Bayesian Probabilistic Numerical Methods

Jon Cockayne, Chris Oates, Tim Sullivan, Mark Girolami

TL;DR

This paper formalizes Bayesian probabilistic numerical methods as solutions to inverse problems, providing conditions for their well-definition, convergence, and compositional use in complex tasks, bridging numerical analysis and uncertainty quantification.

Contribution

It establishes a rigorous Bayesian framework for probabilistic numerics, including convergence analysis and methods for composing solutions to complex numerical problems.

Findings

Bayesian probabilistic numerical methods are well-defined under general conditions.

A numerical approximation scheme with proven asymptotic convergence is proposed.

The framework is extended to pipelines of computation for complex tasks.

Abstract

The emergent field of probabilistic numerics has thus far lacked clear statistical principals. This paper establishes Bayesian probabilistic numerical methods as those which can be cast as solutions to certain inverse problems within the Bayesian framework. This allows us to establish general conditions under which Bayesian probabilistic numerical methods are well-defined, encompassing both non-linear and non-Gaussian models. For general computation, a numerical approximation scheme is proposed and its asymptotic convergence established. The theoretical development is then extended to pipelines of computation, wherein probabilistic numerical methods are composed to solve more challenging numerical tasks. The contribution highlights an important research frontier at the interface of numerical analysis and uncertainty quantification, with a challenging industrial application presented.

Click any figure to enlarge with its caption.

Figure 1

Figure 1 Figure 2

Figure 2 Figure 3

Figure 3 Figure 4

Figure 4 Figure 5

Figure 5 Figure 6

Figure 6 Figure 7

Figure 7 Figure 8

Figure 8 Figure 9

Figure 9 Figure 10

Figure 10 Figure 11

Figure 11 Figure 12

Figure 12 Figure 13

Figure 13 Figure 14

Figure 14 Figure 15

Figure 15 Figure 16

Figure 16 Figure 17

Figure 17 Figure 18

Figure 18 Figure 19

Figure 19 Figure 20

Figure 20 Figure 21

Figure 21 Figure 22

Figure 22 Figure 23

Figure 23 Figure 24

Figure 24 Figure 25

Figure 25 Figure 26

Figure 26 Figure 27

Figure 27 Figure 28

Figure 28 Figure 29

Figure 29Peer Reviews

No public reviews on file for this paper yet. If you reviewed it on a platform where reviews are public (OpenReview, ICLR, NeurIPS, ICML), you can paste yours below so the community can read it here.

Videos

No videos yet. Explain this paper in a talk, walkthrough, or lecture? Add one.

Bayesian Probabilistic Numerical Methods

Jon Cockayne111University of Warwick, [email protected]

Chris Oates222Newcastle University and Alan Turing Institute, [email protected]

Tim Sullivan333Free University of Berlin and Zuse Institute Berlin, [email protected]

Mark Girolami444Imperial College London and Alan Turing Institute, [email protected]

Abstract

The emergent field of probabilistic numerics has thus far lacked clear statistical principals. This paper establishes Bayesian probabilistic numerical methods as those which can be cast as solutions to certain inverse problems within the Bayesian framework. This allows us to establish general conditions under which Bayesian probabilistic numerical methods are well-defined, encompassing both non-linear and non-Gaussian models. For general computation, a numerical approximation scheme is proposed and its asymptotic convergence established. The theoretical development is then extended to pipelines of computation, wherein probabilistic numerical methods are composed to solve more challenging numerical tasks. The contribution highlights an important research frontier at the interface of numerical analysis and uncertainty quantification, with a challenging industrial application presented.

1 Introduction

Numerical computation underpins almost all of modern scientific and industrial research and development. The impact of a finite computational budget is that problems whose solutions are high- or infinite-dimensional, such as the solution of differential equations, must be discretised in order to be solved. The result is an approximation to the object of interest. The declining rate of processor improvement as physical limits are reached is in contrast to the surge in complexity of modern inference problems, and as a result the error incurred by discretisation is attracting increased interest (e.g. Capistrán et al., 2016).

The situation is epitomised in modern climate models, where use of single-precision arithmetic has been explored to permit finer temporal resolution. However, when computing in single-precision, a detailed time discretisation can increase total error, due to the increased number of single precision computations, and in practice some form of ad-hoc trade-off is sought (Harvey and Verseghy, 2015). It has been argued that statistical considerations can permit more principled error control strategies for such models (Hennig et al., 2015).

Numerical methods are designed to mitigate discretisation errors of all forms (Press et al., 2007). Nonetheless, the introduction of error is unavoidable and it is the role of the numerical analyst to provide control of this error (Oberkampf and Roy, 2013). The central theoretical results of numerical analysis have in general not been obtained through statistical considerations. More recently, the connection of discretisation error to statistics was noted as far back as Henrici (1963); Hull and Swenson (1966), who argued that discretisation error can be modelled using a series of independent random perturbations to standard numerical methods. However, numerical analysts have cast doubt on this approach, since discretisation error can be highly structured; see Kahan (1996) and Higham (2002, Section 2.8). To address these objections, the field of probabilistic numerics has emerged with the aim to properly quantify the uncertainty introduced through discretisation in numerical methods.

The foundations of probabilistic numerics were laid in the 1970s and 1980s, where an important shift in emphasis occurred from the descriptive statistical models of the 1960s to the use of formal inference modalities that generalise across classes of numerical tasks. In a remarkable series of papers, Larkin (1969, 1970, 1972); Kuelbs et al. (1972); Larkin (1974, 1979a, 1979b), Mike Larkin presented now classical results in probabilistic numerics, in particular establishing the correspondence between Gaussian measures on Hilbert spaces and optimal numerical methods. Re-discovered and re-emphasised on a number of occasions, the role for statisticians in this new outlook was clearly captured in Kadane and Wasilkowski (1985):

Statistics can be thought of as a set of tools used in making decisions and inferences in the face of uncertainty. Algorithms typically operate in such an environment. Perhaps then, statisticians might join the teams of scholars addressing algorithmic issues.

The 1980s culminated in development of Bayesian optimisation methods (Mockus, 1989; Törn and Žilinskas, 1989), as well as the relation of smoothing splines to Bayesian estimation (Kimeldorf and Wahba, 1970b; Diaconis and Freedman, 1983).

The modern notion of a probabilistic numerical method (henceforth PNM) was described in Hennig et al. (2015); these are algorithms whose output is a distribution over an unknown, deterministic quantity of interest, such as the numerical value of an integral. Recent research in this field includes PNMs for numerical linear algebra (Hennig, 2015; Bartels and Hennig, 2016), numerical solution of ordinary differential equations (ODEs; Schober et al., 2014; Kersting and Hennig, 2016; Schober et al., 2016; Conrad et al., 2016; Chkrebtii et al., 2016), numerical solution of partial differential equations (PDEs; Owhadi, 2015; Cockayne et al., 2016; Conrad et al., 2016) and numerical integration (O’Hagan, 1991; Briol et al., 2016).

Open Problems

Despite numerous recent successes and achievements, there is currently no general statistical foundation for PNMs, due to the infinite-dimensional nature of the problems being solved. For instance, at present it is not clear under what conditions a PNM is well-defined, except for in the standard conjugate Gaussian framework considered in (Larkin, 1972). This limits the extent to which domain-specific knowledge, such as boundedness of an integrand or monotonicity of a solution to a differential equation, can be encoded in PNMs. In contrast, classical numerical methods often exploit such information to achieve substantial reduction in discretisation error. For instance, finite element methods for solution of PDEs proceed based on a mesh that is designed to be more refined in areas of the domain where greater variation of the solution is anticipated (Strang and Fix, 1973).

Furthermore, although PNMs have been proposed for many standard numerical tasks (see Section 2.6.1), the lack of common theoretical foundations makes comparison of these methods difficult. Again taking PDEs as an example, Cockayne et al. (2016) placed a probability distribution on the unknown solution of the PDE, whereas Conrad et al. (2016) placed a probability distribution on the unknown discretisation error of a numerical method. The uncertainty modelled in each case is fundamentally different, but at present there is no framework in which to articulate the relationship between the two approaches. Furthermore, though PNMs are often reported as being “Bayesian” there is no clear definition of what this ought to entail.

A more profound consequence of the lack of common foundation occurs when we seek to compose multiple PNMs. For example, multi-physics cardiac models involve coupled ODEs and PDEs which must each be discretised and approximately solved to estimate a clinical quantity of interest (Niederer et al., 2011). The composition of successive discretisations leads to non-trivial error propagation and accumulation that could be quantified, in a statistical sense, with PNMs. However, proper composition of multiple PNMs for solutions of ODEs and PDEs requires that these PNMs share common statistical foundations that ensure coherence of the overall statistical output. These foundations remain to be established.

Contributions

The main contribution of this paper is to establish rigorous foundations for PNMs:

The first contribution is to argue for an explicit definition of a “Bayesian” PNM. Our framework generalises the seminal work of Larkin (1972) and builds on the modern and popular mathematical framework of Stuart (2010). This illuminates subtle distinctions among existing methods and clarifies the sense in which non-Bayesian methods are approximations to Bayesian PNMs.

The second contribution is to establish when PNMs are well-defined outside of the conjugate Gaussian context. For exploration of non-linear, non-Gaussian models, a numerical approximation scheme is developed and shown to asymptotically approach the posterior distribution of interest. Our aim here is not to develop new or more computationally efficient PNMs, but to understand when such development can be well-defined.

The third contribution is to discuss pipelines of composed PNMs. This is a critical area of development for probabilistic numerics; in isolation, the error of a numerical method can often be studied and understood, but when composed into a pipeline the resulting error structure may be non-trivial and its analysis becomes more difficult. The real power of probabilistic numerics lies in its application to pipelines of numerical methods, where the probabilistic formulation permits analysis of variance (ANOVA) to understand the contribution of each discretisation to the overall numerical error. This paper introduces conditions under which a composition of PNMs can be considered to provide meaningful output, so that ANOVA can be justified.

Structure of the Paper

In Section 2 we argue for an explicit definition of Bayesian PNM and establish when such methods are well-defined. Section 3 establishes connections to other related fields, in particular with relation to evaluating the performance of PNMs. In Section 4 we develop useful numerical approximations to the output of Bayesian PNMs. Section 5 develops the theory of composition for multiple PNMs. Finally, in Section 6 we present applications of the techniques discussed in this paper.

All proofs can be found in either the Appendix or the Electronic Supplement.

2 Probabilistic Numerical Methods

The aim of this section is to provide rigorous statistical foundations for PNMs.

2.1 Notation

For a measurable space , the shorthand will be used to denote the set of all distributions on . For we write when is absolutely continuous with respect to . The notation will be used to denote a Dirac measure on , so that . Let denote the indicator function of an event . For a measurable function and a distribution , we will on occasion use the notation and . The point-wise product of two functions and is denoted . For a function or operator , denotes the associated push-forward operator555Recall that, for measurable , the pushforward of a distribution is defined as for all . that acts on measures on the domain of . Let denote conditional independence. The subset is defined to consist of sequences for which is convergent. will be used to denote the set of continuous functions on .

2.2 Definition of a PNM

To first build intuition, consider numerical approximation of the Lebesgue integral

[TABLE]

for some integrable function , with respect to a measure on . Here we may directly interrogate the integrand at any , but unless is finite we cannot evaluate at all with a finite computational budget. Nonetheless, there are many algorithms for approximation of this integral based on information at some collection of locations .

To see the abstract structure of this problem, assume the state variable exists in a measurable space . Information about is provided through an information operator whose range is a measurable space . Thus, for the Lebesgue integration problem, the information operator is

[TABLE]

The space , in this case a space of functions, can be high- or infinite-dimensional, but the space of information is assumed to be finite-dimensional in accordance with our finite computational budget. In this paper we make explicit a quantity of interest (QoI) , defined by a map into a measurable space . This captures that itself may not be the object of interest for the numerical problem; for the Lebesgue integration illustration, the QoI is not itself but .

The standard approach to such computational problems is to construct an algorithm which, when applied, produces some approximation of based on the information , whose theoretical convergence order can be studied. A successful algorithm will often tailor the information operator to the QoI . For example, classical Gaussian cubature specifies sigma points at which the integrand must be evaluated, based on exact integration of certain polynomial test functions.

The probabilistic numerical approach, instead, begins with the introduction of a random variable on . The true state is fixed but unknown; the randomness is used an abstract device used to represent epistemic uncertainty about prior to evolution of the information operator (Hennig et al., 2015). This is now formalised:

Definition 2.1** (Belief Distribution).**

An element is a belief distribution666Two remarks are in order: First, we have avoided the use of “prior” as this abstract framework encompasses both Bayesian and non-Bayesian PNMs (to be defined). Second, the use of “belief” differs to the set-valued belief functions in Dempster–Shafer theory, which do not require that (Shafer, 1976). for if it carries the formal semantics of belief about the true, unknown state variable .

Thus we may consider to be the law of . The construction of an appropriate belief distribution for a specific numerical task is not the focus of this research and has been considered in detail in previous work; see the Electronic Supplement for an overview of this material. Rather we consider the problem of how one updates the belief distribution in response to the information obtained about the unknown . Generic approaches to update belief distributions, which generalise Bayesian inference beyond the unique update demanded in Bayes theorem, were formalised in Bissiri et al. (2016); de Carvalho et al. (2017).

Definition 2.2** (Probabilistic Numerical Method).**

Let , and be measurable spaces and let , and where and are measurable functions. The pair is called a probabilistic numerical method for estimation of a quantity of interest . The map is called an information operator, and the map is called a belief update operator.

The output of a PNM is a distribution . This holds the formal status of a belief distribution for the value of , based on both the initial belief about the value of and the information that are input to the PNM.

An objection sometimes raised to this construction is that itself is not random. We emphasise that this work does not propose that should be considered as such; the random variable is a formal statistical device used to represent epistemic uncertainty (Kadane, 2011; Lindley, 2014). Thus, there is no distinction from traditional statistics, in which represents a fixed but unknown parameter and encodes epistemic uncertainty about this parameter.

Before presenting specific instances of this general framework, we comment on the potential analogy between and the likelihood function, and between and Bayes’ theorem. Whilst intuitively correct, the mathematical developments in this paper are not well-suited to these terms; in Section 2.5 we show that Bayes formula is not well-defined, as the posterior distribution is not absolutely continuous with respect to the prior.

To strengthen intuition we now give specific examples of established PNMs:

Example 2.3** (Probabilistic Integration).**

Consider the numerical integration problem earlier discussed. Take , a separable Banach space of real-valued functions on , and the Borel -algebra for . The space is endowed with a Gaussian belief distribution . Given information , define to be the restriction of to those functions which interpolate at the points ; that is again Gaussian follows from linearity of the information operator (see Bogachev, 1998, for details). The QoI remains .

This problem was first considered by Larkin (1972). The belief update operator proposed therein, and later considered in Diaconis (1988); O’Hagan (1991) and others, was . Since Gaussians are closed under linear projection, the PNM output is a univariate Gaussian whose mean and variance can be expressed in closed-form for certain choices of Gaussian covariance function and reference measure on . Specifically, if has mean function and covariance function , then

[TABLE]

where are defined as , , is defined as and . This method was extensively studied in Briol et al. (2016), who provided a listing of combinations for which and possess a closed-form.

An interesting fact is that the mean of coincides with classical cubature rules for different choices of and (Diaconis, 1988; Särkkä et al., 2016). In Section 3 we will show that this is a typical feature of PNMs. The crucial distinction between PNMs and classical numerical methods is the distributional nature of , which carries the formal semantics of belief about the QoI. The full distribution was examined in Briol et al. (2016), who established contraction to the exact value of the integral under certain smoothness conditions on the Gaussian covariance function and on the integrand. See also Kanagawa et al. (2016); Karvonen and Särkkä (2017).

Example 2.4** (Probabilistic Meshless Method).**

As a canonical example of a PDE, take the following elliptic problem with Dirichlet boundary conditions

[TABLE]

where we assume and is a known coefficient. Let be a separable Banach space of appropriately differentiable real-valued functions and take to be the Borel -algebra for . In contrast to the first illustration, the QoI here is , as the goal is to make inferences about the solution of the PDE itself.

Such problems were considered in Cockayne et al. (2016) wherein was restricted to be a Gaussian distribution on . The information operator was constructed by choosing finite sets of locations and at which the system defined in Eq. (2.3) was evaluated, so that

[TABLE]

The belief update operator was chosen to be , where is the restriction of to those functions for which is satisfied. In the setting of a linear system of PDEs such as that in Eq. (2.3), the distribution is again Gaussian (Bogachev, 1998). Full details are provided in Cockayne et al. (2016).

As in the previous example, we note that the mean of coincides with the numerical solution to the PDE provided by a classical method (the symmetric collocation method; Fasshauer, 1999). The full distribution provides uncertainty quantification for the unknown exact solution and can again be shown to contract to the exact solution under certain smoothness conditions (Cockayne et al., 2016). This method was further analysed for a specific choice of covariance operator in the belief distribution , in an impressive contribution from Owhadi (2017).

2.2.1 Classical Numerical Methods

Standard numerical methods fit into the above framework, as can be seen by taking

[TABLE]

independent of the distribution , where a function gives the output of some classical numerical method for solving the problem of interest. Here maps to a Dirac measure centred on . Thus, information in is used to construct a point estimate for the QoI.

The formal language of probabilities is not used in classical numerical analysis to describe numerical error. However, in many cases the classical and probabilistic analyses are mathematically equivalent. For instance, there is an equivalence between the standard deviation of for probabilistic integration and the worst-case error for numerical cubature rules from numerical analysis (Novak and Woźniakowski, 2010). The explanation for this phenomenon will be given in Section 3.

2.3 Bayesian PNMs

Having defined a PNM, we now state the central definition of this paper, that is of a Bayesian PNM. Define to be the conditional distribution of the random variable , given the event . For now we assume that this can be defined without ambiguity and reserve a more technical treatment of conditional probabilities for Section 2.5.

In this work we followed Larkin (1972) and cast the problem of determining in Eq. (2.1) as a problem of Bayesian inversion, a framework now popular in applied mathematics and uncertainty quantification research (Stuart, 2010). However, in a standard Bayesian inverse problem the observed quantity is assumed to be corrupted with measurement error, which is described by a “likelihood”. This leads, under mild assumptions, to general versions of Bayes’ theorem (see Stuart, 2010, Section 2.2)

For PNM, however, the information is not corrupted with measurement error. As a result, the support of the likelihood is a null set under the prior, making the standard approaches to such problems, including Bayes’ theorem, ill-defined outside of the conjugate Gaussian case when unknowns are infinite-dimensional. This necessitates a new definition:

Definition 2.5** (Bayesian Probabilistic Numerical Method).**

A probabilistic numerical method is said to be Bayesian777The use of “Bayesian” contrasts with Bissiri et al. (2016), for whom all belief update operators represent Bayesian learning algorithms to some greater or lesser extent. An alternative term could be “lossless”, since all the information in is conditioned upon in . for a quantity of interest if, for all , the output

[TABLE]

That is, a PNM is Bayesian if the output of the PNM is the push-forward of the conditional distribution through . This definition is familiar from the examples in Section 2.2, which are both examples of Bayesian PNMs.

For Bayesian PNMs we adopt the traditional terminology in which is the prior for and the output the posterior for . Note that, for fixed and , the Bayesian choice of belief update operator (if it exists) is uniquely defined.

It is emphasised that the class of Bayesian PNMs is a subclass of all PNMs; examples of non-Bayesian PNMs are provided in Section 2.6.1. Our analysis is focussed on Bayesian PNMs due to their appealing Bayesian interpretation and ease of generalisation to pipelines of computation in Section 5. For non-Bayesian PNMs, careful definition and analysis of the belief update operator is necessary to enable proper interpretation of the uncertainty quantification being provided. In particular, the analysis of non-Bayesian PNMs may present considerable challenges in the context of computational pipelines, whereas for Bayesian PNMs this is shown in Section 5 to be straight-forward.

2.4 Model Evidence

A cornerstone of the Bayesian framework is the model evidence, or marginal likelihood (MacKay, 1992). Let be equipped with the Lebesgue reference measure , such that admits a density . Then the model evidence , based on the information that , can be used as the basis for Bayesian model comparison. In particular, two prior distributions , , can be compared through the Bayes factor

[TABLE]

where . Here the second expression is independent of the choice of reference measure and is thus valid for general . The model evidence has been explored in connection with the design of Bayesian PNM. For the integration and PDE examples 2.3 and 2.4, the model evidence has a closed form and was investigated in Briol et al. (2016); Cockayne et al. (2016). In Section 6 we investigate the model evidence in the context of non-linear ODEs and PDEs for which it must be approximated.

2.5 The Disintegration Theorem

The purpose of this section is to formalise and to determine conditions under which exists and is well-defined. From Definition 2.5, the output of a Bayesian PNM is . If exists, the pushforward exists as is assumed to be measurable; thus, in this section, we focus on the rigorous definition of .

Unlike many problems of Bayesian inversion, proceeding by an analogue of Bayes’ theorem is not possible. Let . Then we observe that, if it is measurable, may be a set of zero measure under . Standard techniques for infinite-dimensional Bayesian inversion rely on constructing a posterior distribution based on its Radon–Nikodým derivative with respect to the prior (Stuart, 2010). However, when no Radon–Nikodým derivative exists and we must turn to other approaches to establish when a Bayesian PNM is well-defined.

Conditioning on null sets is technical and was formalised in the celebrated construction of measure-theoretic probability by Kolmogorov (1933). The central challenge is to establish uniqueness of conditional probabilities. For this work we exploit the disintegration theorem to ensure our constructions are well-defined. The definition below is due to Dellacherie and Meyer (1978, p.78), and a statistical introduction to disintegration can be found in Chang and Pollard (1997).

Definition 2.6** (Disintegration).**

For , a collection is a disintegration of with respect to the (measurable) map if:

- 1

(Concentration:) for -almost all ;

and for each measurable it holds that

- 2

(Measurability:) is measurable; 2. 3

(Conditioning:) .

The concept of disintegration extends the usual concept of conditioning of random variables to the case where is a null set, in a way closely related to regular conditional distributions (Kolmogorov, 1933). Existence of disintegrations is guaranteed under general weak conditions:

Theorem 2.7** (Disintegration Theorem; Thm. 1 of Chang and Pollard (1997)).**

Let be a metric space, be the Borel -algebra and be Radon. Let be countably generated and contain all singletons for . Then there exists a disintegration of with respect to . Moreover, if is another such disintegration, then is a null set.

The requirement that is Radon is weak and is implied when is a Radon space, which encompasses, for example, separable complete metric spaces. The requirement that is countably generated is also weak and includes the standard case where with the Borel -algebra. From Theorem 2.7 it follows that exists and is essentially unique for all of the examples considered in this paper. Thus, under mild conditions, we have established that Bayesian PNMs are well-defined, in that an essentially unique disintegration exists. It is noted that a variational definition of has been posited as an alternative approach, for when the existence of a disintegration is difficult to establish (p3 of Garcia Trillos and Sanz-Alonso, 2017).

2.6 Prior Construction

The Gaussian distribution is popular as a prior in the PNM literature for its tractability, both in the fact that finite-dimensional distributions take a closed-form and that an explicit conditioning formula exists. More general priors, such as Besov priors (Dashti et al., 2012) and Cauchy priors (Sullivan, 2016) are less easily accessed. In this section we summarise a common construction for these prior distributions, designed to ensure that a disintegration will exist.

Let denote an orthogonal Schauder basis for , assumed to be a separable Banach space in this section. Then any can be represented through an expansion

[TABLE]

for some fixed element and a sequence . Construction of measures is then reduced to construction of almost-surely convergent measures on and studying the pushforward of such measures into . In particular, this will ensure that is Radon (as is a separable complete metric space), a key requirement for existence of a disintegration .

To this end it is common to split into a stochastic and deterministic component; let represent an i.i.d sequence of random variables, and for some . Then with , for the prior distribution to be well-posed we require that almost-surely . Different choices of give rise to different distributions on . For instance, , is termed a uniform prior and gives a Gaussian prior, where determines the regularity of the covariance operator (Bogachev, 1998). The choice of gives a Cauchy prior in the sense of Sullivan (2016); here we require for a separable Banach space, or for when is a Hilbert space.

A range of prior specifications will be explored in Section 6, including non-Gaussian prior distributions for numerical solution of nonlinear ODEs.

2.6.1 Dichotomy of Existing PNMs

This section concludes with an overview of existing PNMs with respect to our definition of a Bayesian PNM. This serves to clarify some subtle distinctions in existing literature, as well as to highlight the generality of our framework. To maintain brevity we have summarised our findings in Table LABEL:table:comparison.

3 Decision-Theoretic Treatment

Next we assess the performance of PNMs from a decision-theoretic perspective (Berger, 1985) and explore connections to average-case analysis of classical numerical methods (Ritter, 2000). Note that the treatment here is agnostic to whether the PNM in question is Bayesian, and also encompasses classical numerical methods. Throughout, the existence of a disintegration will be assumed.

3.1 Loss and Risk

Consider a generic loss function where describes the loss incurred when the true QoI is estimated with . Integrability of is assumed.

The belief update operator returns a distribution over which can be cast as a randomised decision rule for estimation of . For randomised decision rules, the risk function is defined as

[TABLE]

The average risk of the PNM with respect to is defined as

[TABLE]

Here a state is drawn at random and the risk of the PNM output is computed. We follow the convention of terming the Bayes risk of the PNM, though the usual objection that a frequentist expectation enters into the definition of the Bayes risk could be raised.

Next, we consider a sequence of information operators indexed such that is -dimensional (i.e. pieces of information are provided about ).

Definition 3.1** (Contraction).**

A sequence of PNMs is said to contract at a rate under a belief distribution if .

This definition allows for comparison of classical and probabilistic numerical methods (Kadane and Wasilkowski, 1983; Diaconis, 1988). In each case an important goal is to determine methods that contract as quickly as possible for a given distribution that defines the Bayes risk. This is the approach taken in average-case analysis (ACA; Ritter, 2000) and will be discussed in Section 3.4. For Examples 2.3 and 2.4 of Bayesian PNMs, Briol et al. (2016) and Cockayne et al. (2016) established rates of contraction for particular prior distributions ; we refer the reader to those papers for details.

3.2 Bayes Decision Rules

A (possibly randomised) decision rule is said to be a Bayes rule if it achieves the minimum Bayes risk among all decision rules. In the context of (not necessarily Bayesian) PNMs, let and let

[TABLE]

That is, for fixed , is the set of all belief update operators that achieve minimum Bayes risk.

This raises the natural question of which belief update operators yield Bayes rules. Although the definition of a Bayes rule applies generically to both probabilistic and deterministic numerical methods, it can be shown888The proof is included in the Electronic Supplement. that if is non-empty, then there exists a which takes the form of a classical numerical method, as expressed in Eq. (2.4). Thus in general, Bayesian PNMs do not constitute Bayes rules, as the extra uncertainty inflates the Bayes risk, so that such methods are not optimal.

Nonetheless, there is a natural connection between Bayesian PNMs and Bayes rules, as exposed in Kadane and Wasilkowski (1983):

Theorem 3.2**.**

Let be a Bayesian probabilistic numerical method for the QoI . Let be an inner-product space and let the loss function have the form , where is the norm induced by the inner product. Then the decision rule that returns the mean of the distribution is a Bayes rule for estimation of .

This well-known fact from Bayesian decision theory999This is the fact that the Bayes act is the posterior mean under squared-error loss (Berger, 1985). is interesting in light of recent research in constructing PNMs whose mean functions correspond to classical numerical methods (Schober et al., 2014; Hennig, 2015; Särkkä et al., 2016; Teymur et al., 2016; Schober et al., 2016). Theorem 3.2 explains the results in Examples 2.3 and 2.4, in which both instances of Bayesian PNMs were demonstrated to be centred on an established classical method.

3.3 Optimal Information

The previous section considered selection of the belief update operator , but not of the information operator . The choice of determines the Bayes risk for a PNM, which leads to a problem of experimental design to minimise that risk.

The theoretical study of optimal information is the focus of the information complexity literature (Traub et al., 1988; Novak and Woźniakowski, 2010), while other fields such as quasi-Monte Carlo (QMC, Dick and Pillichshammer, 2010) attempt to develop asymptotically optimal information operators for specific numerical tasks, such as the choice of evaluation points for numerical approximation of integrals in the case of QMC. Here we characterise optimal information for Bayesian PNMs.

Consider the choice of from a fixed subset of the set of all possible information operators. To build intuition, for the task of numerical integration, could represent all possible choices of locations where the integrand is evaluated. For Bayesian PNM, one can ask for optimal information:

[TABLE]

where we have made explicit the fact that the optimal information depends on the choice of prior . Next we characterise , while an explicit example of optimal information for a Bayesian PNM is detailed in Example 3.4.

3.4 Connection to Average Case Analysis

The decision theoretic framework in Section 3.1 is closely related to average-case analysis (ACA) of classical numerical methods (Ritter, 2000). In ACA the performance of a classical numerical method is studied in terms of the Bayes risk given in Eq. (3.1), for the PNM with belief operator as in Eq. (2.4). ACA is concerned with the study of optimal information:

[TABLE]

In general there is no reason to expect and to coincide, since Bayesian PNM are not Bayes rules101010The distribution will in general not be supported on the set of Bayes acts.. Indeed, an explicit example where is presented in Appendix S3. However, we can establish sufficient conditions under which optimal information for a Bayesian PNM is the same as optimal information for ACA:

Theorem 3.3**.**

Let be an inner product space and the loss function have the form where is the norm induced by the inner product. Then the optimal information for a Bayesian PNM and for ACA are identical.

It is emphasised that this result is not a trivial consequence of the correspondance between Bayes rules and worst case optimal methods, as exposed in Kadane and Wasilkowski (1983). To the best of our knowledge, information-based complexity research has studied but not .

Theorem 3.3 establishes that, for the squared norm loss, we can extract results on optimal average case information from the ACA literature and use them to construct optimal Bayesian PNMs. An example is provided next.

Example 3.4** (Optimal Information for Probabilistic Integration).**

To illustrate optimal information for Bayesian PNMs, we revisit the first worked example of ACA, due to Sul*′*din (1959, 1960). Set and take the belief distribution to be induced from the Weiner process on , i.e. a Gaussian process with mean [math] and covariance function . Our QoI is and the loss function is .

Consider standard information for fixed knots . Our aim is to determine knots that represent optimal information for a Bayesian PNM with respect to and .

Motivated by Theorem 3.3 we first solve the optimal information problem for ACA and then derive the associated PNM. It will be sufficient to restrict attention to linear methods with . This allows a closed-form expression for the average error:

[TABLE]

Standard calculus can be used to minimise Eq. (3.2) over both the weights and the locations ; the full calculation can be found in Chapter 2, Section 3.3 of Ritter (2000). The result is an ACA optimal method

[TABLE]

which is recognised as the trapezium rule with equally spaced knots. The associated contraction rate is (Lee and Wasilkowski, 1986).

From Theorem 3.3 we have that ACA optimal information is also optimal information for the Bayesian PNM. Thus the optimal Bayesian PNM for the belief distribution is uniquely determined:

[TABLE]

Note how the PNM is centred on the ACA optimal method. However the PNM itself is not a Bayes rule; it in fact carries twice the Bayes risk as the ACA method.

This illustration can be generalised. It is known that for induced from the Weiner process on , a linear functional and a loss function that is convex and symmetric, equi-spaced evaluation points are essentially optimal information, the Bayes rule is the natural spline of degree , and the contraction rate is essentially ; see Lee and Wasilkowski (1986) for a complete treatment.

This completes our performance assessment for PNMs; next we turn to computational matters.

4 Numerical Disintegration

In this section we discuss algorithms to access the output from a Bayesian PNM. The approach considered in this paper is to form an explicit approximation to that can be sampled. The construction of a sampling scheme can exploit sophisticated Monte Carlo methods and allow probing at a computational cost that is de-coupled from the potentially substantial cost of obtaining the information itself.

The construction of an approximation to is non-trivial on a technical level. As shown in Section 2.5, under weak conditions on the space and the operator , the disintegration is well-defined for -almost all . The approach considered in this work is based on sampling from an approximate distribution which converges in an appropriate sense to in the limit. This follows in a similar spirit to Ackerman et al. (2017).

4.1 Sequential Approximation of a Disintegration

Suppose that is an open subset of and that the distribution , admits a continuous and positive density with respect to Lebesgue measure on . Further endow with the structure of a Hilbert space, with norm .

Let denote a decreasing function, to be specified, that is continuous at [math], with and . Consider

[TABLE]

where the normalisation constant

[TABLE]

is non-zero since is bounded away from 0 on a neighbourhood of and is bounded away from 0 on a sufficiently small interval . Our aim is to approximate with for small bandwidth parameter . The construction, which can be considered a mathematical generalisation of approximate Bayesian computation (Del Moral et al., 2012), ensures that . The role of is to admit states for which is close to but not necessarily equal. It is assumed to be sufficiently regular:

Assumption 4.1**.**

There exists such that .

To discuss the convergence of to we must first select a metric on . Let be a normed space of (measurable) functions with norm . For measures , define

[TABLE]

This formulation encompasses many common probability metrics such as the total variation distance and Wasserstein distance (Müller, 1997). However, not all spaces of functions lead to useful theory. In particular the total variation distance between and for will be one in general. Furthermore depending on the choice of , may be merely a pseudometric111111For a pseudometric, need not hold.. Sufficient conditions for weak convergence with respect to are now established:

Assumption 4.2**.**

The map is almost everywhere -Hölder continuous in , i.e.

[TABLE]

for some constant and for almost all .

Sufficient conditions for Assumption 4.2 are discussed in Ackerman et al. (2017), but are somewhat technical.

Theorem 4.3**.**

Let . Then, for sufficiently small,

[TABLE]

for almost all .

This result justifies the approximation of by when the QoI can be well-approximated by integrals with respect to . This result is stronger than that of earlier work, such as Pfanzagl (1979), in that it holds for infinite-dimensional , though it also relies upon the stronger Hölder continuity assumption.

The specific form for is not fundamental, but can impact upon rate constants. For the choice we have , which can be bounded independent of the dimension of . On the other hand, for it can be shown that, for ,

[TABLE]

so that the constant might not be bounded. In general this necessitates effective Monte Carlo methods that are able to sample from the regime where can be extremely small, in order to control the overall approximation error.

4.2 Computation for Series Priors

The series representation of in Eq. (2.6) of Section 2.6 is infinite-dimensional and thus cannot, in general, be instantiated. To this end, define and define the associated projection operator as

[TABLE]

A natural approach is to compute with the modified information operator instead of . This has the effect of updating the distribution of the first coefficients and leaving the tail unchanged, to produce an output . Then computation performed in the Bayesian update step is finite-dimensional, whilst instantiation of the posterior itself remains infinite-dimensional. A “likelihood-informed” choice of basis in such problems was considered in Cui et al. (2016).

Inspired by this approach, we next considered convergence of the output to in the limit . In this section it is additionally required that be everywhere continuous with . Let , so that is a continuous bijection of to itself. The following are also assumed:

Assumption 4.4**.**

For each , it holds that for some constant and all .

Assumption 4.5**.**

for all , where is measurable and satisfies and vanishes as is increased.

Assumption 4.6**.**

.

Assumption 4.7**.**

for some constant and all .

Assumption 4.4 holds for the case with constant . Assumption 4.5 is standard in the inverse problem literature; for instance it is shown to hold for certain series priors in Theorem 3.4 of Cotter et al. (2010). Assumption 4.6 is, in essence, a compactness assumption, in that it is implied by compactness of the state space when is linear. In this sense it is a strong assumption; however it can be enforced in our experiments, where is unbounded, through a threshold map

[TABLE]

where is a large pre-defined constant. Assumption 4.7 places a restriction on the probability metric in which our result is stated.

The following theorem has its proof in the Electronic Supplement:

Theorem 4.8**.**

For some constant , dependent on , it holds that .

An immediate consequence of Theorems 4.3 and 4.8 is that the total approximation error can be bounded by applying the triangle inequality:

[TABLE]

In particular, we have convergence of to in the limit provided that the number of basis functions satisfies .

The approximate posterior analysed above can be sampled when is Gaussian, since the first coefficients can be handled with MCMC and the tail , being Gaussian, can be sampled. However, when is non-Gaussian the tail is not recognised in a form that can be sampled. For the experiments in Section 6, in which both Gaussian and non-Gaussian priors are considered, the series in Eq. (2.6) was truncated at level , with the resultant prior denoted . The associated posterior was then entirely supported on the finite-dimensional subspace ; this is mathematically equivalent to working with the projected output . Analysis of prior truncation, as opposed to modification of the information operator just reported, is known to be difficult. Indeed, while converges to weakly, it does not do so in total variation, and this deficiency generally transfers to the associated posteriors. In general the impact of prior perturbation is a subtle topic — see e.g. Owhadi et al. (2015) and the references therein — and we therefore defer theoretical analysis of this approximation to future work.

4.3 Monte Carlo Methods for Numerical Disintegration

The previous sections established a sequence of well-defined distributions (or for non-Gaussian models) which converge (in a specific weak sense) to the exact disintegration . From construction, and this is sufficient to allow standard Monte Carlo methods to be used. The construction of Monte Carlo methods is de-coupled from the core material in the main text and the main methodological considerations are well-documented (e.g. Girolami and Calderhead, 2011).

For the experiments reported in subsequent sections two approaches were explored; a Sequential Monte Carlo (SMC) method (Doucet et al., 2001) and a parallel tempering method (Geyer, 1991). This provided a transparent sampling scheme, whose non-asymptotic approximation error can be theoretically understood. In particular, they provide robust estimators of model evidence that can be used for Bayesian model comparison. Full details of the Monte-Carlo methods used for this work, along with associated theoretical analysis for the SMC method, are contained in Section S4.1 of the Electronic Supplement.

5 Computational Pipelines and PNM

The last theoretical development in this paper concerns composition of several PNMs. Most analysis of numerical methods focuses on the error incurred by an individual method. However, real-world computational procedures typically rely on the composition of several numerical methods. The manner in which accumulated discretisation error affects computational output may be highly non-trivial (Roy, 2010; Anderson, 2011; Babuška and Söderlind, 2016). An extreme example occurs when one of the numerical methods in a pipeline is charged with integration of a chaotic dynamical system (Strogatz, 2014).

In recent work, Chkrebtii et al. (2016), Conrad et al. (2016) and Cockayne et al. (2016) each used PNMs within a broader statistical procedure to estimate unknown parameters in systems of ODEs and PDEs. The probabilistic description of discretisation error was incorporated into the data-likelihood, resulting in posterior distributions for parameters with inflated uncertainty to properly account for the inferential impact of discretisation error. However, beyond these limited works, no examination of the composition of PNMs has been performed. In particular, the question of which PNMs can be composed, and when the output of such a composition is meaningful, has not been addressed. This is important; for instance, if the output of a composition of PNMs is to be used for analysis of variance to elucidate the main sources of discretisation error, then it is important that such output is meaningful.

This section defines a pipeline as an abstract graphical object that may be combined with a collection of compatible PNMs. It is proven that when compatible Bayesian PNMs are employed in the pipeline, the distributional output of the pipeline carries a Bayesian interpretation under an explicit conditional independence condition on the prior .

To build intuition, for the simple case where two Bayesian PNMs are composed in series, our results provide conditions for when, informally, the output corresponds to a single Bayesian procedure . To reduce the notational and technical burden, in this section we will not provide rigorous measure theoretic details; however we note that those details broadly follow the same pattern as in Section 2.5.

5.1 Computational Pipelines

To analyse pipelines of PNMs, we consider such methods , where each method is defined on a common121212This is without loss of generality, since can be taken as the union of all state spaces required by the individual methods. state space and targets a QoI . A pipeline will be represented as a directed graphical model, wherein the QoIs from parent methods constitute information operators for child methods. It may be that a method will take quantities from multiple parents as input. To allow for this, we suppose that the information operator can be decomposed into components such that and . Thus, each component can be thought of as the QoI output by one of the parents of the method .

Without loss of generality we designate the th QoI to be the principal QoI. That is, the purpose of the computational pipeline is to estimate . The case of multiple principal QoI is a simple extension not described herein. Nodes with no immediate children are called terminal nodes, while nodes with no immediate parents are called source nodes. We denote by the set of all source nodes.

Definition 5.1** (Pipeline).**

A pipeline is a directed acyclic graph defined as follows:

- •

Nodes are of two kinds: Information nodes are depicted by , and method nodes are depicted by .

- •

The graph is bipartite, so that edges connect a method node to an information node or vice-versa. That is, edges are of the form or .

- •

There are method nodes, each with a unique label in .

- •

The method node labelled has parents and one child. Its in-edges are assigned a unique label in .

- •

There is a unique terminal node and it is the child of method node . This represents the principal QoI .

Example 5.2** (Distributed Integration).**

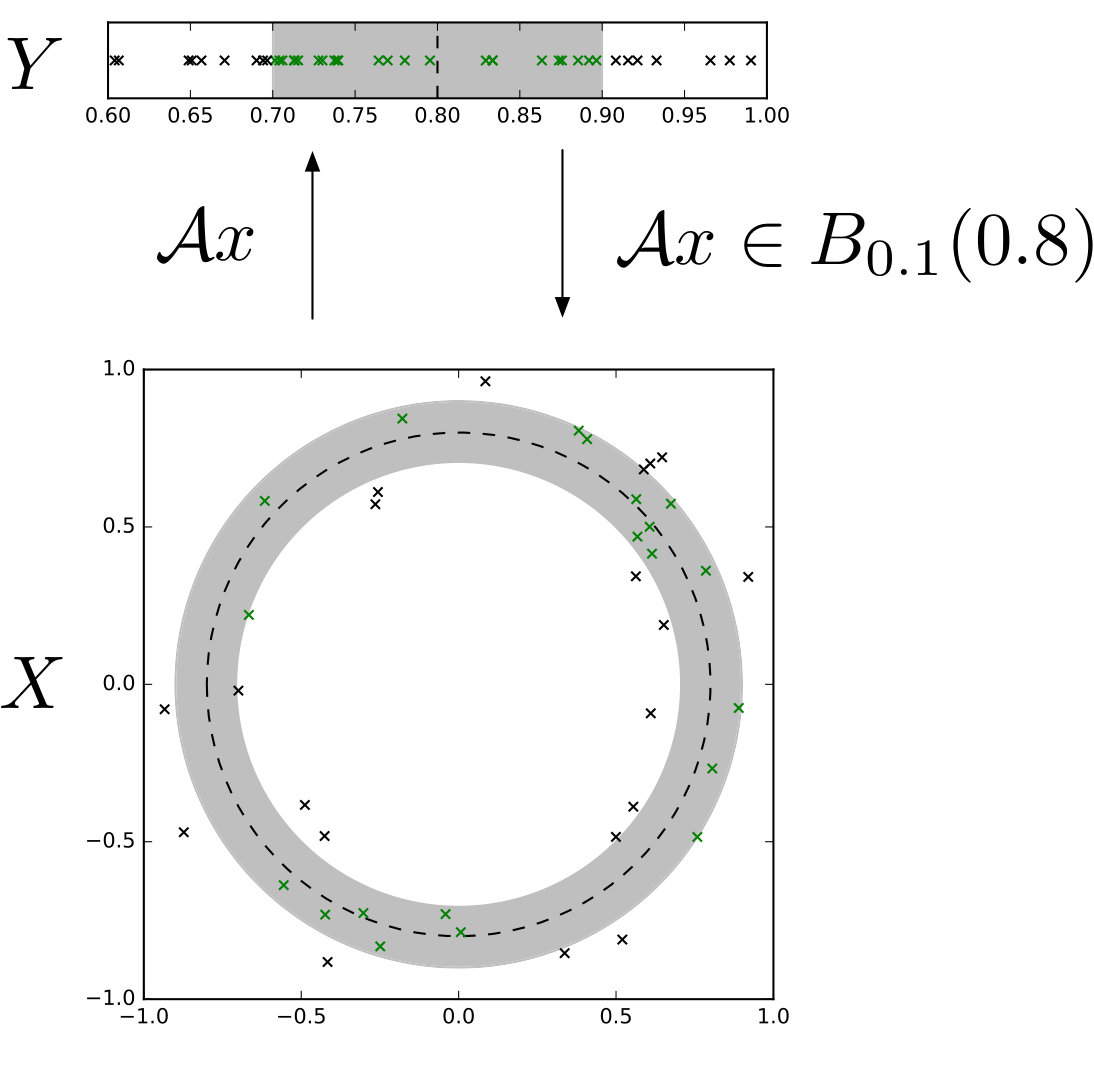

Recall the numerical integration problem of Example 3.4 and, as a thought experiment, consider partitioning the domain of integration in order to distribute computation:

[TABLE]

To keep presentation simple we consider an integral over with equidistant knots . Let be a Bayesian PNM for estimating (a) and be a Bayesian PNM for estimating (b).

In terms of our notational convention, we divide the information operator into four components; , for . and contain the information unique to and . Specifically

[TABLE]

and contain the information that is shared between the two methods; that is . To complete the specification we need a third PNM for estimation of (c) which we denote and which combines the outputs of and by simply adding them together. Formally this has information operator where (a) and (b). Its belief update operator is given by:

[TABLE]

An intuitive graphical representation of this set-up is shown in Figure 1. The pipeline itself, which is identical to Figure 1 but with additional node and edge labels, is shown in Figure 2.

In general, the method node labelled is taken to represent the method . The in-edge to this node labelled is taken to represent the information provided by the relationship . Here can either be deterministic information provided to the pipeline, or statistical information derived from the output of another PNM. To make this formal and to “match the input-output spaces” we next define what it means for the collection of methods to be compatible with the pipeline . Informally, this describes the conditions that must be satisfied for method nodes in a pipeline to be able to connect to each other.

Definition 5.3** (Compatible).**

The collection of PNMs is compatible with the pipeline if the following two requirements are satisfied:

- (i)

(Method nodes which share an information node must have consistent information spaces and information operators.) For a motif

i$$j$$i^{\prime}$$j^{\prime}

we have that and . 2. (ii)

(The space for the output of a previous method must be consistent with the information space of the next method.) For a motif

i$$j$$j^{\prime}

we have that .

Note that we do not require the converse of (i) at this stage; that is, the same information can be represented by more than one node in the pipeline. This permits redundancy in the pipeline, in that information is not recycled. It will transpire that pipelines with such redundancy are non-Bayesian.

The role of the pipeline is to specify the order in which information, either deterministic of statistical, is propagated through the collection of PNMs. This is illustrated next:

Example 5.4** (Propagation of Information).**

For the pipeline in Figure 2, the propagation of information proceeds as follows::

The source nodes, representing are evaluated as . This represents all the information on that is provided. 2. 2.

The distributions

[TABLE]

are computed. 3. 3.

The push-forward distribution

[TABLE]

is computed.

Here is defined on the Cartesian product with independent components and . The notation refers to the push-forward of the function over its second argument. The distribution is the output of the pipeline and is a distribution over the principal QoI .

The procedure in Example 5.4 can be formalised, but to keep the presentation and notation succinct, we leave this implicit:

Definition 5.5** (Computation).**

For a collection of PNMs that are compatible with a pipeline , the computation is defined as the PNM with information operator and belief update operator that takes and as input and returns the distribution as its output , obtained through the procedure outlined in Example 5.4.

That is, the computation is a PNM for the principal QoI . Note that this definition includes a classical numerical work-flow just as a PNM encompasses a standard numerical method.

5.2 Bayesian Computational Pipelines

Noting that is itself a PNM, there is a natural definition for when such a computation can be called Bayesian:

Definition 5.6** (Bayesian Computation).**

Denote by the information and belief operators associated with the computation and let be a disintegration of with respect to the information operator . The computation is said to be Bayesian for the QoI if

[TABLE]

This is clearly an appealing property; the output of a Bayesian computation can be interpreted as a posterior distribution over the QoI given the prior and the information . Or, more informally, the “pipeline is lossless with information”. However, at face value it seems difficult to verify whether a given computation is Bayesian, since it depends on both the individual PNMs and the pipeline that combines them. Our next aim is to establish verifiable sufficient conditions, for which we require another definition:

Definition 5.7** (Dependence Graph).**

The dependence graph of a pipeline is the directed acyclic graph obtained by taking the pipeline , removing the method nodes and replacing all motifs with direct edges .

The dependency graph for Example 5.2 is shown in Figure 3.

For a computation , each of the distinct nodes in can be associated with a random variable where either for some , when the node is a source, or otherwise , for some . Randomness here is understood to be due to , so that the distribution of the is a function of . The convention used here is that the are indexed according to a topological ordering on , which has the properties that (i) the source nodes correspond to indices , and (ii) the final random variable is .

Definition 5.8** (Coherence).**

Consider a computation . Denote by the parent set of node in the dependence graph . Then we say that is coherent for the computation if the implied joint distribution of the random variables satisfies:

[TABLE]

for all .

Note that this is weaker than the Markov condition for directed acyclic graphs (see Lauritzen, 1991), since we do not insist that the variables represented by the source nodes are independent. It is emphasised that, for a given , the coherence condition can in general be checked and verified.

The following result provides sufficient and verifiable conditions which ensure that a computation composed of individual Bayesian PNMs is a Bayesian computation:

Theorem 5.9**.**

Let be Bayesian PNMs and let be coherent for the computation . Then it holds that the computation is Bayesian for the QoI .

Conversely, if non-Bayesian PNM are combined then the computation need not be Bayesian in general.

Example 5.10** (Example 5.2, continued).**

The random variables in this example are:

[TABLE]

From in Figure 3, coherence condition in Definition 5.8 requires that the non-trivial conditional independences and hold. Thus the distribution is coherent for the computation if and only if, for , the associated information variables satisfy and .

The distribution induced by the Weiner process on in Example 3.4 satisfies these conditions. Indeed, under the stochastic process is conditionally independent of its history given the current state . Thus for this choice of , from Theorem 5.9 we have that is Bayesian and parallel computation of and in Eq. (5.1) can be justified from a Bayesian statistical standpoint.

However, for the alternative of belief distributions induced by the Weiner process on , this condition is not satisfied and the computation is not Bayesian. To turn this into a Bayesian procedure for these alternative belief distributions it would be required that provides information about the derivatives for all orders .

5.3 Monte Carlo Methods for Probabilistic Computation

The most direct approach to access is to sample from each Bayesian PNM and treat the output samples as inputs to subsequent PNM. This is sometimes known as ancestral sampling in the Bayesian network literature (e.g. Paige and Wood, 2015), and is illustrated in the following example:

Example 5.11** (Ancestral Sampling for PNM).**

For Example 5.2, ancestral sampling proceeds as follows:

Draw initial samples

[TABLE] 2. 2.

Draw a final sample

[TABLE]

Then is a draw from .

Ancestral sampling requires that PNM outputs can be sampled. Such sampling methods were discussed in Section 4.3. For a more general approach, sequential Monte Carlo methods can be used to propagate a collection of particles through the pipeline , similar to work on SMC for general graphical models (Briers et al., 2005; Ihler and McAllester, 2009; Lienart et al., 2015; Lindsten et al., 2017; Paige and Wood, 2015).

6 Numerical Experiments

In this final section of the paper we present three numerical experiments. The first is a linear PDE, the second is a nonlinear ODE and the third is an application to a problem in industrial process monitoring, described by a pipeline of PNM. In each case we experiment with non-Gaussian belief distributions and, in doing so, go beyond previous work.

6.1 Poisson Equation

Our first illustration is an instance of the Poisson equation, a linear PDE with mixed Dirichlet-Neumann boundary conditions:

[TABLE]

A model solution to this system, generated with a finite-element method on a fine mesh, is shown in Figure 4.

As the spatial domain for this problem is two-dimensional, the basis used for specification of the belief distribution is more complex. Here tensor products of orthogonal polynomials have been used: , . The polynomials were chosen to be normalised Chebyshev polynomials of the first kind. Prior specification then follows the formulation given in Section 2.6, where the remaining parameters were chosen to be , and . The random variables were taken to be either Gaussian or Cauchy and the polynomial basis was truncated to terms, corresponding to a maximum polynomial degree of . For both priors the parameter was set to . Note that closed-form expressions are available for analysis under the Gaussian prior (Cockayne et al., 2016) but, to simplify interpretation of empirical results, were not exploited. Mathematical background on Cauchy priors can be found in Sullivan (2016).

The information operator was defined by a set of locations , , where either the interior condition or one of the boundary conditions was enforced. Denote by the set of interior points, the set of Dirichlet boundary points and the set of Neumann boundary points, where , and , with . Then, the information operator is given by the concatenation of the conditions defined above:

[TABLE]

[TABLE]

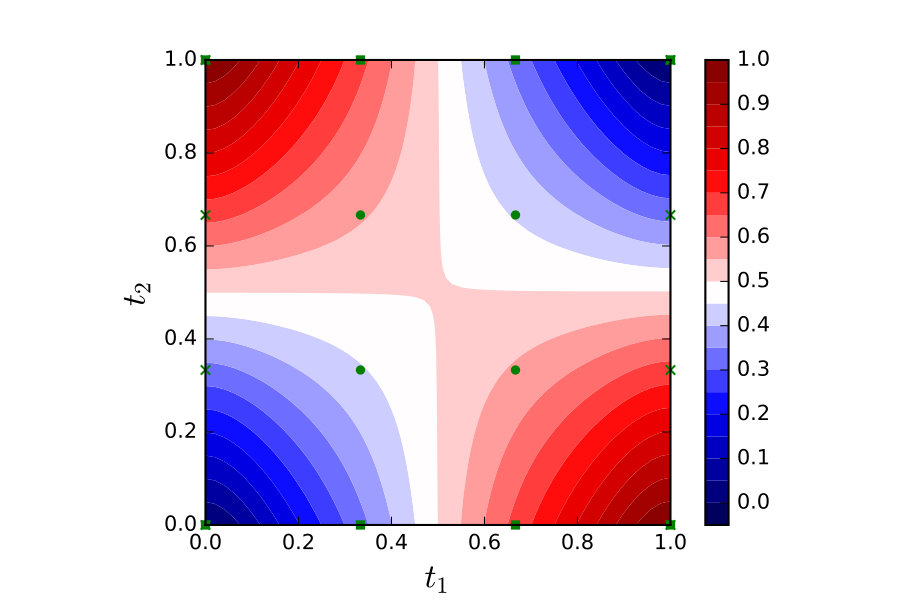

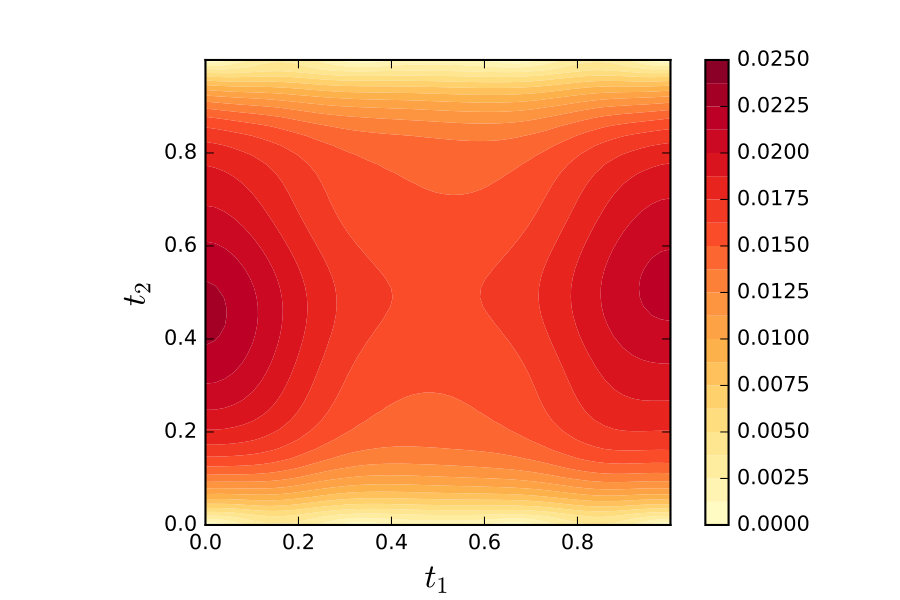

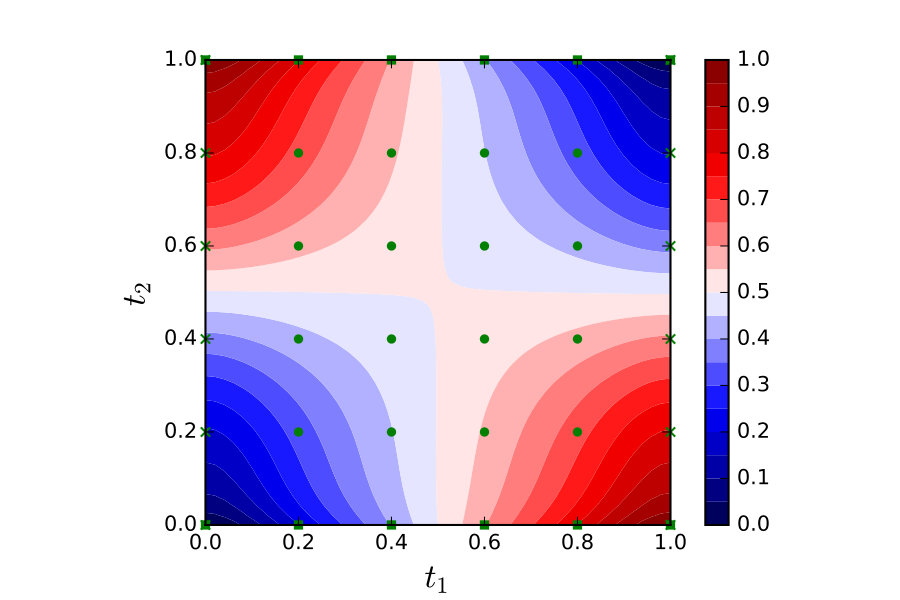

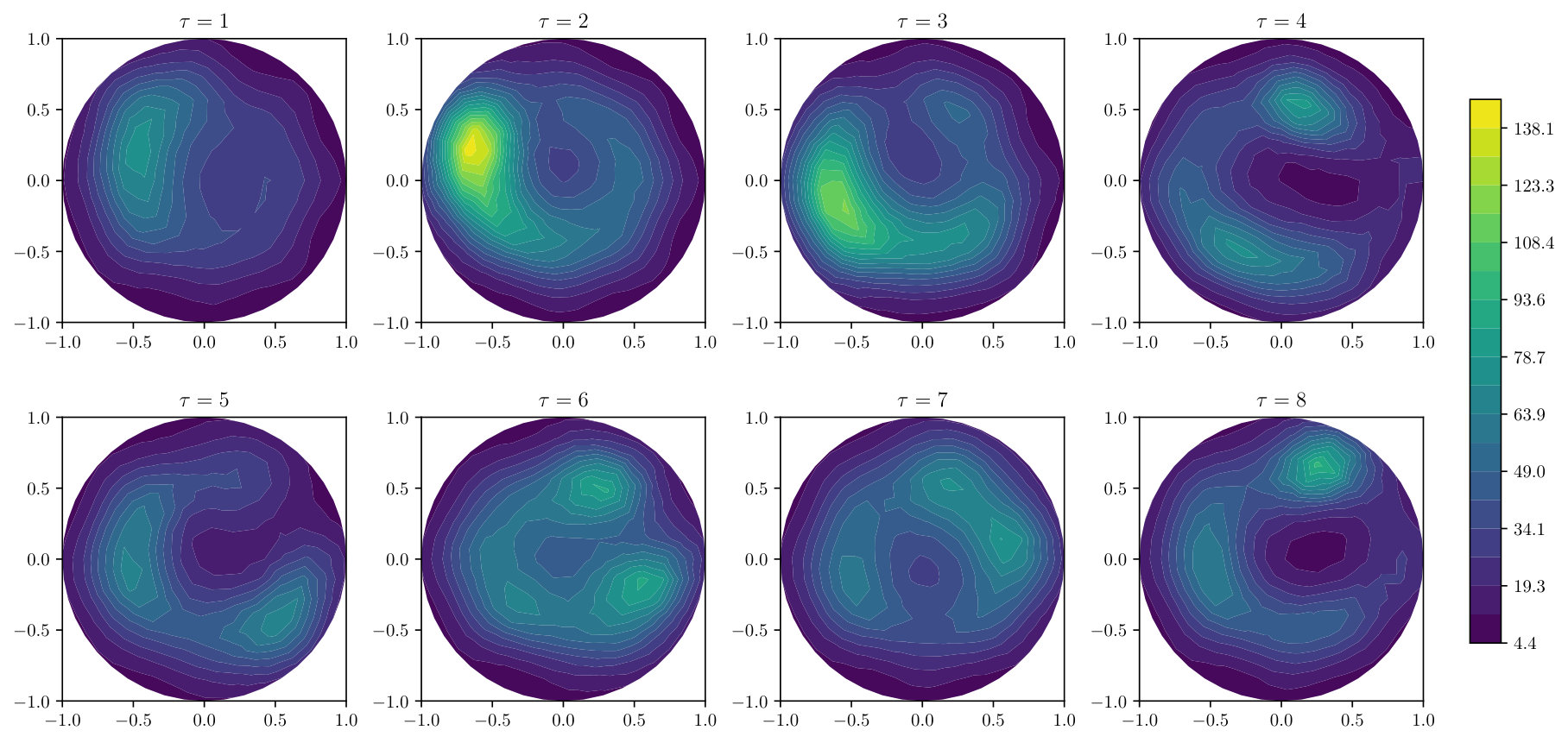

The Bayesian PNM output was approximated by numerical disintegration and sampled with a Monte Carlo method whose description is reserved for the Electronic Supplement. In Figure 5 the mean and pointwise standard-deviations of the posterior distributions are plotted for Gaussian and Cauchy priors with . There is little qualitative difference between the posterior distributions for the Gaussian and Cauchy priors. The mean functions match closely to the mean function from the model solution, as given in Figure 4. The posterior variance is lowest near to the Dirichlet boundaries where the solution is known, and peaks where the Neumann condition is imposed. This is to be expected, as evaluations of the Neumann boundary condition provide less information about the solution itself.

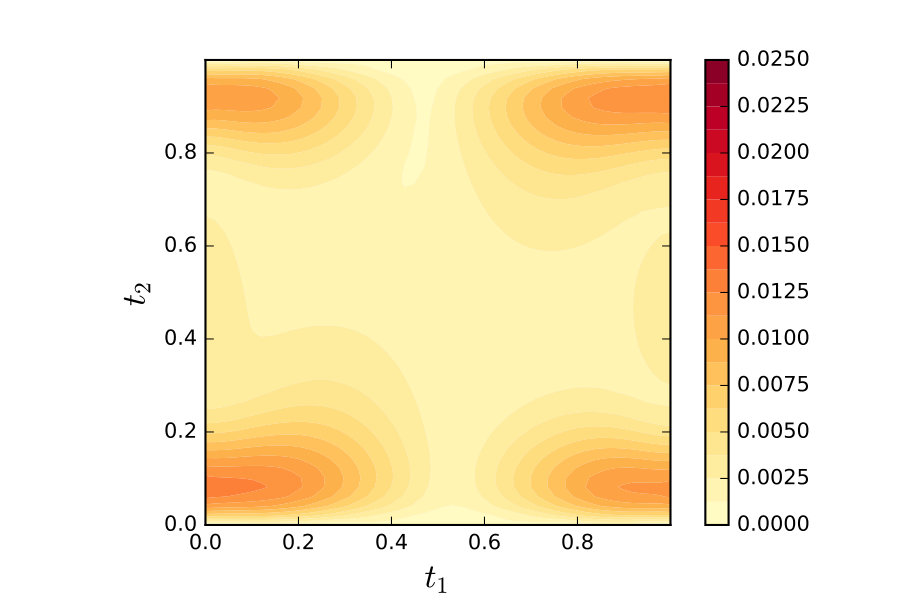

Next, the posterior distribution of the spectrum was investigated. In Figure 6 the posterior distribution over these coefficients is plotted and it is seen that the correlation structure between coefficients is non-trivial, c.f. the joint distribution between and .

Last, in Figure 7 convergence of the posterior distribution is plotted as the number of design points is varied, for . In each case a Gaussian prior was used. As expected, the standard deviation in the posterior distribution is seen to decrease as the number of design points is increased. At , the shape of the region of highest uncertainty changes markedly, with the most uncertain region lying between the Dirichlet boundary and the first evaluation points on the Neumann boundary. This is likely due to the fact that the number of evaluation points is approaching the size of the polynomial basis; when the number of points equals the size of the basis the system is completely determined for a linear model. Thus, we need in order for discretisation error to be quantified.

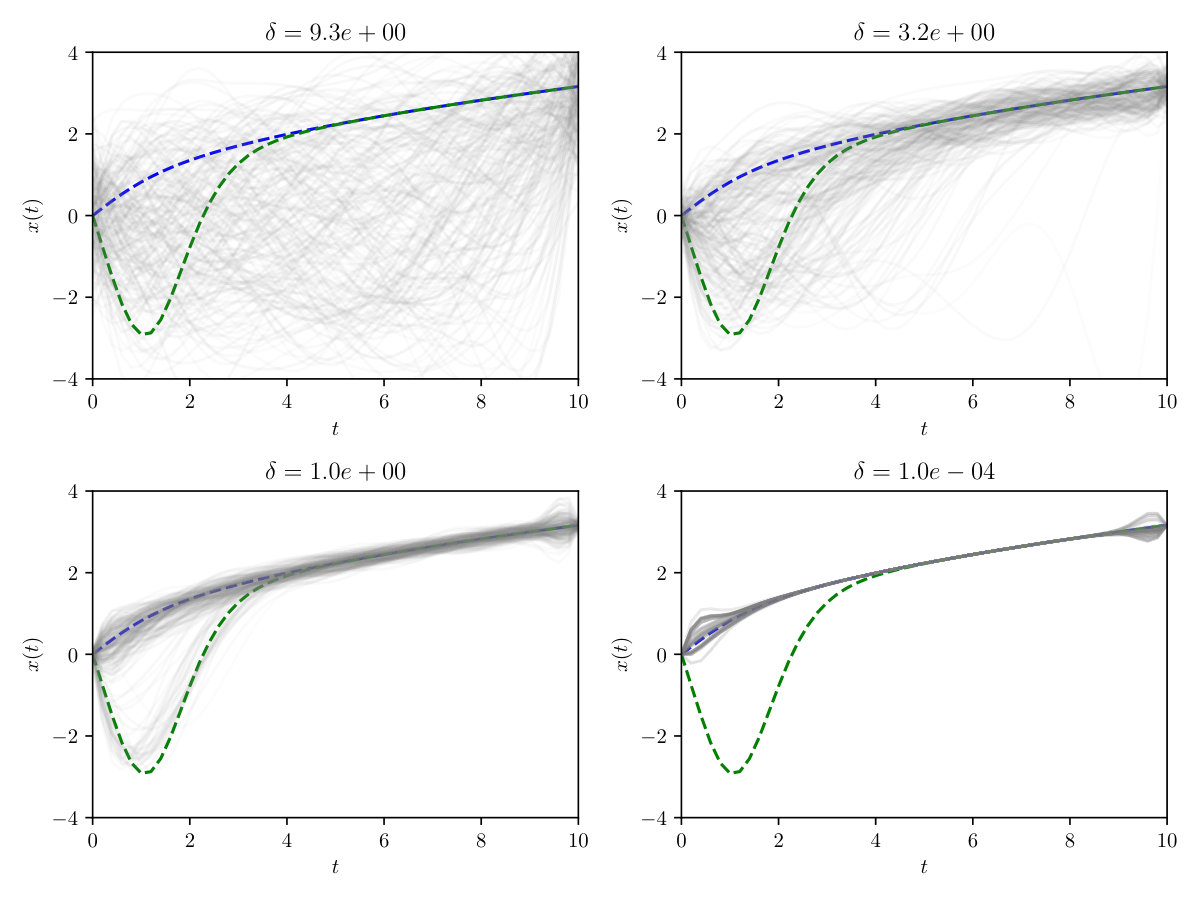

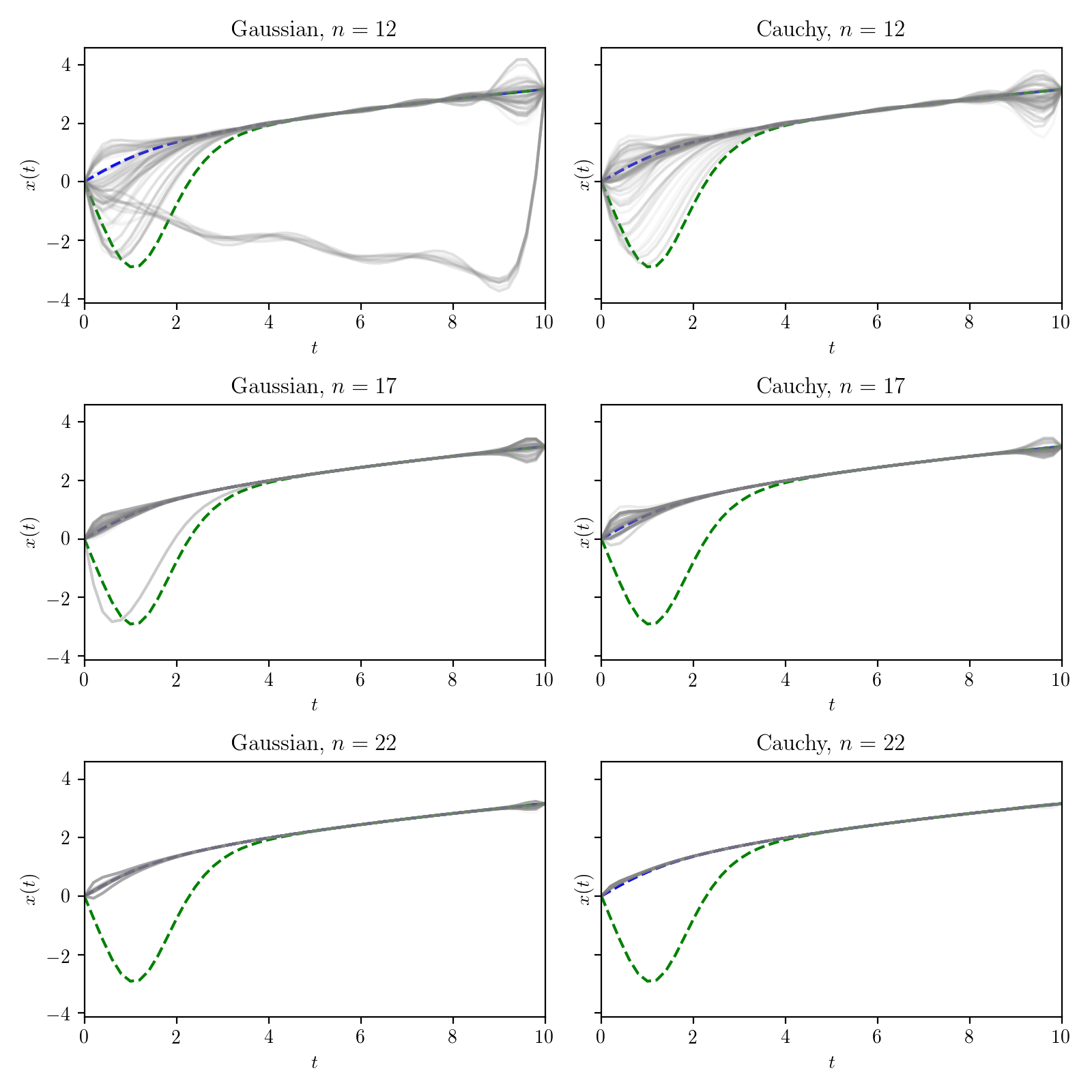

6.2 The Painlevé ODE

In this section a Bayesian PNM is developed to solve a nonlinear ODE based on Painlevé’s first transcendental

[TABLE]

To permit computation, the right-boundary condition was relaxed by truncating the domain to and using the modified condition .

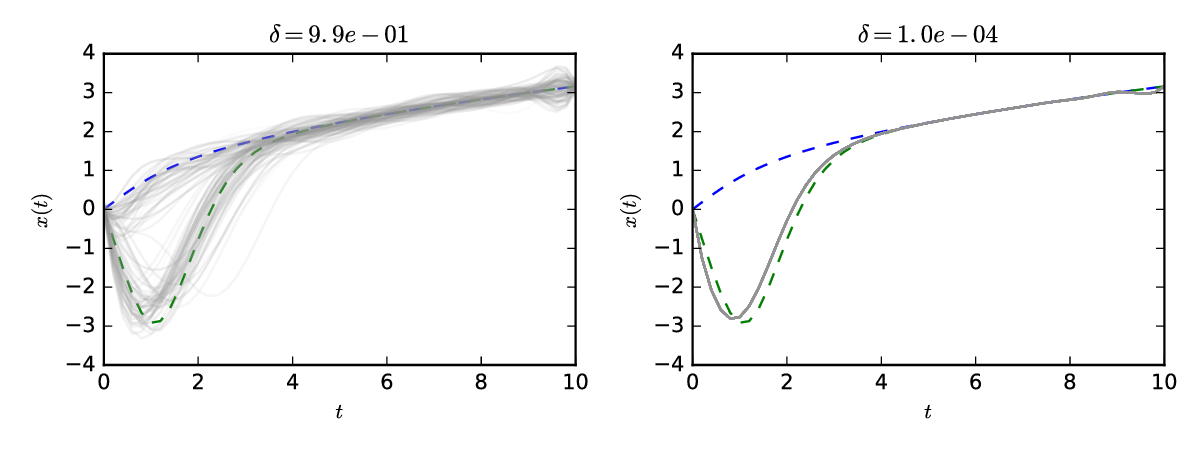

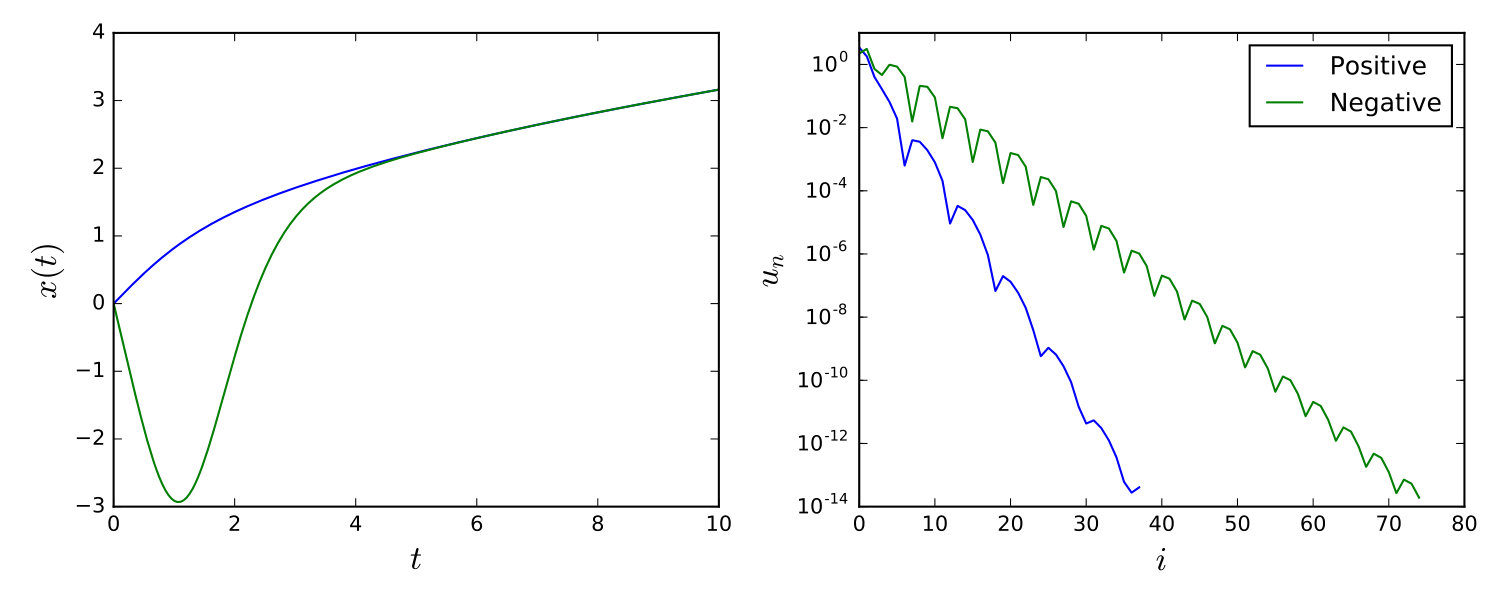

Two distinct solutions are known, illustrated in Figure 8 (left). These model solutions were obtained using the deflation technique described in Farrell et al. (2015). The spectrum plot in Figure 8 (right) represents the coefficients obtained when each solution is represented over a basis of normalised Chebyshev polynomials. As those polynomials are orthonormal with respect to the -inner-product, the slower decay for the negative solution compared to the positive solution is equivalent to the negative solution having a larger -norm. This explains the preference that optimisation-based numerical solvers have for returning the positive solution in general, and also explains some of the results now presented.

Such systems for which multiple solutions exist have been studied before in the context of PNM, both in Chkrebtii et al. (2016) and in Cockayne et al. (2016). It was noted in both papers that existence of multiple solutions can present a substantial challenge to classical numerical methods.

To build a Bayesian PNM, a prior for this problem was defined by using a series expansion as in Eq. (2.6). The basis functions were where the were normalised Chebyshev polynomials of the first kind. Both Gaussian and Cauchy priors were considered by taking , where were taken to be either standard Gaussian or standard Cauchy and in in each case . In accordance with the exponential convergence rate for spectral methods when the solution to the system is a smooth function, the sequence of scale parameters was set to , where and . These values were chosen by inspection of the true spectra (obtained with Matlab’s “chebfun” package) to ensure that both solutions were in the support of the prior.

The information operator was defined by the choice of locations , , which determine the locations at which the posterior will be constrained. Analysis for several values of was performed. In each case , and the remaining were equally spaced on . To be explicit, the information operator was

[TABLE]

with the last two elements enforcing the boundary conditions. Thus our information was , which is dimensional.

The Bayesian PNM output was approximated via numerical disintegration with the first terms of the series representation used. This was sampled with Monte Carlo methods, the details of which are reserved for the Electronic Supplement.

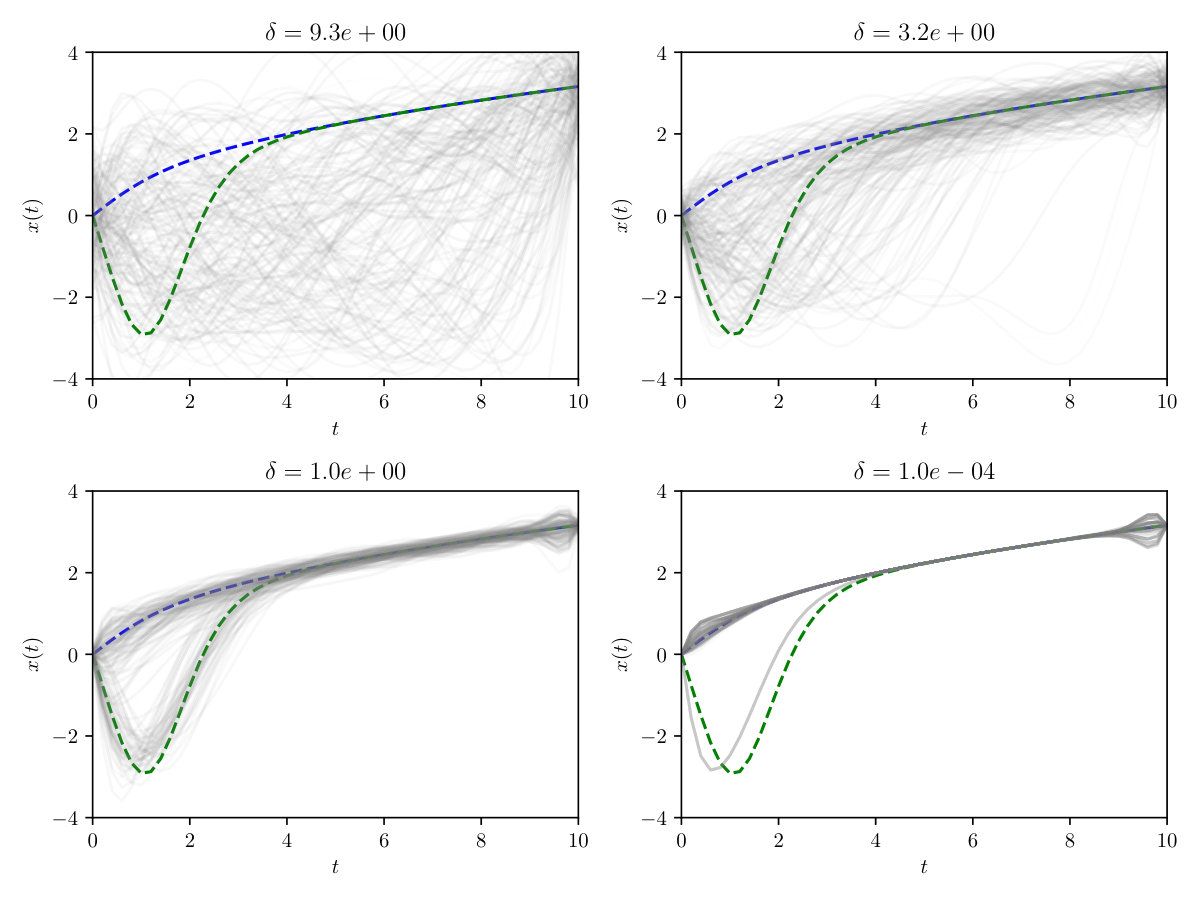

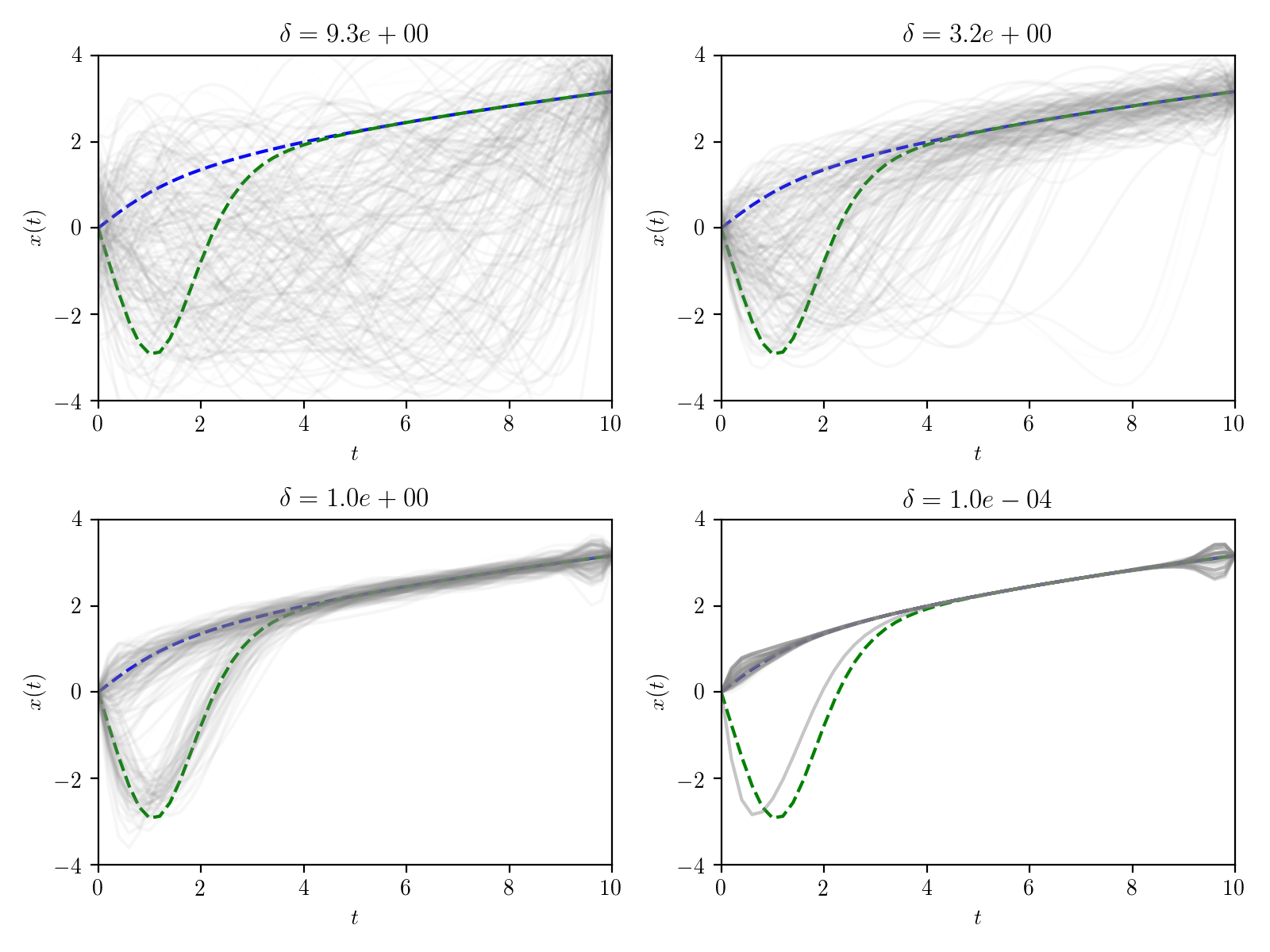

Results for a selection of bandwidths , with , are shown in Figure 9. Note that a strong preference for the positive solution is expressed at the smallest , with mass around both solutions at larger . For the Gaussian prior, some mass remained around the negative solution at the smallest , while this was not so for the Cauchy prior. This reflects the fact that, for a collection of independent univariate Cauchy random variables, one element is likely to be significantly larger in magnitude than the others, which favours faster decay for the remaining elements.

Using the calculation described in Section S4.4, model evidence was computed for both the Gaussian and the Cauchy prior at . The Bayes factor for the Cauchy, compared to the Gaussian prior, was found to be , which constitutes strong evidence in favour of a Cauchy prior for this problem at the given level of discretisation.

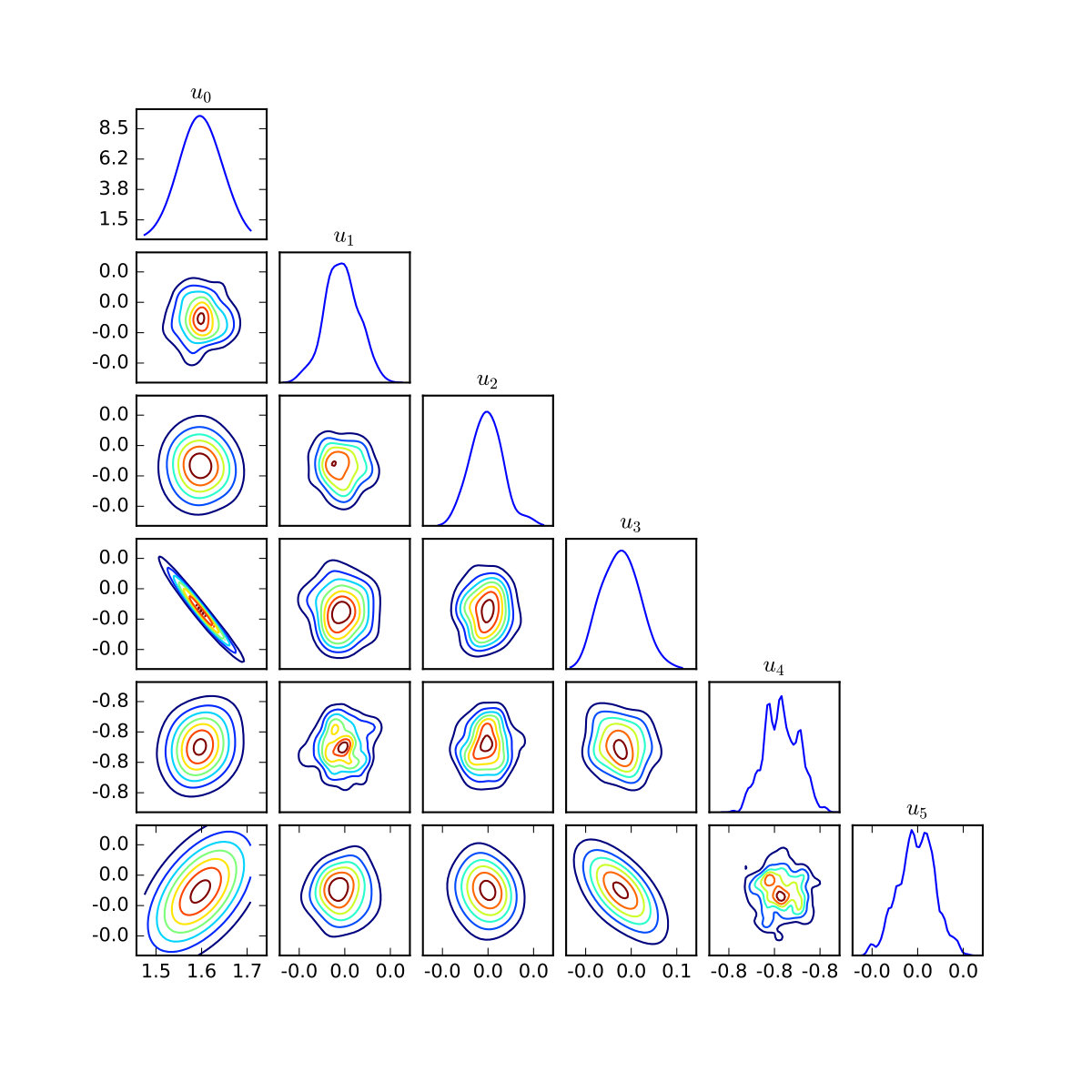

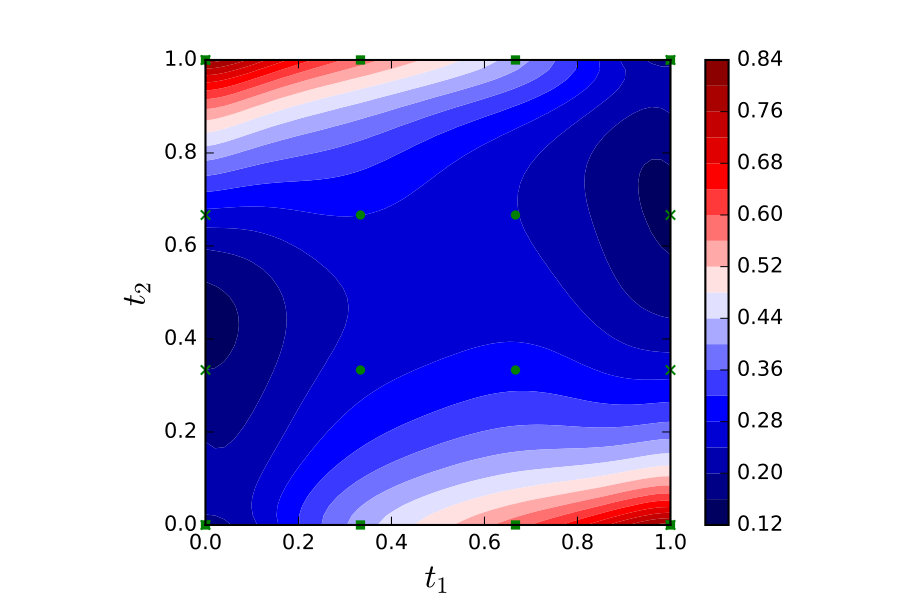

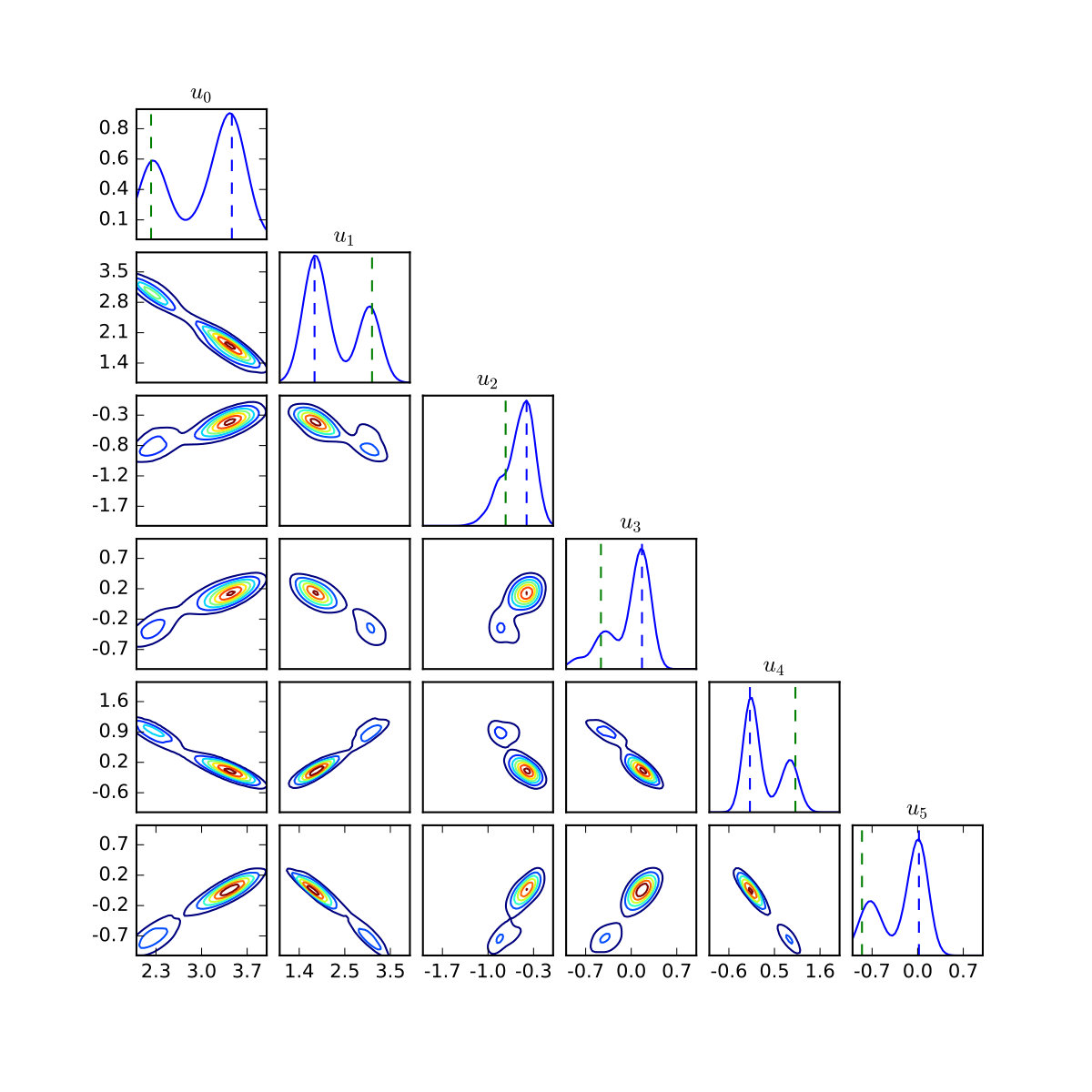

In Figure 10 the posterior distributions for first six coefficients at and are plotted. Strong multimodality is clear, as well as skewed correlation structure between the coefficients. Illustration of such posteriors for smaller is difficult as the posteriors become extremely peaked.

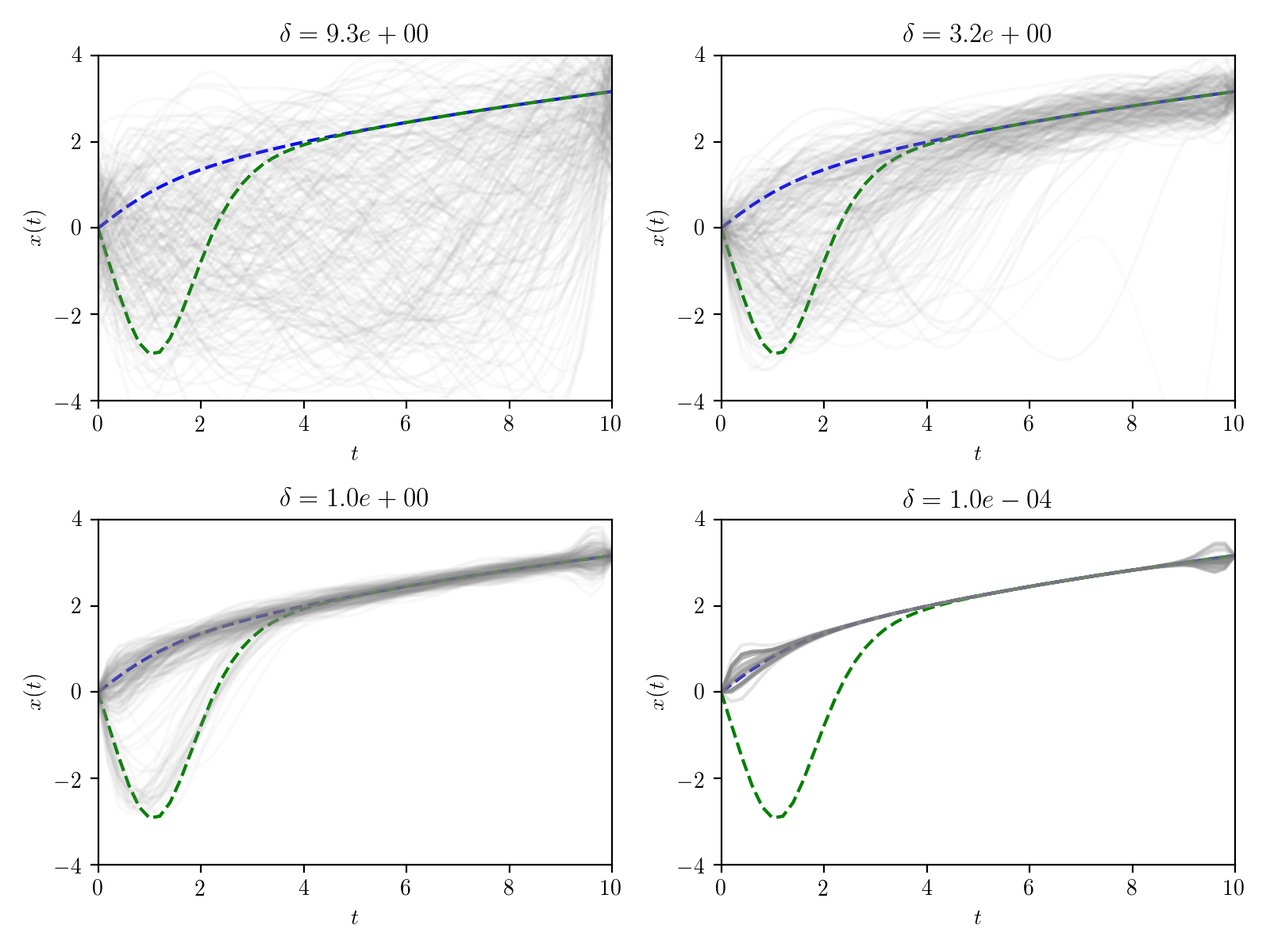

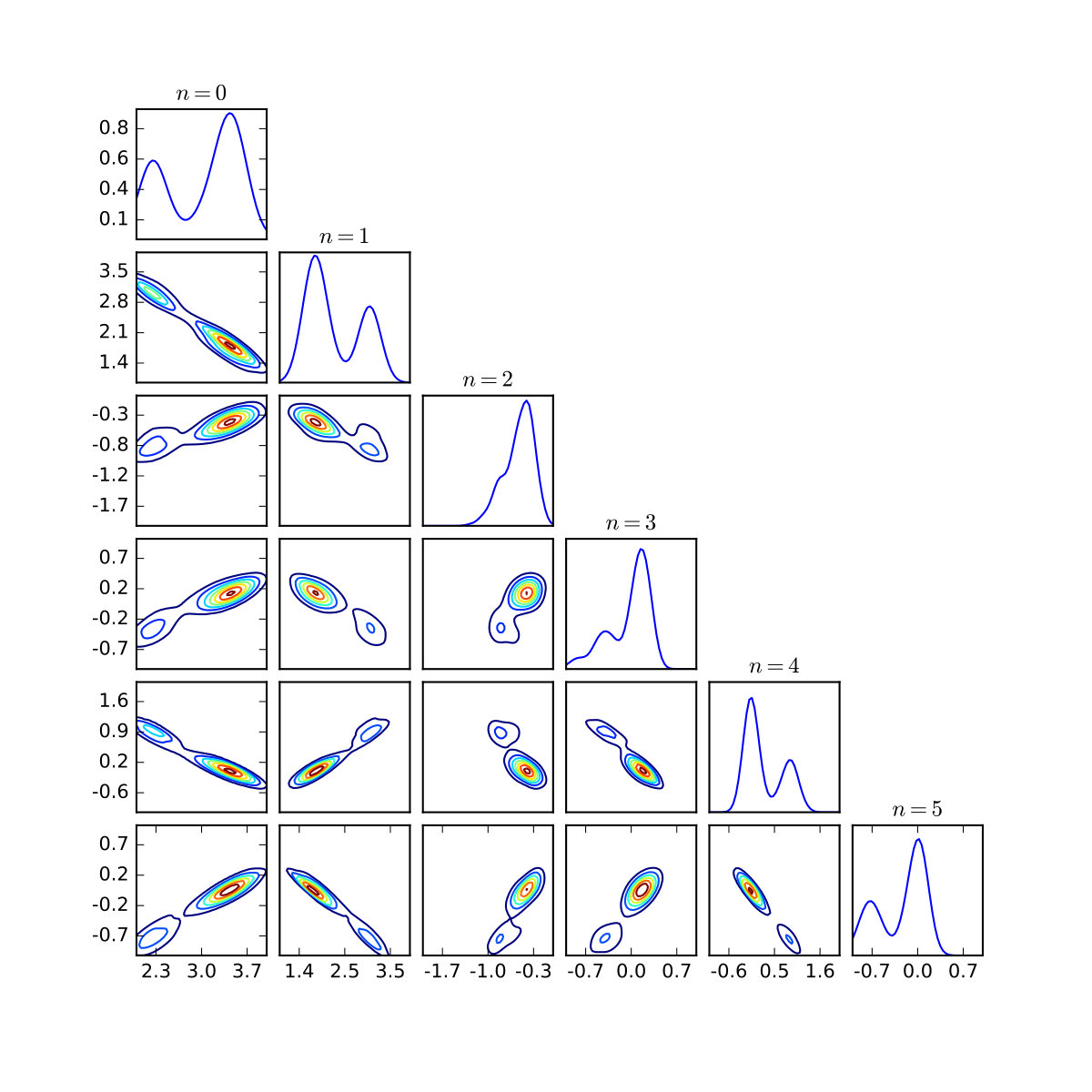

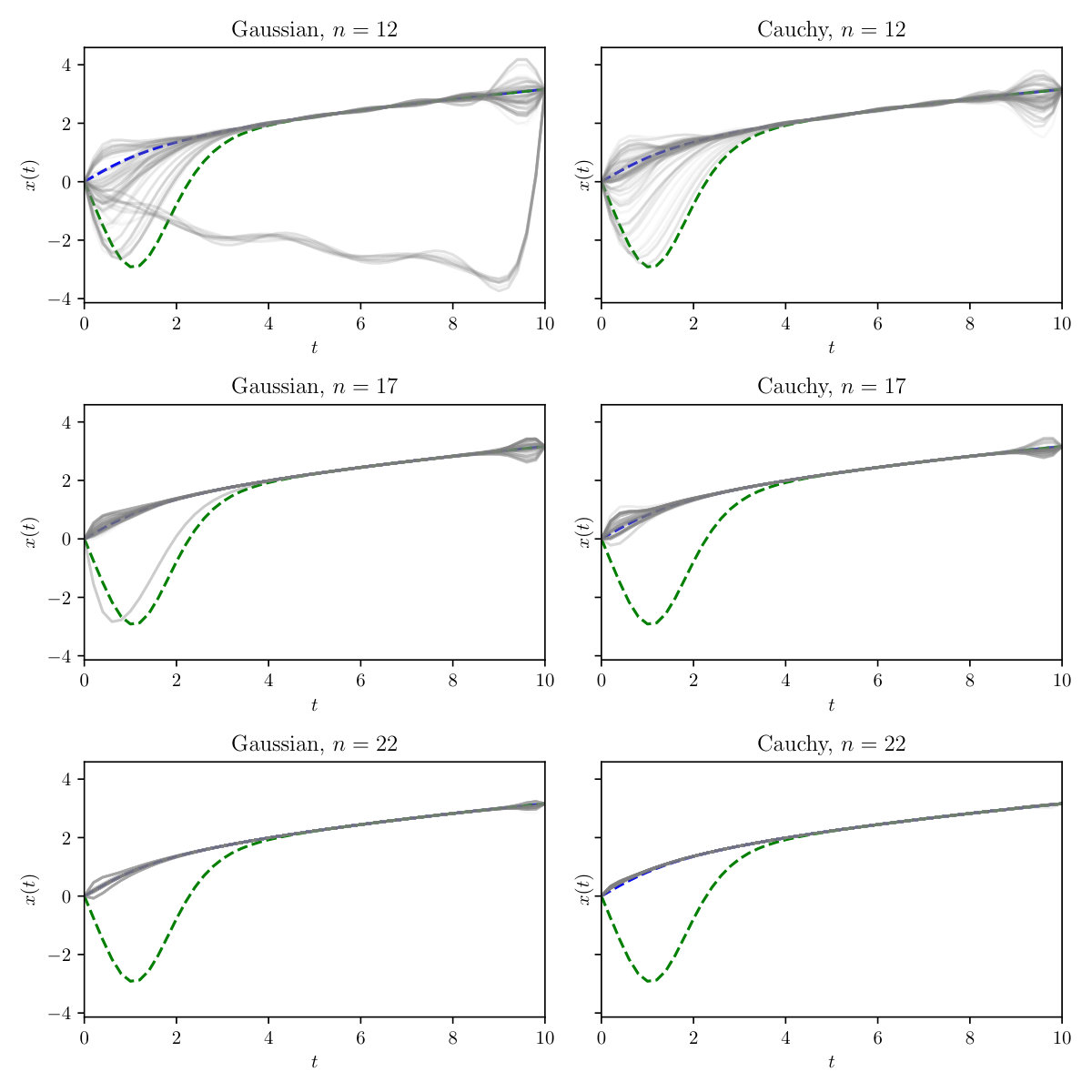

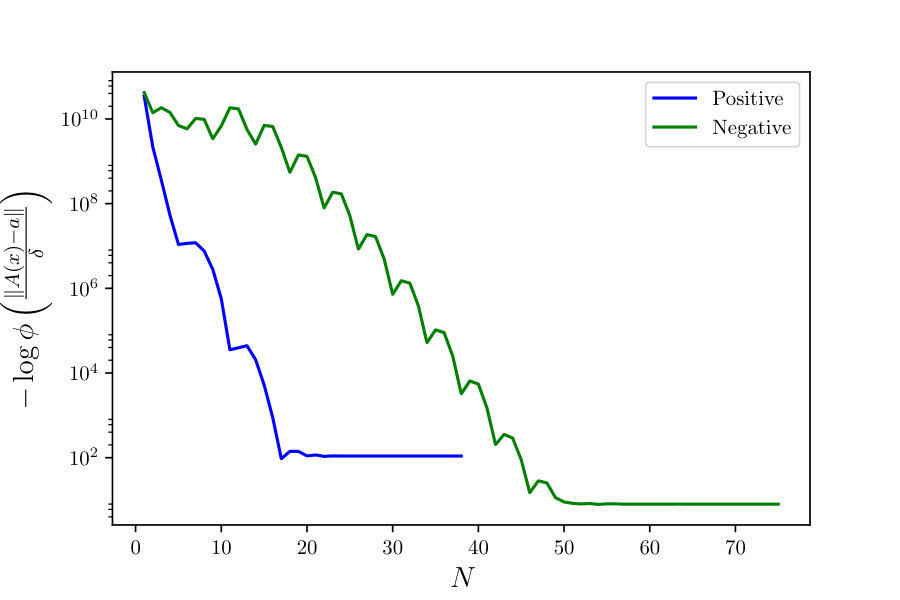

Figure 11 displays convergence of the posterior distributions as is increased. Of particular interest is that for , the posterior distribution based on a Gaussian prior becomes trimodal. For each prior, the posterior mass settles on the positive solution to the system at . This is in accordance with the fact that this solution has smaller -norm. This perhaps reflects the fact that, while in the limiting case both solutions should have an equal likelihood, the curvature of the likelihood at each mode may differ. Prior truncation may also be influential; in Figure 12 the log-likelihood of the negative solution increases at a slower rate than that of the positive solution. Thus, while in the setting of an infinite prior series neither solution should be preferred, in practice truncation might bias one solution over the other. Lastly, it is clear that the parameters and may also have a significant effect on which solution is preferred. Further theoretical work will be required to understand many of the phenomena that we have just described.

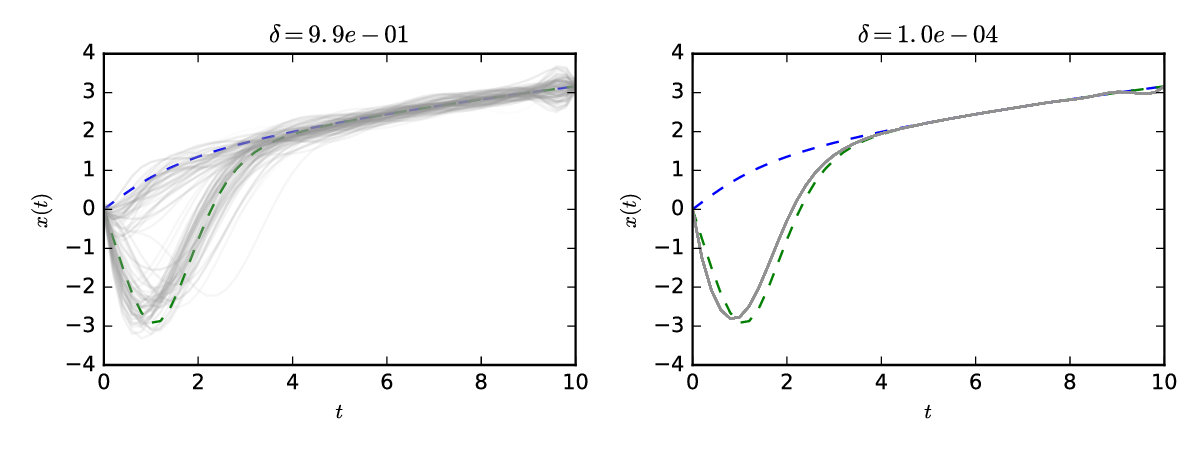

Of particular interest is how a preference for the negative solution could be encoded into a PNM. Owing to the flexible specification the information operator, there is considerable choice in this matter. An elegant approach is the introduction of additional, inequality-based information

[TABLE]

Such information can be difficult to incorporate in standard numerical algorithms, but is of interest in many physical problems (Kinderlehrer and Stampacchia, 2000). For Bayesian PNM we can extend the information operator to include . Posterior distributions for the Gaussian prior at are shown in Figure 13. Note that posterior mass has settled close to the negative solution. This highlights the simplicity with which Bayesian PNMs can encode a preference for a particular solution when a multiplicity of solutions exist.

6.3 Application to Industrial Process Monitoring

This final application illustrates how statistical models for discretisation error can be propagated through a pipeline of computation to model how these errors are accumulated.

Hydrocyclones are machines used to separate solid particles from a liquid in which they are suspended, or two liquids of different densities, using centrifugal forces. High pressure fluid is injected into the top of a tank to create a vortex. The induced centrifugal force causes denser material to move to the wall of the tank while lighter material concentrates in the centre, where it can be extracted. They have widespread applications, including in areas such as environmental engineering and the petrochemical industry (Sripriya et al., 2007). An illustration of the operation is given in Figure 14.

To ensure the materials are well-separated the hydrocyclone must be moitored to allow adjustment of the input flow-rate. This is also important for safe operation, owing to the high pressures involved (Bradley, 2013). However, direct monitoring is impossible owing to the opaque walls of the equipment and the high interior pressure. For this purpose electrical impedance tomography (EIT) has been proposed to allow monitoring of the contents (Gutierrez et al., 2000).

EIT is a technique which allows recovery of an interior conductivity field based upon measurements of voltage obtained from applying a stimulating current on the boundary. It is suited to this problem, as the two materials in the hydrocyclone will generally be of different conductivities. In its simplified form due to Calderón (1980), EIT is described by a linear partial differential equation similar to that in Section 6.1, but with modified boundary conditions to incorporate the stimulating currents and measured voltages:

[TABLE]

where denotes the domain, modelling the hydrocyclone tank, indexes the stimulating electrodes, are the corresponding locations of the electrodes on , is the unknown conductivity field to be determined and denotes the derivative with respect to the outward pointing normal vector. The electrode is referred to as the reference electrode. The vector denotes the stimulation current pattern. Several stimulation patterns were considered, denoted , .

The experimental data described in West et al. (2005) were considered. In the experiment, a cylindrical perspex tank was used with a single ring of eight electrodes. Translation invariance in the vertical direction means that the contents are effectively a single 2D region and electrical conductivity can be modelled as a 2D field. At the start of the experiment, a mixing impeller was used to create a rotational flow. This was then removed and, after a few seconds, concentrated potassium chloride solution was carefully injected into the tap water initially filling the tank. Data, denoted , were collected at regular time intervals by application of several stimulation patterns .

To formulate the statistical problem, consider parameterising the conductivity field as , where is a temporal index while is the spatial coordinate and is the circular domain representing the perspex tank in the experiment. A log-Gaussian prior was placed over the conductivity field so that is a Gaussian process with separable covariance function where is a length-scale parameter representing the anticipated spatial variation of the conductivity field and is a parameter controlling the amplitude of the field. Here was fixed to , while . The problem of estimating based on data can be well-posed in the Bayesian framework (Dunlop and Stuart, 2016). Full details of this experiment can be found in the accompanying report Oates et al. (2017).

Our aim is to use a PNM to account for the effect of discretisation on inferences that are made on the conductivity field. For fixed , a Gaussian prior was posited for , with covariance where was fixed to . The associated Bayesian PNM, a probabilistic meshless method (PMM), was described in Example 2.4.

The statistical inference procedure is formulated in a pipeline of computations in Figure 15. It is assumed that the desired outcome is to monitor the contents of the tank while the current contents are being mixed. This suggests a particle filter approach where a PMM is employed to handle the intractable likelihood that involves the exact solution of a PDE. The distribution of given is denoted an the computation is Bayesian only if the particle approximation error due to the use of a particle filter is overlooked.

To briefly illustrate the method, Figure 16 presents posterior means for the field , for each post-injection time point . These are based on a particle approximation of size , with method nodes based upon a Bayesian PNM, as in Example 2.4, with design points. The high conductivity region representing the potassium chloride solution can be seen rotating through the domain in the frames after injection, with its conductivity reducing as it mixes with the water. The full posterior distribution over the conductivity field is inflated as a result of explicitly modelling the discretisation error; an extensive analysis of these results will be reported in the upcoming Oates et al. (2017).

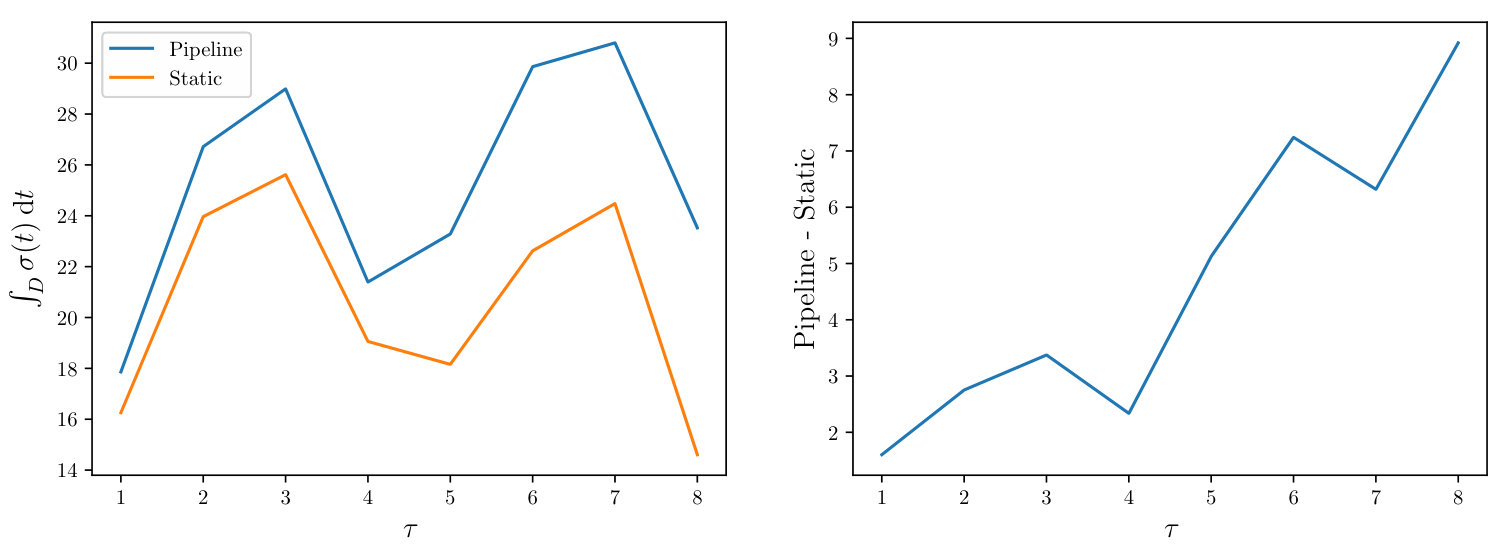

In Figure 17, the integrated standard-deviation is shown for for both the “pipeline”, as described above, and a “static” approach in which no uncertainty was propagated. In this static approach a symmetric collocation PDE solver131313Recall that the PMM has a corresponding symmetric collocation solution to the PDE as its mean function. was used to solve the forward problem, and a separate Bayesian inversion problem was solved at each time point. The parameters of the symmetric collocation solver were identical to those used in the PMM. In the left panel we observe some structural periodicity, present in both the pipeline and the static approach. We speculate that this may be due to the rotation of the medium causing the area of high conductivity to periodically reach an area of the domain, relative to the 8 sensors, in which it is particularly easy to recover. With this periodicity subtracted in the right panel, there was a clear increase in posterior uncertainty in the pipeline compared to the static approach, which is depicted. Temporal regularisation would usually be expected to reduce uncertainty; thus, the fact that the overall uncertainty increased with , relative to the static formulation, demonstrates that we have quantified and propagated uncertainty due to successive discretisation of the PDE at each time point.

7 Discussion

This paper has established statistical foundations for PNMs and investigated the Bayesian case in detail. Through connection to Bayesian inverse problems (Stuart, 2010), we have established when Bayesian PNM can be well-defined and when the output can be considered meaningful. The presentation touched on several important issues and a brief discussion of the most salient points is now provided.

Bayesian vs Non-Bayesian PNMs

The decision to focus on Bayesian PNMs was motivated by the observation that the output of a pipeline of PNMs can only be guaranteed to admit a valid Bayesian interpretation if the constituent PNMs are each Bayesian and the prior distribution is coherent. Indeed, Theorem 5.9 demonstrated that prior coherence can be established at a local level, essentially via a local Markov condition, so that Bayesian PNMs provide a extensible modelling framework as required to solve more challenging numerical tasks. These results support a research strategy that focuses on Bayesian PNMs, so that error can be propagated in a manner that is meaningful.

On the other hand, there are pragmatic reasons why either approximations to Bayesian PNMs, or indeed, non-Bayesian PNMs might be useful. The predominant reason would be to circumvent the off-line computational costs that can be associated with Bayesian PNMs, such as the use of numerical disintegration developed in this research. Recent research efforts, such as Schober et al. (2014, 2016) and Kersting and Hennig (2016) for the solution of ODEs, have aimed for computational costs that are competitive with classical methods, at the expense of fully Bayesian estimation for the solution of the ODE. Such methods are of interest as non-Bayesian PNMs, but their role in pipelines of PNMs is unclear. Our contribution serves to make this explicit.

Computational Cost