Parallel Optimization of Polynomials for Large-scale Problems in Stability and Control

Reza Kamyar

TL;DR

This paper develops parallel algorithms for large-scale polynomial optimization problems in control theory, enabling stability analysis of high-dimensional systems using supercomputers to handle complex SDPs efficiently.

Contribution

It introduces parallel algorithms for solving large SDPs in stability analysis, leveraging problem structure and supercomputing resources for scalability.

Findings

Efficiently analyzes systems with 100+ dimensions

Parallel algorithms utilize hundreds to thousands of processors

Demonstrates scalability on supercomputers

Abstract

In this thesis, we focus on some of the NP-hard problems in control theory. Thanks to the converse Lyapunov theory, these problems can often be modeled as optimization over polynomials. To avoid the problem of intractability, we establish a trade off between accuracy and complexity. We develop a sequence of tractable optimization problems - in the form of LPs and SDPs - whose solutions converge to the exact solution of the NP-hard problem. However, the computational and memory complexity of these LPs and SDPs grow exponentially with the progress of the sequence - meaning that improving the accuracy of the solutions requires solving SDPs with tens of thousands of decision variables and constraints. Setting up and solving such problems is a significant challenge. The existing optimization algorithms and software are only designed to use desktop computers or small cluster computers -…

Click any figure to enlarge with its caption.

Figure 1

Figure 1 Figure 2

Figure 2 Figure 3

Figure 3 Figure 4

Figure 4 Figure 5

Figure 5 Figure 6

Figure 6 Figure 7

Figure 7 Figure 8

Figure 8 Figure 9

Figure 9 Figure 10

Figure 10 Figure 11

Figure 11 Figure 12

Figure 12 Figure 13

Figure 13 Figure 14

Figure 14 Figure 15

Figure 15 Figure 16

Figure 16 Figure 17

Figure 17 Figure 18

Figure 18 Figure 19

Figure 19 Figure 20

Figure 20 Figure 21

Figure 21 Figure 22

Figure 22 Figure 23

Figure 23 Figure 24

Figure 24 Figure 25

Figure 25 Figure 26

Figure 26 Figure 27

Figure 27 Figure 28

Figure 28 Figure 29

Figure 29 Figure 30

Figure 30 Figure 31

Figure 31 Figure 32

Figure 32 Figure 33

Figure 33 Figure 34

Figure 34 Figure 35

Figure 35 Figure 36

Figure 36 Figure 37

Figure 37 Figure 38

Figure 38| \pbox60cmNumber of processors | |||

|---|---|---|---|

| \pbox60cmComputational | |||

| cost per processor |

| Number of processors | |||

|---|---|---|---|

| communication cost per processor |

| 0.036 | 0.143 | 0.286 | 0.429 | 0.571 | 0.714 | 0.857 | 0.964 | |

| 0 | 1 | 2 | |

|---|---|---|---|

| 1 | Infeasible | Infeasible | Infeasible |

| 2 | Infeasible | -0.102 | Out of Memory |

| 3 | Infeasible | Out of Memory | Out of Memory |

| 0.4 | 0.0015 | 45 | 0.1 |

| On-peak | Off-peak | Demand | |

|---|---|---|---|

| APS | 0.089 | 0.044 | 13.50 |

| Prices | Demand-limiting | Production cost | Demand peak | |

|---|---|---|---|---|

| high | 46.78 (0.086) | 7.4132 | ||

| Optimal | medium | 51.56 (0.116) | 8.2898 | |

| low | 59.42 (0.168) | 9.6749 |

| Strategy | Production cost | Demand peak | |

|---|---|---|---|

| Optimal | 1,595,309 | 195.607 | |

| SRP | 1,677,516 | 211.79 |

| Customers | Elect. Bill | Demand peak | |

|---|---|---|---|

| Solar & | 50.052 | 6.1947 | |

| Non-solar | 84.717 | 8.6787 | |

| Single Non-solar | 83.333 | 8.3008 | |

| Single Solar | 54.311 | 6.1916 |

Peer Reviews

No public reviews on file for this paper yet. If you reviewed it on a platform where reviews are public (OpenReview, ICLR, NeurIPS, ICML), you can paste yours below so the community can read it here.

Videos

No videos yet. Explain this paper in a talk, walkthrough, or lecture? Add one.

Taxonomy

TopicsAdvanced Optimization Algorithms Research · Stability and Control of Uncertain Systems · Advanced Control Systems Optimization

title

author

Reza Kamyar

Parallel Optimization of Polynomials for Large-scale Problems in

Stability and Control

author

Reza Kamyar

Abstract

In today’s world, optimal operation of ever-growing industries and markets often requires solving optimization problems with unprecedented sizes. Economic dispatch of generating units in power companies, frequency assignment in large mobile communication networks, profit maximization in competitive markets, and optimal operation of smart grids are few examples of many real-world problems which can be closely modeled as optimization over a large number (tens of thousands) of integer- and real-valued decision variables. Unfortunately, majority of the existing commercial off-the-shelf software are not designed to scale to optimization problems of this size. Moreover, in theory, these optimization problems often fall into the class NP-hard - meaning that despite the tremendous effort towards modernization of optimization algorithms, it is widely suspected that no algorithm can find exact solutions to these problems in a reasonable amount of time.

In this thesis, we focus on some of the NP-hard problems in control theory. Thanks to the converse Lyapunov theory, these problems can often be modeled as optimization over polynomials. To avoid the problem of intractability, we establish a trade off between accuracy and complexity. In particular, we develop a sequence of tractable optimization problems - in the form of Linear Programs (LPs) and/or Semi-Definite Programs (SDPs) - whose solutions converge to the exact solution of the NP-hard problem. However, the computational and memory complexity of these LPs and SDPs grow exponentially with the progress of the sequence - meaning that improving the accuracy of the solutions requires solving SDPs with tens of thousands of decision variables and constraints. Setting up and solving such problems is a significant challenge. Unfortunately, the existing optimization algorithms and software are only designed to use desktop computers or small cluster computers - machines which do not have sufficient memory for solving such large SDPs. Moreover, the speed-up of these algorithms does not scale beyond dozens of processors. This in fact is the reason we seek parallel algorithms for setting-up and solving large SDPs on large cluster- and/or super-computers.

We propose parallel algorithms for stability analysis of two classes of systems: 1) Linear systems with a large number of uncertain parameters; 2) Nonlinear systems defined by polynomial vector fields. First, we develop a distributed parallel algorithm which applies Polya’s and/or Handelman’s theorems to some variants of parameter-dependent Lyapunov inequalities with parameters defined over the standard simplex. The result is a sequence of SDPs which possess a block-diagonal structure. We then develop a parallel SDP solver which exploits this structure in order to map the computation, memory and communication to a distributed parallel environment. We produce a Message Passing Interface (MPI) implementation of our parallel algorithms and provide a comprehensive theoretical and experimental analysis on its complexity and scalability. Numerical tests on a supercomputer demonstrate the ability of the algorithm to efficiently utilize hundreds and potentially thousands of processors and analyze systems with 100+ dimensional state-space. We then apply our algorithms to two real-world problems: Stability of plasma in a Tokamak reactor, and optimal electricity pricing in a smart grid environment. Finally, we extend our algorithms to analyze robust stability over more complicated geometries such as hypercubes and arbitrary convex polytopes. Our algorithms can be readily extended to address a wide variety of problems in control; e.g., control synthesis for systems with parametric uncertainty, computing control Lyapunov functions for optimal control problems, and analysis and control of switched/hybrid systems.

TABLE OF CONTENTS

-

3.3 Interior-point Algorithms for Convex Problems with Inequality Constraints

-

3.5 A Primal-dual Interior-point Algorithm for Semi-definite Programming

-

4 PARALLEL ALGORITHMS FOR ROBUST STABILITY ANALYSIS OVER SIMPLEX

-

4.3 Setting-up the Problem of Robust Stability Analysis over a Simplex

-

4.3.3 The Elements of the SDP Problem Associated with Polya’s Theorem

-

4.6.1 Complexity Analysis for Systems with Large Number of States

-

4.6.2 Complexity of Increasing Accuracy/Decreasing Conservativeness

-

4.7.1 Example 1: Application to Control of a Discretized PDE Model in Fusion Research

-

5 PARALLEL ALGORITHMS FOR ROBUST STABILITY ANALYSIS OVER HYPERCUBES

-

5.2 Notation and Preliminaries on Multi-homogeneous Polynomials

-

5.3 Setting-up the Problem of Robust Stability Analysis over Multi-simplex

-

5.3.2 The SDP Elements Associated with the Multi-simplex Version of Polya’s Theorem

-

5.4 Computational Complexity Analysis of the Set-up Algorithm

-

5.4.3 Speed-up and Memory Requirement of the Set-up Algorithm:

-

5.5.2 Example 2: Verifying Robust Stability over a Hypercube

-

6.5.1 Complexity of the LP Associated with Handelman’s Representation

-

6.5.2 Complexity of the SDP Associated with Polya’s Algorithm

-

7 OPTIMIZATION OF SMART GRID OPERATION: OPTIMAL UTILITY PRICING AND DEMAND RESPONSE

-

7.2 Problem Statement: User-level and Utility Level Problems

-

7.3 Solving User- and Utility-level Problems by Dynamic Programming

-

7.4.1 Effect of Electricity Prices on Peak Demand and Production Costs

-

7.4.2 Optimal Thermostat Programming with Optimal Electricity Prices

-

8 SUMMARY, CONCLUSIONS AND FUTURE DIRECTIONS OF OUR RESEARCH

-

8.2.1 A Parallel Algorithm for Nonlinear Stability Analysis Using Polya’s Theorem

-

8.2.2 Parallel Computation for Parameter-varying -optimal Control Synthesis

-

8.2.3 Parallel Computation of Value Functions for Approximate Dynamic Programming

LIST OF TABLES

- 4.1 Per Processor, Per Iteration Computational Complexity of the Set-up Algorithm. is the Number of Monomials Is ; Is the Number of Monomials in ; Is the Number of Monomials in .

- 4.2 Per Processor, Per Iteration Communication Complexity of the Set-up Algorithm. is the Number of Monomials Is ; Is the Number of Monomials in ; Is the Number of Monomials in .

- 4.3 Data for Example 1: Nominal Values of the Plasma Resistivity

- 4.4 Upper Bounds Found for by the SOS Algorithm Using Different Degrees for and (inf: Infeasible, O.M.: Out of Memory)

- 5.1 The Lower-bounds on Computed by Algorithm 7 Using Different Degree Vector and Using Methods in Bliman (2004a) and Chesi (2005).

- 7.1 Building’s Parameters as Determined in Section 7.2.1

- 7.2 On-peak, Off-peak & Demand Prices of Arizona Utility APS

- 7.3 CASE I: Electricity Bills (or Three Days) and Demand Peaks for Different Strategies. Electricity Prices Are from APS.

- 7.4 CASE I: Costs of Production (for Three Days) and Demand Peaks for Various Prices and Strategies. Prices Are Non-regulated and SRP’s Coefficients of Utility Cost Are: 0.00401 \nu=/(MWh)

- 7.5 CASE II: Production Costs (for Three Days) and Demand Peaks Associated with Regulated Optimal Electricity Prices (Calculated by Algorithm 10) and SRP’s Electricity Prices. SRP’s Marginal Costs: a=0.0814\frac{\}{kWh},b=59.76\frac{$}{kW}$

- 7.6 CASE III: Optimal Electricity Prices, Bills (for Three Days) and Demand Peaks for Various Customers. Marginal osts from SRP: a=0.0814\frac{\}{kWh},b=59.76\frac{$}{kW}$

LIST OF FIGURES

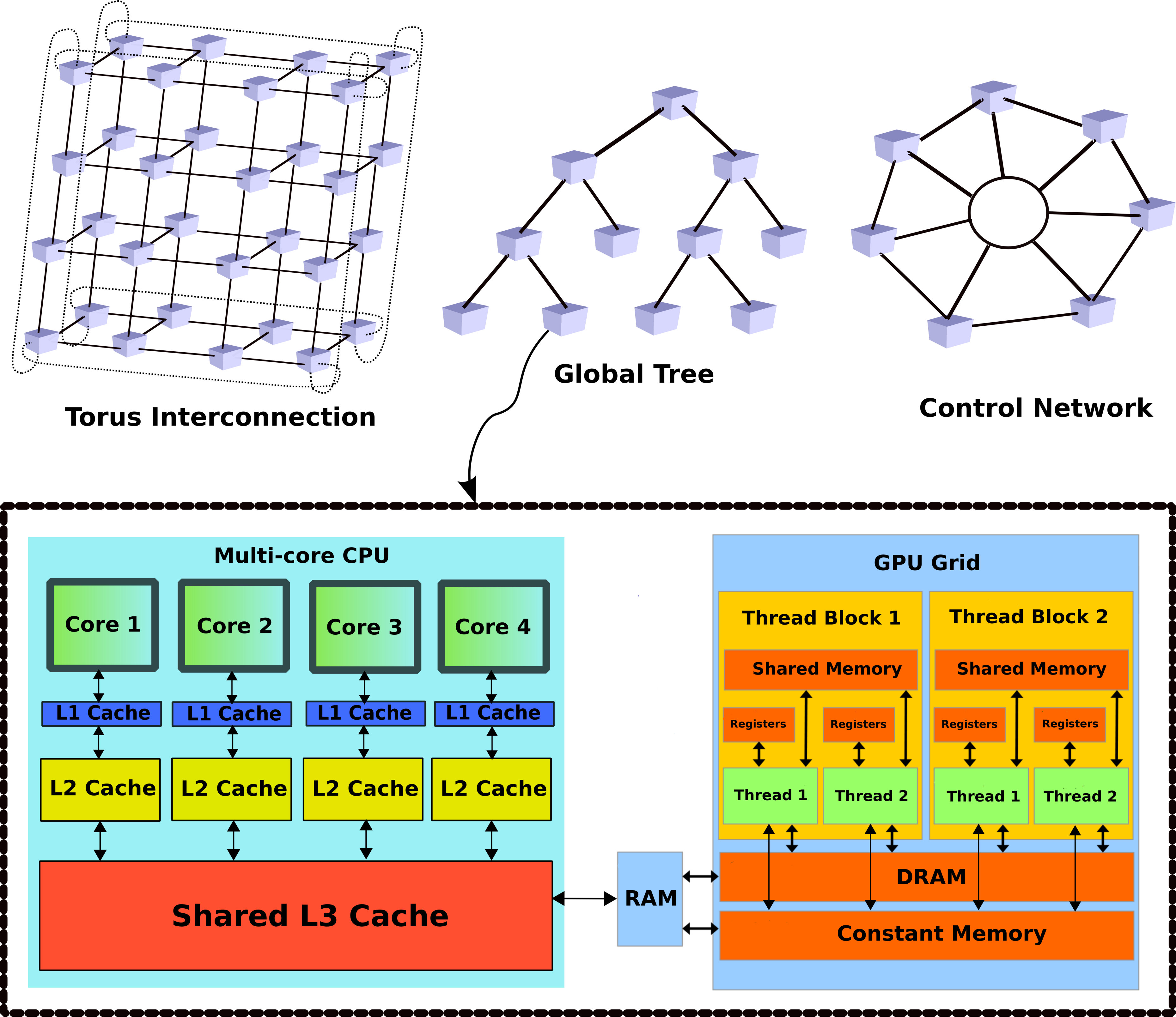

- 4.1 Various Interconnections of Nodes in a Cluster Computer (Top), Typical Memory Hierarchies of a GPU and a Multi-core CPU (bottom)

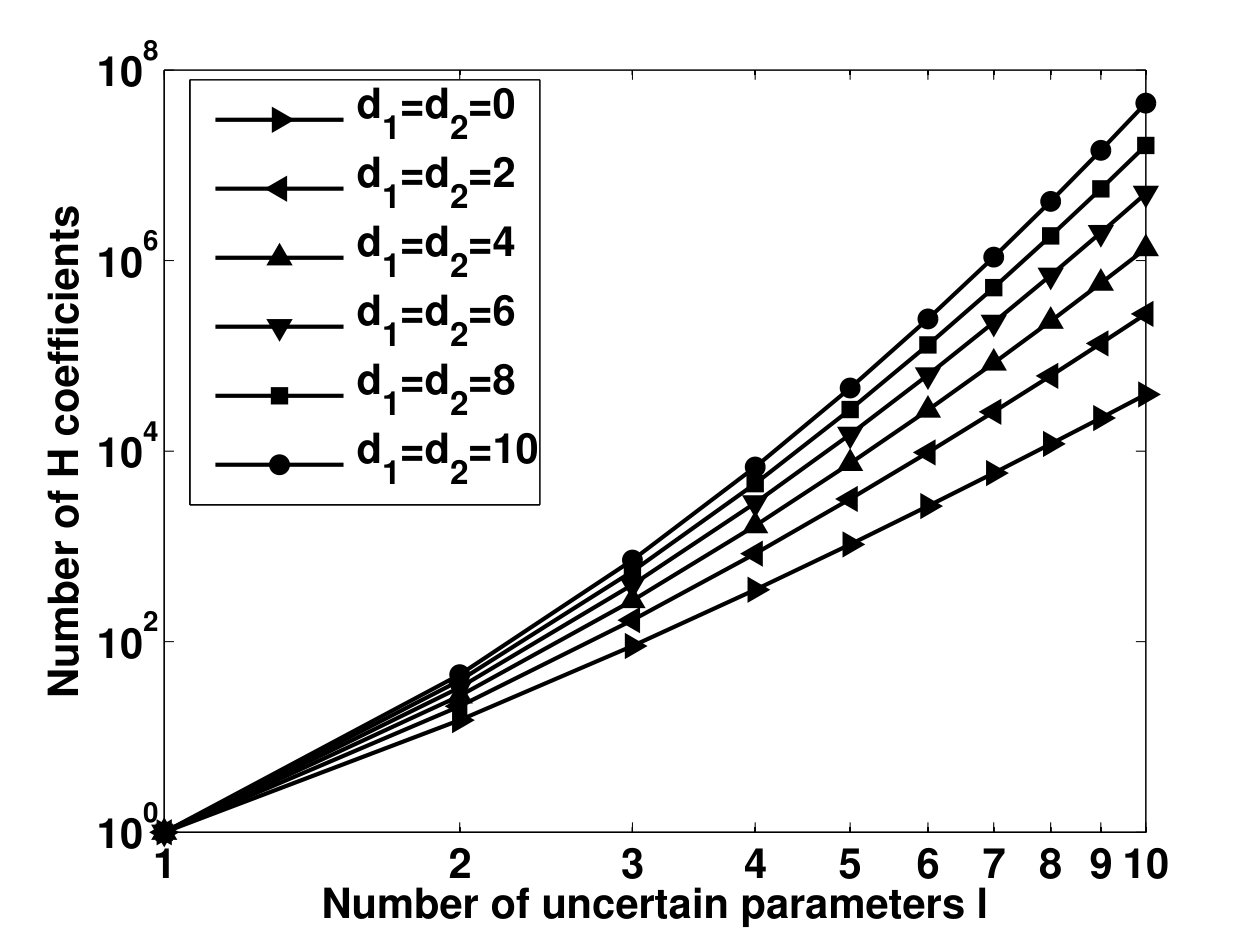

- 4.2 Number of Coefficients vs. the Number of Uncertain Parameters for Different Polya’s Exponents and for

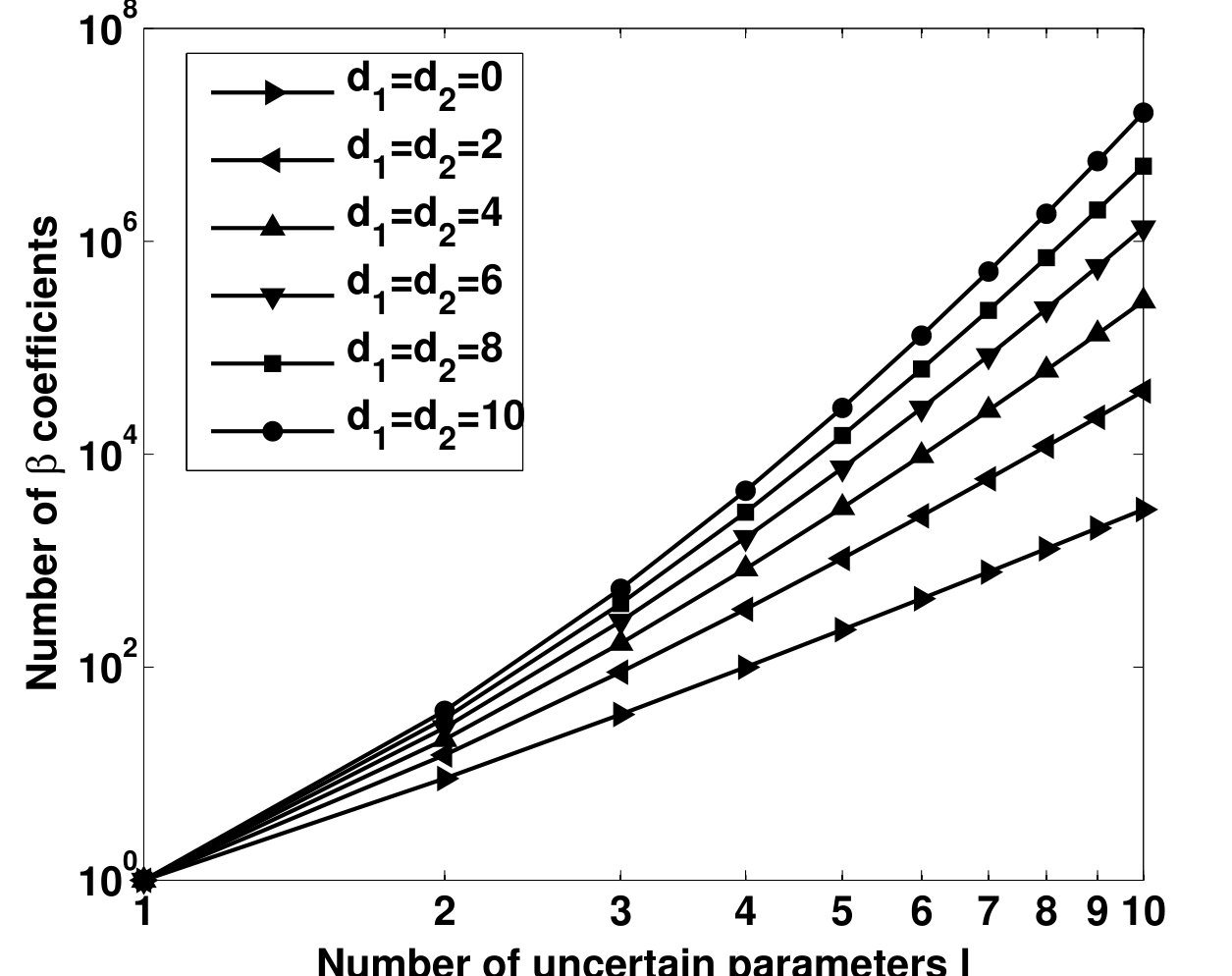

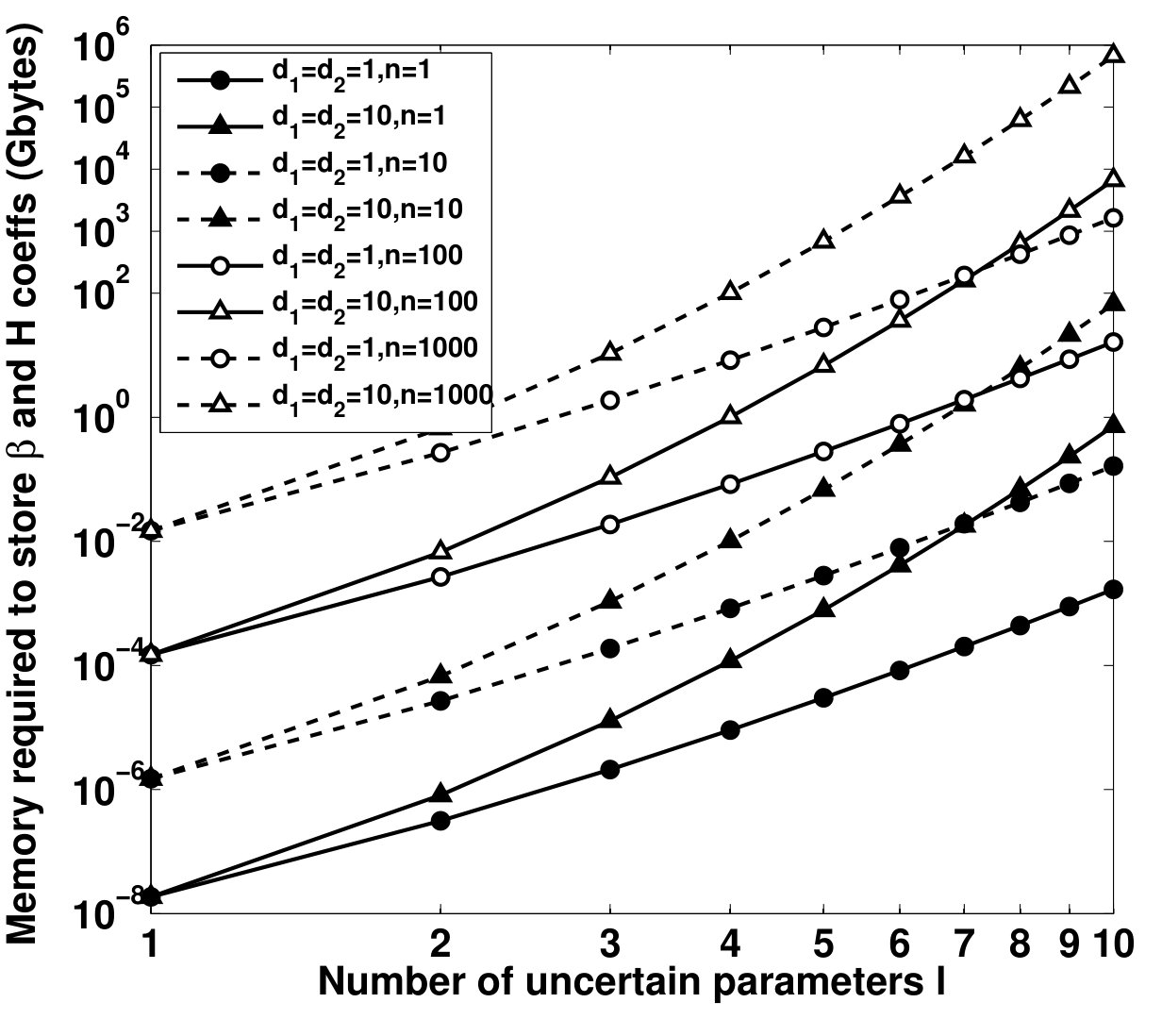

- 4.4 Memory Required to Store the Coefficients and vs. Number of Uncertain Parameters, for Different and

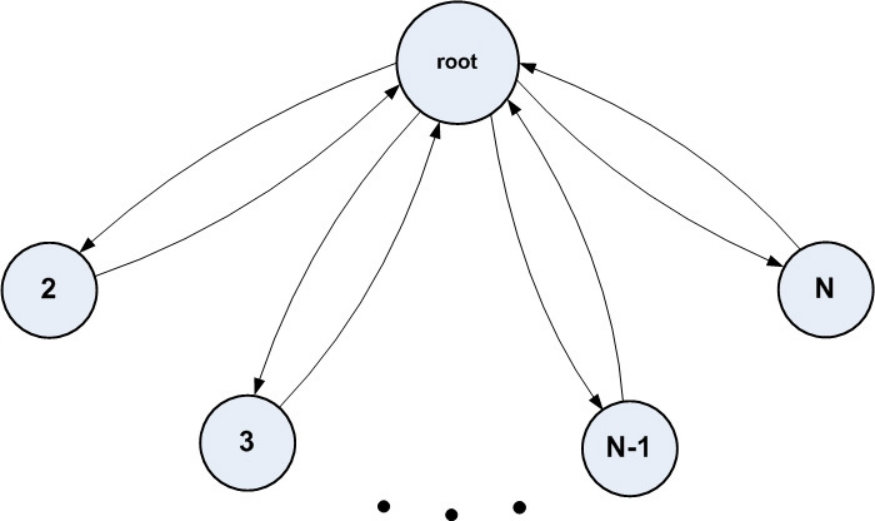

- 4.5 Graph Representation of the Network Communication of the Set-up Algorithm. (a) Communication Directed Graph for the Case . (b) Communication Directed Graph for the Case .

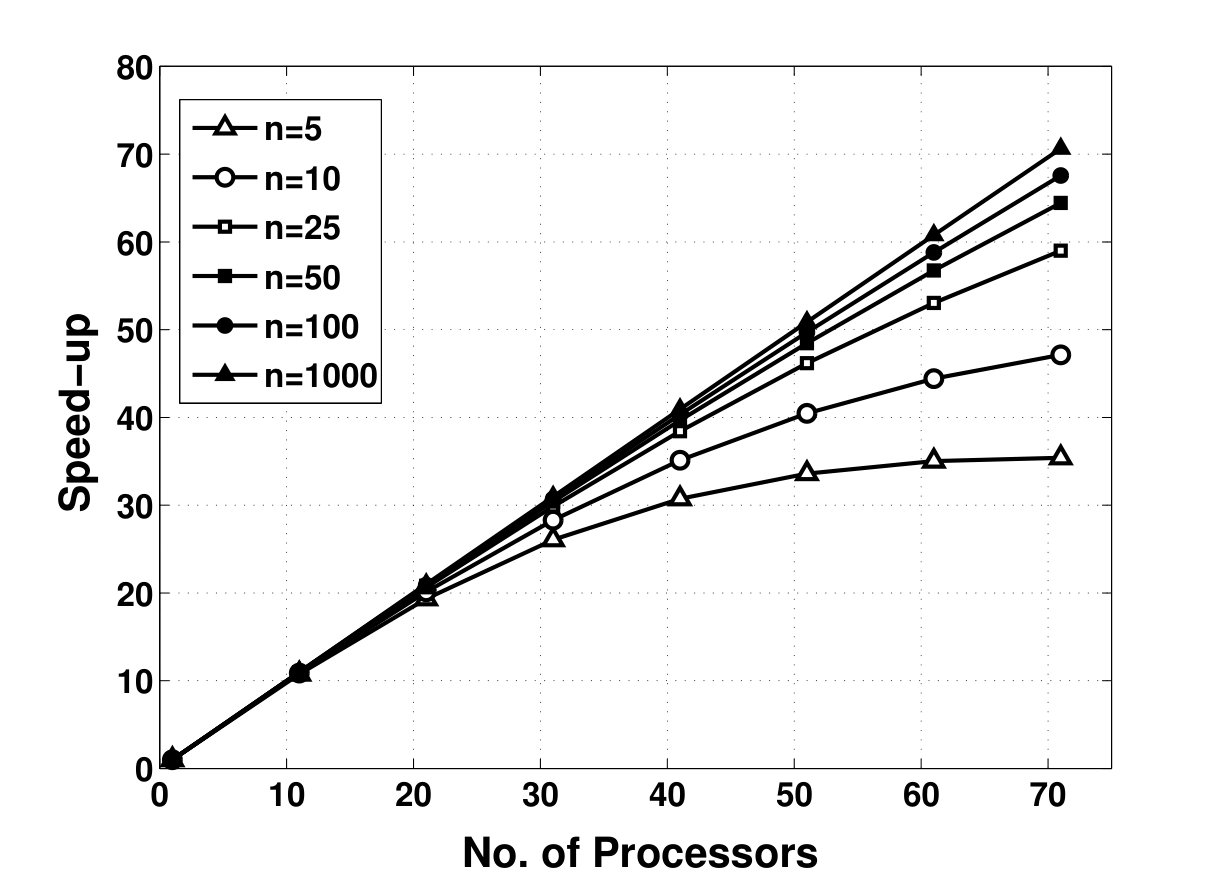

- 4.6 Theoretical Speed-up vs. No. of Processors for Different System Dimensions for , , and , Where

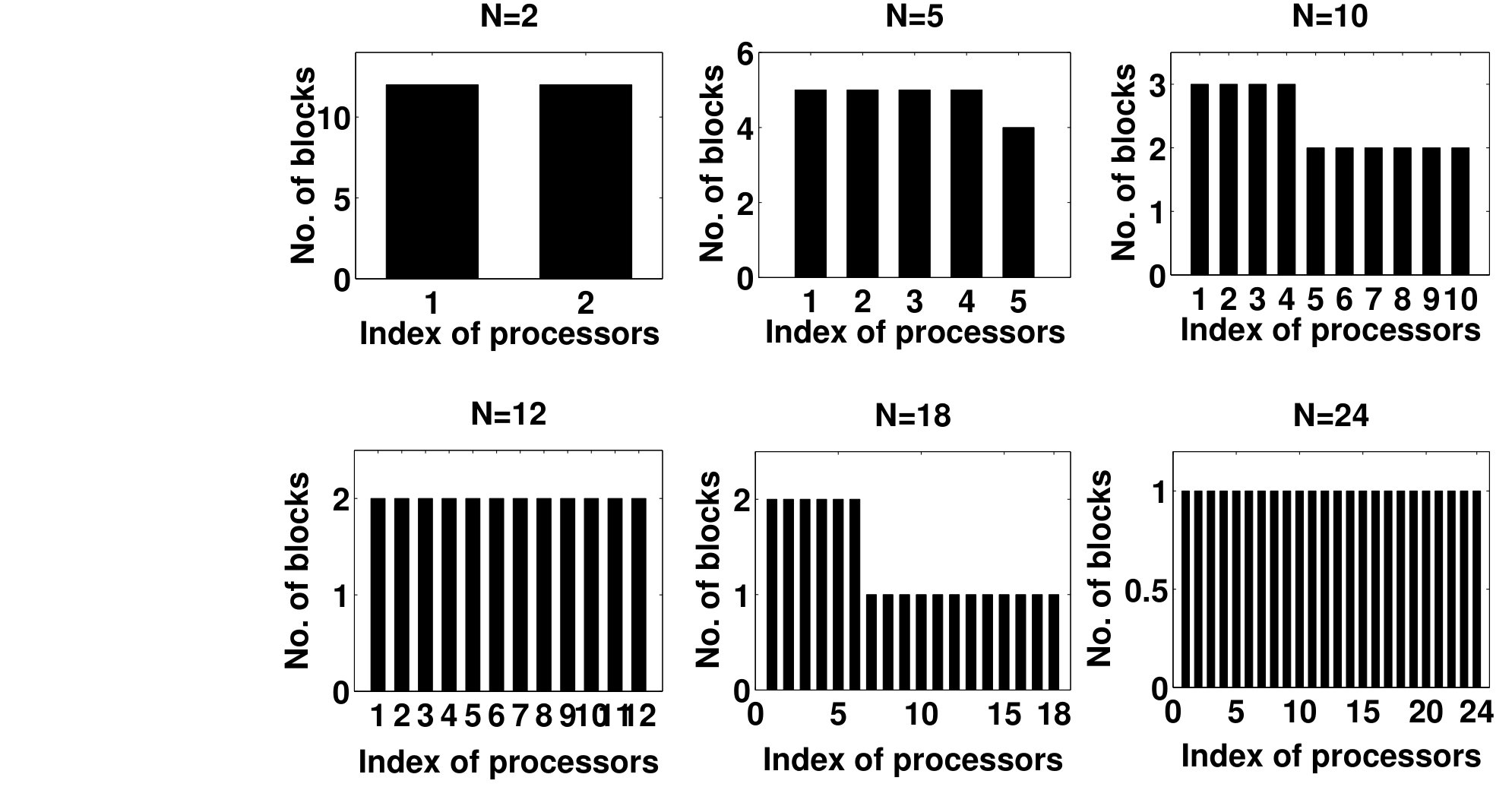

- 4.7 The Number of Blocks of the SDP Elements Assigned to Each Processor. An Illustration of Load Balancing.

- 4.8 The Communication Graph of the SDP Algorithm

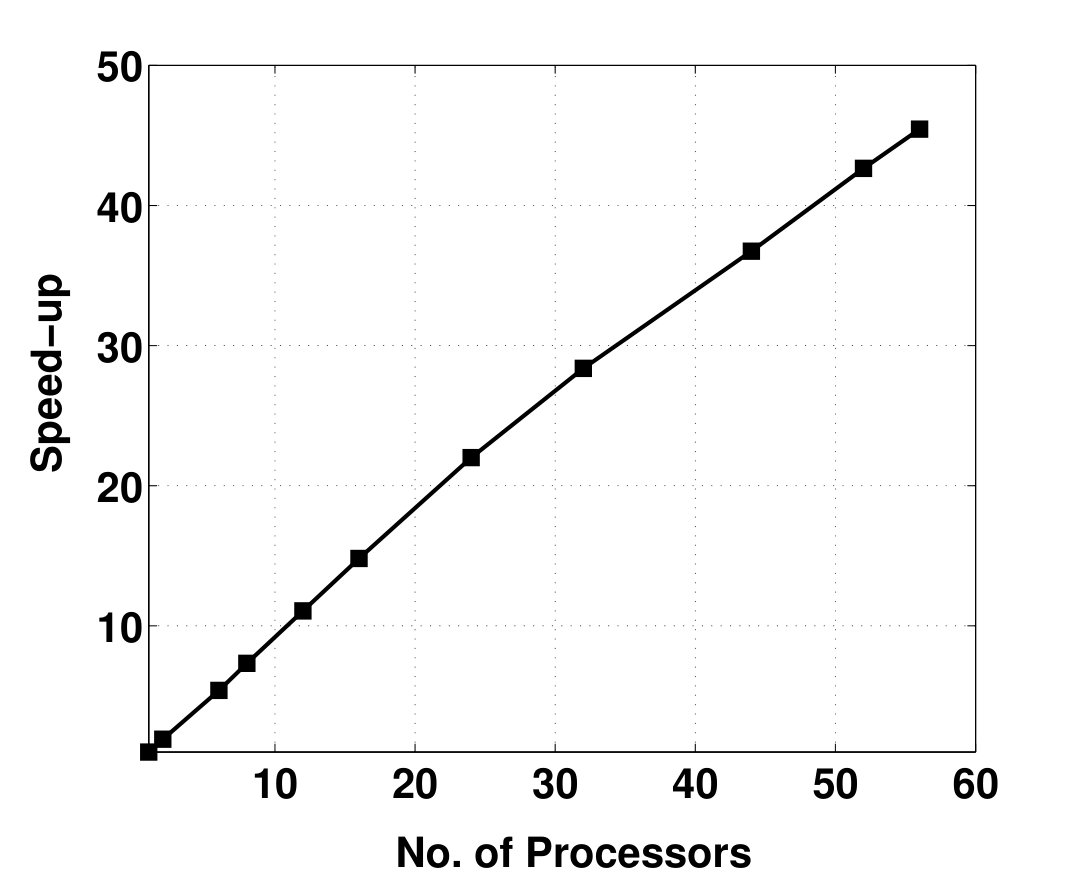

- 4.9 Speed-up of Set-up and SDP Algorithms vs. Number of Processors for a Discretized Model of Magnetic Flux in Tokamak

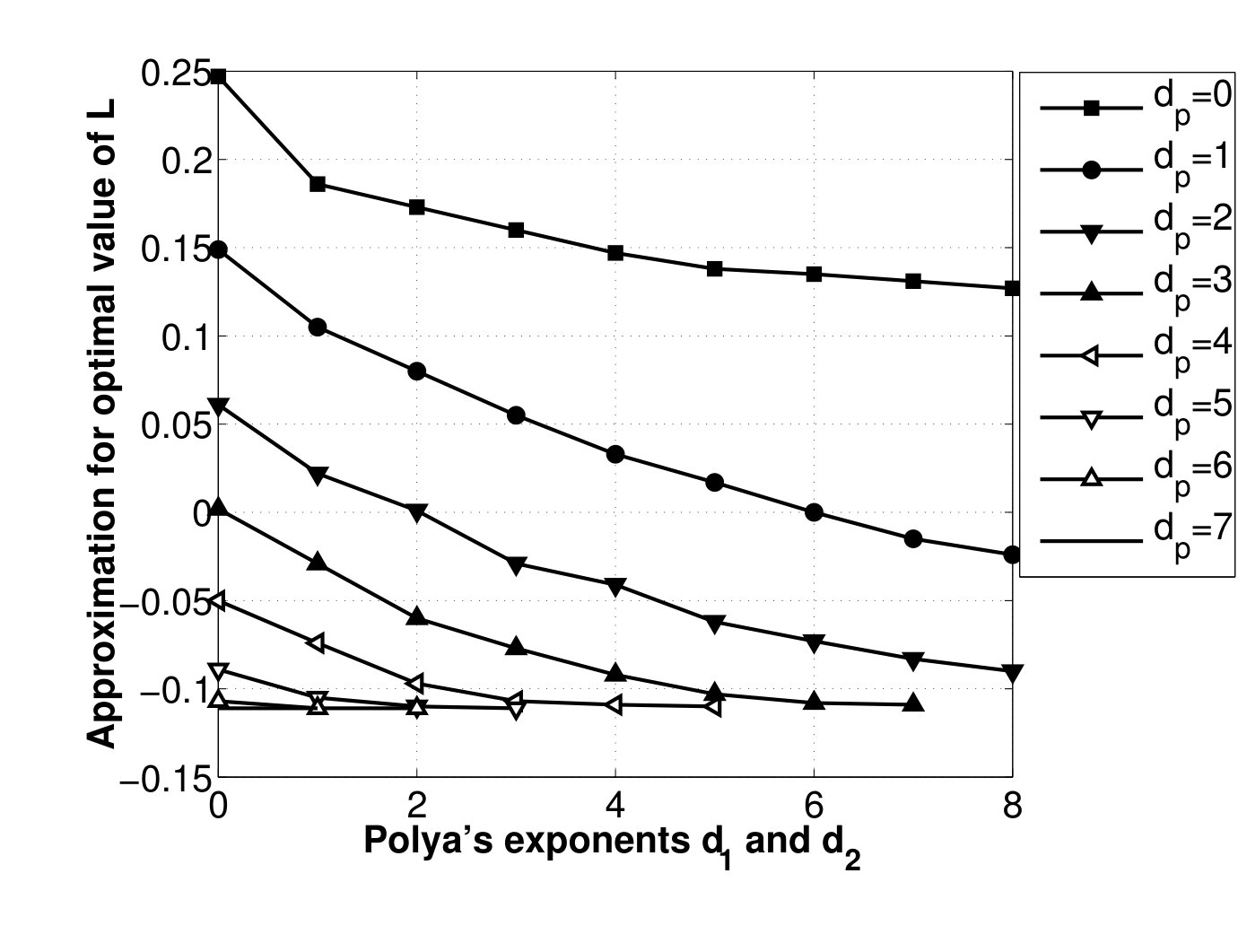

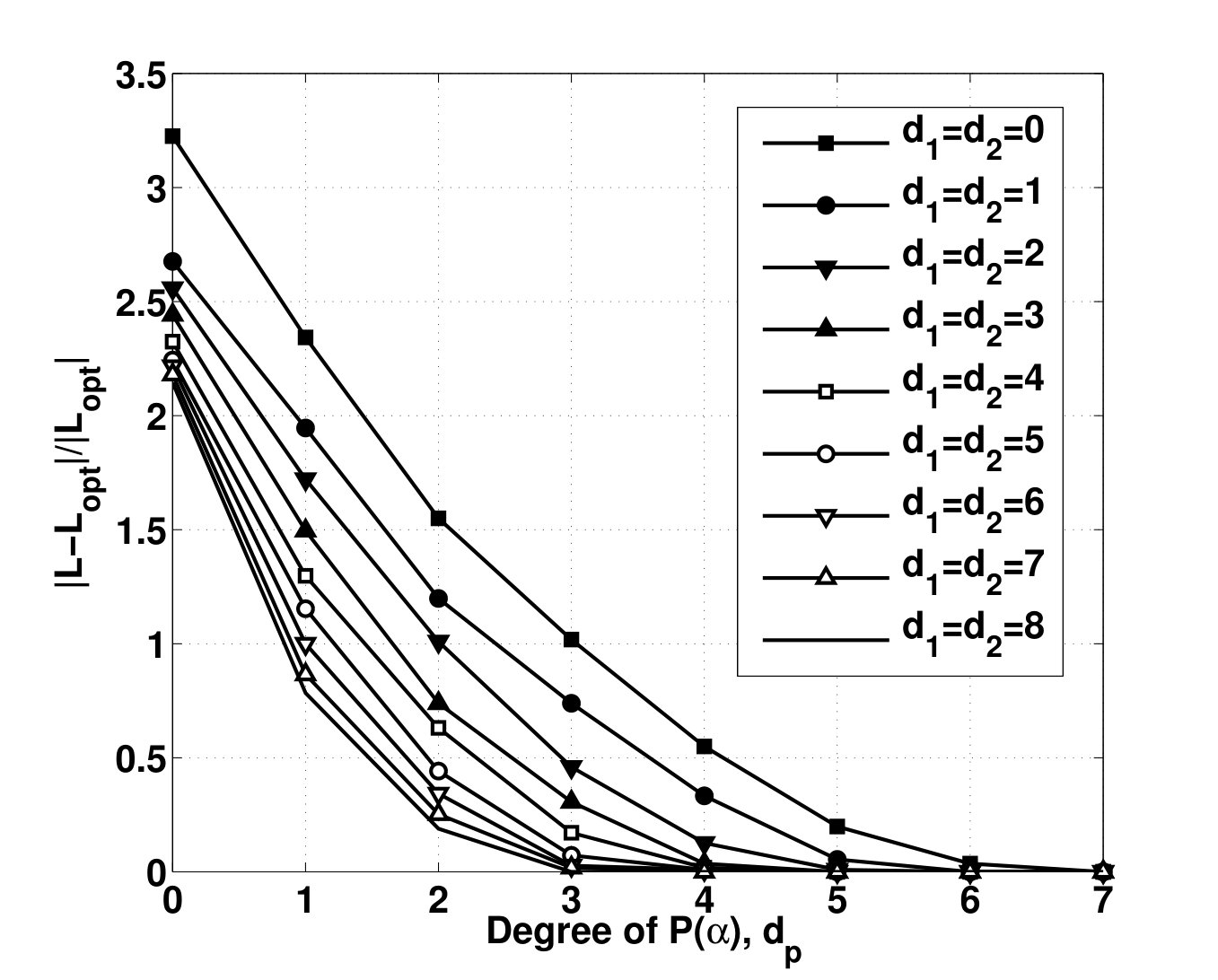

- 4.10 Upper Bound on Optimal vs. Polya’s Exponents and , for Different Degrees of . ().

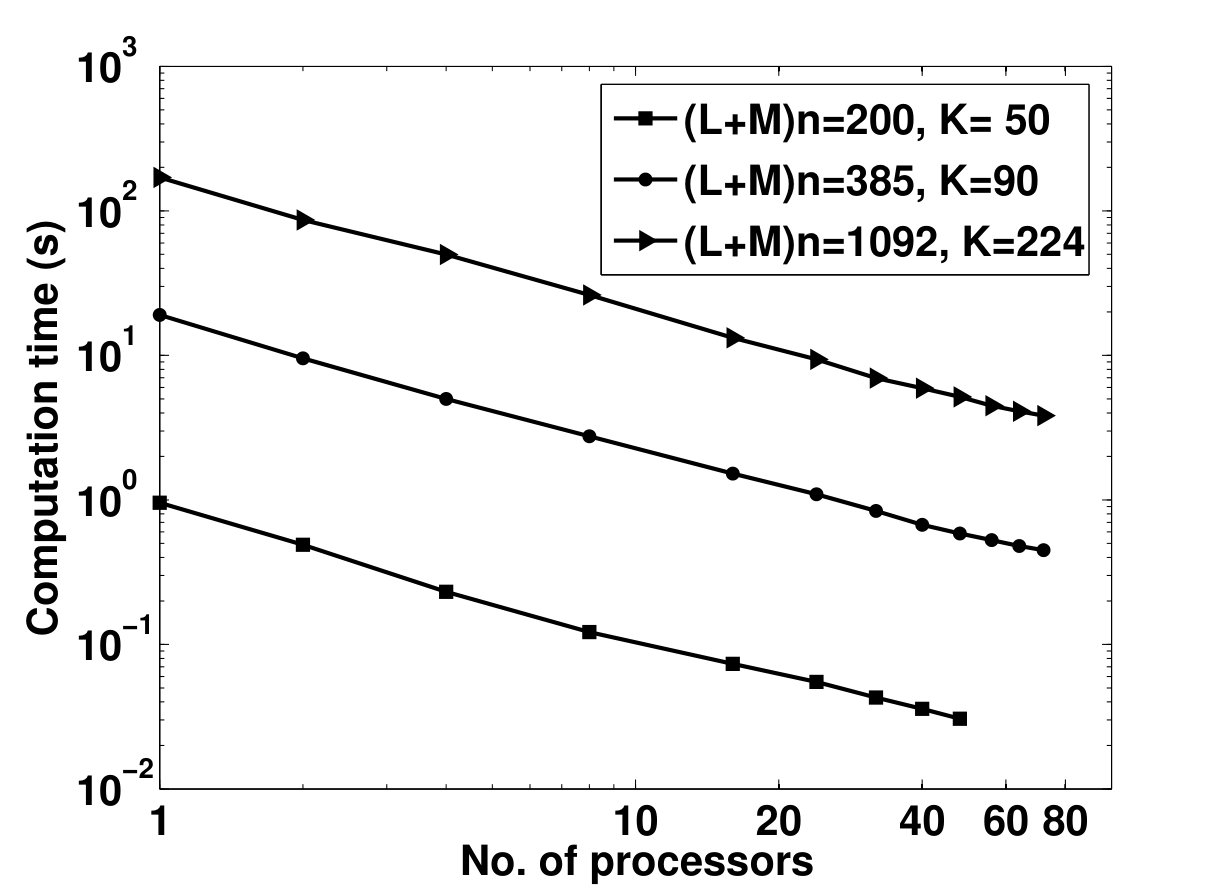

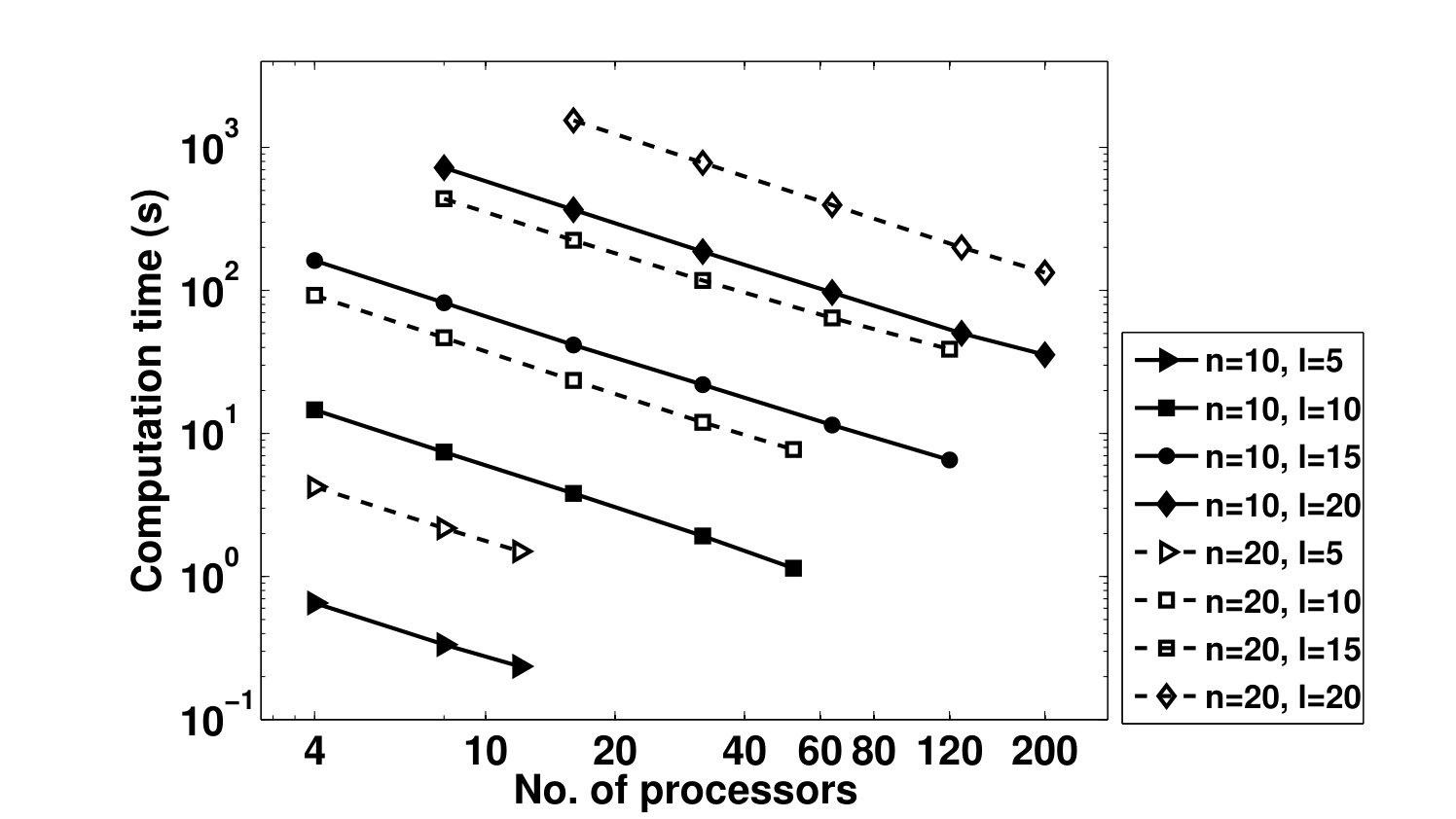

- 4.12 Computation Time of the Parallel Set-up Algorithm vs. Number of Processors for Different Dimensions of Linear System and Numbers of Uncertain Parameters - Executed on Blue Gene Supercomputer of Argonne National Labratory

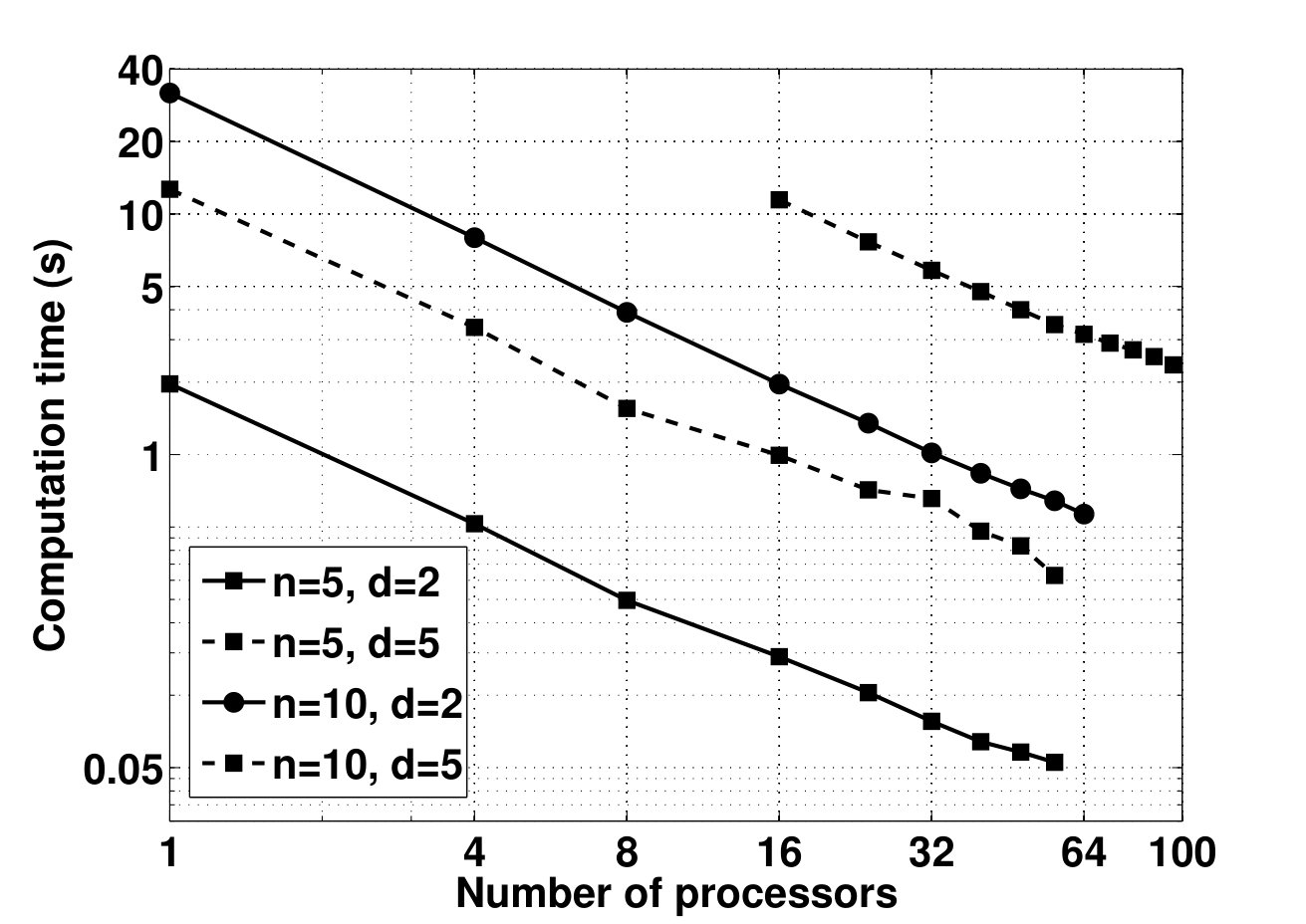

- 4.13 Computation Time of the Parallel SDP Algorithm vs. Number of Processors for Different Dimensions of Primal Variable and of Dual Variable - Executed on Karlin Cluster Computer

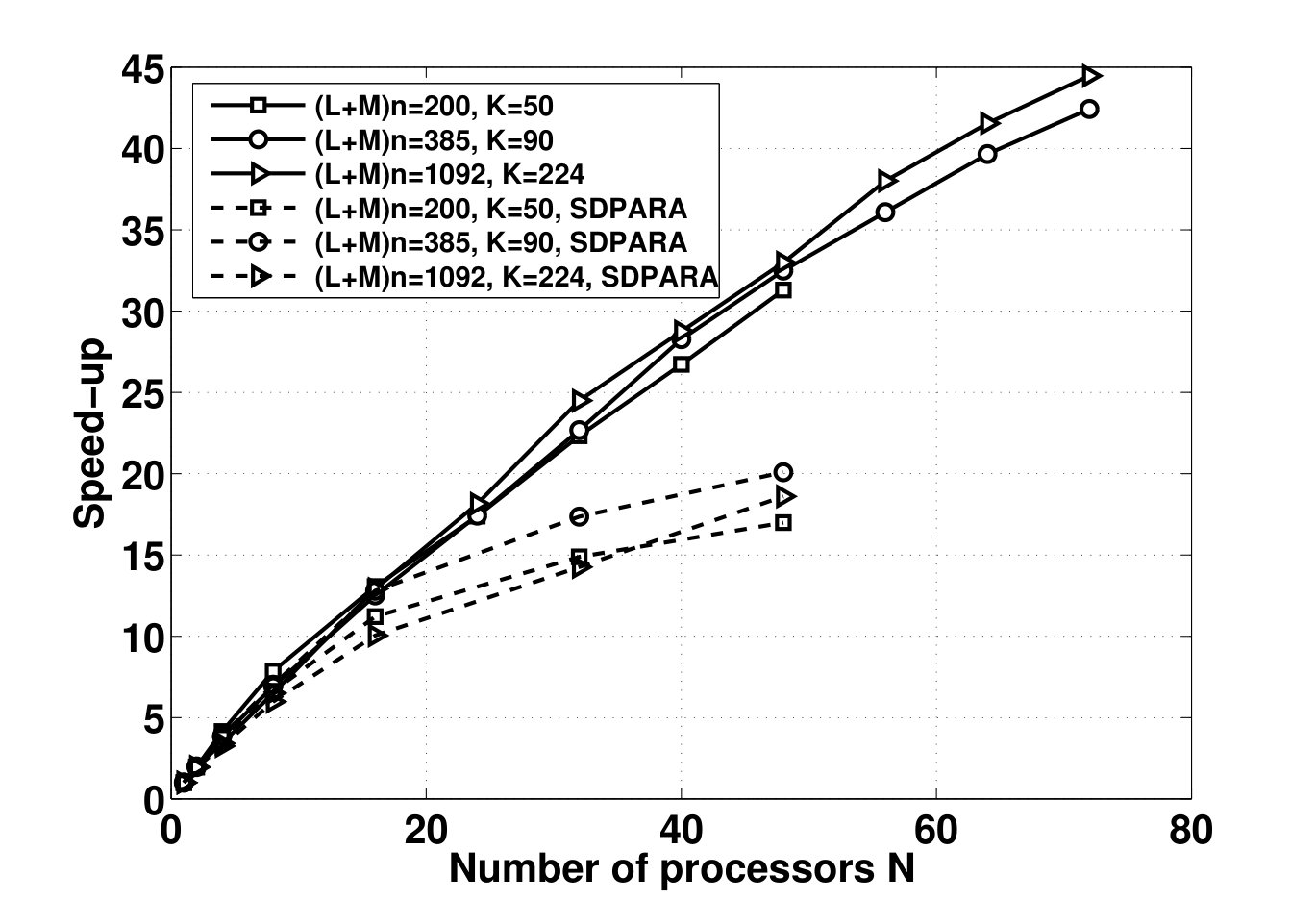

- 4.14 Comparison Between the Speed-up of the Present SDP Solver and SDPARA 7.3.1, Executed on Karlin Cluster Computer

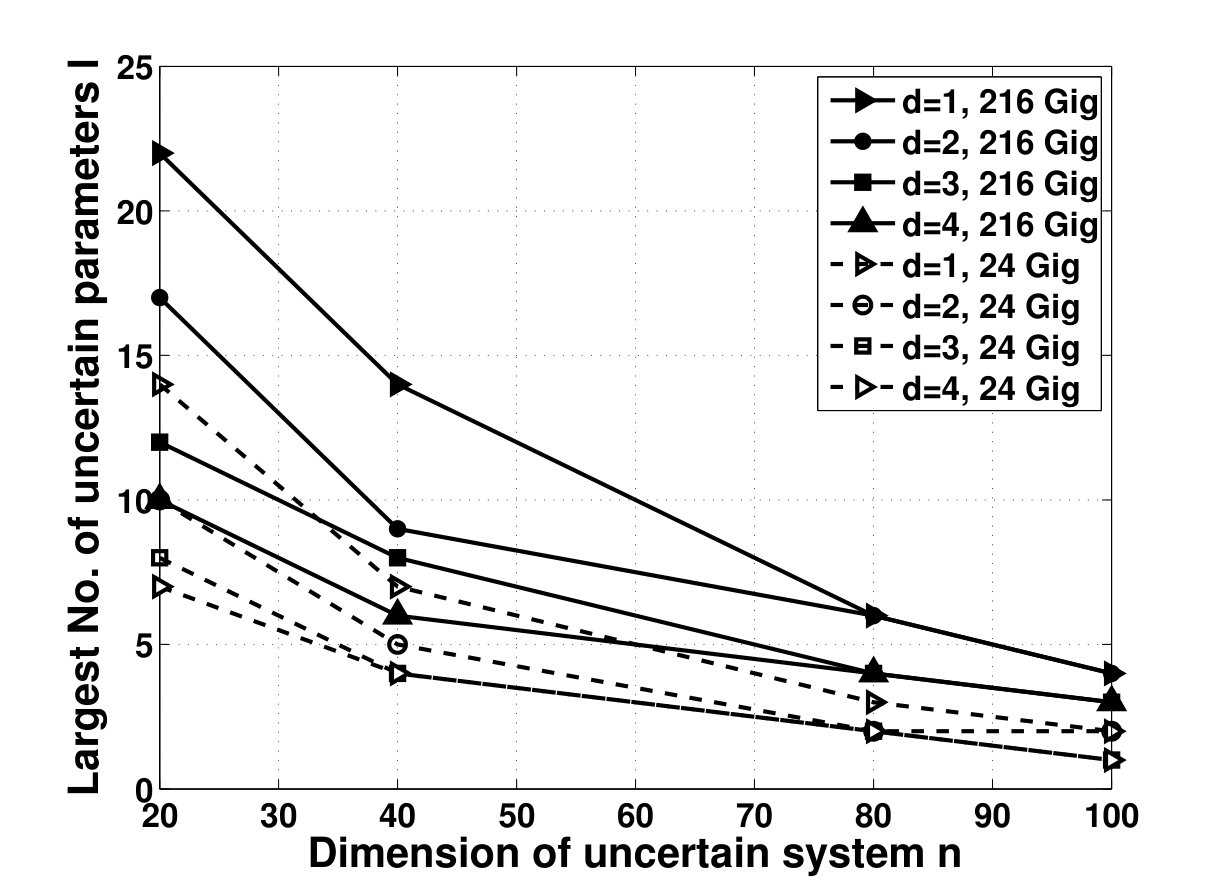

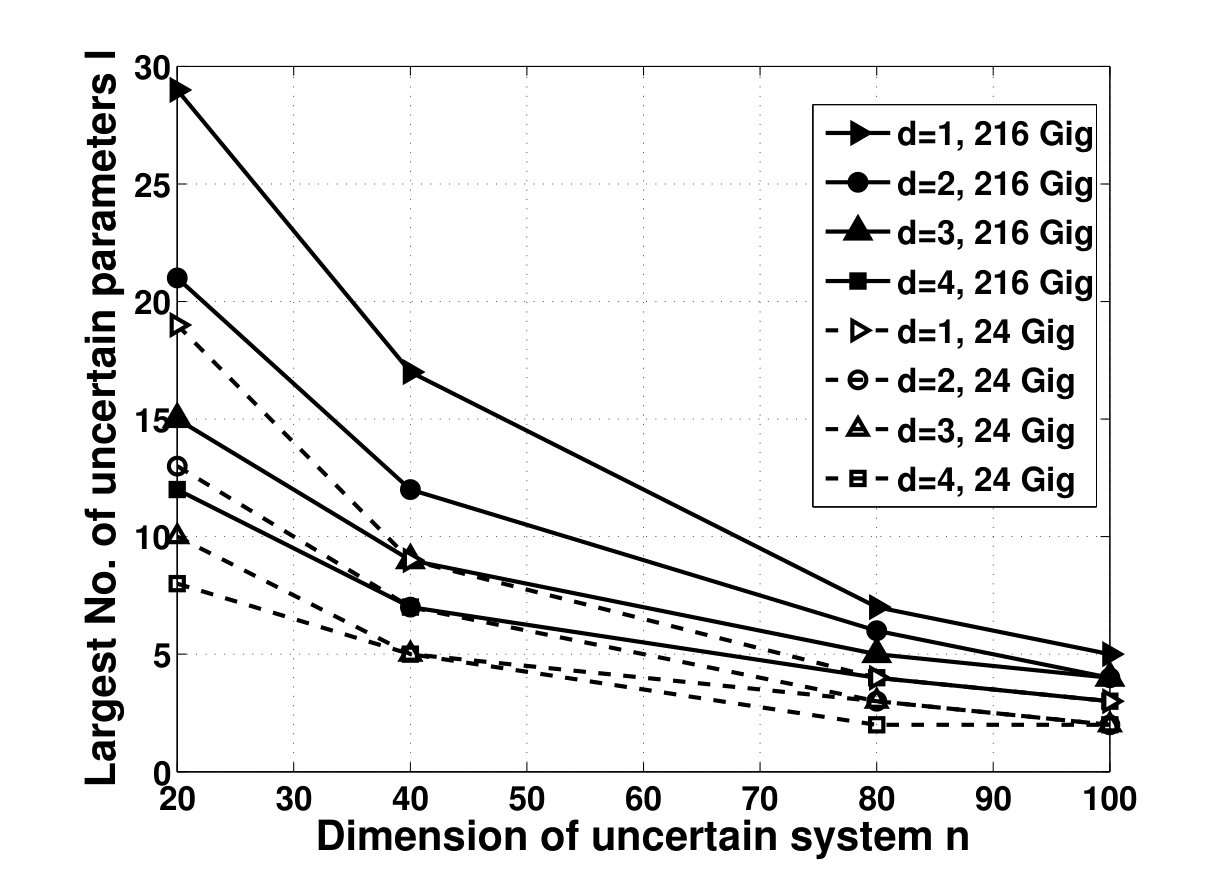

- 4.15 Largest Number of Uncertain Parameters of -Dimensional Systems for Which the Set-up Algorithm (Left) and SDP Solver (Right) Can Solve the Robust Stability Problem of the System Using 24 and 216 GB of RAM

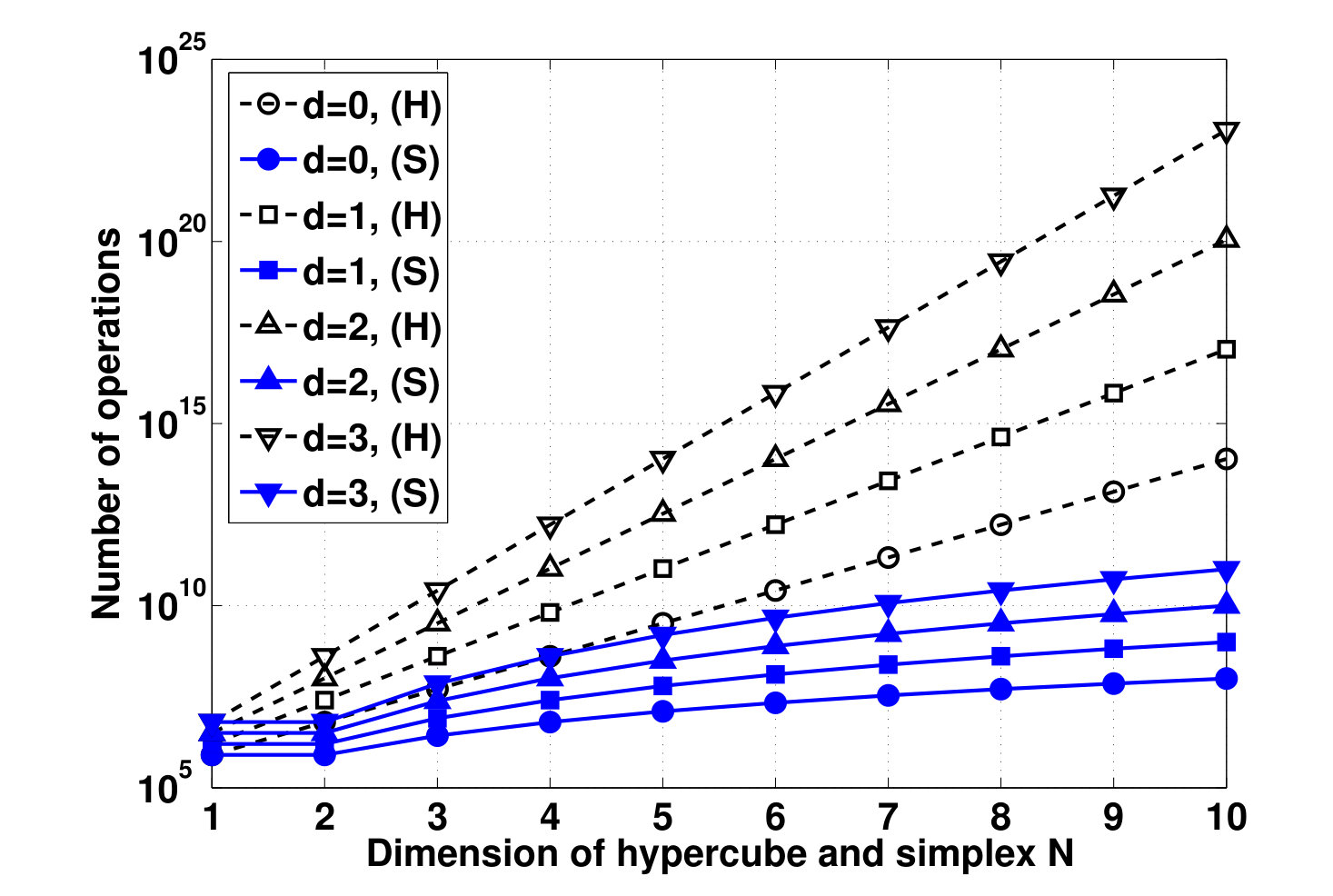

- 5.1 Number of Operations vs. Dimension of the Hypercube, for Different Polya’s Exponents . (H): Hypercube and (S): Simplex.

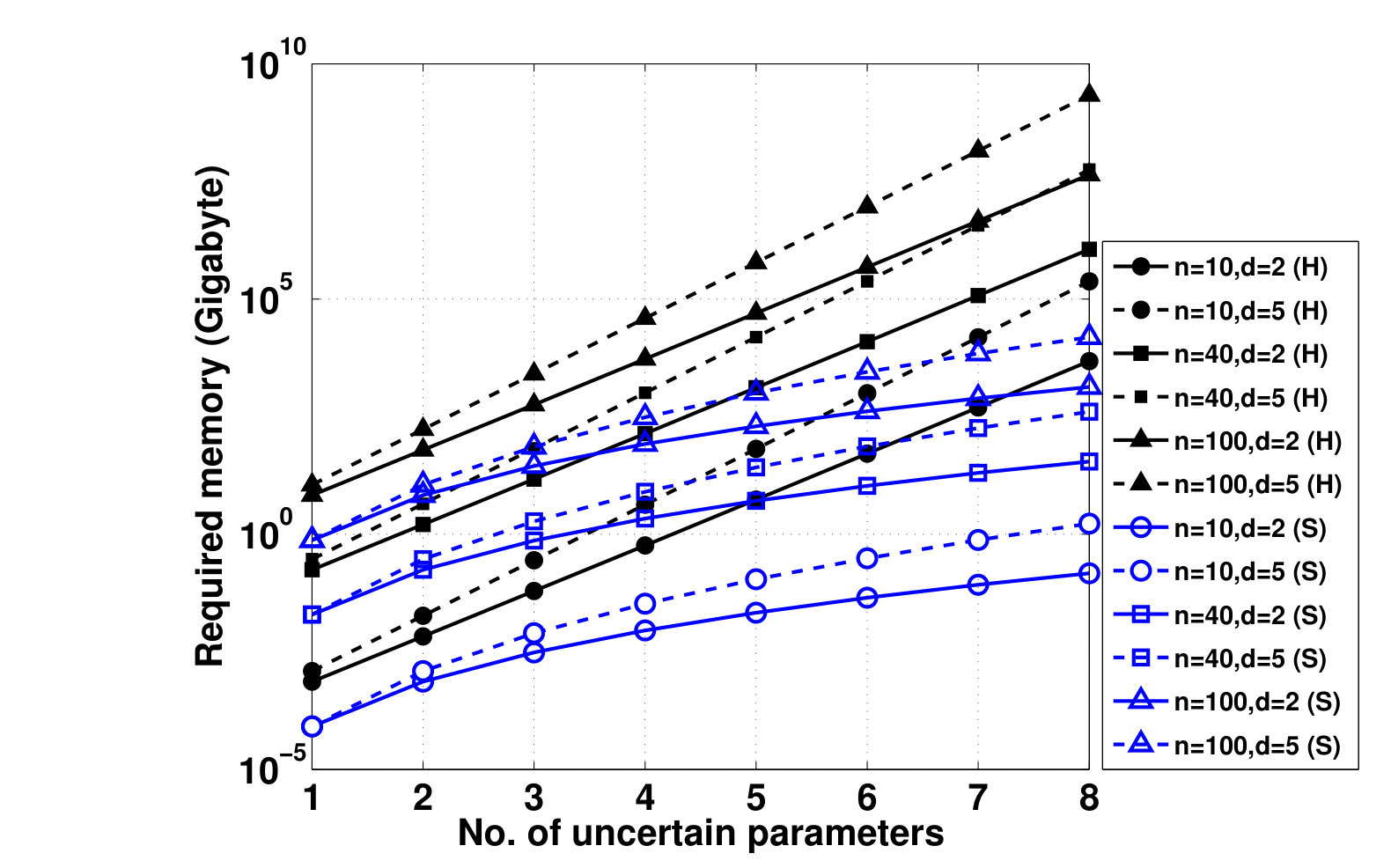

- 5.2 Required Memory for the Calculation of SDP Elements vs. Number of Uncertain Parameters in Hypercube and Simplex, for Different State-space Dimensions and Polya’s Exponents . (H): Hypercube, (S): Simplex.

- 5.3 Execution Time of the Set-up Algorithm vs. Number of Processors, for Different State-space Dimensions and Polya’s Exponents

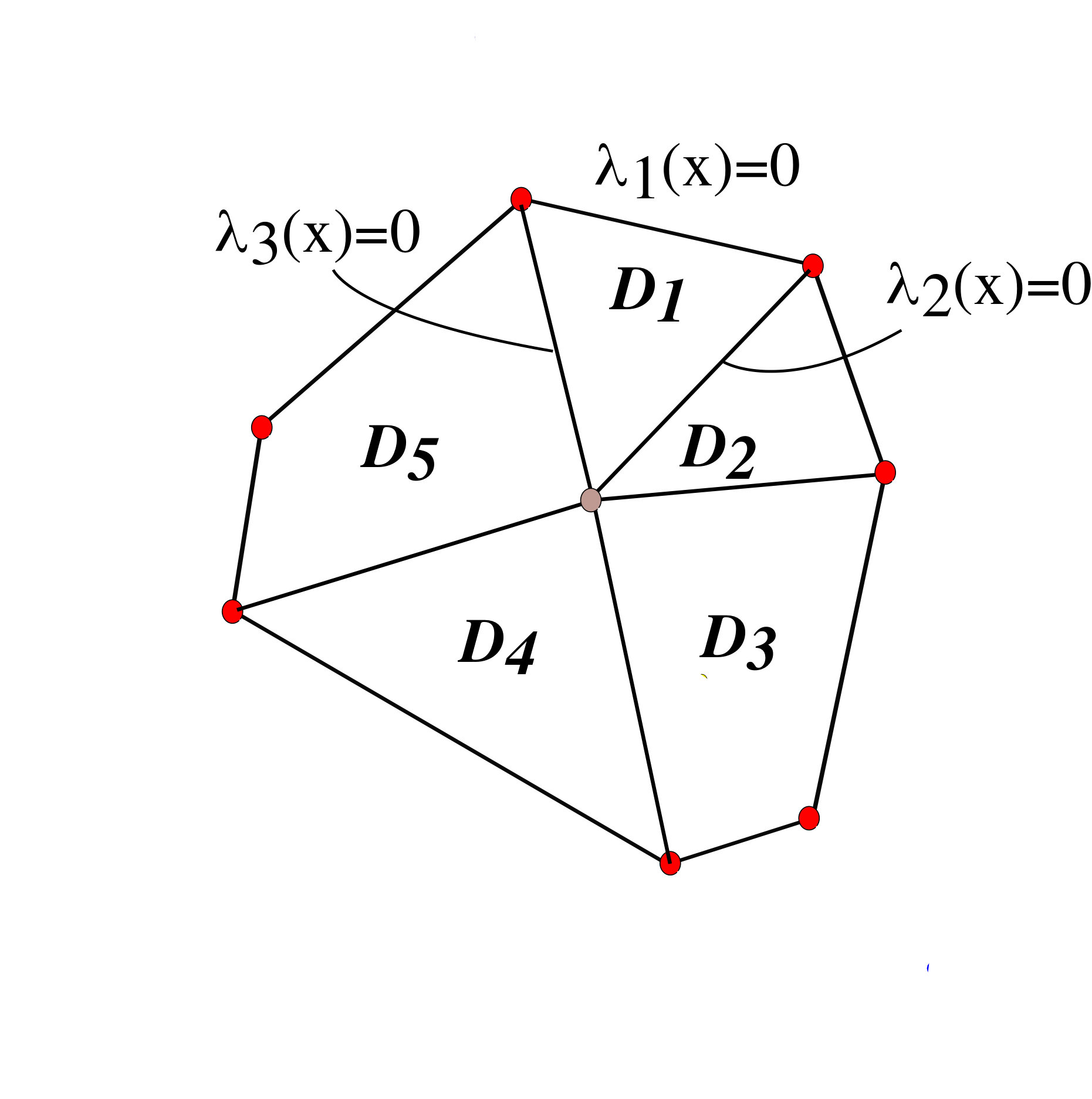

- 6.1 An Illustration of a D-decomposition of a 2D Polytope. for .

- 6.2 Decomposition of the Hypercube in , and Dimensions

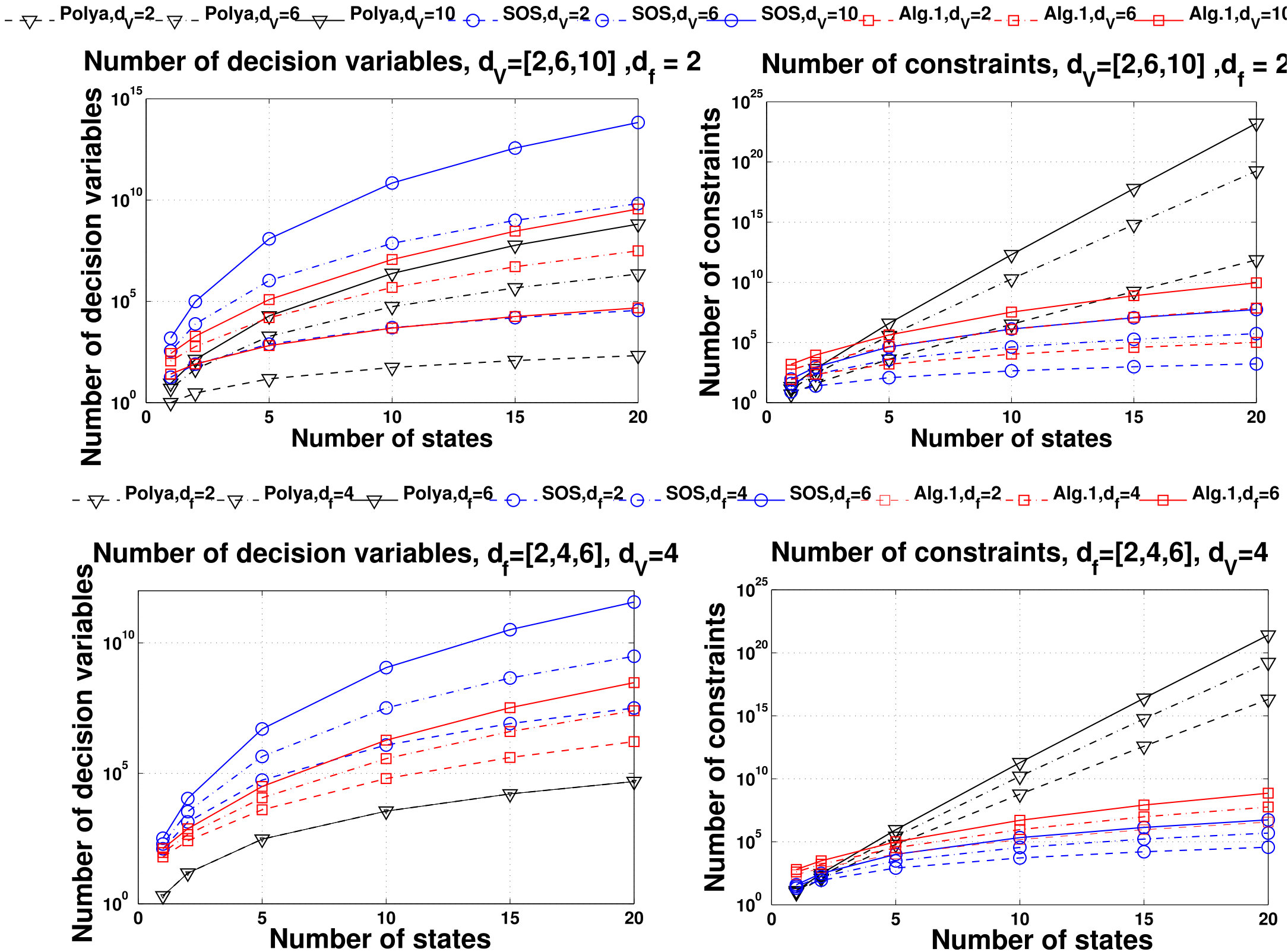

- 6.3 Number of Decision Variables and Constraints of the Optimization Problems Associated with Algorithm 1, Polya’s Algorithm and SOS Algorithm for Different Degrees of the Lyapunov Function and the Vector Field

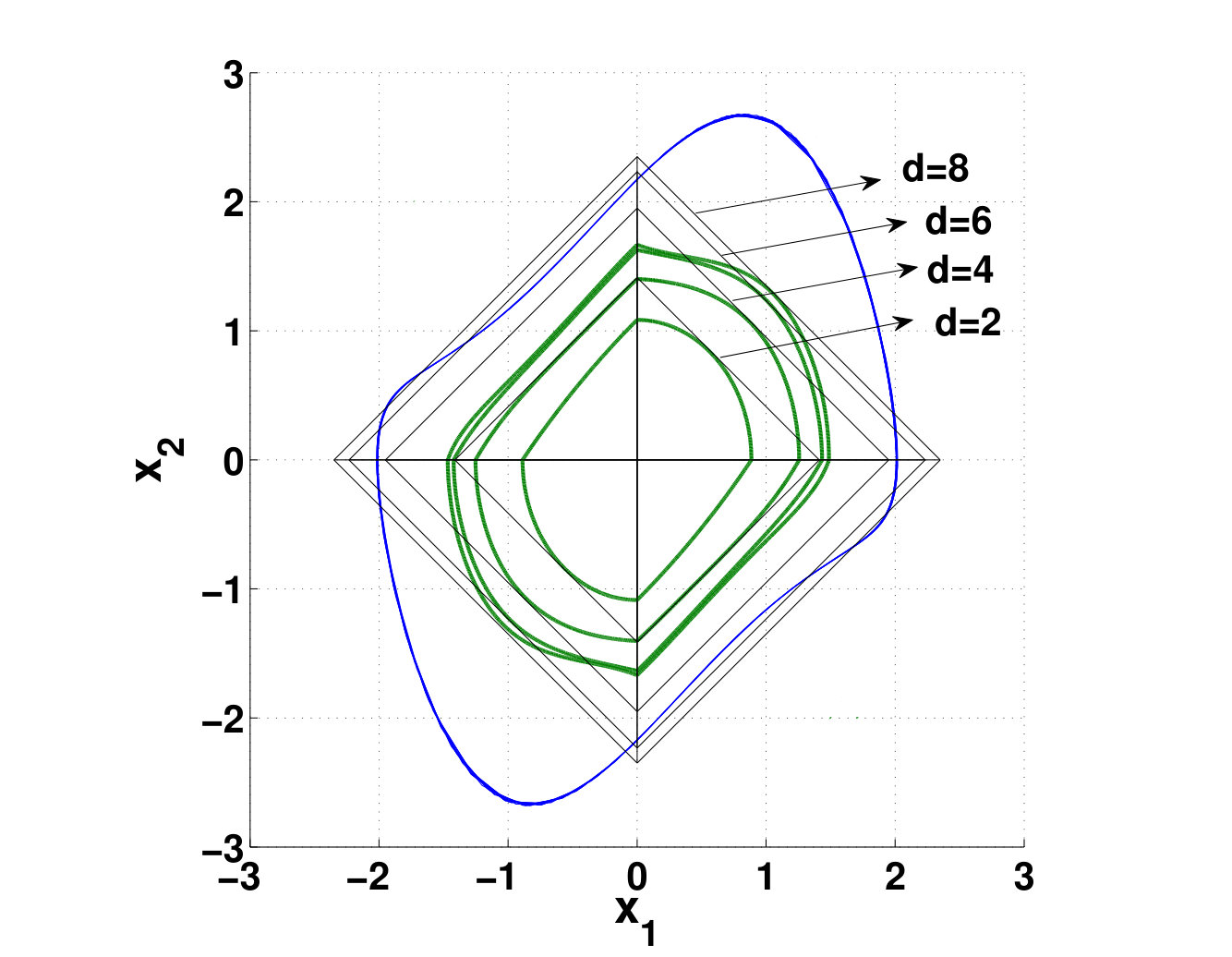

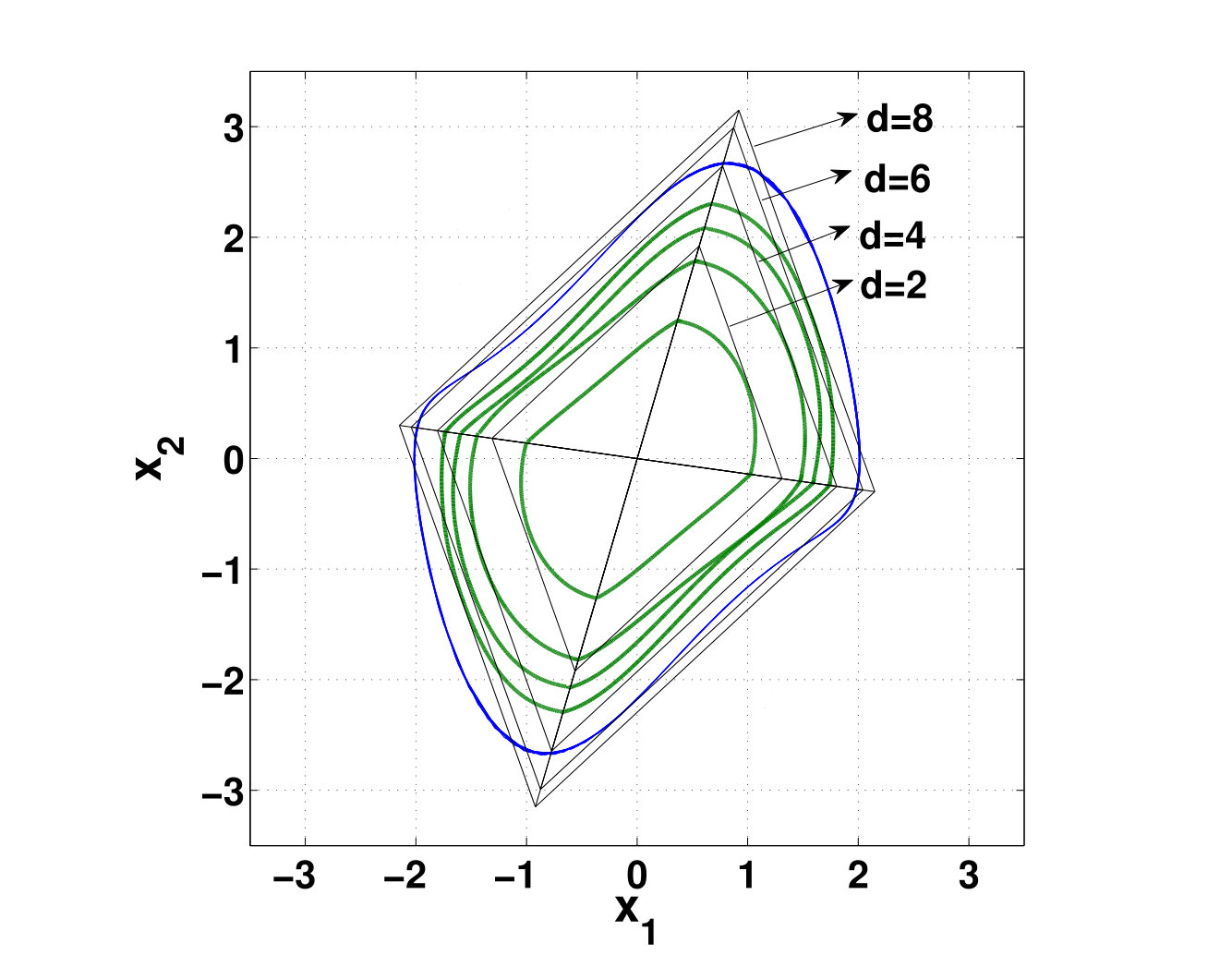

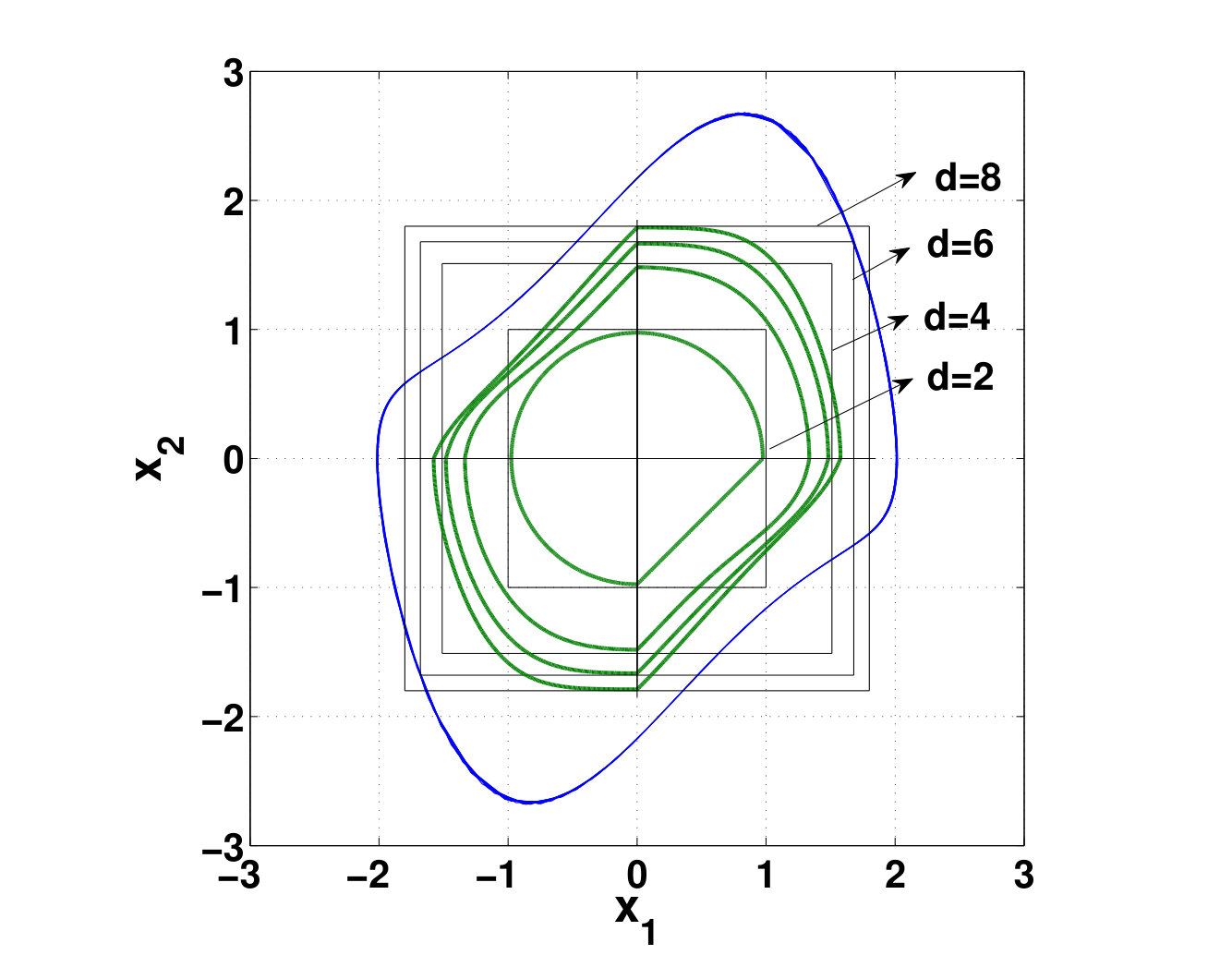

- 6.4 The Largest Level-set of Lyapunov Function (6.21) Inscribed in Polytope (6.20)

- 6.5 Largest Level-sets of Lyapunov Functions of Different Degrees and Their Associated Parallelograms

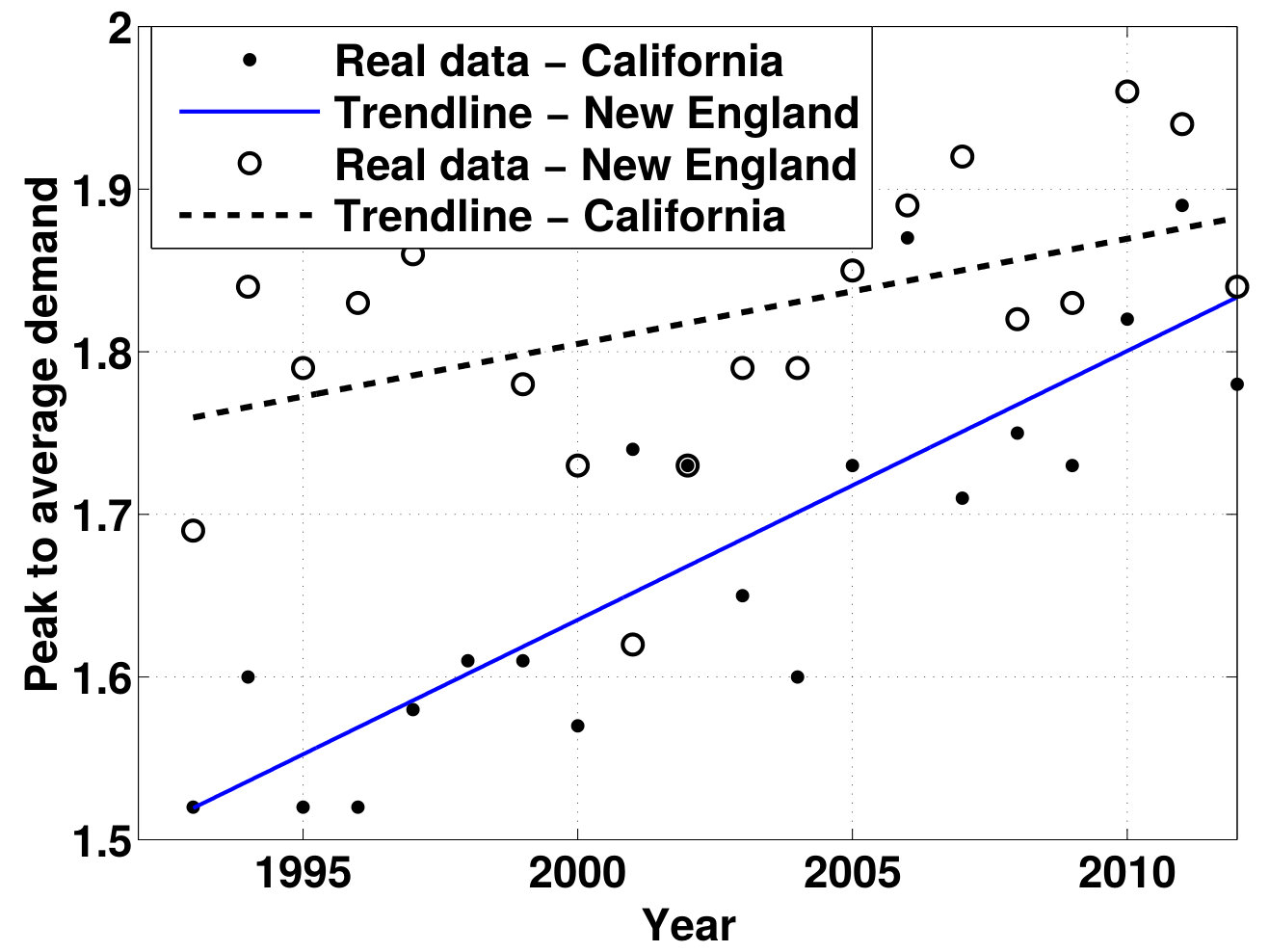

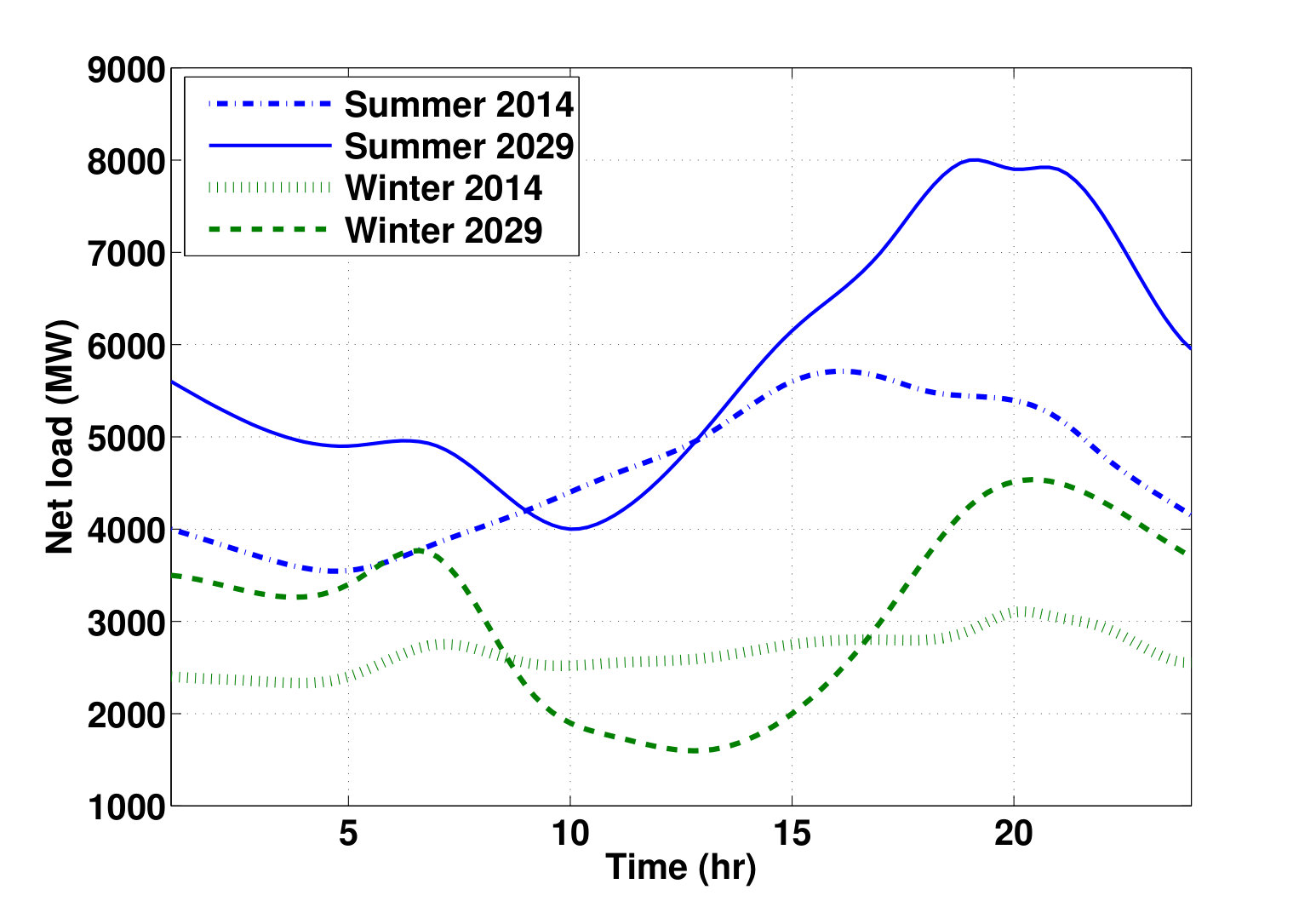

- 7.1 Effect of Solar Power on Demand: Net Loads for Typical Summer and Winter Days in Arizona in 2014 and for 2029 (Projected), from Arizona Public Service (2014)

- 7.2 Peak to Average Demand of Electricity and Its Trend-line in California and New England from 1993 to 2012, Data Adopted from Shear (2014)

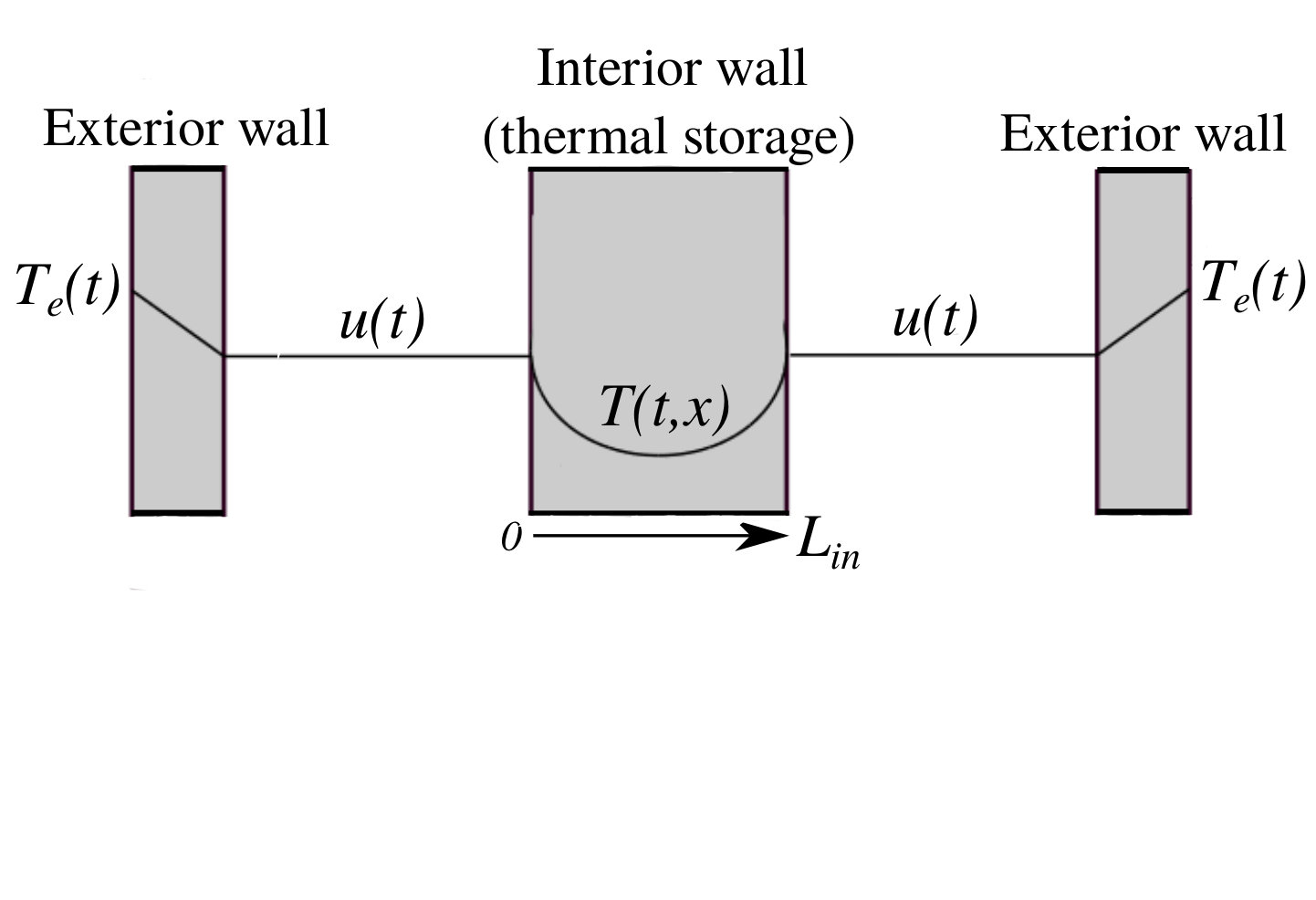

- 7.3 A Schematic View of Our Thermal Mass Model

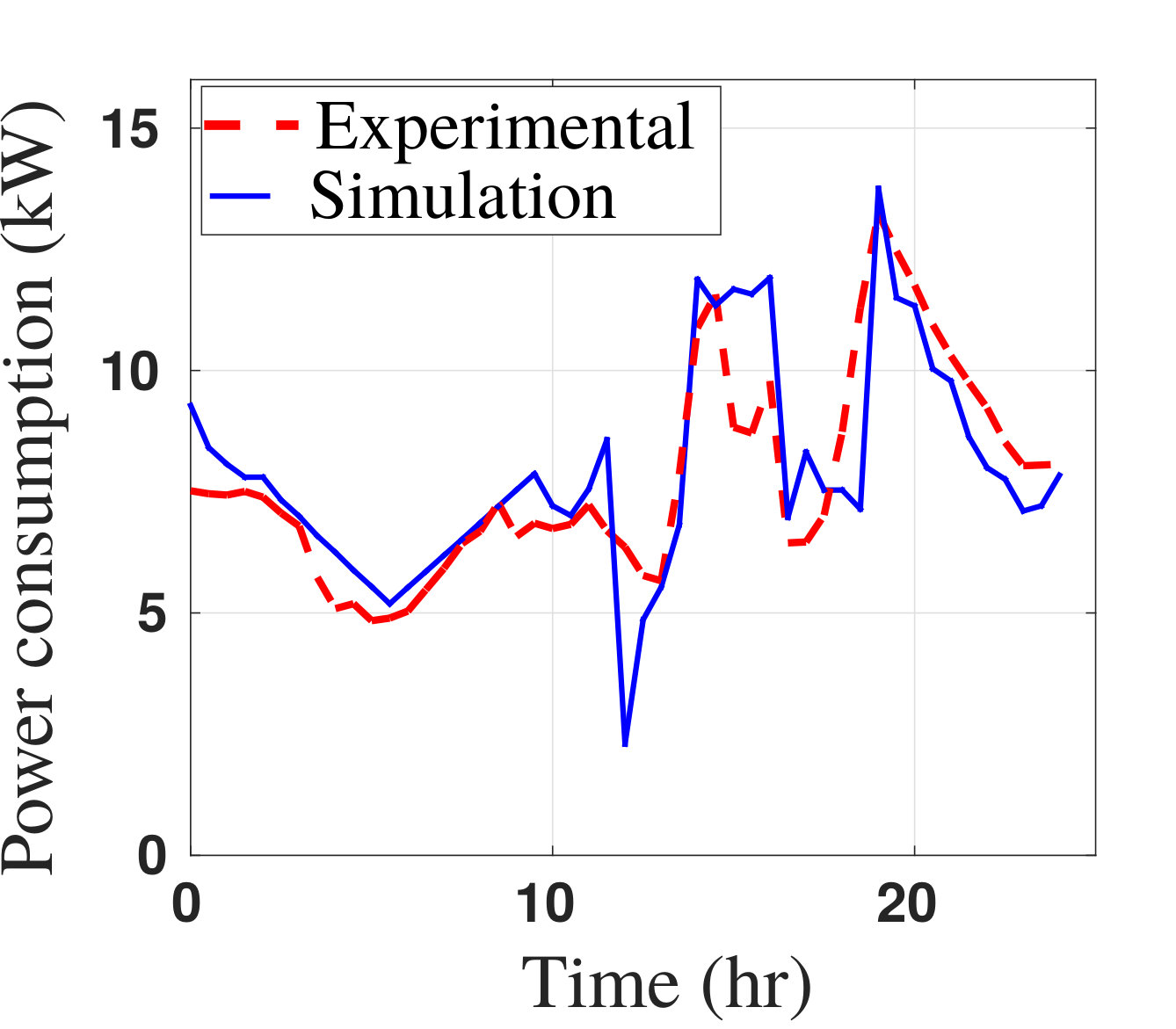

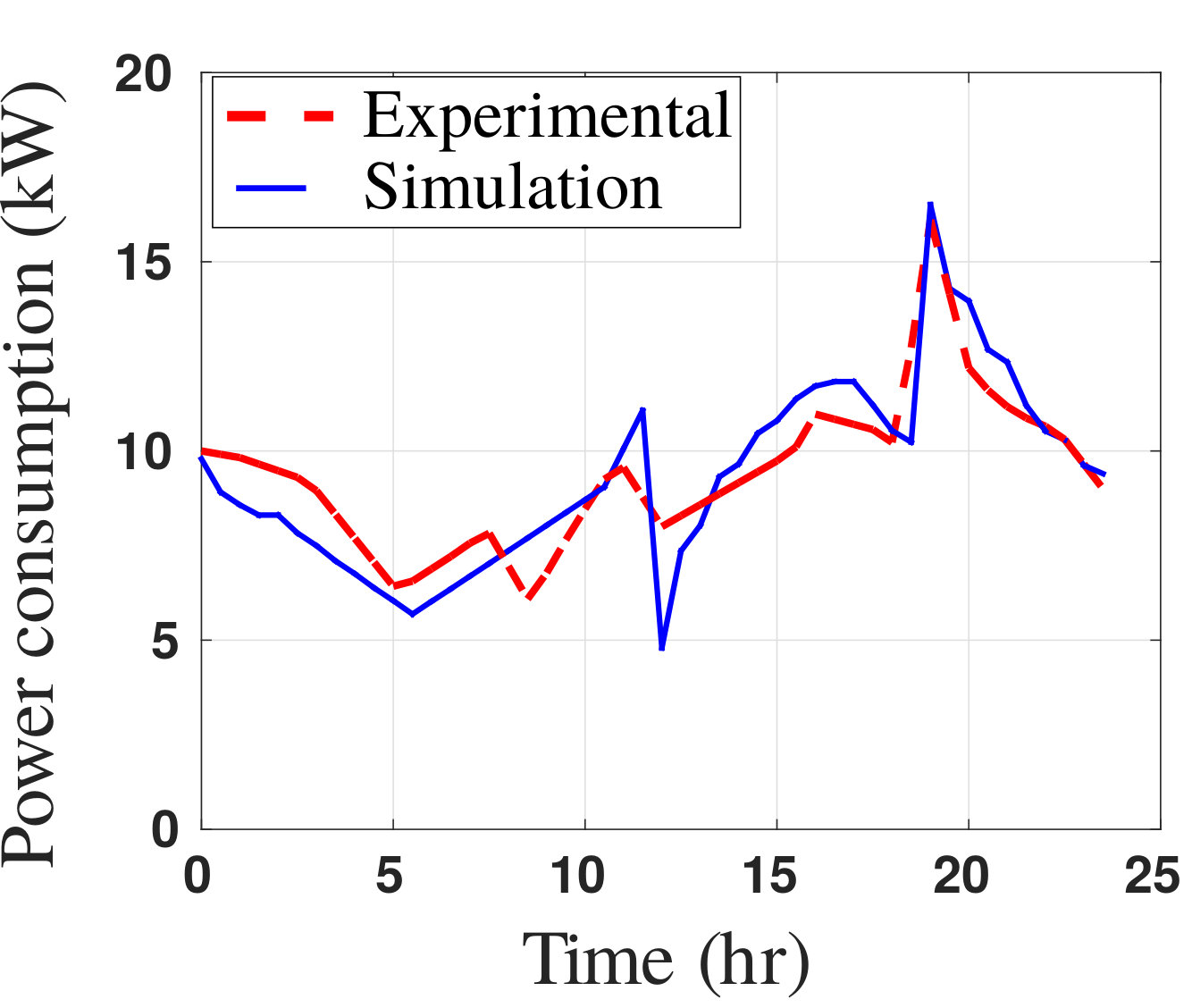

- 7.4 Simulated and Measured Power Consumptions

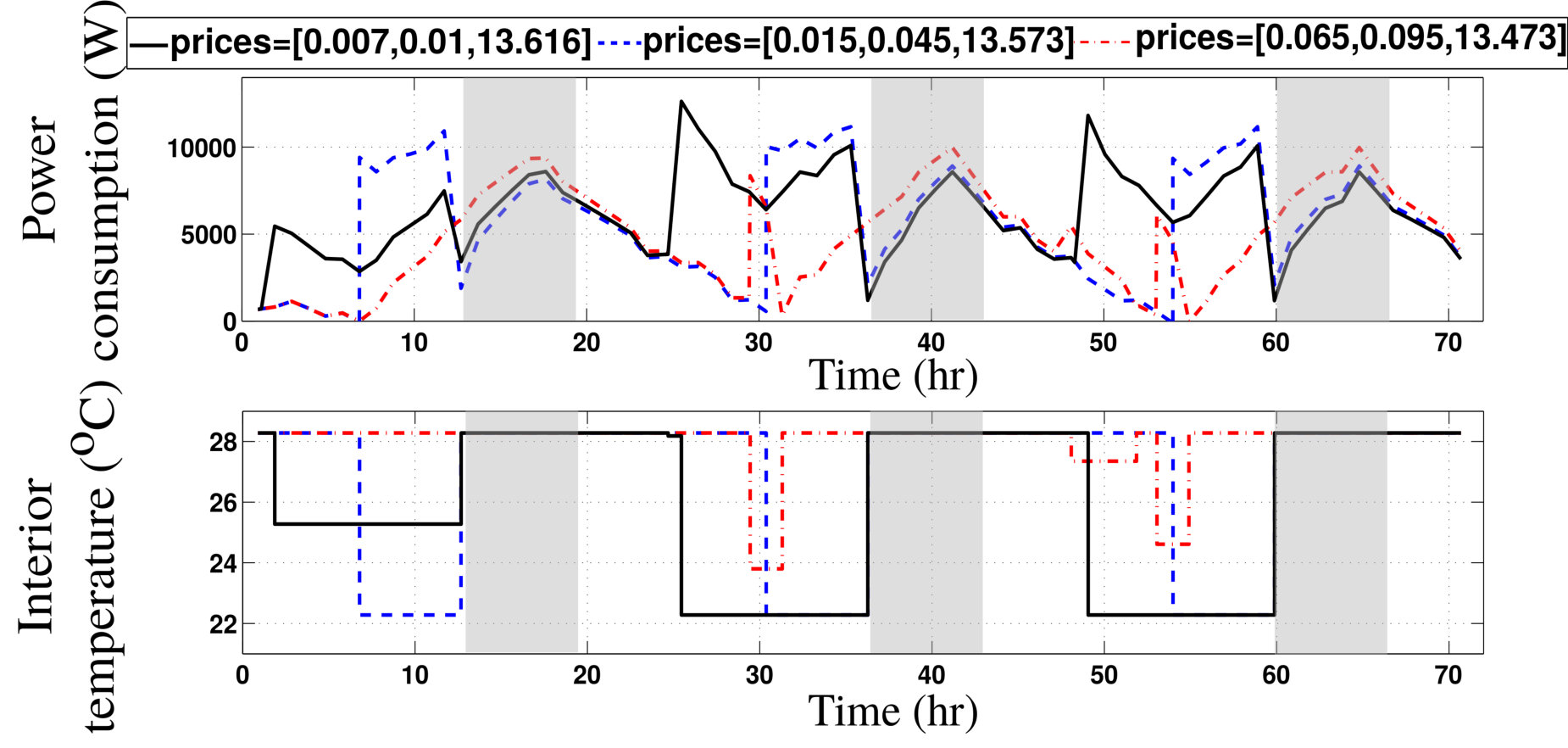

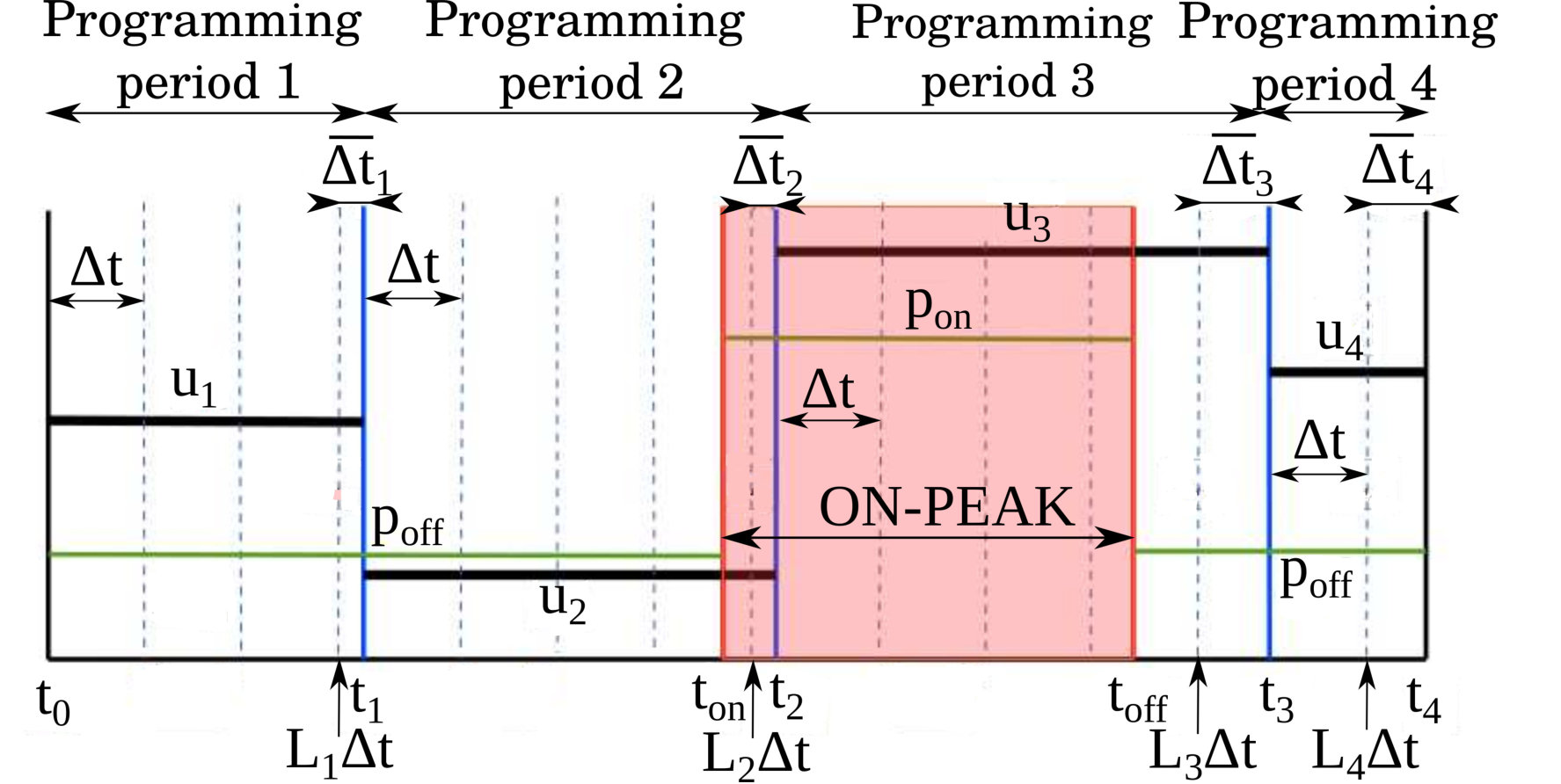

- 7.5 An Illustration for the Programming Periods of the 4-Setpoint Thermostat Problem, Switching Times , Pricing Function , and .

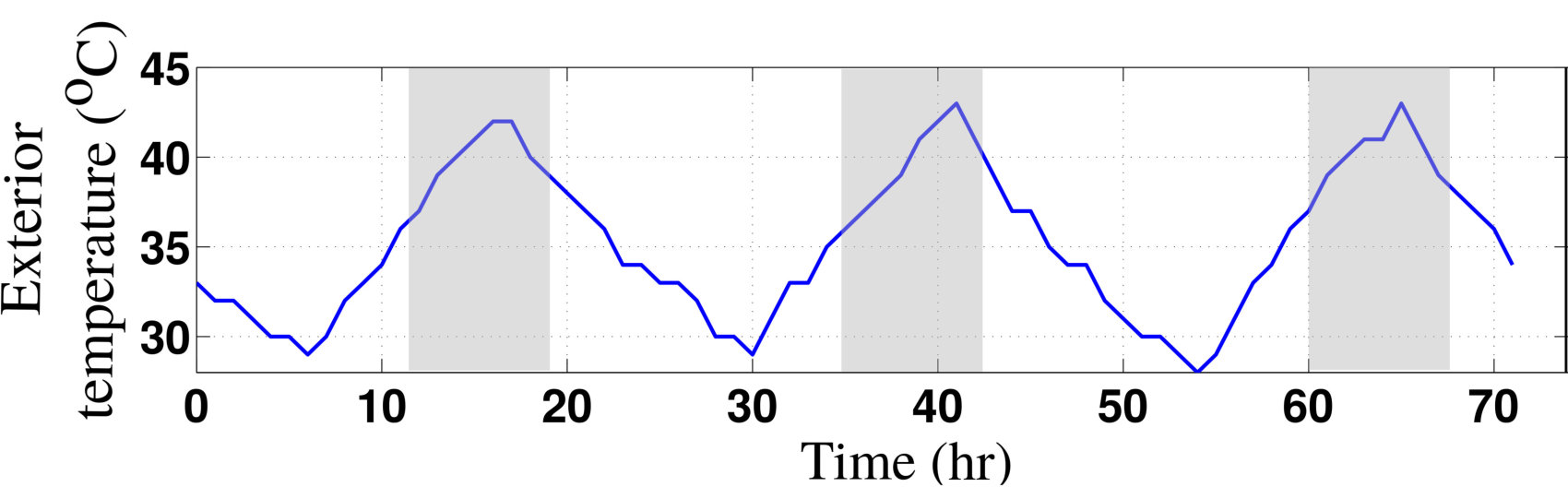

- 7.6 External Temperature of Three Typical Summer Days in Phoenix, Arizona. Shaded Areas Correspond to On-peak Hours.

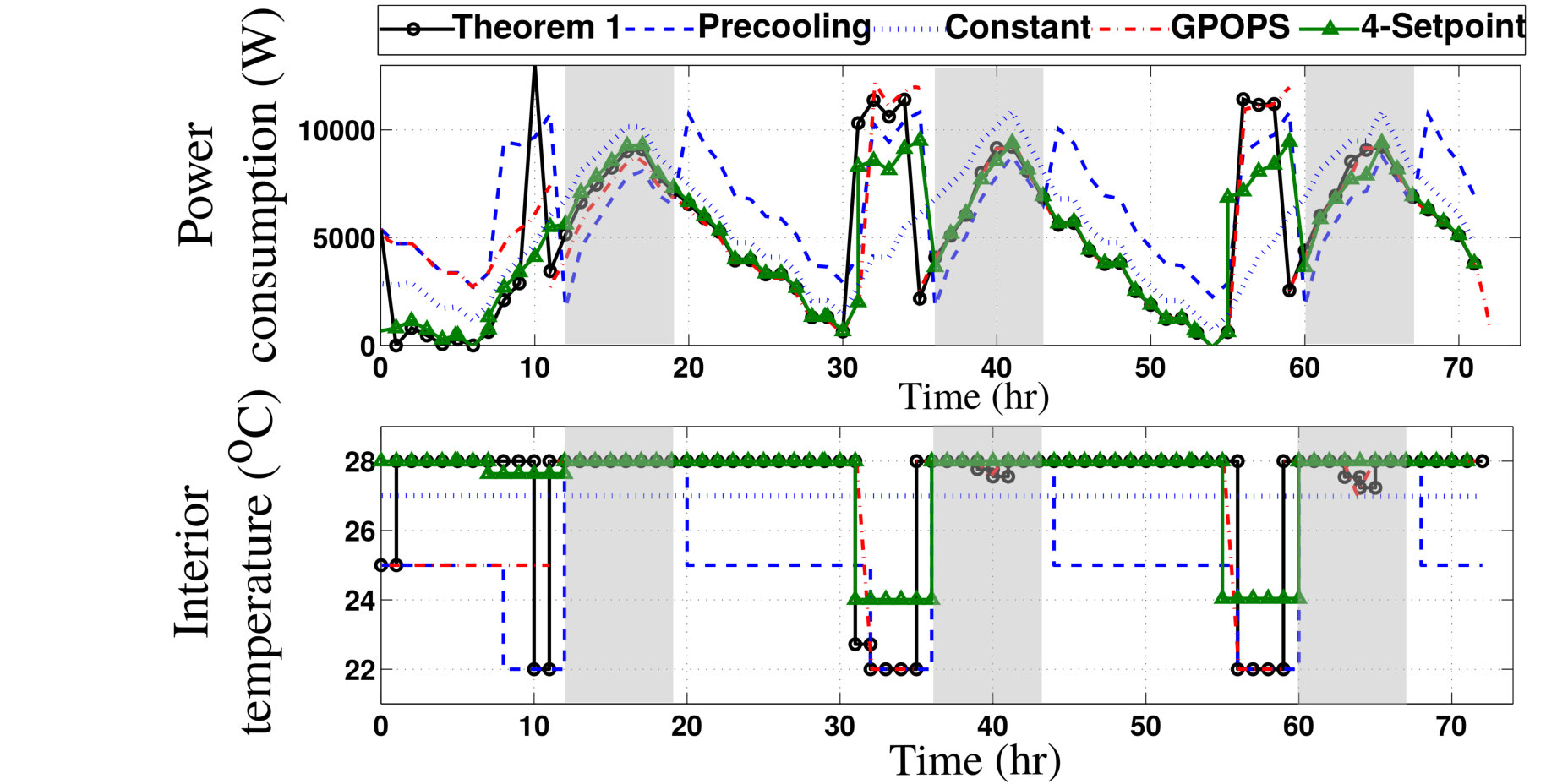

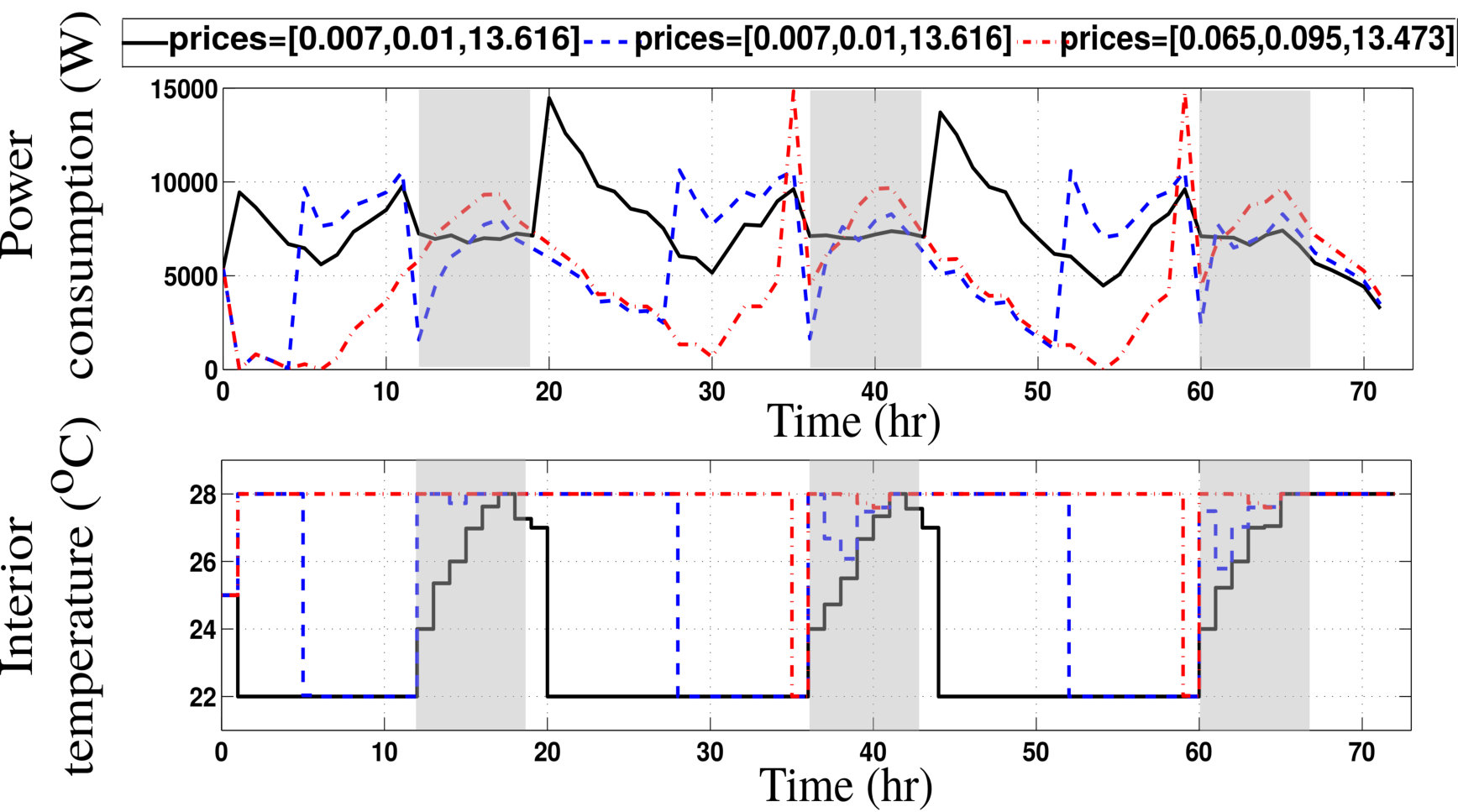

- 7.7 CASE I: Power Consumption and Temperature Settings for Various Programming Strategies Using APS’s Rates.

- 7.8 CASE I: Power Consumption and Optimal Temperature Settings for High, Medium and Low Demand Penalties. Shaded Areas Correspond to On-peak Hours.

- 7.9 CASE I: Power Consumption and Temperature Settings for High, Medium and Low Demand Penalties Using 4-Setpoint Thermostat Programming.

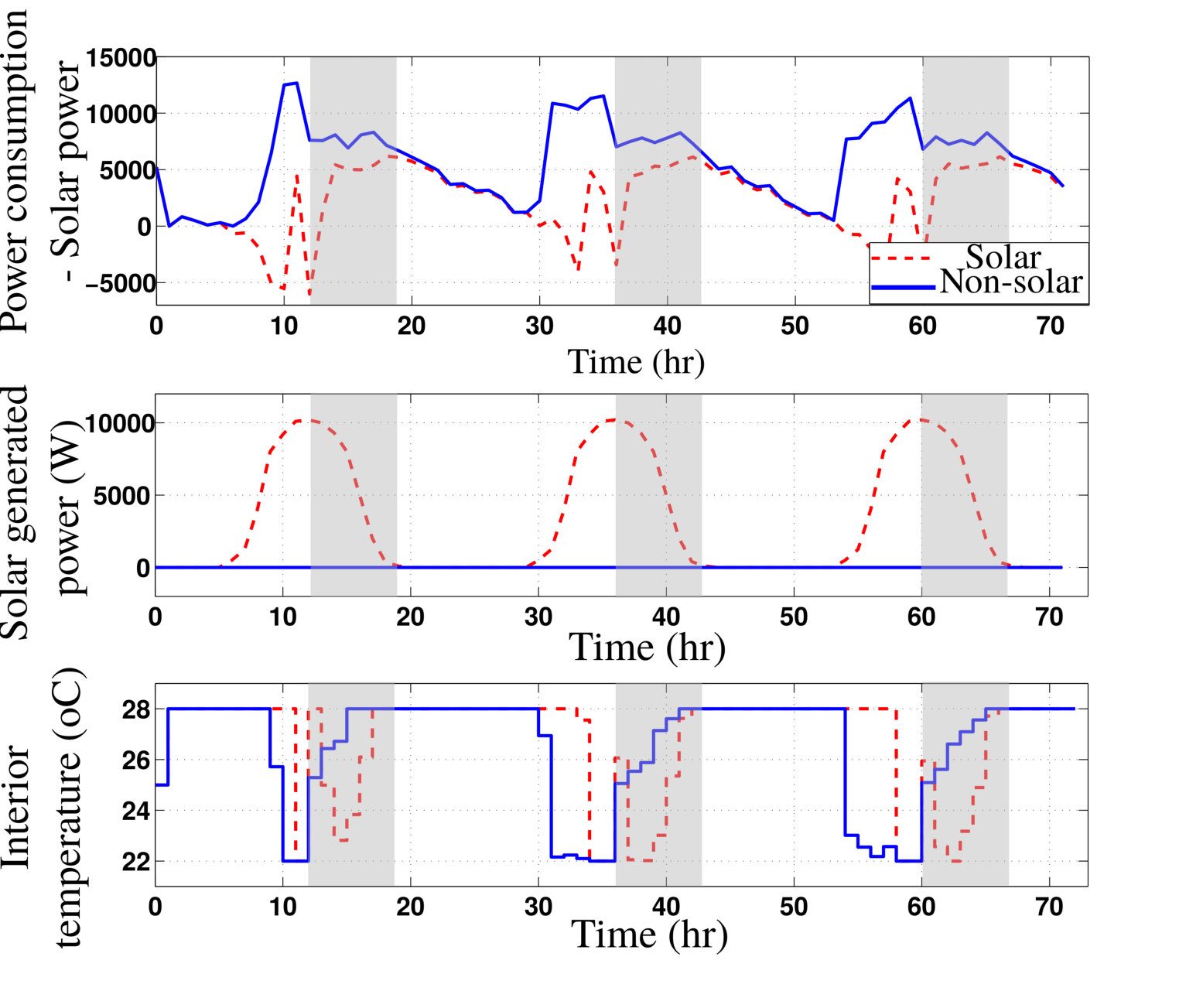

- 7.10 CASE III: Power Consumption, Solar Generated Power and Optimal Temperature Settings for the Non-solar and Solar Users.

Chapter 1 INTRODUCTION

Consider problems such as portfolio optimization, path-planning, structural design, local stability of nonlinear ordinary differential equations, control of time-delay systems and control of systems with uncertainties. These problems can all be formulated as polynomial optimization and/or optimization of polynomials. In this dissertation, we show how computation can be applied in a variety of ways to solve these classes of problems. A simple example of polynomial optimization is , where is a multi-variate polynomial and . In general, since and are not convex, this is not a convex optimization problem. In fact, it has been proved that polynomial optimization is NP-hard (L. Blum and Smale (1998)). Fortunately, algorithms such as branch-and-bound can find arbitrarily precise solutions to polynomial optimization problems by repeatedly partitioning into subsets and computing lower and upper bounds on over each . To find an upper bound for over each , one could use a local optimization algorithm such as sequential quadratic programming. To find a lower bound on over each , one can solve the following optimization problem.

[TABLE]

This problem is in fact an instance of the problem of optimization of polynomials. Optimization of polynomials is convex, yet again NP-hard. We will discuss optimization of polynomials in more depth in Chapter 2. In the following, we discuss some of the state-of-the-art methods for solving optimization of polynomials - hence finding lower bounds on .

1.1 Sum of Squares Method

One approach to find lower bounds on the optimal objective is to apply Sum of Squares (SOS) programming (Parrilo (2000), Papachristodoulou et al. (2013)). A polynomial is SOS if there exist polynomials such that . The set is called an SOS decomposition of , where is the ring of real polynomials. An SOS program is an optimization problem of the form

[TABLE]

where and are given. If is SOS, then clearly on . While verifying on is NP-hard, verifying whether is SOS - hence non-negative - can be done in polynomial time (Parrilo (2000)). It was first shown in Parrilo (2000) that verifying the existence of a SOS decomposition is a Semi-Definite Program (SDP). Fortunately, there exist several algorithms (Monteiro (1997); Helmberg et al. (1996); Alizadeh et al. (1998)) and solvers (Yamashita et al. (2010); Sturm (1999); Tutuncu et al. (2003)) which solve SDPs to arbitrary precision in polynomial time. To find lower bounds on , consider the SOS program

[TABLE]

Clearly . One can compute by performing a bisection search on and using semi-definite programming to verify is SOS. SOS programming can also be used to find lower bounds on global minimum of polynomials over a semi-algebraic set generated by . Given Problem (1.1) with , Positivstellensatz results (Stengle (1974), Putinar (1993), Schmudgen (1991)) define a sequence of SOS programs whose objective values form a sequence of lower bounds on the global minimum . For instance, Putinar’s Positivstellensatz defines the optimization problem

[TABLE]

where denotes the cone of SOS polynomials of degree . Putinar (1993) has shown that under certain conditions (verifiable by semi-definite programming) on and for sufficiently large , . See Laurent (2009) for a comprehensive discussion on the Positivstellensatz results.

1.2 Moments Method

As a dual to SOS program, Lasserre (2001) used the theory of moments to define a sequence of lower bounds for global optima of polynomials. Let , where is compact and with the index set . Let us denote the degree of by . Then, Lasserre (2001) showed that defined as

[TABLE]

is a lower bound on . In Equation (1.4), , where is called the moment of order and is represented by any probability measure111Let be a set and be a algebra over . Then is a probability measure if

and .

For all countable collections of pairwise disjoint subsets of , .

on such that . Moreover, is called the moment matrix associated with sequence and in two dimensions is defined as

[TABLE]

It can be shown that the SDPs in (1.4) are duals to the SDPs in (1.3) - implying that . Indeed, if has a non-empty interior, then for all sufficiently large , the duality gap is zero, i.e., . See Laurent (2009) and Jeyakumar et al. (2014) for conditions on convergence of the lower bounds to global minima and extension of moments method to polynomial optimization over non-compact semi-algebraic sets.

In the sequel, we explore the merits of some of the alternatives to SOS programming and moments method. There exist several results in the literature that can be applied to polynomial optimization; e.g., Quantifier Elimination (QE) algorithms (Collins and Hoon (1991)) for testing the feasibility of semi-algebraic sets, Reformulation Linear Techniques (RLTs) (Sherali and Tuncbilek (1992, 1997)) for linearizing polynomial optimizations, Polya’s theorem (G. Hardy and Polya (1934)) for positivity over the positive orthant, Bernstein’s (Boudaoud et al. (2008); Leroy (2012)) and Handelman’s (Handelman (1988a)) theorems for positivity over simplices and convex polytopes, and other results based on Groebner bases (Adams and Loustaunau (1994)) and Blossoming (Ramshaw (1987)) techniques. In particular, we will focus on Polya’s, Bernstein’s and Handelman’s results in more depth and elaborate on the computational advantages of these results over the others. The discussion of the other results are beyond the scope of this dissertation, however the ideas behind these results can be summarized as follows.

1.3 Quantifier Elimination

QE algorithms apply to First-Order Logic formulae, e.g.,

[TABLE]

to eliminate the quantified variables and (preceded by quantifiers ) and construct an equivalent formula in terms of the unquantified variable . The key result underlying QE algorithms is Tarski-Seidenberg theorem (Tarski (1951)). The theorem implies that for every formula of the form , where , there exists an equivalent quantifier-free formula of the form with . QE implementations (e.g., Brown (2003) and Dolzmann and Sturm (1997)) with a bisection search yields the exact solution to optimization of polynomials, however the complexity scales double exponentially in the dimension of variables .

1.4 Reformulation Linear Techniques

RLT was initially developed to find the convex hull of feasible solutions of zero-one linear programs (Sherali and Adams (1990)). It was later generalized by Sherali and Tuncbilek (1992) to address polynomial optimizations of the form subject to . RLT constructs a hierarchy of linear programs by performing two steps. In the first step (reformulation), RLT introduces the new constraints for all . In the second step (linearization), RTL defines a linear program by replacing every product of variables by a new variable. By increasing and repeating the two steps, one can construct a hierarchy of lower bounding linear programs. A combination of RLT and branch-and-bound partitioning of was developed by Sherali and Tuncbilek (1997) to achieve tighter lower bounds on the global minimum. For a survey of different extensions of RLT see Sherali and Liberti (2009).

1.5 Groebner Basis Technique

Groebner bases can be used to reduce a polynomial optimization over a semi-algebraic set to the problem of finding the roots of univariate polynomials (Chang and Wah (1994)). First, one needs to construct the system of polynomial equations

[TABLE]

where is the Lagrangian function. It is well-known that the set of solutions to (1.5) is the set of extrema of the polynomial optimization . Let

[TABLE]

Using the elimination property (Adams and Loustaunau (1994)) of the Groebner bases, the minimal Groebner basis of the ideal of defines a triangular-form system of polynomial equations. This system can be solved by calculating one variable at a time and back-substituting into other polynomials. The most computationally expensive part is the calculation of the Groebner basis, which in the worst case scales double-exponentially in the number of decision variables.

1.6 Blossoming Technique

The blossoming technique involves a bijective map between the space of polynomials and the space of multi-affine functions (polynomials that are affine in each variable), where is the degree of in variable . For instance, the blossom of a cubic polynomial is the multi-affine function

[TABLE]

It can be shown that the blossom, , of any polynomial with degree in variable satisfies the so-called diagonal property (Ramshaw (1987)), i.e.,

[TABLE]

By using this property, one can reformulate any polynomial optimization as

[TABLE]

where and is the semi-algebraic set defined by the blossoms of the generating polynomials of . In the special case, where is a hypercube, Sassi and Girard (2012) showed that the Lagrangian dual optimization problem to Problem (1.6) is a linear program. Hence, the optimal objective value of this linear program is a lower bound on the minimum of over the hypercube. Application of blossoming in estimation of reachability sets of discrete-time dynamical systems can be found in Sassi et al. (2012).

1.7 Bernstein, Polya and Handelman Theorems

While QE, RLT, Groebner bases and blossoming are all useful techniques with advantages and disadvantages (such as exponential complexity), we focus on Polya’s, Bernstein’s and Handelman’s theorems - results which yield polynomial-time tests for positivity of polynomials. Polya’s theorem yields a basis to represent the cone of polynomials that are positive over the positive orthant. Bernstein’s and Handelman’s theorems yield bases which represent the cones of polynomials that are positive over simplices and convex polytopes, respectively. Similar to SOS programming, one can find certificates of positivity using Polya’s, Bernstein’s and Handelman’s representations by solving a sequence of Linear Programs (LPs) and/or SDPs. However, unlike the SDPs associated with SOS programming, the SDPs associated with these theorems have a block-diagonal structure. In this dissertation, we exploit this structure to design parallel algorithms for optimization of polynomials of high degrees with several independent variables. See Kamyar and Peet (2012a), Kamyar and Peet (2012b), Kamyar and Peet (2013) and Kamyar et al. (2013) for parallel implementations of variants of Polya’s theorem applied to various Lyapunov inequalities.

Unfortunately, unlike the SOS methodology, the bases given by Polya’s theorem, Bernstein’s theorem and Handelman’s theorem cannot be used to represent the cone of non-negative polynomials which have zeros in the interior of simplices and polytopes. This is indeed a barrier against using these theorems to compute polynomial Lyapunov functions, since Lyapunov functions, by definition, have a zero at the origin. There do, however, exist some variants of Polya’s theorem which consider zeros at the corners Powers and Reznick (2006) and edges Castle et al. (2011) by constructing local certificates of non-negativity over closed subsets, , of the simplex such that is the simplex. These results apply to non-negative polynomials whose zeros are on the corners and/or edges of the simplex. Moreover, Oliveira et al. (2008) and Kamyar and Peet (2012b) propose versions of Polya’s theorem which prove positivity over hypercubes by: 1) Providing certificates of positivity on the Cartesian product of unit simplices; and 2) Introducing a one-to-one map between products of unit simplices (multi-simplex) and hypercubes. A generalization of Polya’s theorem for proving positivity on the entire was introduced by de Loera and Santos (1996). This generalization first applies Polya’s theorem to each orthant of to compute a certificate of positivity over each orthant. Then, it uses the merging technique in Lombardi (1991) to obtain a unified certificate - in the form of SOS of rationals - over . A recent extension of Polya’s theorem by Dickinson and Pohv (2014) can be used to prove positivity over an intersection of a semi-algebraic set with the positive orthant. Finally, positivity of polynomials with rational exponents can be verified by a weak version of Polya’s theorem in Delzell (2008).

1.8 Motivations and Summary of Contributions

The novelty of our research centers on the areas of: computation and energy. In the realm of computation, we observed that processors speeds are not growing at the rate they once were. The entire controls community seems to have ignored this fact, since everyone speaks of polynomial-time algorithms as the gold standard for what the solution to a control problem should look like. But what good is a polynomial-time algorithm when the degree of the polynomial is bounded by the current state-of-the-art computers. Our solution was to look at the only area where the computing world was getting faster (growing) - supercomputers. Surprisingly, there have been no studies on the use of parallel computers for controls since the 1970’s. The reason was that the mathematical machinery for analysis and control is based on Semidefinite Programming, which is inherently sequential (NC-hard). Our idea, however, was that if the SDP problem has special structure, then this structure can be exploited to distribute computation among processors. With this in mind, we decided to seek out alternatives to the classical Sum-of-Squares approach to nonlinear and robust stability analyses. We identified more than seven different alternatives to the Sum-of-Squares approach. In the end, not all of these had usable structures for parallelization. However, we identified three which did: polynomial positivity results by Handelman, Polya and Bernstein. To demonstrate how well this approach works in practice, we developed a Message Passing Interface code for Polya’s theorem. The result enabled stability analysis for systems three times larger (in terms of number of states) than any other algorithm. As a real-world application, we further used our code to analyze robust stability of plasma in the Tore Supra Tokamak reactor.

In the realm of energy, we noticed that the two electrical utility companies of Arizona (APS and SRP) have recently started charging their customers for their maximum rate of electricity usage. This intrigued us as a mathematical problem of how to optimize the thermostat settings of HVAC systems (the major sources of electricity consumption in Arizona) in order to minimize the electricity bill. This problem is interesting in that the time of peak electricity use is not usually at the hottest time of day, but rather a couple of hours after - a behaviour which is usually associated with a diffusion PDE. We used the heat equation to model the thermostat programming problem as an optimal control problem and it turned out to be unsolved. The mathematical reason being that the cost function is not separable in time - a property which is necessary for optimal control algorithms to converge to an optimal solution. We noticed that an arbitrarily precise approximation of the cost function however, satisfy certain properties which make it solvable on a Pareto-optimal front. The result is an optimal thermostat which can significantly reduce the electricity bills and peak demand of both solar and nonsolar customers under the current pricing plans. Expanding this approach, we started thinking about related topics, such as how to set the demand price on order to influence customers’ behavior in an optimal manner. Based on that, we proposed an optimal pricing algorithm which resulted in a moderate reduction in the cost of generating, transmission and distribution of electricity at SRP.

We highlight our contributions as follows. In Chapter 4, we propose a parallel set-up algorithm which applies Polya’s theorem to the parameter-dependent Lyapunov inequalities and with belonging to the standard simplex. Feasibility of these inequalities implies robust stability of the system of linear Ordinary Differential Equations (ODEs) over the simplex. The output of our set-up algorithm is a sequence of SDPs of increasing size and precision. A solution to any of these SDPs yield a Lyapunov function which is quadratic in the states and depends polynomially on the uncertain parameters. An interesting property of these SDPs is that they possess a block-diagonal structure. We show how this structure can be exploited to design a parallel interior-point primal-dual SDP solver which distributes the computation of search direction among a large number of processors. We then produce a Message Passing Interface (MPI) implementation of our set-up and solver algorithms. Through numerical experiments, we show that these algorithms achieve a near-linear theoretical and experimental speed-up (the increase in processing speed per additional processor). Moreover, our numerical experiments on cluster computers demonstrate the ability of our algorithms in utilizing hundreds and potentially thousands of processors to analyze systems with 100+ states.

In Chapter 5, we generalize our methodology to perform robust stability analysis over hypercubes. We first propose an extended version of Polya’s theorem. This theorem parameterizes every homogeneous polynomial which is positive over a hypercube. We then propose an extended set-up algorithm which maps the computation and memory - associated with applying the extended Polya’s theorem to stability analysis problems - to parallel machines. This set-up algorithm has no centralized computation and its per-core communication complexity scales polynomially with the state-space dimension and the number of uncertain parameters. As the result, it demonstrates a near-linear speed-up.

In Chapter 6, we further extend our analysis to address stability of nonlinear ODEs defined by a polynomial vector field . Our proposed solution to this problem is to reformulate the nonlinear stability problem using only strictly positive forms. Specifically, we use our extended version of Polya’s theorem in Chapter 5 to compute a matrix-valued homogeneous polynomial such that and for all inside a hypercube containing the origin in its interior. This yields a Lyapunov function of the form for the system . To do this, we design a new parallel set-up algorithm which applies Polya’s theorem to the inequalities and . The result is a sequence of SDPs with coefficients of as decision variables. Again, we show that these SDPs have a block-diagonal structure - thus can be solved in parallel using our SDP solver in Chapter 4. As an extension to stability analysis over arbitrary convex polytopes, we then propose an algorithm which applies Handelman’s theorem to the aforementioned Lyapunov inequalities. Unfortunately, as in the case of Polya’s theorem, Handelman’s theorem is incapable of parameterizing polynomials which possess zeros in the interior of a polytope. However, we show that this is not the case if the zeros are on the vertices of the polytope. By using this property, we propose the following methodology: 1) Decompose the polytope into several convex sub-polytopes with a common vertex on the equilibrium; 2) Apply Handelman’s theorem to Lyapunov inequalities defined on each sub-polytope. The result is a sequence of linear programs whose solutions define a piecewise polynomial Lyapunov function - hence proving asymptotic stability over the sublevel-set of inscribed in the original polytope. We provide a comprehensive comparison between the computational complexities of SOS algorithm, our Polya’s algorithms and our Handelman algorithm. Our analysis shows that by using a certain decomposition scheme, our algorithm (based on Handelman’s theorem) has the lowest computational complexity compared to the SOS and Polya’s algorithms.

Chapter 2 FUNDAMENTAL RESULTS FOR OPTIMIZATION OF POLYNOMIALS

In this chapter, we first provide an overview of fundamental theorems on positivity of polynomials over various sets. Then, we show how applying these theorems to optimization of polynomials problems of the Form (1.1) yields tractable convex optimization problems in the forms of LPs and/or SDPs. Any solution to these LPs and/or SDPs yields a lower-bound on the global minimum of the polynomial optimization problem .

2.1 Background on Positivity Results

In 1900, Hilbert published a list of mathematical problems, one of which is: For every non-negative , does there exist any non-zero such that is a sum of squares? In other words, is every non-negative polynomial a sum of squares of rational functions? This question was motivated by his earlier works (Hilbert (1888, 1893)), in which he proved: 1) Every non-negative bi-variate degree 4 homogeneous polynomial (A polynomial whose monomials all have the same degree) is a SOS of three polynomials; 2) Every bi-variate non-negative polynomial is a SOS of four rational functions; 3) Not every non-negative homogeneous polynomial with more than two variables and degree greater than 5 is SOS of polynomials. While there exist systematic ways (e.g., semi-definite programming) to prove that a non-negative polynomial is SOS, proving that a non-negative polynomial is not a SOS of polynomials is not straightforward. Indeed, the first example of a non-negative non-SOS polynomial was published eighty years after Hilbert posed his 17th problem. Motzkin (1967) constructed a PSD degree 6 polynomial with three variables which is not SOS:

[TABLE]

Non-negativity of follows directly from the inequality of arithmetic and geometric means, i.e., , by letting and . To show that is not SOS, first by contradiction suppose that there exist some and coefficients such that

[TABLE]

By substituting (2.1) in (2.2) and equating the coefficients of both sides of (2.2), it follows that . This is a contradiction, thus is not SOS of polynomials. A generalization of Motzkin’s example is given by Robinson (Reznick (2000)). Polynomials of the form are not SOS if polynomial of degree is not SOS. Hence, although the non-homogeneous Motzkin polynomial is non-negative it is not SOS.

Artin (1927) answered Hilbert’s problem in the following theorem.

Theorem 1**.**

(Artin’s theorem) A polynomial satisfies on if and only if there exist SOS polynomials and such that .

Although Artin settled Hilbert’s problem, his proof was neither constructive nor gave a characterization of the numerator and denominator . In 1939, Habicht provided some structure on and for a certain class of polynomials . Habicht (1939) showed that if a homogeneous polynomial is positive definite and can be expressed as for some polynomial , then one can choose the denominator . Moreover, he showed that by using , the numerator can be expressed as a sum of squares of monomials. Habicht used Polya’s theorem (Hardy et al. (1934), Theorem 56) to obtain the above characterizations for and .

Theorem 2**.**

(Polya’s theorem) Suppose a homogeneous polynomial satisfies for all . Then can be expressed as

[TABLE]

where and are homogeneous polynomials with all positive coefficients. Furthermore, for every homogeneous and some , the denominator can be chosen as .

To see Habicht’s result, suppose is homogeneous and positive on the positive orthant and can be expressed as for some homogeneous polynomial . By using Polya’s theorem, , where and polynomials and have all positive coefficients. Furthermore, from Theorem 2 we may choose . Then, . Now let , then . Since has all positive coefficients, is a sum of squares of monomials.

Similar to the case of positive definite polynomials, ternary positive semi-definite polynomials of the form can be parameterized using the denominator (Scheiderer (2006)). However, in any dimension higher than three, there exist positive semi-definite polynomials such that if is SOS, then has a zero other than the origin. Thus, for such polynomials , cannot be SOS. Indeed, it has been shown by Reznick (2005) that there exists no single SOS polynomial which satisfies for every positive semi-definite and some SOS polynomial .

As in the case of positivity on , there has been an extensive research regarding positivity of polynomials on bounded sets. A pioneering result on local positivity is Bernstein’s theorem (Bernstein (1915)). Bernstein’s theorem uses the polynomials as a basis to parameterize univariate polynomials which are positive on .

Theorem 3**.**

(Bernstein’s theorem) If a polynomial on , then there exist such that

[TABLE]

for some .

Powers and Reznick (2000) used Goursat’s transformation of to find an upper bound on . Unfortunately, the bound itself is a function of the minimum of on . In order to reduce the computational complexity of testing positivity, Boudaoud et al. (2008) proposed a decomposition scheme for breaking into a collection of sub-intervals. Subsequently, Bernstein’s theorem was applied to over each sub-interval to find a certificate of positivity over each sub-interval. An extension of this technique was proposed in Leroy (2012) to verify positivity over simplices (a simplex is the convex hull of vertices in ). Moreover, Leroy (2012) provided a degree bound as a function of the minimum of over the simplex, the number of variables in , the degree of and the maximum of certain affine combinations of the coefficients .

Handelman (1988b) also used products of affine functions as a basis (the Handelman basis) to extend Bernstein’s theorem to multi-variate polynomials which are positive on convex polytopes.

Theorem 4**.**

(Handelman’s Theorem) Given and , define the polytope . If a polynomial on , then there exist , such that for some ,

[TABLE]

Recently, S. Sankaranarayanan and Abrahám (2013) combined the Handelman basis with positive basis functions

[TABLE]

to compute Lyapunov functions over a hypercube , where and are the minimum and maximum of over the hypercube . A generalization of Handelman’s theorem was made by Schweighofer (2005) to verify non-negativity of polynomials over compact semi-algebraic sets. Schweighofer used the cone of polynomials111A set of polynomials is a cone if:

- and imply and ; and

- implies . defined in (2.5) to parameterize any polynomial which has the following properties:

is non-negative over the compact semi-algebraic set defined in (2.4) 2. 2.

for some in the Cone (2.5) and for some over

[TABLE]

Theorem 5**.**

(Schweighofer’s theorem) Suppose

[TABLE]

is compact. Define the following set of polynomials which are positive on .

[TABLE]

If on and there exist and polynomials on such that for some , then .

On the assumption that are affine functions, and are constant, Schweighofer’s theorem gives the same parameterization of as in Handelman’s theorem. Another special case of Schweighofer’s theorem is when . In this case, Schweighofer’s theorem reduces to Schmudgen’s Positivstellensatz (Schmudgen (1991)). Schmudgen’s Positivstellensatz states that the cone

[TABLE]

is sufficient to parameterize every over the semi-algebraic set generated by . Unfortunately, the cone contains products of , thus finding a representation of Form (2.6) for requires a search for at most SOS polynomials. Putinar’s Positivstellensatz (Putinar (1993)) reduces the complexity of Schmudgen’s parameterization in the case where the quadratic module (as defined in (2.8)) of polynomials is Archimedean, i.e., there exists such that

[TABLE]

Equivalently, if there exists some such that is compact, then is Archimedean.

Theorem 6**.**

(Putinars’s Positivstellensatz) Let and define

[TABLE]

If there exist some such that , then is Archimedean. If is Archimedean and over , then .

Finding a representation of Form (2.8) for , only requires a search for SOS polynomials using SOS programming. Verifying the Archimedian Condition (2.7) is also an SOS program. Observe that if is not Archimedean, one can add a redundant constraint (for sufficiently large ) to in order to make Archimedean. Archimedean condition clearly implies compactness of the semi-algebraic set because for any , . The following theorem lifts the compactness requirement for the semi-algebraic set .

Theorem 7**.**

(Stengle’s Positivstellensatz) Let and define the cone

[TABLE]

If on , then there exist such that .

Notice that the Parameterziation (2.3) in Handelman’s theorem is affine in and the coefficients . Likewise, the parameterizations in Theorems 5 and 6, i.e., and are affine in and . Thus, one can use convex optimization to find , and efficiently. Unfortunately, since the parameterization in Stengle’s Positivstellensatz is non-convex (bilinear in and ), it is more difficult to verify compared to Handelman’s and Putinar’s parameterizations.

For a comprehensive discussion on the Positivstellensatz and other results on polynomial positivity in algebraic geometry see Laurent (2009); Scheiderer (2009), and Prestel and Delzell (2004).

2.2 Polynomial Optimization and Optimization of Polynomials

Given for and , define a semi-algebraic set as

[TABLE]

We then define polynomial optimization problems as

[TABLE]

For example, the integer program

[TABLE]

with given and , can be formulated as a polynomial optimization problem by setting in (2.10) and setting

[TABLE]

in the definition of in (2.9).

Given and for and , we define Optimization of polynomials problems as

[TABLE]

where is defined in (2.9) and

[TABLE]

with , where coefficients are given. If the goal is to optimize over a polynomial variable, , this may be achieved using a basis of monomials for so that the polynomial variable becomes . Optimization of polynomials can be used to find in (2.10). For example, we can compute the optimal objective value of the polynomial optimization problem

[TABLE]

by solving the problem

[TABLE]

where Problem (2.13) can be expressed in the Form (2.12) by setting

[TABLE]

[TABLE]

Optimization of polynomials (2.12) can be reformulated as the feasibility problem

[TABLE]

where and are given and

[TABLE]

where polynomials and are given. The question of feasibility of a semi-algebraic set is NP-hard (L. Blum and Smale (1998)). However, if we have a test to verify , we can find by performing a bisection on . In the following section, we use the results of Section 2.1 to provide sufficient conditions, in the form of Linear Matrix Inequalities (LMIs), for .

2.3 Algorithms for Optimization of Polynomials

In this section, we discuss how to find lower bounds on for different classes of polynomial optimization problems. The results in this section are primarily expressed as methods for verifying and can be used with bisection to solve polynomial optimization problems.

2.3.1 Case 1: Optimization over the Standard Simplex

Define the standard unit simplex as

[TABLE]

Consider the polynomial optimization problem

[TABLE]

where is a homogeneous polynomial of degree . If is not homogeneous, we can homogenize it by multiplying each monomial in by . Notice that since for all , the homogenized is equal to for every . To find , one can solve the following optimization of polynomials problem.

[TABLE]

Clearly, Problem (2.16) can be re-stated as the following feasibility problem

[TABLE]

For a given , we can use the following version of Polya’s theorem to verify .

Theorem 8**.**

(Polya’s theorem, simplex version) If a homogeneous matrix-valued polynomial satisfies for all , then there exists such that all the coefficients of

[TABLE]

are positive definite.

See pages 57-59 of G. Hardy and Polya (1934) for a proof. The converse of the theorem only implies over the unit simplex. Given , it follows from the converse of Theorem 8 that if there exists some such that

[TABLE]

has all positive coefficients, where recall that is the degree of . We can compute lower bounds on by performing a bisection on . For each of the bisection, if there exists some such that all of the coefficients of (2.17) are positive, then . We have detailed this procedure in Algorithm 1.

In Chapter 4, we will propose a decentralized version of Algorithm 1 to perform robust stability analysis over a simplex.

2.3.2 Case 2: Optimization over The Hypercube

Given , define the hypercube

[TABLE]

Define the set of -variate multi-homogeneous polynomials of degree vector as

[TABLE]

In a more general case, if the coefficients are matrices, we call a matrix-valued multi-homogeneous polynomial. Now consider the polynomial optimization problem

[TABLE]

To find , one can solve the following feasibility problem.

[TABLE]

For a given , we propose the following version of Polya’s theorem (Kamyar and Peet (2012b)) to verify .

Theorem 9**.**

(Polya’s theorem: multi-simplex version) A matrix-valued multi-homogeneous polynomial satisfies for all , if there exist such that all the coefficients of

[TABLE]

are positive definite.

We will prove this result in Section 5.2. The converse of Theorem 9 only implies non-negativity of over the hypercube. To find lower bounds on , we first obtain the multi-homogeneous form of the polynomial in (2.20). In 5.2 we have provided a procedure to construct . Given and , it follows from the converse of Theorem 9 that defined in (2.20) is empty if there exists some such that

[TABLE]

has all positive coefficients, where is the degree of in . We can compute lower bounds on , as defined in (2.20), by performing a bisection on . For each of the bisection, if there exists some such that all of the coefficients of (2.21) are positive, then . By replacing (2.17) with (2.21) in Algorithm 1, this algorithm computes . In Chapter 5, we will propose a parallel algorithm to perform robust stability analysis for systems with uncertain parameters inside a hypercube.

2.3.3 Case 3: Optimization over The Convex Polytope

Given and , define the convex polytope

[TABLE]

Suppose is bounded. Consider the polynomial optimization problem

[TABLE]

where is a polynomial of degree . To find , one can solve the feasibility problem

[TABLE]

Given , one can use Handelman’s theorem to verify .

Theorem 10**.**

(Handelman’s Theorem) Given and , define the polytope . If a polynomial on , then there exist , such that for some ,

[TABLE]

Consider the Handelman basis associated with polytope defined as

[TABLE]

Basis spans the space of polynomials of degree or less, however it is not minimal. As a special case, if we take to be the standard unit simplex of , i.e.,

[TABLE]

then the following set of polynomials is called the Bernstein basis associated with .

[TABLE]

Unlike , is a minimal basis222This follows from the fact that every polynomial can be uniquely represented in the canonical basis and every member of the canonical basis is a unique linear combination of . A derivation for these linear combinations can be found in Farin (2002) for the vector space of polynomials of degree .

Given , polynomial of degree and , if there exist

[TABLE]

such that

[TABLE]

for some , then for all . Thus . Since is not a minimal basis, if (2.24) is feasible, then are not unique. Feasibility of Conditions (2.24) and (2.25) can be determined using linear programming. To set-up the linear program, we first represent the right and left hand side of (2.25) in the canonical basis as

[TABLE]

[TABLE]

where it can be shown that are affine in and is the cardinality of the index set . In (2.27),

[TABLE]

where and define the polytope in (2.22). Recall that in (2.27), denotes the vector of all variate monomials of degree or less. By equating (2.26) and (2.27) and cancelling from both sides, the problem of finding a lower bound on can be expressed as the following linear program.

[TABLE]

If Linear Program (2.28) is infeasible for some , then one can increase and repeat setting-up and solving Linear Program (2.28). From Handelman’s theorem, if for all , then for some , Conditions (2.24) and (2.25) hold and Linear Program (2.28) will have a solution. We have outlined this procedure in Algorithm 2. Unfortunately, to this date all the proposed upper-bounds on (see e.g., Powers and Reznick (2001) and Leroy (2012)) are functions of the minimum of over the polytope . In Chapter 6, we will combine this algorithm with a polytope decomposition scheme to construct Lyapunov functions for nonlinear systems with polynomial vector fields.

2.3.4 Case 4: Optimization over Compact Semi-algebraic Sets

Recall that we defined a semi-algebraic set as

[TABLE]

Suppose is bounded. Consider the polynomial optimization problem

[TABLE]

Define the following cone of polynomials which are positive over .

[TABLE]

where denotes the cone of SOS polynomials of degree . From Putinar’s Positivstellensatz (Theorem 6) it follows that if the Cone (2.30) is Archimedean, then the solution to the following SOS program is a lower bound on . Given , define

[TABLE]

On the other hand, every has a quadratic representation with a positive semi-definite matrix. To see this, suppose , where are polynomials of degree . Each can be written in the canonical basis as , where is the vector of all variate monomials of degree or less. Hence, we can write as

[TABLE]

where clearly . Therefore, for given and , Problem (2.31) can be formulated as the following linear matrix inequality.

[TABLE]

where and , where is the subspace of symmetric matrices in and . See G. Blekherman and Thomas (2013) for methods of solving SOS programs. Also Papachristodoulou et al. (2013) provide a MATLAB package called SOSTOOLs for solving SOS programs.

If the Cone (2.30) is not Archimedean, then we can use Schmudgen’s Positivstellensatz to obtain the following SOS program with solution .

[TABLE]

The Positivstellensatz and SOS programming can also be applied to polynomial optimization over a more general form of semi-algebraic sets defined as

[TABLE]

It can be shown that if and only if

[TABLE]

Thus, for any , we have

[TABLE]

Therefore, to find lower bounds on , one can apply SOS programming and Putinar’s Positivstellensatzs to .

2.3.5 Case 5: Tests for Non-negativity on :

The following result from Habicht (1939) defines a test for non-negativity of homogeneous polynomials over .

Theorem 11**.**

(Habicht theorem) For every homogeneous polynomial that satisfies for all , there exists some such that all of the coefficients of

[TABLE]

are positive. In particular, the product is a sum of squares of monomials.

Using this theorem, one can verify non-negativity of any homogeneous polynomial over by multiplying repeatedly by . If for some , the Product (2.34) has all positive coefficients, then . We can define an alternative test for non-negativity over using the following theorem (de Loera and Santos (1996)).

Theorem 12**.**

*Define . Suppose a polynomial of degree satisfies for all and its homogenization333Associated to every polynomial of degree , there exists a degree homogeneous polynomial , where .

is positive definite. Then*

there exist and coefficients such that

[TABLE]

where and . 2. 2.

there exist positive such that .

Based on the converse of Theorem 12, we propose the following test for non-negativity of polynomials over the cone for some . Multiply a given polynomial repeatedly by for some . If there exists some such that , then (2.35) clearly implies that for all . Since , we can repeat the test times to obtain a test for non-negativity of over .

The second part of Theorem 12 gives a solution to Hilbert’s problem (see Section 2.1). For a construction of this solution (i.e., numerator and denominator ) see de Loera and Santos (1996).

Chapter 3 SEMI-DEFINITE PROGRAMMING AND INTERIOR-POINT ALGORITHMS

As discussed in Chapter 2, Polya’s theorem, Handelman’s theorem and the Positivstellensatz results can be used to approximate the minimum of a polynomial over simplicies, hypercubes, polytopes and semi-algebraic sets. We showed that these theorems define sequences of Linear/Semi-Definite Programs (SDPs) whose solutions define lower bounds on the objective of the polynomial optimization problem. In this section, we focus on solving these SDPs. In particular, we discuss the primal and dual forms of semi-definite programming problems and introduce a state-of-the-art primal-dual interior-point algorithm for solving SDPs. In Section 4.5, we will propose a new parallel version of this algorithm - an algorithm which is specifically designed to solve the SDPs defined by applying Polya’s theorem to optimization of polynomials arising in robust stability and control problems.

3.1 Convex Optimization and Duality

Let us define the constrained optimization problem

[TABLE]

where and . For every problem of Form (3.1), one can define the Lagrangian function as

[TABLE]

where and are called the Lagrange multipliers associated with the inequality constraints and the equality constraints in (3.1), respectively. The vectors and are called the dual variables of Problem (3.1). Let us define the Lagrange dual function as

[TABLE]

The Lagrange dual functions have some interesting properties. First, because the Lagrangian is affine in and and the pointwise infimum of a family of affine functions is concave (Boyd and Vandenberghe (2004)), is a concave function. Second, it is easy to show that the dual functions yield lower bounds on as define in (3.1), i.e., . To find the best lower bound on using the Lagrange dual function, one can solve the Lagrange dual problem defined as

[TABLE]

Every pair which satisfies and is called a dual feasible point for Problem (3.3). Likewise, every satisfying for and for is a primal feasible point for Problem (3.1). Dual feasible points can be used to bound sub-optimality of a primal feasible point. In particular, for every primal feasible point and dual feasible point ,

[TABLE]

where is called the duality gap associated with and . For certain problems, the duality gap associated with primal optimal point and dual optimal point is zero, i.e.,

[TABLE]

This property is often called strong duality. One important class of problems which usually posses this property is convex optimization problems. A convex optimization problem is an optimization problem of Form (3.1), where the functions are convex111A function is convex if for all and for all such that and . and are affine. For example, the Lagrange dual problem (3.3) is by definition a convex problem (it is a maximization of a concave function) whether or not its primal (Eq. (3.1)) is convex. It can be shown that (Slater (2014)) if the primal problem (3.1) is convex and there exists some such that

[TABLE]

then strong duality holds. Strong duality can be exploited to solve the primal problem via its dual. This is useful specially when the dual is easier or computationally less expensive to solve. Suppose a dual optimal solution is known and strong duality holds. If

[TABLE]

is unique and primal feasible, is the primal optimal solution.

3.2 Descent Algorithms for Convex Optimization

Suppose is differentiable. For to be a minimum of , the necessary condition is that . The Karush-Kuhn-Tucker (KKT) conditions (Kuhn et al. (1951)) generalize this necessary condition for the constrained optimization problem (3.1), under the assumption that the functions and are differentiable. The KKT conditions can be stated as follows: Suppose is a primal optimal point for (3.1) and and are dual optimal points for (3.3). Moreover, suppose the strong duality holds, i.e., . Then, the optimal primal and dual points satisfy the following.

[TABLE]

The first line follows from the fact that is a minimizer of the Lagrangian . The second, third and fourth lines indicate that and are primal and dual feasible. The last line is called the complementary slackness and follows from strong duality. This condition implies that for , either the primal constraint must be active at (i.e., ) or its corresponding optimal dual variable must be zero.

In general, the KKT conditions are only necessary conditions for optimality. Indeed, under certain regularity conditions, local minima of the primal Problem (3.1) satisfy the KKT conditions. However, when the primal problem is convex and there exists which satisfies (3.4), the KKT conditions become necessary and sufficient. Motivated by this result, many of the existing convex optimization algorithms are in principle algorithms for solving the KKT conditions iteratively. These algorithms are often called descent algorithms because they generate a sequence of primal feasible solutions which satisfy

[TABLE]

unless is optimal. One example of descent algorithms is the Newton’s algorithm. Given a primal feasible starting point , Newton’s algorithm finds a sequence of search directions and step length such that all the iterates

[TABLE]

are feasible and satisfy (3.6). Given a primal feasible point , Newton’s algorithm calculates the search directions by first defining the convex optimization problem

[TABLE]

The objective function of Problem (3.7) is the second-order Taylor’s approximation of the objective function at . Then, the KKT optimality conditions for Problem (3.7) yield the following system of linear equations.

[TABLE]

where . If the coefficient matrix in (3.8) is nonsingular, then there exist a unique Newton’s search direction and optimal dual point for the dual to Problem (3.8). Finally, Newton’s algorithm calculates the new iterate as , where a step length can be obtained using a line search method such as backtracking (Dennis Jr and Schnabel (1996)) or bisection. A typical stopping criterion for Newton’s algorithm is for some desired , where recall that is the minimum of the second-order Taylor’s approximation of at , subject to the equality constraints in (3.7). The difference between and can also be interpreted as the size of Newton’s search direction defined by the following weighted norm of :

[TABLE]

For a comprehensive discussion on the complexity and convergence of Newton’s algorithm, refer to Boyd and Vandenberghe (2004).

3.3 Interior-point Algorithms for Convex Problems with Inequality Constraints

Suppose in Problem (3.1), are convex and differentiable and are affine and differentiable. One of the most successful class of algorithms for solving this type of problems is interior-point algorithms. Typically, interior-point algorithms solve this problem in two steps: 1- Reducing the problem to a sequence of convex optimization programs with only linear equality constraints; and 2- Applying a descent algorithm, e.g., Newton’s algorithm, to solve the equality constrained problem. One way to define this sequence of equality constrained problems is to incorporate the inequality constraints into the objective function using barrier functions. For example, by using logarithmic barrier functions one can approximate Problem (3.1) as

[TABLE]

for some . Clearly, if any of the inequality constraints becomes active (), then the objective function blows up. Thus, any solution to Problem (3.10) lies in the interior (as the name ‘interior-point’ suggests) of the feasible set

[TABLE]

Since Problem (3.10) is convex, one can use Newton’s algorithm to find the optimal solution for any . In particular, given and feasible , Newton’s algorithm finds a sequence by solving the modified KKT conditions

[TABLE]

for and and setting . The set of optimal solutions for all is called the central path. Corresponding to any in the central path, one can verify that

[TABLE]

are dual feasible and together with yield the duality gap . This indicates that as , converges to the optimal solution of Problem 3.1 under the assumption that are convex and differentiable and are affine and differentiable. Based on this result, we can summarize the interior-point barrier algorithm for inequality constrained problems in Algorithm 3.

An alternative subclass of interior-point algorithms for solving inequality constrained problems is the primal-dual algorithms. Similar to the barrier algorithm, primal-dual algorithms find their search direction by solving the KKT optimality conditions. However, instead of incorporating the inequality constraints into the objective function (equivalently, eliminating the dual variable from the KKT condition (3.5)), primal-dual algorithms simultaneously solve the primal problem and its dual by computing independent Newton’s search directions , and for primal and dual variables and . Given a feasible point for Problem (3.1) and , the basic version of primal-dual algorithms computes the search directions by approximating the modified KKT conditions

[TABLE]

at the point as

[TABLE]

and solving for . The primal-dual iterates are then updated according to

[TABLE]

Similar to the barrier algorithm, the duality gap corresponding to any feasible primal-dual iterate is . Thus, as in (3.12), the resulting iterates converge to the optimal solution of Problem (3.1), assuming that are convex and are affine. In the sequel, we describe a primal-dual algorithm for solving semi-definite programs - a class of convex optimization problems which has several applications in control theory.

3.4 Semi-definite Programming

Consider the delay-differential equation

[TABLE]

where and . From Repin (1965), a sufficient condition for asymptotic stability of this system is existence of such that the quadratic functional

[TABLE]

satisfies for all and . The derivative can be expanded as

[TABLE]

Thus, , where and

[TABLE]

Thus, stability of System (3.13) can be verified by solving the following feasibility problem:

[TABLE]

Now let us parameterize each as

[TABLE]

for , where and for . Then, we can formulate the problem of stability of System (3.13) as the convex optimization problem

[TABLE]

where the matrices for are defined as

[TABLE]

where

[TABLE]

Problem (3.15) is an example of the dual form of the Semi-Definite Programming (SDP) problem. We define SDP as the optimization of a linear objective function over the cone of positive definite matrices subject to linear matrix equality and linear matrix inequality constraints. Given for , for , and , the primal SDP problem is

[TABLE]

where the linear maps and are defined as

[TABLE]

To derive the dual SDP to Problem (3.17), we employ Lagrange multipliers and as follows.

[TABLE]

Then, from the min-max inequality, i.e.,

[TABLE]

it follows that

[TABLE]

Note that

[TABLE]

only if . In this case, clearly the maximum occurs when

[TABLE]

Therefore, we can the write dual SDP problem as

[TABLE]

From (3.15) and (3.19) it is clear that the problem of stability of the delay-differential Equation (3.13) can be formulated as the dual SDP defined by the elements

[TABLE]

where we have defined in (3.16).

SDPs are popular among controls community because not only they can be solved efficiently using convex optimization algorithms, but also a wide variety of problems in controls can be formulated as SDPs; e.g., robust stability (Bliman (2004a); Oliveira and Peres (2007)) and robust performance (Peaucelle and Arzelier (2001); Scherer (2006)) of uncertain systems, -optimal filter design (Li and Fu (1997); Geromel and de Oliveira (2001)), estimation of regions of attraction (Wang et al. (2005); Tan and Packard (2008); Topcu et al. (2010)) and reachability sets (Wang et al. (2013)) of nonlinear systems, stability and control of hybrid systems (Boukas (2006); Papchristodoulou and Prajna (2009)) and game theory (Parrilo (2006)). In the next section, we describe a state-of-the-art primal-dual algorithm by Helmberg et al. (2005) for solving SDPs.

3.5 A Primal-dual Interior-point Algorithm for Semi-definite Programming

Fortunately, there exists several interior-point algorithms in the literature for solving SDPs; e.g., dual scaling (Benson (2001); Benson et al. (1998)), primal-dual (Alizadeh et al. (1998); Monteiro (1997); Helmberg et al. (1996)) and cutting-plane/spectral bundle (Helmberg and Rendl (2000); Sivaramakrishnan (2010); Nayakkankuppam (2007)) algorithms. In our study, we are particularly interested in a state-of-the-art primal-dual algorithm proposed by Helmberg et al. (2005) mainly because at each iteration, it preserves a certain property (see (4.47)) of the primal and dual search directions. In Section 4.5, we will exploit this property to propose a distributed parallel version of this algorithm for solving large-scale SDPs in robust and/or nonlinear stability analysis. In the following, we briefly discuss the original version of this algorithm algorithm.

Similar to the barrier method described in Section 3.3, we can incorporate the inequality constraints in the dual SDP (3.19) using logarithmic barrier functions and the barrier parameter as

[TABLE]

The Lagrangian for Problem (3.20) is defined as

[TABLE]

Then, the KKT optimality conditions for Problem (3.20) is , which can be expanded as

[TABLE]

where and are defined in (3.18).

Given a barrier parameter , at each iteration, the primal-dual algorithm finds a search direction such that the new iterate belongs to the central path, i.e.,

[TABLE]

Conversely, given a point , one can use (3.23) and (3.24) to find its corresponding barrier parameter as

[TABLE]

The search direction of the primal-dual algorithm is the sum of two steps: the predictor step and the corrector or centering step . The predictor step is defined as the Newton’s step for solving the optimality conditions (3.21)-(3.24) with , starting at any point which satisfies

[TABLE]

Similar to the Taylor’s approximation in (3.12), we find the Newton’s step by solving

[TABLE]

for . Substituting for from (3.21)-(3.24) into (3.27) yields the following system of equations for the predictor step.

[TABLE]

[TABLE]

where

[TABLE]

The corrector step is defined as the Newton’s step for solving the KKT conditions (3.21)-(3.24), using the barrier parameter as defined in (3.25) and starting at

[TABLE]

where can be any point satisfying (3.26) and can be calculated using (3.28)-(3.30). Thus, to derive the corrector step, we substitute for from KKT conditions (3.21)-(3.24) into

[TABLE]

This yields the following set of equations for the corrector step.

[TABLE]

[TABLE]

By solving (3.28)-(3.30) for the predictor step and solving (3.31)-(3.33) for the corrector step, we can calculate the search direction as

[TABLE]

where is the symmetric part of matrix . We have provided an outline of the discussed primal-dual algorithm in Algorithm 4.

Chapter 4 PARALLEL ALGORITHMS FOR ROBUST STABILITY ANALYSIS OVER SIMPLEX

4.1 Background and Motivations

Control system theory when applied in practical situations often involves the use of large state-space models, typically due to inherent complexity of the system, the interconnection of subsystems, or the reduction of an infinite-dimensional or PDE model to a finite-dimensional approximation. One approach to dealing with such large scale models has been to use model reduction techniques such as balanced truncation (Gugercin and Antoulas (2004)). However, the use of model reduction techniques are not necessarily robust and can result in arbitrarily large errors. In addition to large state-space, practical problems often contain uncertainty in the model due to modeling errors, linearization, or fluctuation in the operating conditions. The problem of stability and control of systems with uncertainty has been widely studied. See, e.g. the texts Ackermann et al. (2001); Bhattacharyya et al. (1995); Green and Limebeer (1995); Zhou and Doyle (1998); Dullerud and Paganini (2000). Famous results such as the small-gain theorem, Popov’s criterion, passivity theorems and Kharitonov’s theorem have been widely used to find tractable solutions to certain robust stability problems of a single and/or interconnected uncertain systems. As an example, Kharitonov’s theorem reduces the stability problem of an infinite family of differential equations

[TABLE]

to verifying whether the following four characteristic polynomials

[TABLE]

[TABLE]

[TABLE]

[TABLE]

have all their roots in the open left half-plane - a problem which can be tractably solved (in operations) using the Routh-Hurwitz criterion. Despite all the progress in robust control theory during the past few decades, a drawback of existing computational methods for analysis and control of systems with uncertainty is high computational complexity. This is a consequence of the fact that a wide range of problems in robust stability and control of systems with parametric uncertainty are known to be NP-hard. For example, even the classical problem of stability of for all inside a hypercube (the matrix analog of System (4.1)) is NP-hard111Nemirovskii (1993) proves that the -integer linear programming problem (a well-known NP-complete problem) admits a polynomial-time reduction to the problem of verifying positive semi-definiteness of a family of symmetric matrices with entries belonging to an interval on . . Other examples are calculation of structured singular values for robust performance analysis and -synthesis (Zhou et al. (1996)), deciding null-controllability222A system is called null-controllable if for every initial state , there exist some and controls such that of for a given (Blondel and Tsitsiklis (1999)), and computing arbitrarily precise bounds on the joint spectral radius of matrices for stability analysis of systems with time-varying uncertainty (Gripenberg (1996)). See Blondel and Tsitsiklis (2000) for a comprehensive survey on NP-hard problems in control theory. The result of such complexity is that for systems with parametric uncertainty and with hundreds of states, existing algorithms fail with the primary point of failure usually being lack of unallocated memory.

In this dissertation, we seek to distribute the computation over an array of processors within the context of existing computational resources; specifically cluster-computers and supercomputers. When designing algorithms to run in a parallel computing environment, one must both synchronize computational tasks among the processors while minimizing communication overhead among the processors. This can be difficult, as each architecture has a specific memory hierarchy and communication graph (See Figure 4.1). Likewise, in a lower level, individual computing units may have different processing architectures and memory hierarchies; e.g., see a comparison of the memory hierarchy of a multi-core CPU and a GPU in Figure 4.1. We account for communication by explicitly modeling the required communication graph between processors. This communication graph is then mapped to the processor architecture using the Message-Passing Interface (MPI) (Walker and Dongarra (1996)). While there are many algorithms for robust stability analysis and control of linear systems, ours is the first which explicitly accounts for the processing architecture in the emerging multi-core computing environment.

Our approach to robust stability is based on the well-established use of parameter-dependent Quadratic-In-The-State (QITS) Lyapunov functions. The use of parameter-dependent Lyapunov QITS functions eliminates the conservativity associated with e.g. quadratic stability (Packard and Doyle (1990)), at the cost of requiring some restriction on the rate of parameter variation. Specifically, our QITS Lyapunov variables are polynomials in the vector of uncertain parameters. This is a generalization of the use of QITS Lyapunov functions with affine parameter dependence as in Barmish and DeMarco (1986) and expanded in, e.g. Gahinet et al. (1996); Oliveira and Peres (2005, 2001) and Ramos and Peres (2001). The use of polynomial QITS Lyapunov variables can be motivated by Bliman (2004b), wherein it is shown that any feasible parameter-dependent LMI with parameters inside a compact set has a polynomial solution or Peet (2009) wherein it is shown that local stability of a nonlinear vector field implies the existence of a polynomial Lyapunov function.