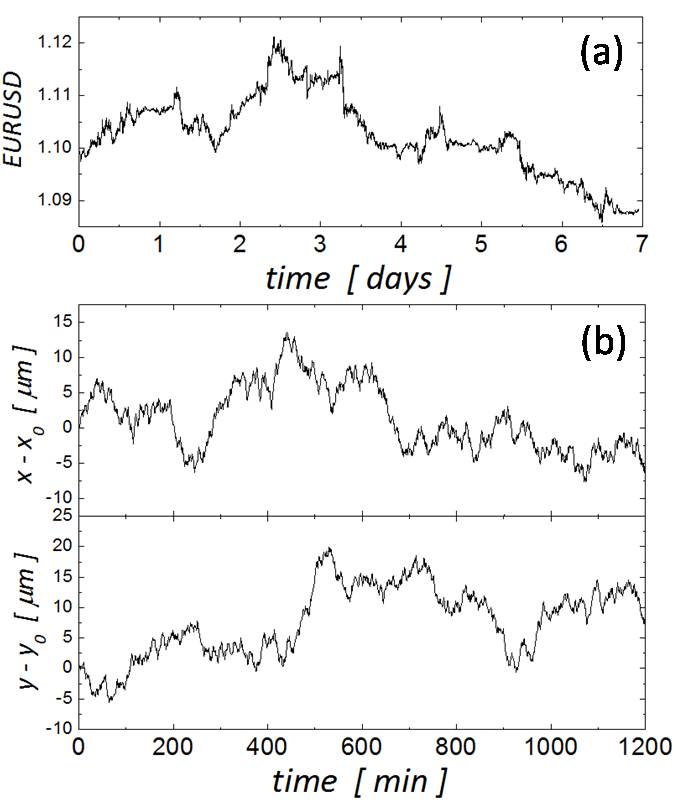

We have selected the EURUSD instantaneous price at time intervals of 1 minute. The price trajectory strikingly resembles the trajectory of a colloidal particle in suspension, shown in Fig. 1. Intrigued by this resemblance, we wonder if the dynamics from currency exchange markets and the one from colloids exhibit a more significant symmetry and if ultimately can be described by equivalent physical laws. Note that colloidal dynamics is driven by parameters such as interparticle interactions, density or applied shear Puertas et al. (2002, 2007); Clara-Rahola et al. (2014, 2015), whereas market dynamics is determined by parameters of very different nature, such as trading volume, number of investors at a given period or balance between supply and demand Kaizoji et al. (2002); Duarte-Queiros (2016); Stosic et al. (2016).

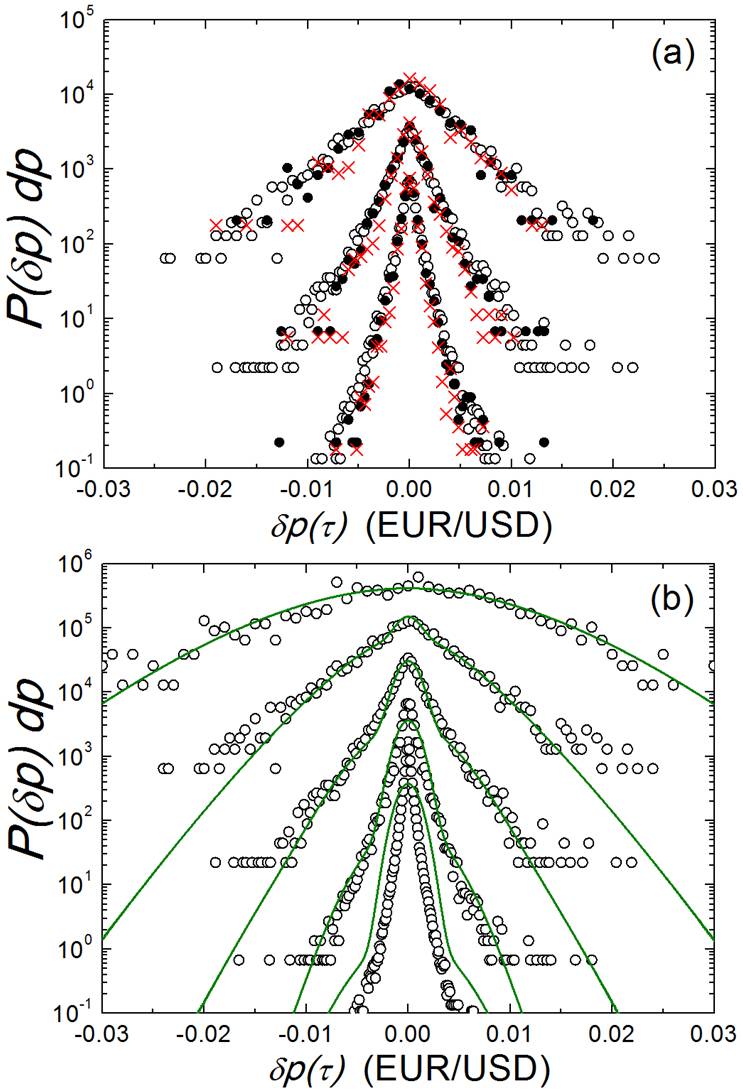

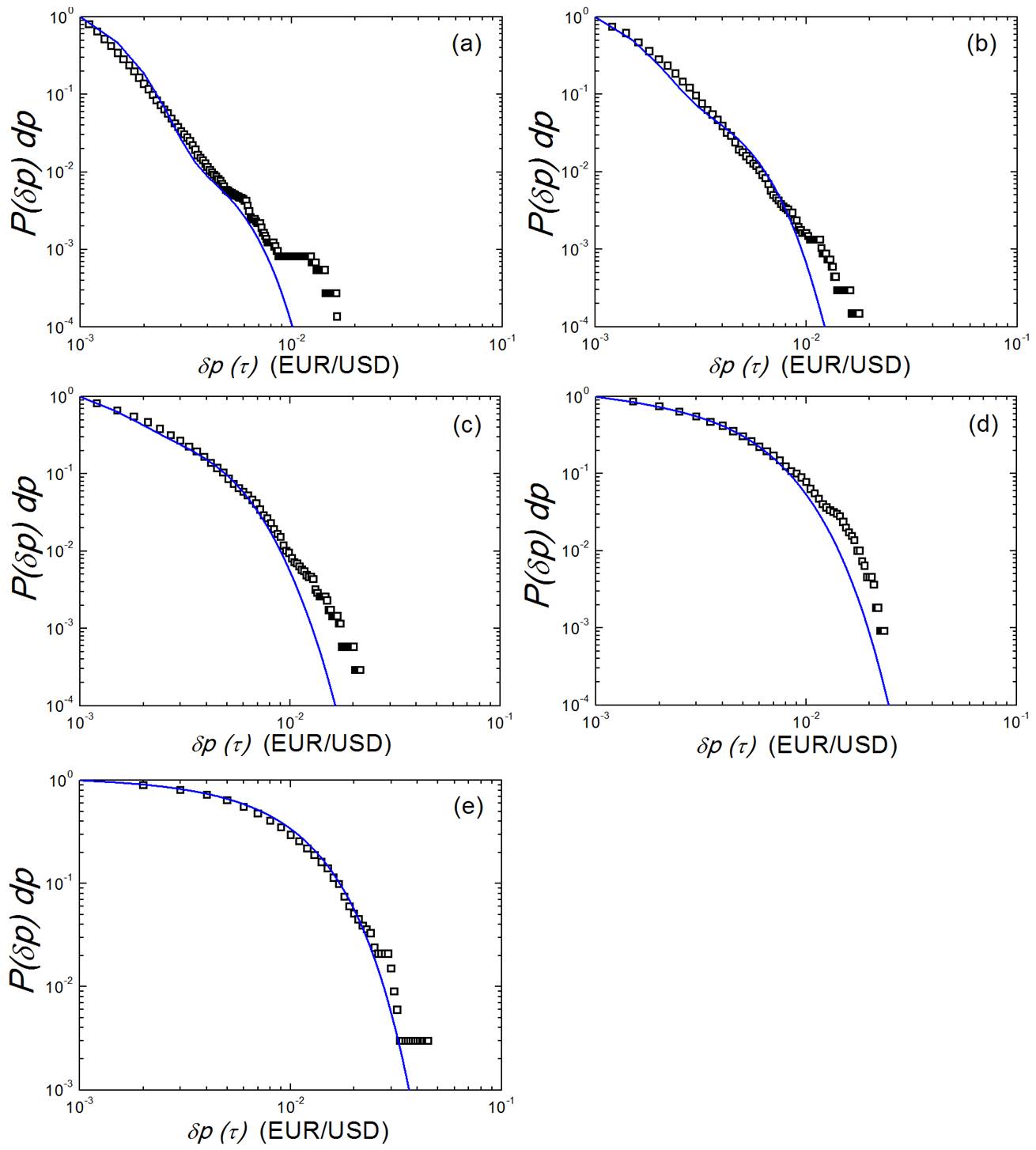

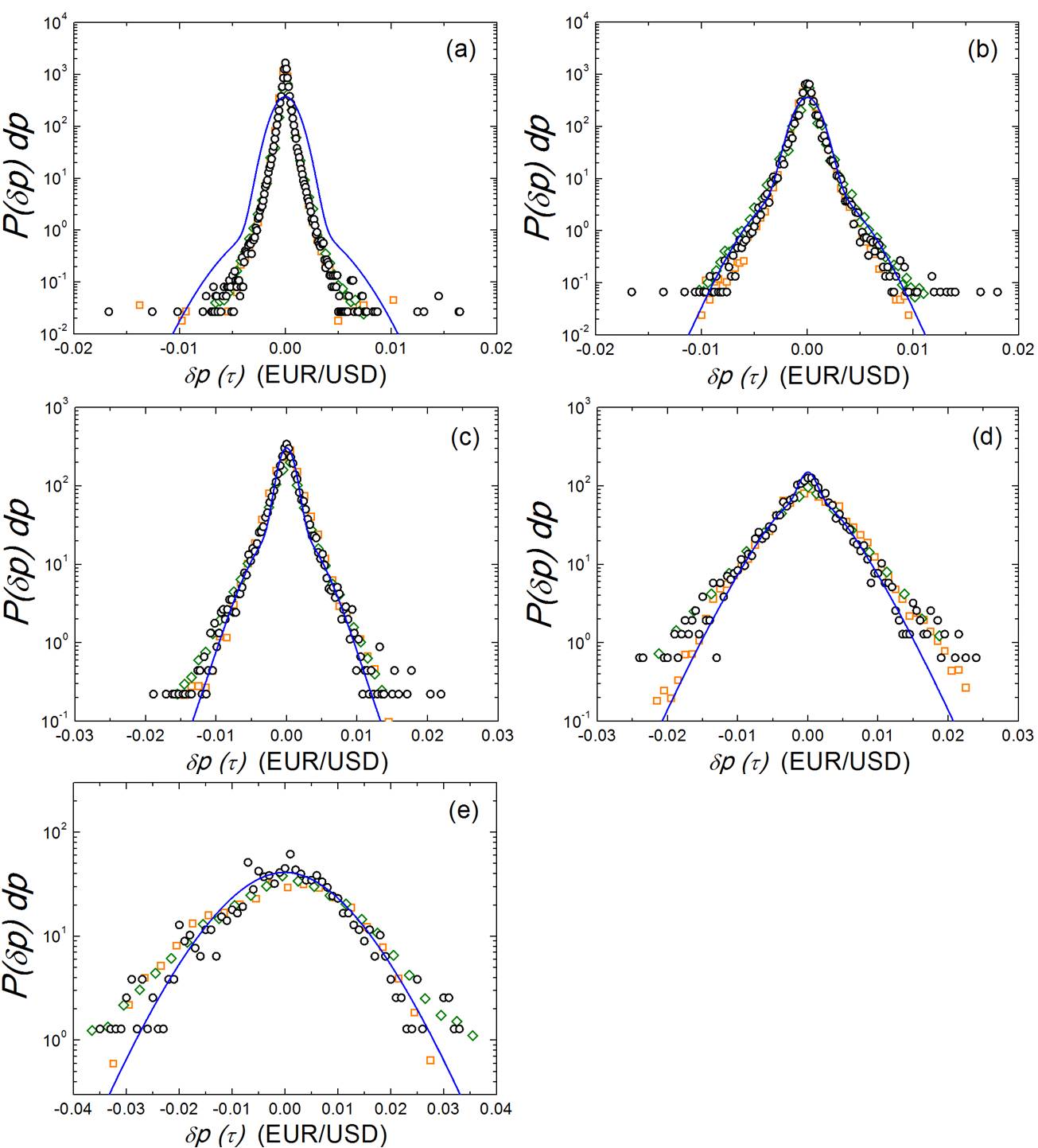

We first study price fluctuations in the EURUSD market, i.e. the difference between prices separated by a lag time , , where the brackets indicate averaging over different time origins, Not . By fixing the magnitude of , we construct the probability distribution function (pdf) of , an analogue to the standard particle displacement distribution. Fig. 2 shows the pdf considering a total time period from 2010 up to 2015, with and min., shifted vertically for clarity. All pdf exhibit a symmetric profile featured by long tails at large , except at the largest , where the pdf is Gaussian within the statistical noise. Similar tailed pdf have been observed in other price fluctuations in finance Mantegna and Stanley (2007); Bouchaud and Potters (2000). These pdf are characteristic to the particular system under study, the EURUSD in our case, and it does not change if different periods are studied; Fig. 2(a) compares the pdf for the years 2001 and 2007 (years with particular economic evolution), with the average in the period .

Aiming to obtain a quantitative description of the price pdf, we borrow a model from glasses that has proven successful when describing data from experiments and simulations Chaudhuri et al. (2007). Typically, tailed distributions in economy are approached by self-similarity or described through Levy flights combined with Gaussian ones Sanchez et al. (2015); Mantegna and Stanley (2007), which are employed in few models, in particular the Cont-Bouchaud spin model Cont and Bouchaud (2000), or the power law one Clauset et al. (2009). However, these require heuristic arguments or restrictions, such as a constant number of market investors or agents correlated according to trading strategies, proposed to be equal to spin domains. Our scope avoids considering these kind of conditions, as we directly study the EURUSD market as a whole, where any agent can behave freely. In physical glasses, every particle is ideally caged by its own neighbours, restricting the structural relaxation of the whole system. Thermal fluctuations, however, allows particles to jump from one cage to another, on a large time scale. It is also useful to recall the classical description of glasses or undercooled fluids in terms of their free energy landscape containing multiple shallow minima (basins), separated by high barriers Goldstein (1969). A similar model for financial markets, implying that the price is transiently trapped and eventually jumps out on large time scales, is attempted in the following, based on a simple model for particle glasses developed by Chaudri et al. Chaudhuri et al. (2007).

In the model, particles are transiently trapped in cages, described by a time-independent Gaussian pdf ( in their work). Long range jumps are possible, according to a Gaussian distribution , on a large time scale. The probability to jump for the first time is given by an exponential distribution while subsequent jumps occur faster according to , with . The overall displacement distribution, or van Hove function, depicts the probability of finding a particle in , at time , and it is calculated in the Fourier-Laplace domain, . Here, we have considered this van Hove distribution to analyze the EURUSD pdf, taking into consideration the new dimensionality of the problem, the scalar price instead of the position vector. Back transforming to price-time domain, the distribution reads:

[TABLE]

Here , is the Fourier transform of function , is the conjugate variable of price in the Fourier space and denotes the Inverse Fourier Transform. In this original model, the particle is assumed to explore its cage on a time scale much shorter than or , thus is time independent. Because this assumption can not be made a priori in the EURUSD system, the model is modified to introduce short time diffusion, implying thus a finite time to explore the cage. For this purpose, we consider an Ornstein-Uhlenbeck process to calculate , with the diffusion coefficient and Uhlenbeck and Ornstein (1930); Gillespie (1996); Risken (1989). This depicts a particle describing Brownian motion with a linear central force pulling it towards its origin.

Using this new model, the experimental pdf are fitted, as shown in Fig. 2 (lower panel), using , , , and , as fitting parameters, identical for all values of . The values of the parameters are: , , resulting in very good agreement with the experimental data, except for the lowest . The comparison of the complementary cumulative distribution functions (cdf) from the model and experimental data, which is focused on the behaviour at long distances, is also satisfactory, as shown in the supplemental material Sup . Note that parameters indicate the EURUSD price caged within intervals of ca. cents, and jumps out of this range occur on a time scale of approximately five hours.

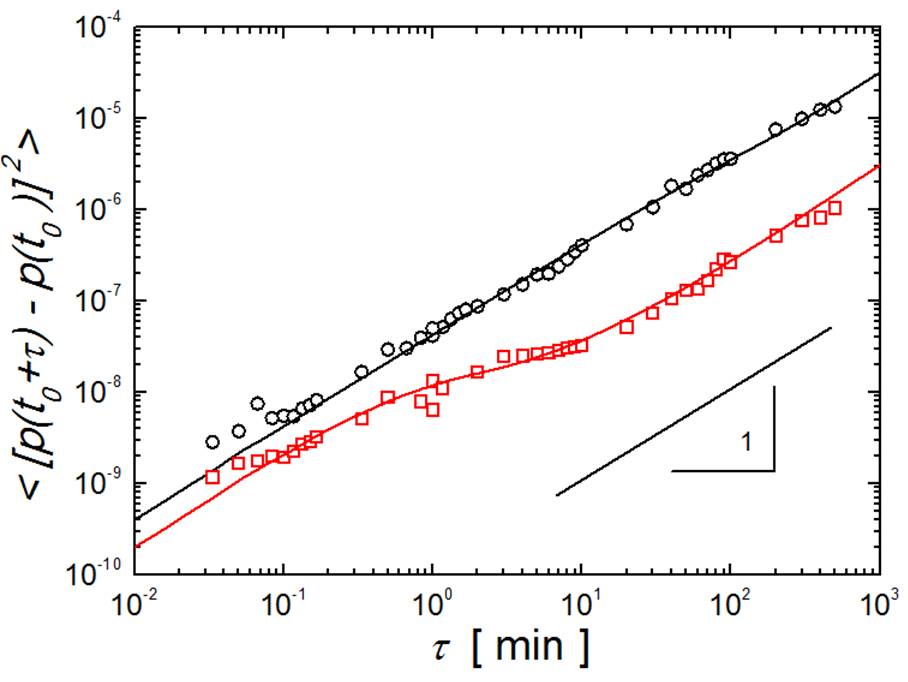

A hallmark of undercooled systems, as mentioned previously, is the separation between microscopic and structural dynamics, which results in correlation functions decaying in two steps, or intermediate plateaus in the tagged particle mean squared displacement (MSD)Lubelski et al. (2008); Scheffold et al. (2001); Weitz and Pine (1993). Analogously, we propose the mean squared price displacement (MSPD):

[TABLE]

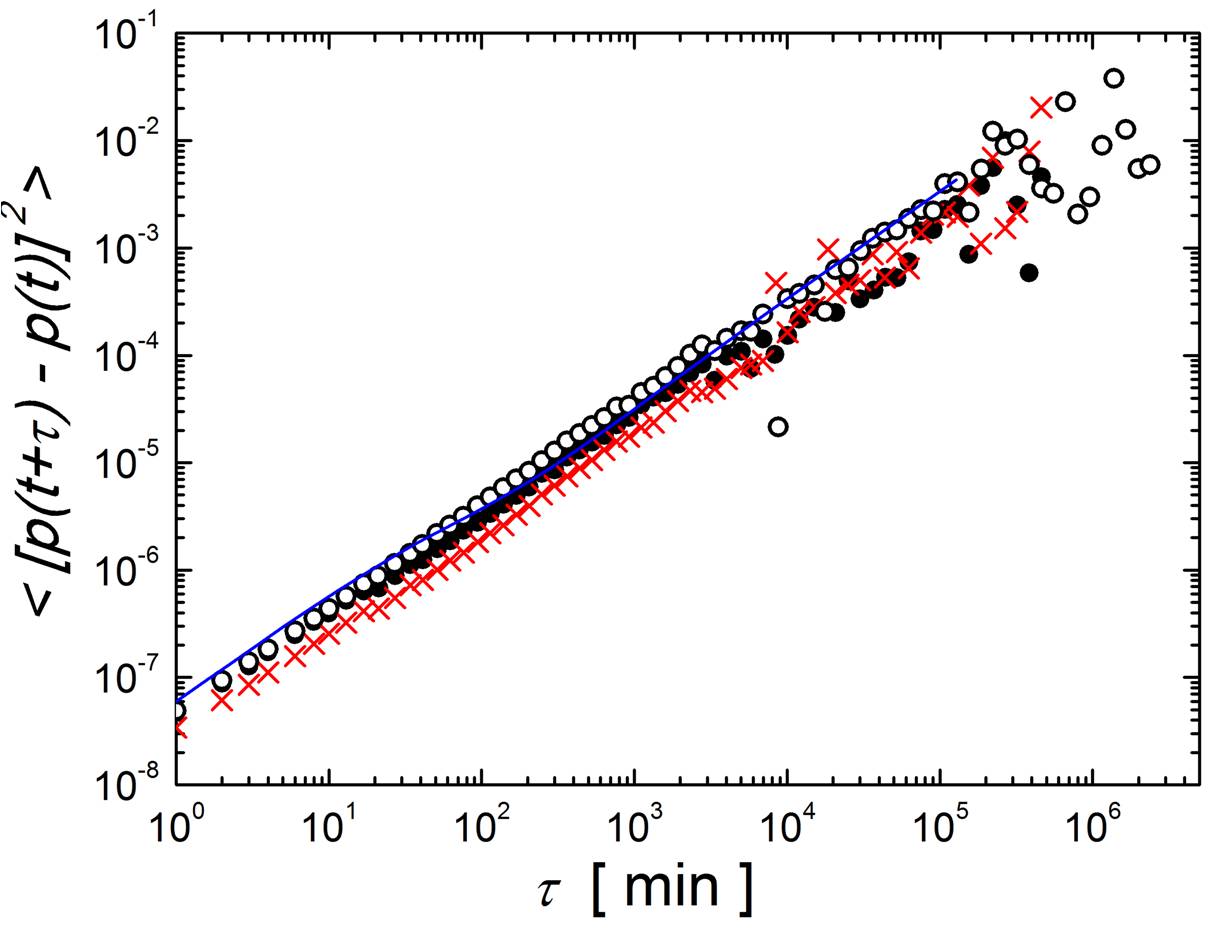

Despite fluctuation pdf being characteristic to arrested systems, the MSPD is linear, as indicated in Fig. 3. Even more, such diffusive behavior is found in all years, shown in Fig. 3, and all MSPDs exhibit a common origin, indicating that the diffusion coefficient, therefore market dynamics, is characteristic of the EURUSD regardless of the year considered, including years of conflict to economy, such as or . In passing we note that short time dynamics is Brownian, what leads to establish the analogy with undercooled colloids, either glasses or gels, rather than atomic glasses. The MSPD calculated from our model is also presented in Fig. 3, correctly reproducing the data. The precise combination of the parameters and produces this linear evolution of although the pdf differ clearly from Gaussian.

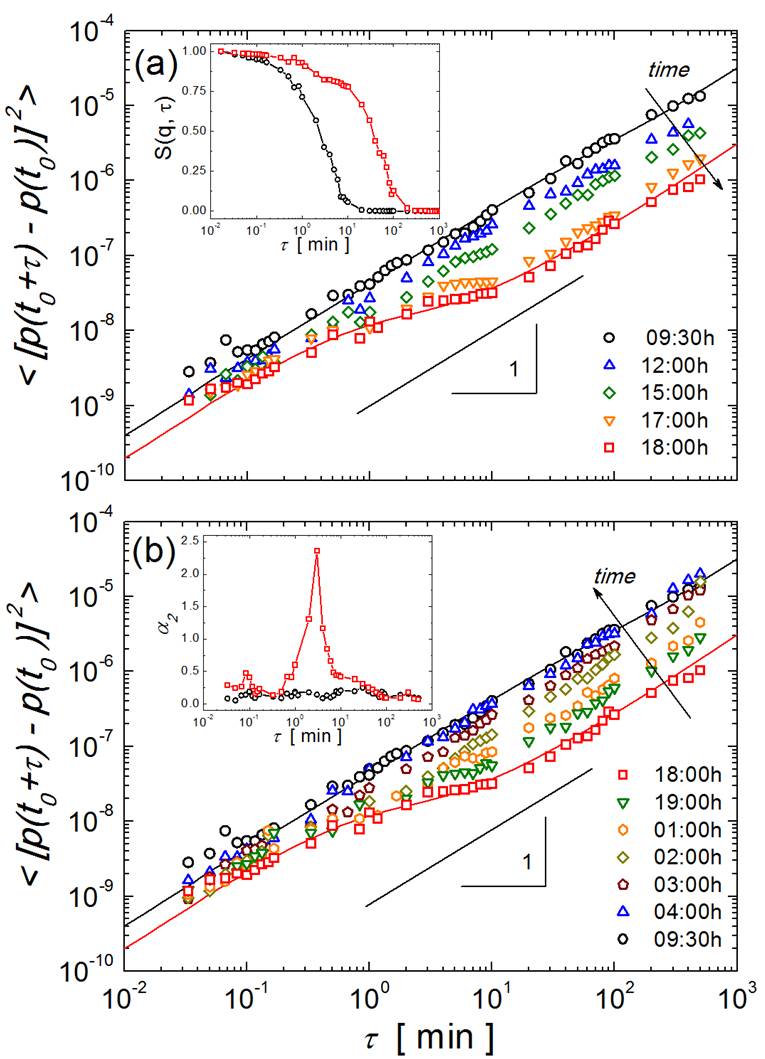

Given this unexpected result, we seek a particular case or regime where the non-Gaussian components are important enough to produce deviations in the MSPD with respect to Brownian diffusion. Thus, we de-aggregate the data according to the commencing time, and study the dynamics for the next 24 hours. Additionally, we change the database to second-resolved prices, to access the short time dynamics. In particular, the year is studied and we first set the starting point for the calculation of at the opening of the New York Stock Exchange (NYSE), 9:30 am Eastern Time (ET). The MSPD for the forthcoming 24 hours after this commencing time, , is averaged over all possible days. The same procedure is repeated for different values of , covering the range of 24 hours. Recall that foreign exchange markets remain open continuously besides weekends. Results are presented in Fig. 4, where a striking dependence of the MSPD with can be identified.

When the opening of the NYSE is taken as starting time, the dynamics is diffusive, but for later commencing times, the magnitude of the MSPD decreases and a shoulder appears at intermediate times, when approaches the closure of NYSE. This trend continues developing and at 6:00pm ET the MSPD becomes minimal, exhibiting an initial diffusion-like increase at low , crossing over to a quasi-plateau, and recovering again the linear behaviour for large . This behaviour is close to the profile commonly found in arrested colloidal systems, either by aggregation, or at high particle density Wyss et al. (2001); Nugent et al. (2007), due to the transient trapping of particles inside cages of neighbours (in glasses), or in a network of bonds (in gels). The same behaviour in the MSPD suggests that price dynamics considered at daily periods with the starting time between 3:00pm and 6:00pm ET undergoes to a temporary dynamic arrest. The transient trapping has a typical time scale of about min., and is followed by diffusive dynamics. Commencing times later than 6:00pm reverse this trend; MSPDs increase and the intermediate plateau vanishes, approaching diffusion when the starting point of the MSPD calculation is between 2:00am and 4:00am, with the maximum MSPD at 9:30am. This observation is consistent with the correlation of market behaviour with activity, as done by Ito and Hashimoto for the US Dollar - Japanese Yen market Ito and Hashimoto (2006).

The theoretical model can rationalize this behaviour, as shown in Fig. 4, for the two extreme cases, 9:30am and 6:00pm. To fit the model, and the time scales and where fixed for all , as these are expected to be intrinsic to the EURUSD system, and only and are varied. The fits shown in the figure are obtained for and for 9:30am, and and for 6:00pm. Note that in the latter, both and are much smaller, but also , characteristic of arrested systems, and the cage size is of order .

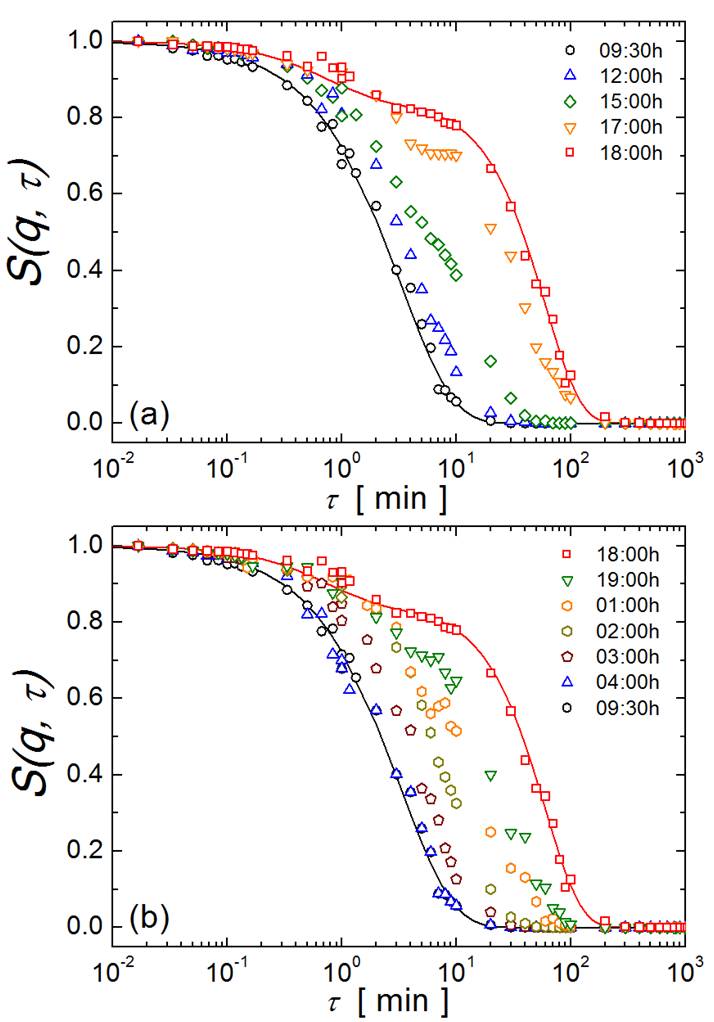

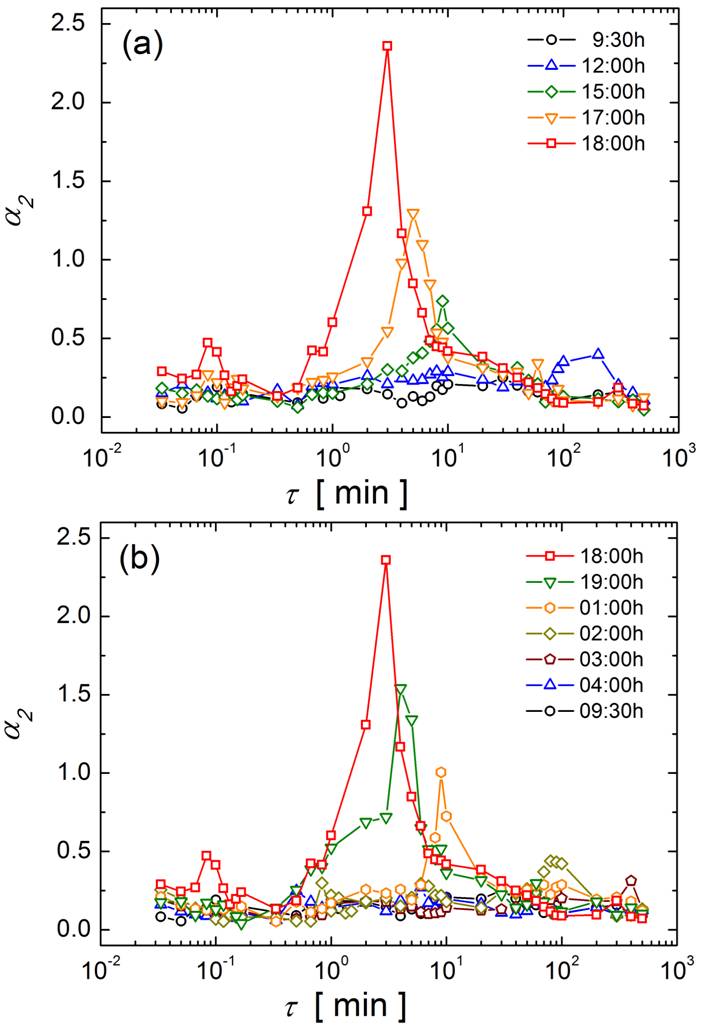

Given this similarity at the level of the MSPD, we study other properties which serve to identify undercooled states or glasses, in particular, the dynamic structure factor, , and the one-dimensional non-Gaussian parameter, . starts from decaying to zero in fluids and to a finite value in glasses. In undercooled systems, it shows an intermediate plateau, that depends on the wavevector, . For the EURUSD system, we select a value of to probe this range of price variations, and the resulting correlation functions are shown in the inset to Fig. 4a, and further detailed at the supplemental material Sup . The non-Gaussian parameter, , on the other hand, quantifies the deviation of the pdf from Gaussian. In undercooled fluids, starts from zero (the pdf is Gaussian at short times), describes a maximum when the particles are caged and start to break free, to become zero again at long times. The non-Gaussian parameter for the EURUSD system, shown in the inset to Fig. 4b and detailed at the supplemental material Sup , indeed shows a maximum when 6:00pm in the time range where the shoulder of the MSPD appears. Both and confirm the analogy between the dynamics of supercooled fluids and the EURUSD market.

The dynamics of economic markets is often described as diffusive, based on the linear MSPD profile when considering long periods, where the efficient market hypothesis (EMH) or fractal market hypothesis (FMH) can be invoked to explain such behavior Malkiel and Fama (1970); Peters (1989). The EMH states that market prices are due to all market information being available, making it impossible to beat the market; such statement is in fact compatible with a random walk. We show in this study that this diffusion-like behaviour is found only when averages over long times are taken in the MSPD, , but disappear when local time averages at hours periods are performed and where either diffusive or arrested dynamics are featured. The FMH states, on the other hand, that investment strategies converge when considering short time frames, arresting the market dynamics and making it more inefficient. Our analysis suggests a fluid-to-glass transition upon the choice of the reference MSPD time, implying that markets become either efficient or fractal-like, depending on their activity.

In particle systems, the different dynamical regimes typical of fluid-to-glass transitions are obtained switching a physical parameter that controls the interaction between particles. It must be then further sought, which is the origin of the non-trivial dynamics shown above and if the analogy can be exploited to identify the equivalent set of parameters that control market dynamics, such as traded volume, number of investors in the market or even policy decisions from regulatory institutions. Furthermore, the symmetry between colloidal systems and the EURUSD exchange market is as well found in other currency pairs, such as the EURCHF. A new approach appears, where exchange rate currency pairs can be regarded as colloidal systems and due to their coupled dynamics, the whole foreign exchange market can be considered a single undercooled system. This view and its natural extension to stock and other markets lays promising when modeling financial markets and needs to be further addressed.

Acknowledgements.

We acknowledge histdata.com and oanda.com for providing all currency exchange data. Funding from UOC, project N11-6139473, aimed at enhancing submission to H2020 calls, (J. C.-R.), the Spanish Ministerio de Economía, Industria y Competitividad and the European Regional Development Fund (ERDF) under project No. FIS2015-69022-P and MTM2015-64373-P, are gratefully acknowledged.

The reference list from the paper itself. Each links out to its DOI / PubMed record.

- 1Dove (2003) M. T. Dove, Structure and Dynamics: An Atomic View of Materials (Oxford University Press, 2003).

- 2Arimondo et al. (2015) E. Arimondo, C. C. Lin, and S. F. Yelin, eds., Advances in Atomic, Molecular, and Optical Physics (Academic Press Inc, 2015).

- 3Giordano and Ruta (2016) V. M. Giordano and B. Ruta, Nat. Commun. 7 , 10344 (2016).

- 4Franklin and Shattuck (2015) S. V. Franklin and M. D. Shattuck, eds., Handbook of Granular Materials (CRC Press, 2015).

- 5Josserand et al. (2000) C. Josserand, A. V. Tkachenko, D. M. Mueth, and H. M. Jaeger, Phys. Rev. Lett. 85 , 3632 (2000).

- 6Liu and Nagel (2001) A. J. Liu and S. R. Nagel, eds., Jamming and Rheology (CRC Press, 2001).

- 7Cipelletti and Ramos (2002) L. Cipelletti and L. Ramos, Curr. Op. Coll. Interf. Sci. 7 , 228 (2002).

- 8de Vegvar and Fulton (1993) P. G. N. de Vegvar and T. A. Fulton, Phys. Rev. Lett. 71 , 3537 (1993).